Piper Sandler lowers Arbor Realty Trust stock price target on credit issues

Introduction & Market Context

Vulcan Materials Company (NYSE:VMC) released its third quarter 2025 supplemental information on October 30, highlighting strong financial performance despite mixed construction market conditions. The nation’s largest producer of construction aggregates reported significant growth in revenue and profitability metrics, though the company’s stock fell 3.38% to $284.65 following the release, suggesting some investor caution despite the positive results.

The presentation, titled "Durable Growth, The Vulcan Way," showcased the company’s strategic positioning in high-growth markets and its operational discipline, which have enabled it to outperform peers across key financial metrics.

Quarterly Performance Highlights

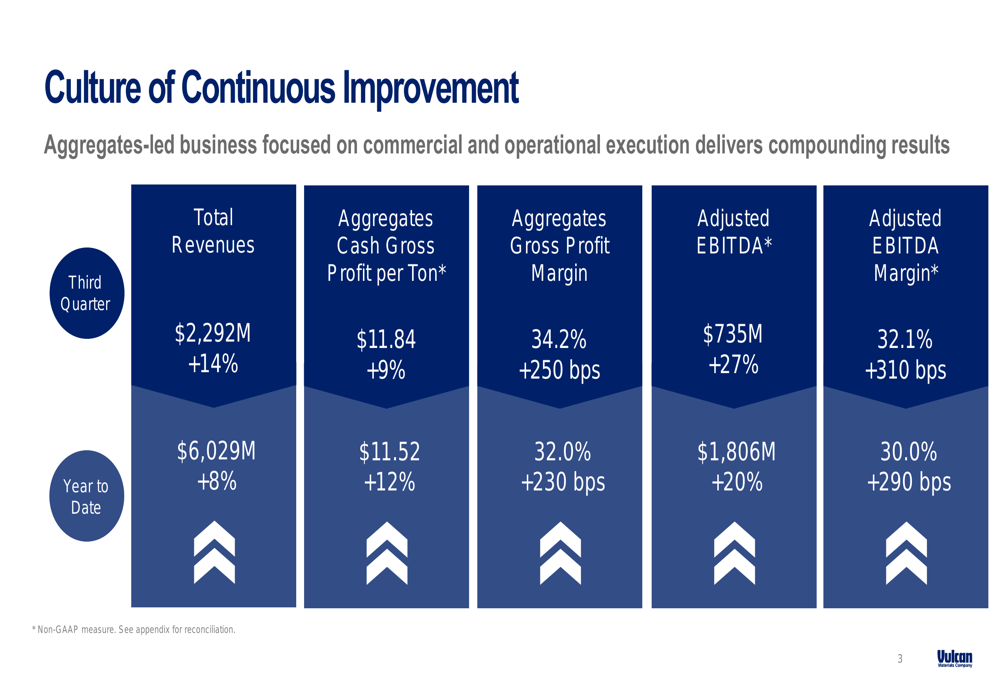

Vulcan reported impressive third-quarter results, with total revenues reaching $2,292 million, a 14% increase year-over-year. More notably, adjusted EBITDA surged 27% to $735 million, with EBITDA margin expanding by 310 basis points to 32.1%. The company’s focus on pricing discipline and operational efficiency drove aggregates gross profit margin up by 250 basis points to 34.2%.

As shown in the following financial highlights chart:

Year-to-date performance has been similarly strong, with total revenues up 8% to $6,029 million and adjusted EBITDA increasing 20% to $1,806 million through the first nine months of 2025. The company’s aggregates cash gross profit per ton, a key metric of operational efficiency, improved 12% to $11.52 year-to-date.

