Street Calls of the Week

Introduction & Market Context

Wallenius Wilhelmsen ASA (OB:WAWI) reported its Q2 2025 results on August 12, showing stable performance despite significant market volatility. The company’s stock responded positively, rising 4.99% to close at 96.1 NOK, approaching its 52-week high of 140.7 NOK.

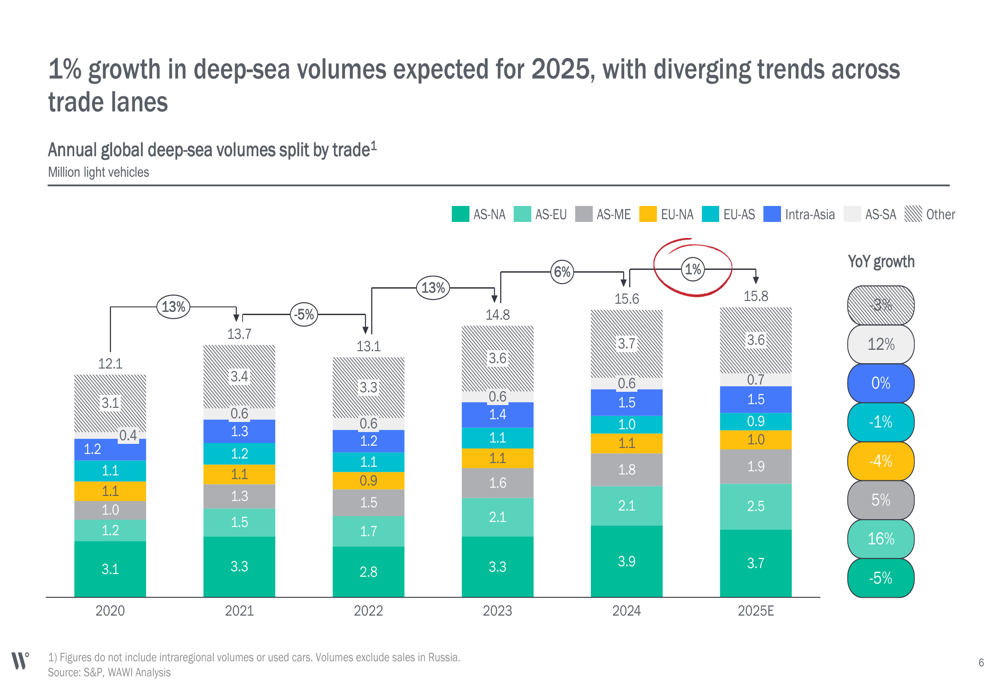

The global shipping market continues to experience diverging trends across trade lanes, with Asian exports showing strong growth while volumes from Europe and North America decline. This growing East-West imbalance is reshaping the industry landscape and influencing Wallenius Wilhelmsen’s operational strategy.

As shown in the following chart of deep-sea volume growth expectations, the company anticipates 1% overall growth in 2025, with significant variations by trade lane:

