EOG Resources completes $5.6 billion acquisition of Encino Acquisition Partners

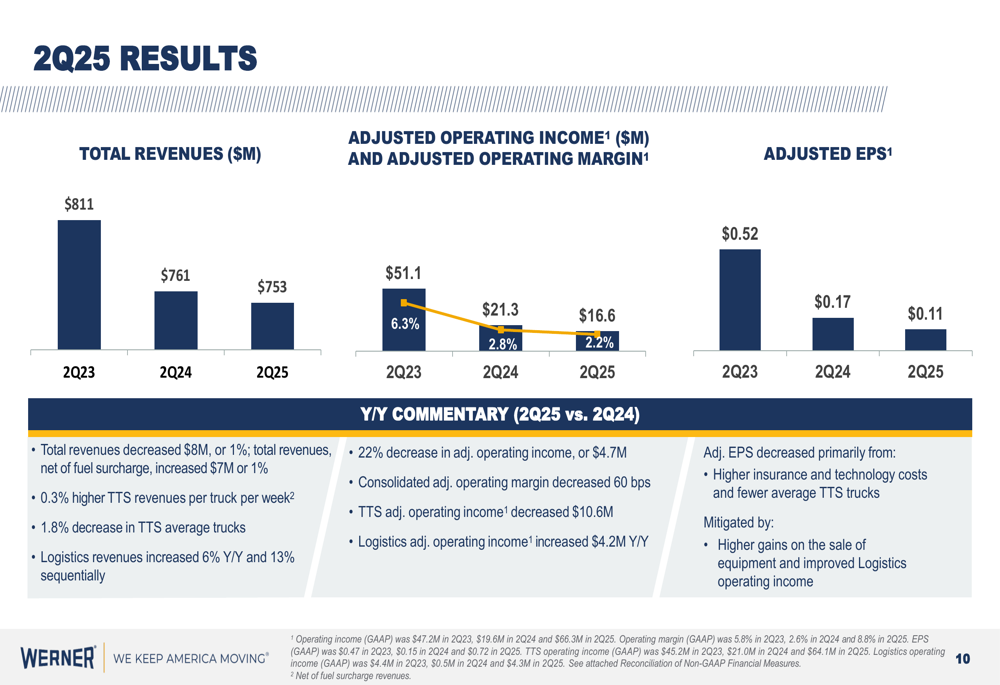

Werner Enterprises (NASDAQ:WERN) reported its second-quarter 2025 results on July 29, showing sequential improvement from a challenging first quarter but continued year-over-year pressure on key metrics. The transportation and logistics company posted revenues of $753 million, down 1% from the year-ago period, while adjusted earnings per share fell 36% to $0.11.

Quarterly Performance Highlights

Werner’s second quarter showed mixed results with total revenues decreasing $8 million year-over-year, though revenues net of fuel surcharge increased $7 million or 1%. The company reported GAAP earnings per share of $0.72, up 380% year-over-year, largely due to one-time factors, while adjusted EPS declined from $0.17 in Q2 2024 to $0.11 in Q2 2025.

As shown in the following chart of quarterly financial performance:

The results represent a significant sequential improvement from Q1 2025, when the company reported a negative adjusted EPS of $0.12 amid elevated insurance costs and operational inefficiencies. Despite the year-over-year decline, Werner’s Q2 adjusted operating income of $16.6 million (down 22% Y/Y) and adjusted operating margin of 2.2% (down 60 basis points) mark a return to profitability after the first quarter’s challenges.