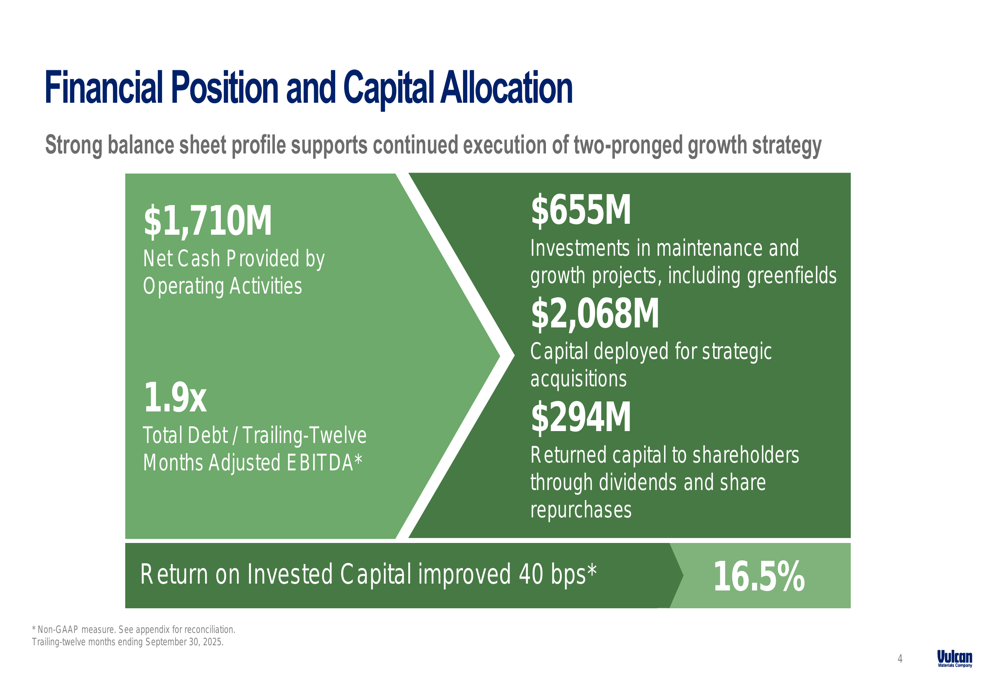

Vulcan’s financial position remains solid, with $1,710 million in net cash provided by operating activities and a leverage ratio of 1.9x total debt to trailing-twelve-months adjusted EBITDA. The company has strategically deployed capital across various initiatives, including $655 million for maintenance and growth projects, $2,068 million for strategic acquisitions, and $294 million returned to shareholders through dividends and share repurchases.