Quarterly Performance Highlights

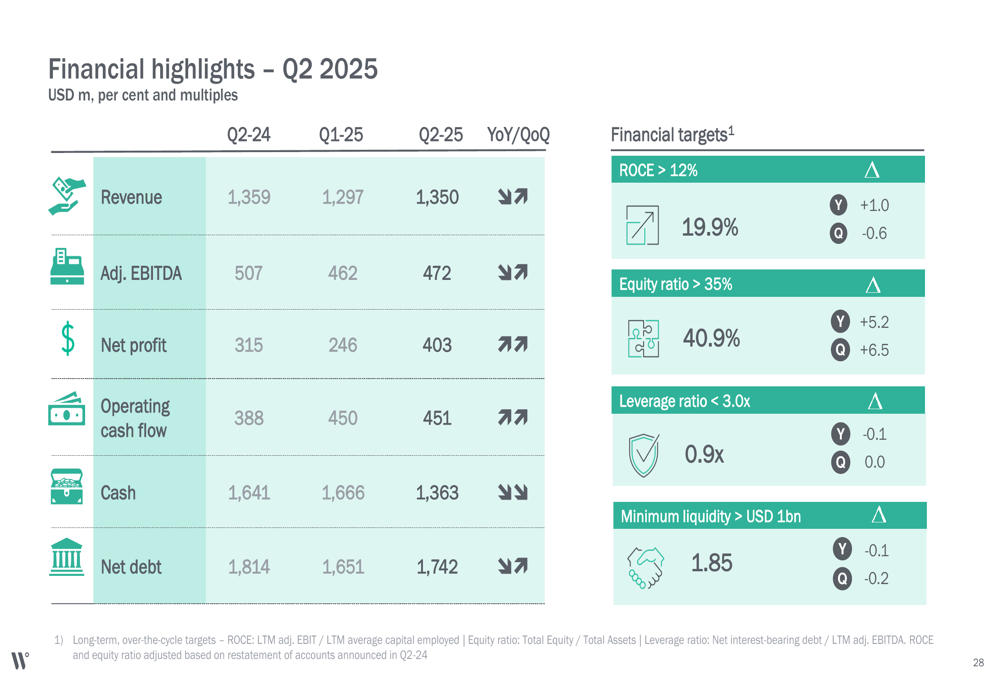

Wallenius Wilhelmsen delivered an EBITDA of USD 472 million in Q2 2025, up 2% quarter-over-quarter despite market challenges. The company resolved to pay a dividend of USD 1.10 per share, based on 50% of H1 2025 underlying EPS combined with the full proceeds of USD 210 million from the MIRRAT sale.

The company’s financial performance remained strong across all segments, with particularly robust results in Shipping Services:

Total (EPA:TTEF) revenue reached USD 1,350 million, with Shipping Services contributing USD 1,033 million, Logistics Services USD 273 million, and Government Services USD 106 million. The company’s net profit for the quarter was USD 403 million, significantly strengthening its financial position.

The following chart provides a comprehensive overview of the company’s financial highlights for Q2 2025:

Shipping and Logistics Performance

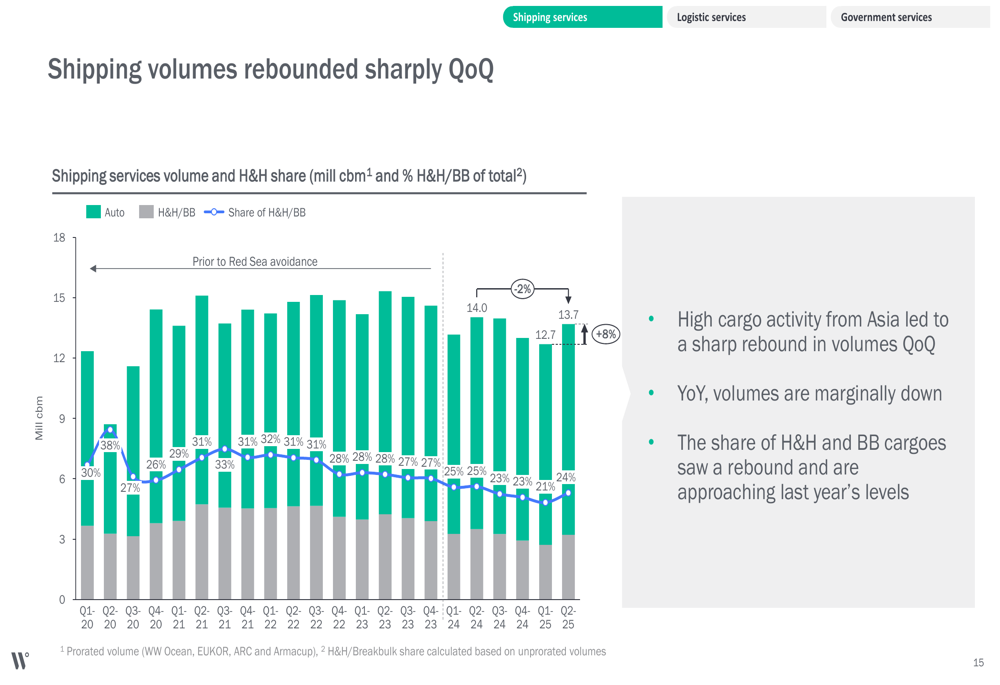

Shipping Services delivered an adjusted EBITDA of USD 411 million, up 6% quarter-over-quarter, driven by increased volumes particularly from Asia. The segment benefited from high cargo activity from Asia, leading to a sharp rebound in volumes QoQ, though year-over-year volumes were marginally down.