Segment Analysis: TTS and Logistics

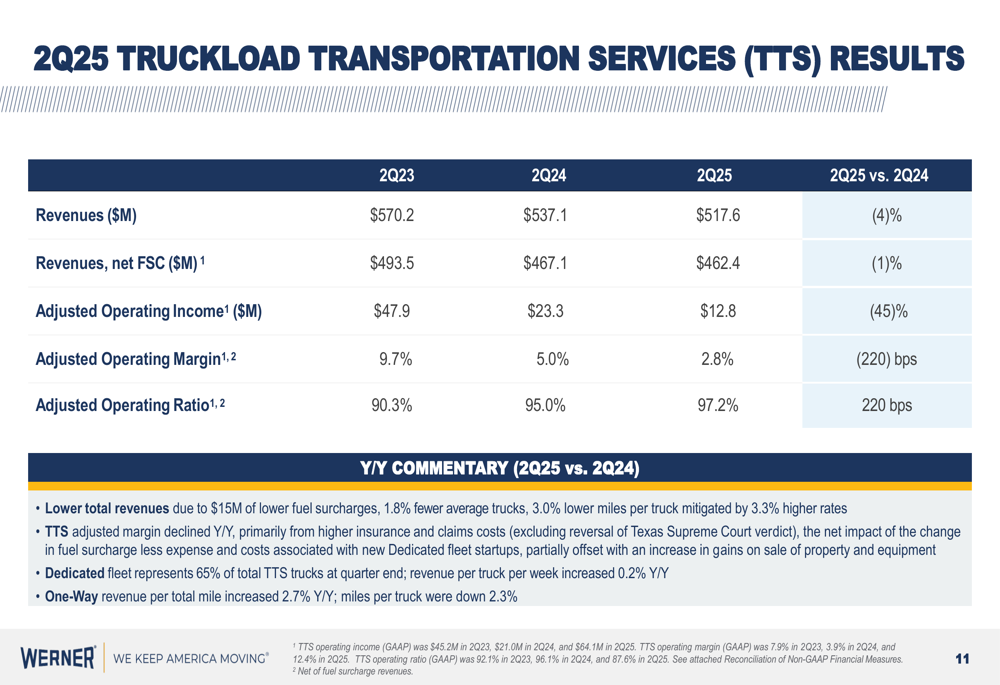

Werner’s Truckload Transportation Services (TTS) segment, which accounts for approximately 71% of total revenues, continued to face margin pressure in Q2. The segment reported revenues of $517.6 million, down 4% year-over-year, with adjusted operating income declining 45% to $12.8 million and adjusted operating margin falling 220 basis points to 2.8%.

The following chart details TTS segment performance:

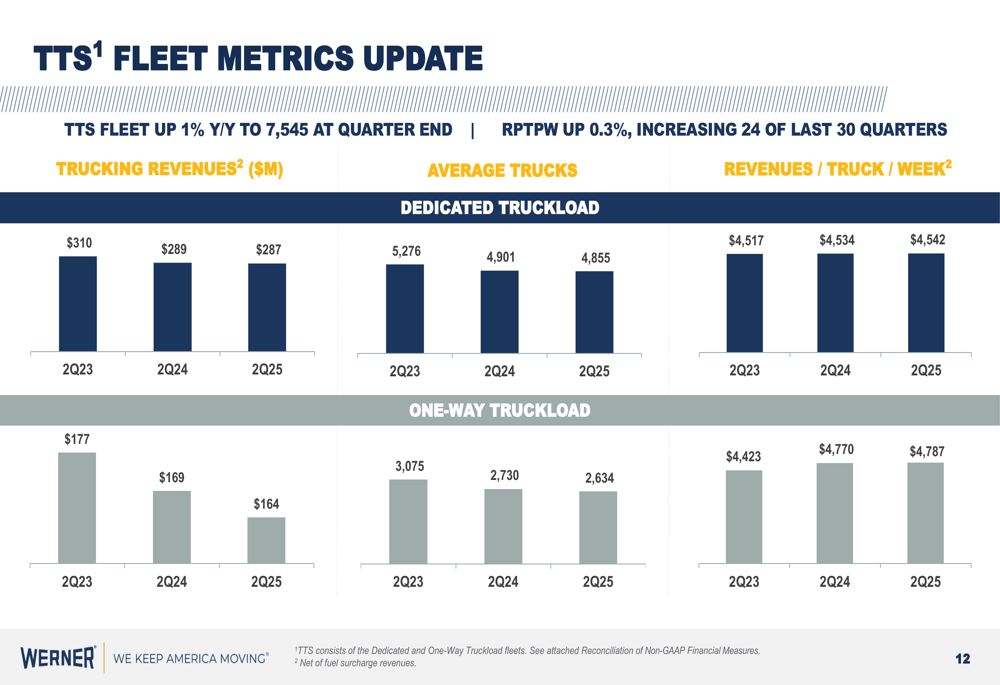

The company’s Dedicated fleet, which represents 65% of total TTS trucks at quarter end, saw revenue per truck per week increase slightly by 0.2% year-over-year to $4,542. Meanwhile, One-Way Truckload revenue per total mile increased 2.7% year-over-year, though miles per truck were down 2.3%.

