Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Introduction & Market Context

Voss Veksel- og Landmandsbank ASA (OB:VVL), a Norwegian regional bank currently celebrating its 125th anniversary, released its Q1 2025 interim report on May 14, 2025. The bank, trading at its 52-week high of 368 NOK, demonstrated resilient performance with continued loan and deposit growth despite a modest decline in quarterly profits compared to the same period last year.

The presentation highlighted VVL’s strong capital position and stable business model, with a continued focus on its core retail banking operations while maintaining solid regulatory metrics well above minimum requirements.

Quarterly Performance Highlights

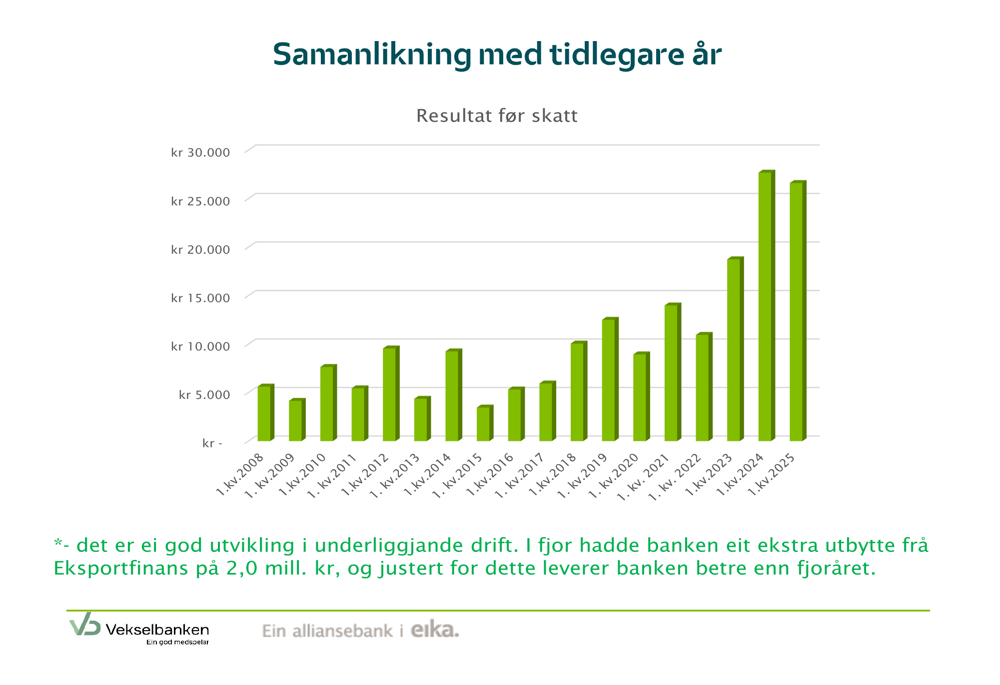

VVL reported a profit before tax of 26.61 million NOK for Q1 2025, representing a slight decrease from 27.68 million NOK in Q1 2024. However, the bank noted that when adjusted for a one-time 2 million NOK dividend received from Eksportfinans in the previous year, the underlying operational performance actually improved year-over-year.

As shown in the following chart of quarterly profit trends, the bank has maintained a generally positive trajectory in its first-quarter results over the past decade:

Net profit after tax reached 19.96 million NOK, down from 20.75 million NOK in Q1 2024, while earnings per share decreased to 8.52 NOK from 8.96 NOK. Despite these modest declines, total comprehensive income improved to 22.59 million NOK from 20.35 million NOK in the comparable period.

The detailed income statement reveals stable net interest income and improved other operating income:

Detailed Financial Analysis

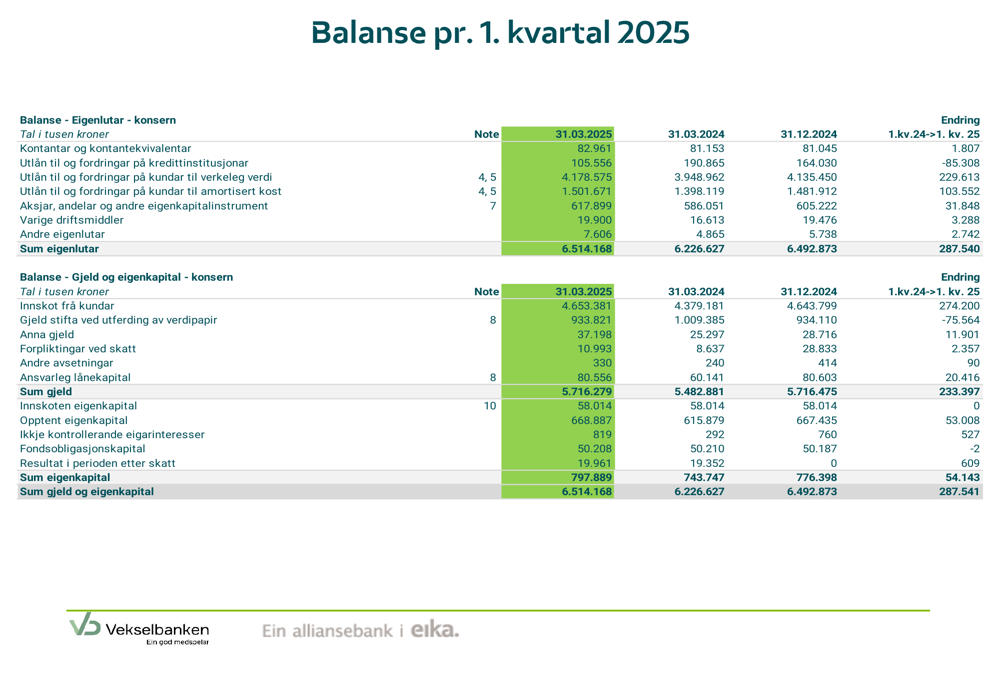

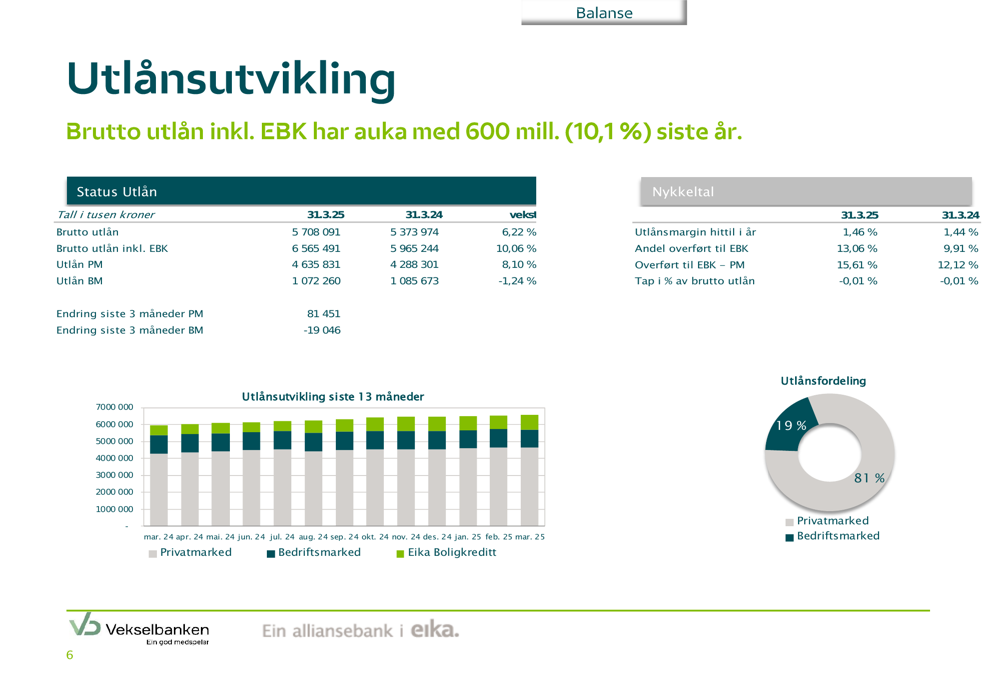

VVL’s balance sheet expanded during the quarter, with total loans increasing 6.22% year-over-year to 6.51 billion NOK. When including loans transferred to Eika Boligkreditt, the bank’s loan growth reached 10.06%, demonstrating strong momentum in its lending activities.