The following chart illustrates the shipping volumes rebound:

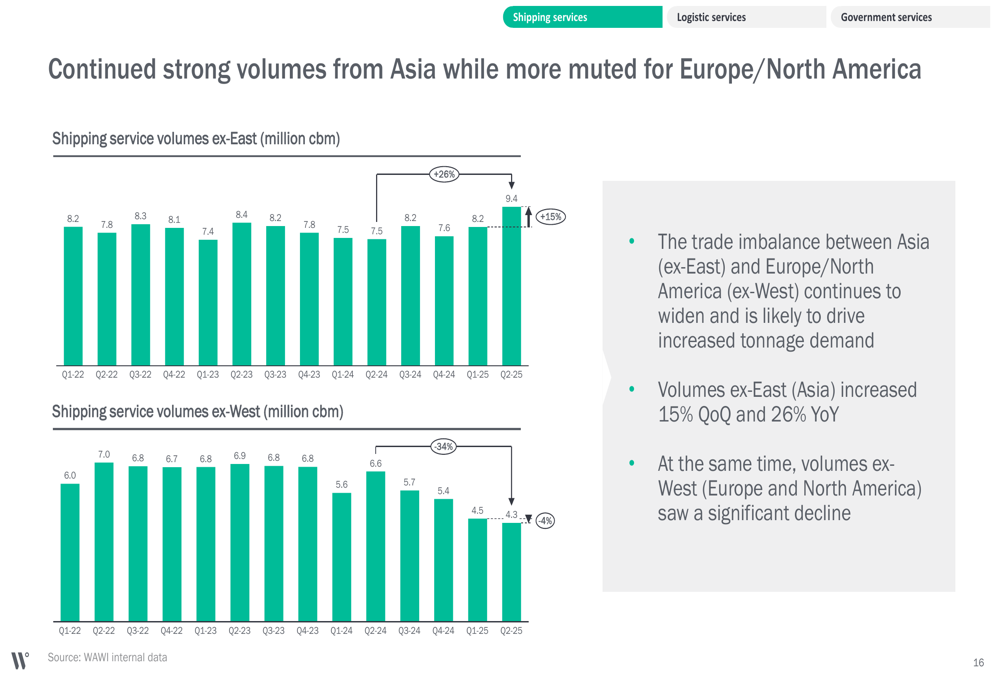

A key trend affecting the company’s operations is the widening trade imbalance between Asia (ex-East) and Europe/North America (ex-West). Volumes ex-East increased 15% QoQ and 26% YoY, while volumes ex-West saw a significant decline. This imbalance drives increased tonnage demand but reduces profitability on a round voyage basis due to less cargo on the backhaul leg.

The East-West imbalance in passenger car volumes is clearly illustrated in this chart:

Logistics Services reported an adjusted EBITDA of USD 32 million, down 12% QoQ, primarily due to the sale of MIRRAT. Despite this decline, the segment maintained relatively stable auto volumes quarter-over-quarter, with margin improvements resulting from cost efficiency measures.

Strategic Initiatives and Fleet Development

Wallenius Wilhelmsen continues to strengthen its market position with USD 500 million worth of contract backlog added during the quarter. The company also secured attractive financing for 10 out of 14 Shaper Class vessels, with USD 300 million in post-delivery financing for four vessels at favorable terms.

A significant strategic focus is the preparation of the Shaper Class vessels for a multi-fuel future. In Q2, the engine configuration for seven vessels was changed to dual fuel LNG with fuel tanks capable of carrying ammonia. The Shaper class will ultimately have seven dual fuel methanol and seven dual fuel LNG (ammonia-prepared) vessels, positioning the company well for future environmental regulations.