The following visualization shows the TTS fleet metrics:

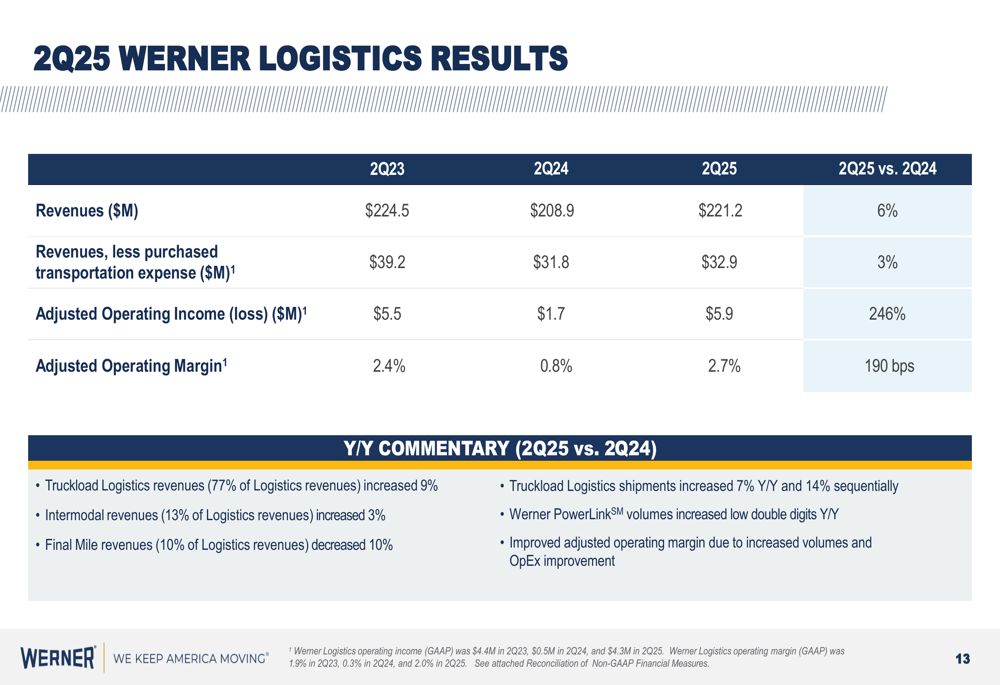

In contrast to TTS, Werner’s Logistics segment emerged as a bright spot in Q2, with revenues increasing 6% year-over-year to $221.2 million and adjusted operating income surging 246% to $5.9 million. The segment’s adjusted operating margin improved 190 basis points to 2.7%.

As illustrated in the following chart of Logistics segment performance:

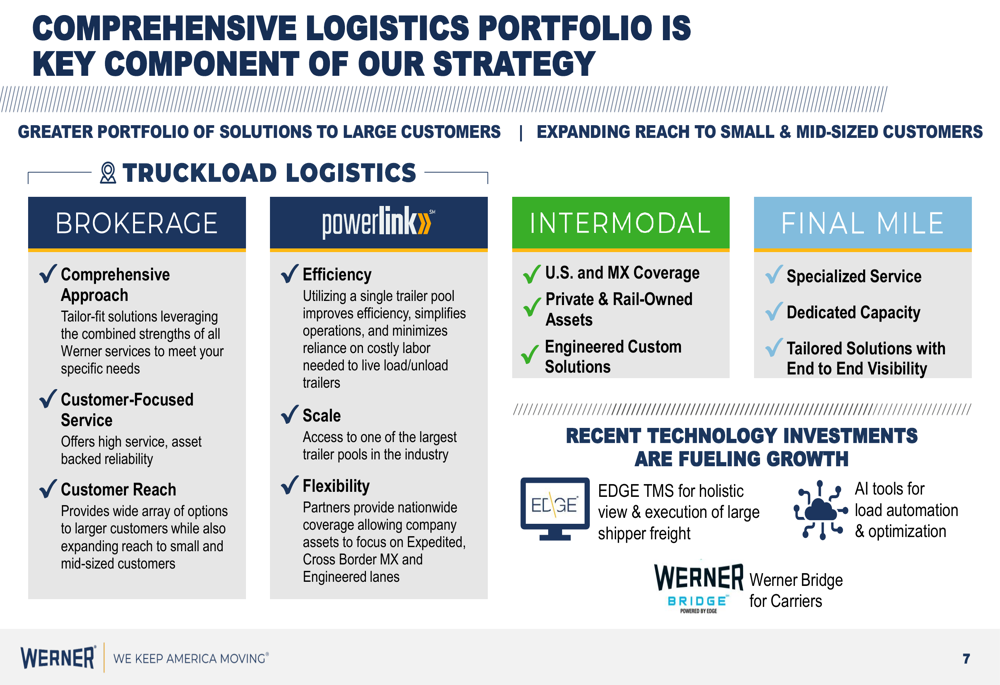

Truckload Logistics, which represents 77% of Logistics revenues, increased 9% year-over-year, while Intermodal revenues (13% of Logistics revenues) grew 3%. Werner PowerLinks™ volumes increased by low double digits compared to the prior year. The company’s comprehensive logistics portfolio continues to be a strategic focus area:

Cost Containment and Cash Flow

Werner has accelerated its cost containment initiatives, increasing its 2025 cost savings target from $40 million to $45+ million, with more than $20 million achieved through Q2. The company reported a 4% year-over-year reduction in consolidated salaries, wages, and benefits expenses in Q2, with Logistics SWB down 13%.