The bank’s balance sheet composition remained healthy with strong growth in both assets and liabilities:

The loan portfolio maintained its retail-focused approach with 81% of loans to private customers and 19% to corporate clients. This composition has remained relatively stable, supporting the bank’s risk management strategy.

The following chart illustrates the development of VVL’s loan portfolio over the past year:

On the funding side, customer deposits grew by 6.26% year-over-year to 4.65 billion NOK, providing a deposit coverage ratio of 81.53%. The deposit base showed a similar composition to the loan portfolio, with 78% from retail customers and 22% from corporate clients.

The deposit development over the past year is illustrated in this chart:

Capital and Liquidity Position

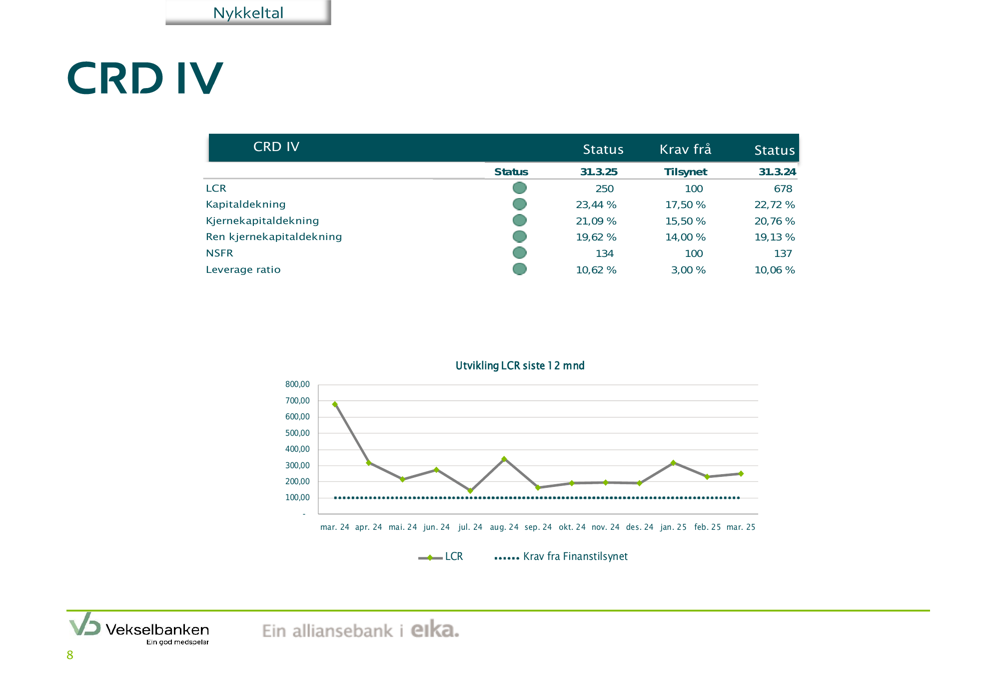

VVL maintained robust capital ratios well above regulatory requirements. The bank’s capital adequacy ratio improved to 23.44% from 22.72% a year earlier, while the CET1 ratio strengthened to 21.09% from 20.76%. These figures significantly exceed the regulatory requirements of 17.50% and 15.50%, respectively.

Liquidity metrics remained strong despite some normalization from exceptionally high levels in the previous year. The Liquidity Coverage Ratio (LCR) stood at 250, down from 678 in Q1 2024 but still well above the regulatory requirement of 100. Similarly, the Net Stable Funding Ratio (NSFR) was 134, slightly below the 137 recorded a year earlier but comfortably exceeding the required minimum of 100.

The bank’s key regulatory metrics are summarized in the following chart:

Forward-Looking Statements

While the presentation did not include explicit forward guidance, VVL’s consistent performance and strong capital position suggest the bank is well-positioned to continue its steady growth trajectory. The bank’s cost-to-income ratio of 40.64% and return on equity of 10.35% demonstrate operational efficiency and profitability that support sustainable performance.

The bank’s focus on retail banking, with over three-quarters of both loans and deposits coming from private customers, provides stability while its strong capital buffers offer protection against potential economic headwinds. With loan losses remaining negative at -0.04% of average gross loans (indicating net recoveries), credit quality appears to remain strong.

As VVL continues to celebrate its 125th anniversary year, the Q1 2025 results demonstrate the resilience of its traditional banking model combined with prudent growth and solid capital management.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.