Strategic Market Position

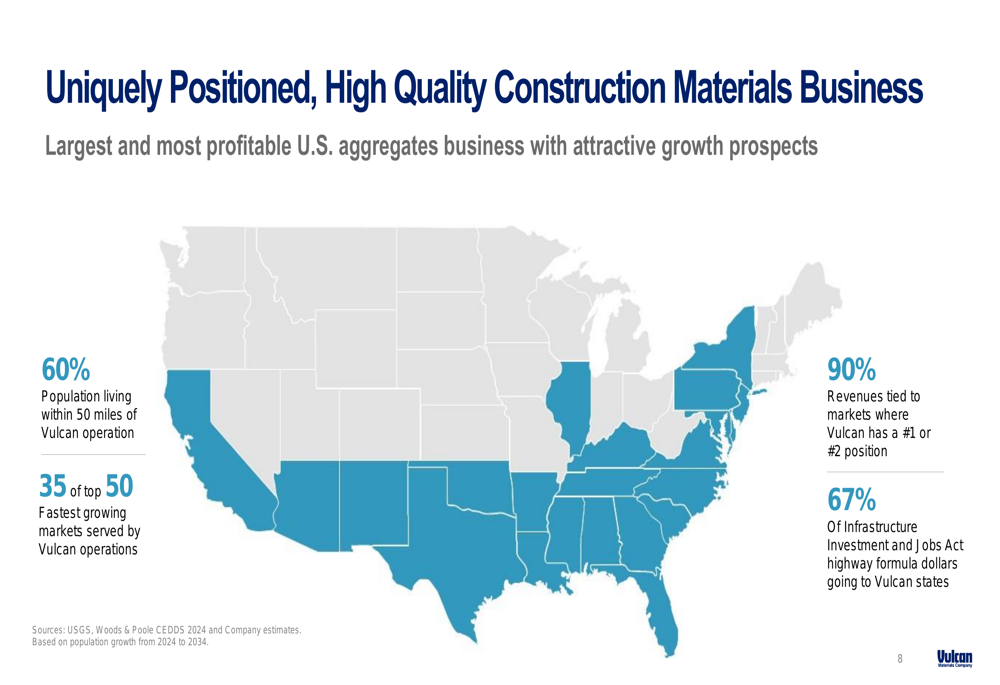

A key factor in Vulcan’s outperformance has been its strategic market positioning. The company serves areas representing 60% of the U.S. population living within 50 miles of its operations, including 35 of the top 50 fastest-growing markets. Importantly, 90% of Vulcan’s revenues come from markets where it holds either the #1 or #2 position.

The company is also well-positioned to benefit from federal infrastructure spending, with 67% of Infrastructure Investment and Jobs Act highway formula dollars flowing to states where Vulcan operates.

This advantageous market position has allowed Vulcan to capitalize on the strong growth in public construction, which has increased 17% in Vulcan markets compared to 10% for the U.S. overall and just 5% in other markets. The company has also seen a recovery in private nonresidential construction, which grew 7% in Vulcan markets versus 4% nationally, while residential construction remains challenging with a 5% decline.

Competitive Industry Performance

Vulcan’s "Vulcan Way of Selling" and "Vulcan Way of Operating" strategies have driven significant improvements in pricing and profitability. Since 2017, the company has achieved 63% aggregates price growth, outpacing its peer average. Even more impressive is the 77% increase in aggregates cash gross profit per ton over the same period, reaching $10.61 in 2024.

The following chart illustrates this consistent improvement in profitability:

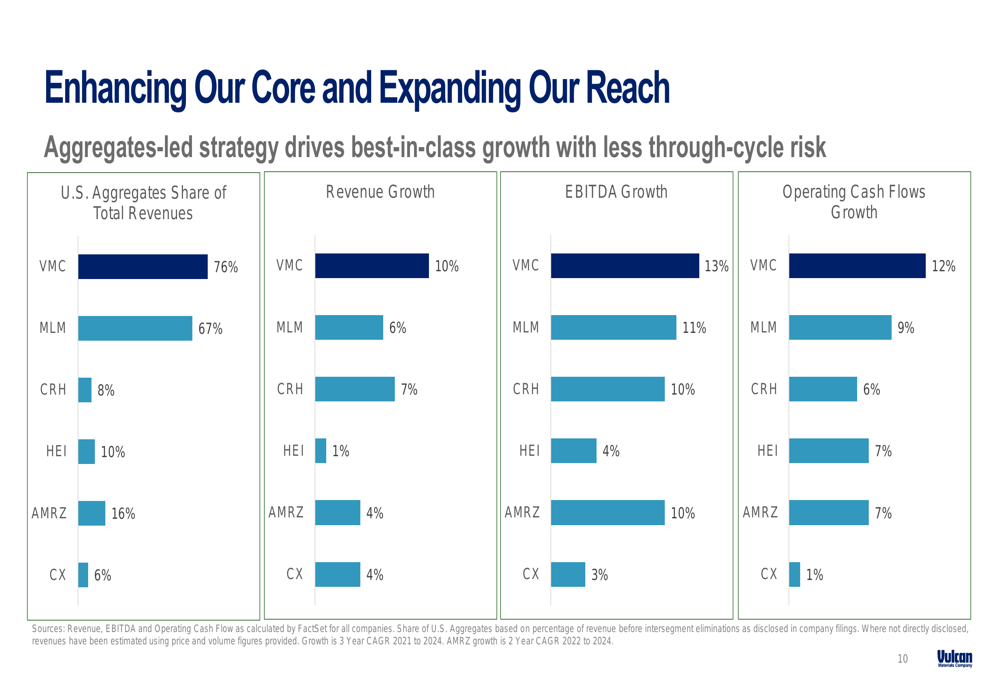

When compared to industry peers, Vulcan demonstrates superior performance across key metrics. The company leads in revenue growth (10% three-year CAGR), EBITDA growth (13%), and operating cash flows growth (12%). Additionally, Vulcan maintains the highest proportion of U.S. aggregates in its revenue mix at 76%, compared to Martin Marietta at 67% and significantly higher than other competitors.