The following chart illustrates Werner’s cost containment progress:

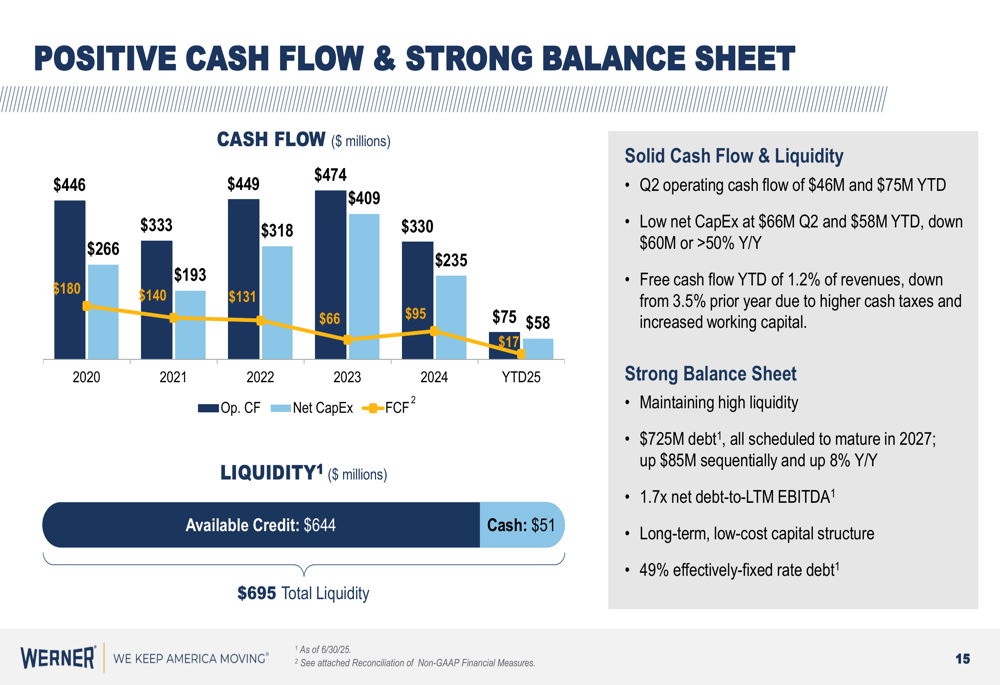

The company generated $46 million in operating cash flow during Q2 and $75 million year-to-date. Net capital expenditures were significantly lower at $66 million in Q2 and $58 million year-to-date, down more than 50% compared to the prior year.

As shown in the following cash flow and balance sheet overview:

Free cash flow year-to-date represented 1.2% of revenues, down from 3.5% in the prior year due to higher cash taxes and increased working capital. The company maintained a strong balance sheet with $51 million in cash and $644 million in available credit, though debt increased 8% year-over-year to $725 million, resulting in a net debt-to-LTM EBITDA ratio of 1.7x.

Market Outlook and Guidance

Werner provided an updated market outlook for the remainder of 2025, noting that truckload fundamentals are expected to remain stable through the end of the year, with the market approaching equilibrium as capacity continues to exit. The company observed that consumers remain resilient, particularly in non-discretionary spending, while retail inventories have mostly normalized.