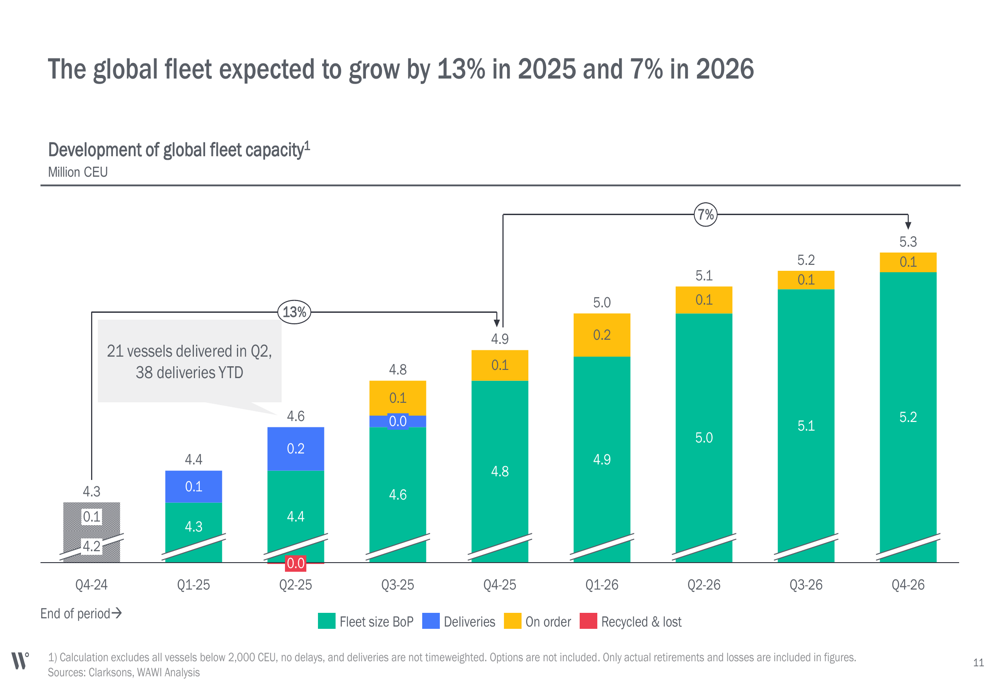

The global fleet capacity is projected to grow significantly in the coming years, as shown in the following chart:

Financial Position and Dividend

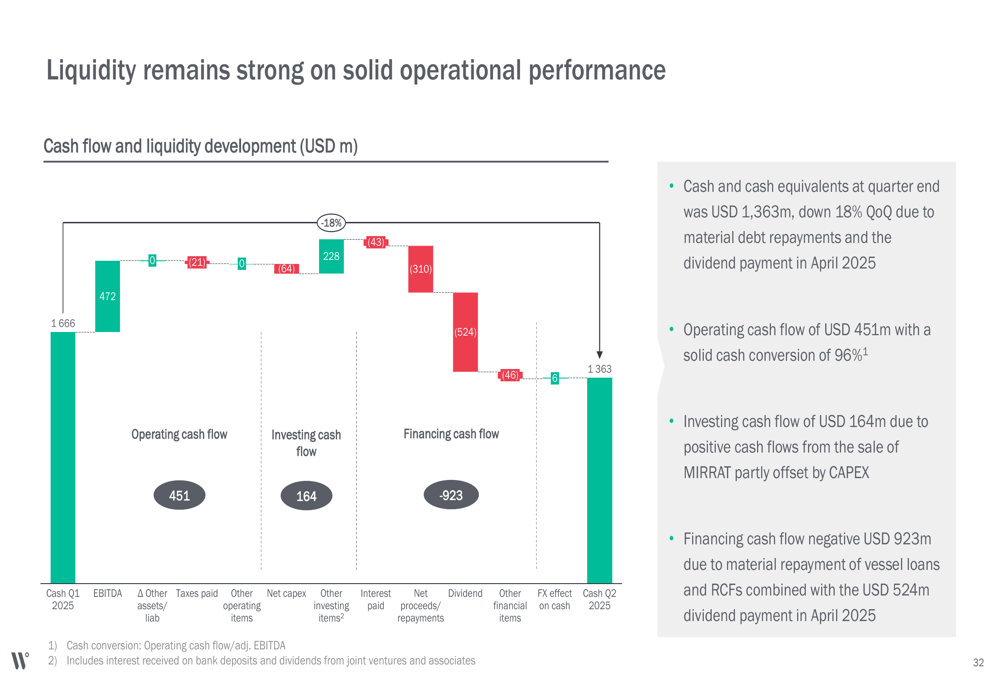

Wallenius Wilhelmsen maintained a strong financial position with solid liquidity. Cash and cash equivalents at quarter end were USD 1,363 million, down 18% QoQ due to material debt repayments and the dividend payment in April 2025. Operating cash flow remained robust at USD 451 million with a solid cash conversion of 96%.

The company’s liquidity position is illustrated in the following chart:

The equity ratio increased from 34% to 40.9% during the quarter, primarily driven by the net profit of USD 403 million. The company’s financial targets were updated, with the ROCE (over the cycle) target increased from 8% to 12%, while maintaining an equity ratio above 35% and reducing the leverage ratio target from <3.5x to <3.0x.

The company declared dividends totaling USD 465 million, or USD 1.10 per share, based on 50% of the underlying H1 2025 net profit plus the proceeds from the MIRRAT sale.

Forward-Looking Statements

Looking ahead, Wallenius Wilhelmsen expects growth out of China to continue while volumes from Europe and the US will likely continue to decline or level out, causing a further increase in the trade imbalance between East and West. The company reiterated that the volume outlook beyond Q3 is uncertain given the current market environment.

Despite these challenges, Wallenius Wilhelmsen expects its EBITDA for 2025 to be in line with 2024. The company is well-positioned to manage volatility in US import and production volumes, and continues to experience a balanced shipping market.

With its strategic focus on fleet renewal, multi-fuel capabilities, and strong financial position, Wallenius Wilhelmsen appears well-equipped to navigate the evolving market landscape and capitalize on growth opportunities, particularly in Asian exports.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.