Forward-Looking Statements

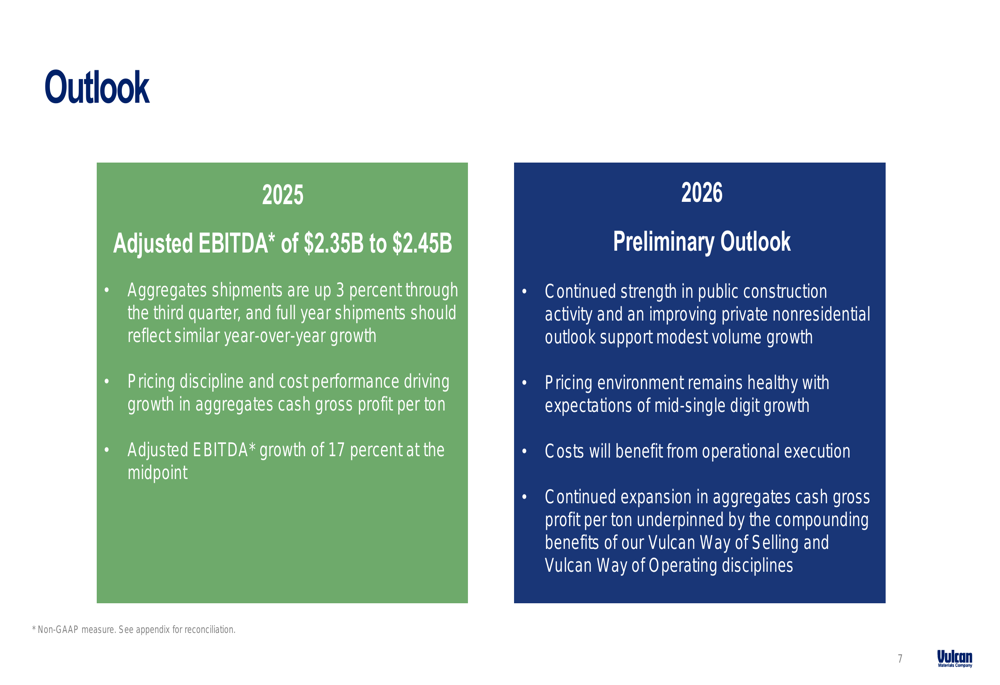

Looking ahead, Vulcan has provided a positive outlook for both 2025 and 2026. For the full year 2025, the company expects adjusted EBITDA of $2.35 billion to $2.45 billion, representing 17% growth at the midpoint. Aggregates shipments are projected to increase by approximately 3% for the year, consistent with year-to-date performance.

For 2026, Vulcan anticipates continued strength in public construction activity and improving private nonresidential outlook, supporting modest volume growth. The pricing environment is expected to remain healthy with mid-single-digit growth. The company’s operational execution should continue to benefit costs, while the compounding effects of the Vulcan Way strategies are expected to drive further expansion in aggregates cash gross profit per ton.

"We are in the early innings of the Vulcan Way of Operating," stated Ronnie Pruitt, President and CEO, during the earnings call, suggesting further operational improvements ahead. Chairman Tom Hill added that the "Public side is good and getting better," reinforcing confidence in the company’s market position.

Despite these positive indicators, investors should note potential challenges, including ongoing weakness in residential construction, economic uncertainties affecting infrastructure spending, and rising operational costs. The market’s cautious reaction to Vulcan’s strong results may reflect these concerns, with the stock closing at $284.65, well below its 52-week high of $311.74.

Nevertheless, Vulcan’s strategic market positioning, operational discipline, and strong financial performance continue to provide a solid foundation for future growth in an evolving construction market landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.