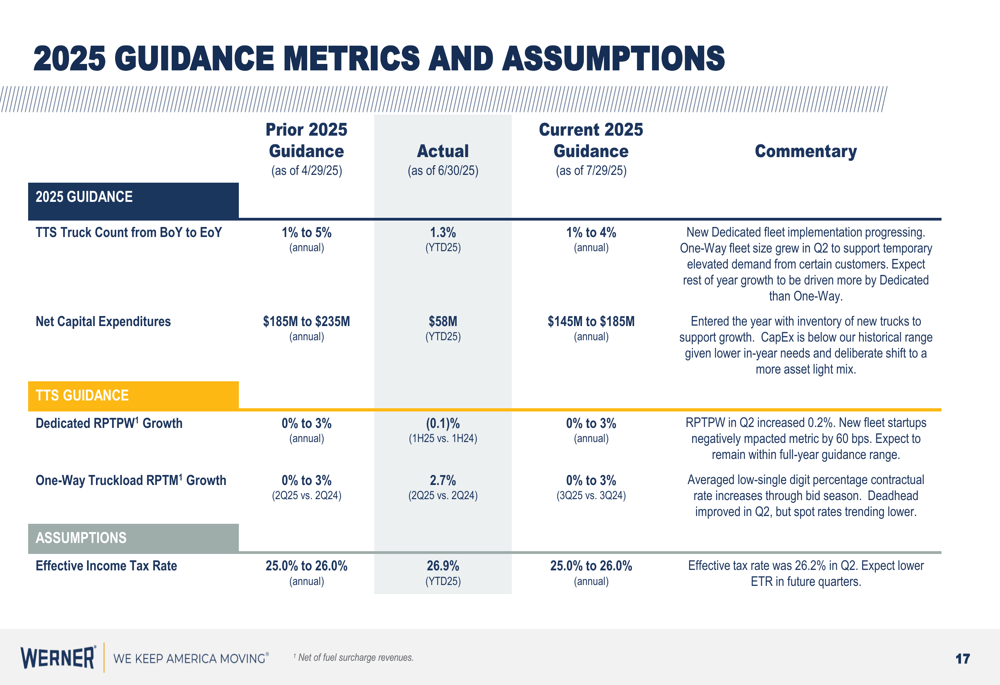

The company updated its 2025 guidance, maintaining its Dedicated revenue per truck per week growth forecast of 0% to 3% annually and One-Way Truckload revenue per total mile growth of 0% to 3% for Q3 2025 compared to Q3 2024. Werner revised its full-year truck count growth projection to 1% to 4%, down slightly from the previous 1% to 5%, and reduced its net capital expenditure guidance to $145 million to $185 million from the previous $185 million to $235 million.

As detailed in the following guidance table:

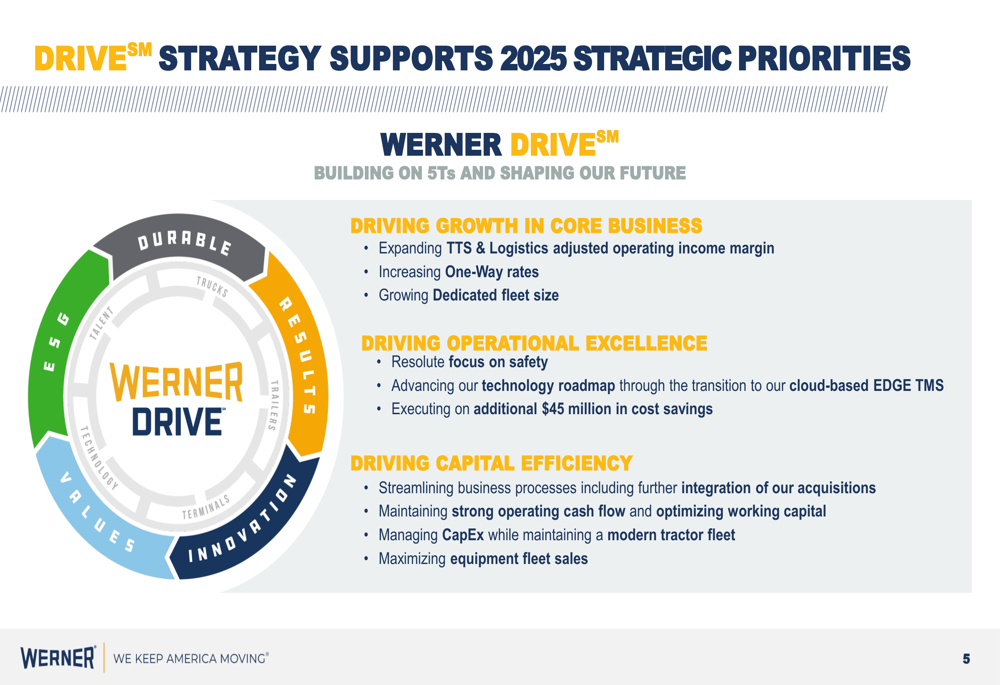

Werner’s DRIVE strategy continues to focus on three key areas: driving growth in the core business, driving operational excellence, and driving capital efficiency. The company highlighted its ongoing technology transformation through the transition to its cloud-based EDGE TMS and execution of additional cost savings as key priorities for the remainder of 2025.

While Werner faces continued challenges in its TTS segment, the strong performance of its Logistics business, combined with aggressive cost containment measures and reduced capital expenditures, positions the company to navigate the current market environment as it works toward improving overall profitability in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.