BofA update shows where active managers are putting money

Introduction & Market Context

WesBanco Inc. (NASDAQ:WSBC) presented its second quarter 2025 earnings results on July 29, showcasing the significant impact of its recently completed acquisition of Premier Financial Corp (PFC). The regional bank reported substantial growth across key metrics, with total assets increasing by 54% year-over-year, positioning WesBanco among the top 100 largest U.S. banks by asset size.

Despite the positive quarterly results, WesBanco’s stock closed at $32.19 on the day of the presentation, down 1.15% from the previous close. The stock has traded between $26.42 and $37.36 over the past 52 weeks, currently trading at a level that suggests investors are still assessing the long-term benefits of the Premier acquisition.

Quarterly Performance Highlights

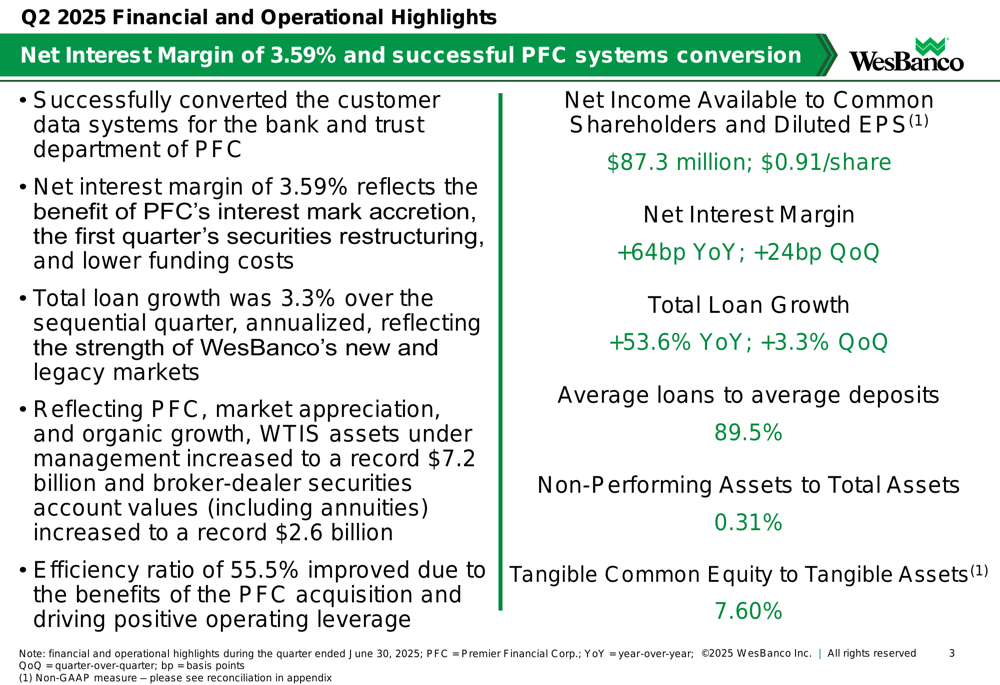

WesBanco reported net income available to common shareholders of $87.3 million or $0.91 per diluted share for Q2 2025, excluding restructuring and merger-related expenses. This represents significant improvement from the previous quarter’s EPS of $0.66, which had already exceeded analyst expectations.

The bank successfully completed the conversion of PFC’s customer data systems for both banking and trust departments during the quarter, a critical milestone in the integration process. This conversion, along with other synergies from the acquisition, helped drive improvements in key performance metrics.

As shown in the following comprehensive overview of Q2 2025 results, WesBanco achieved notable improvements across multiple financial metrics:

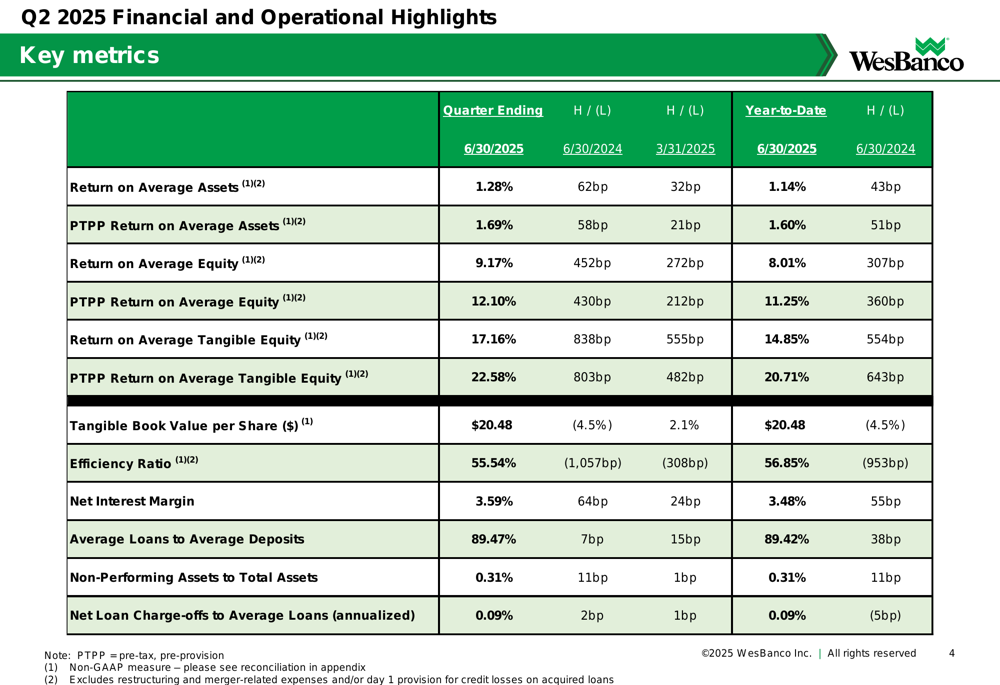

The bank’s efficiency ratio improved to 55.5%, reflecting the benefits of the PFC acquisition and positive operating leverage. Return on average assets reached 1.28%, while return on average tangible equity climbed to 17.16%, representing year-over-year improvements of 62 and 838 basis points, respectively.

Detailed Financial Analysis

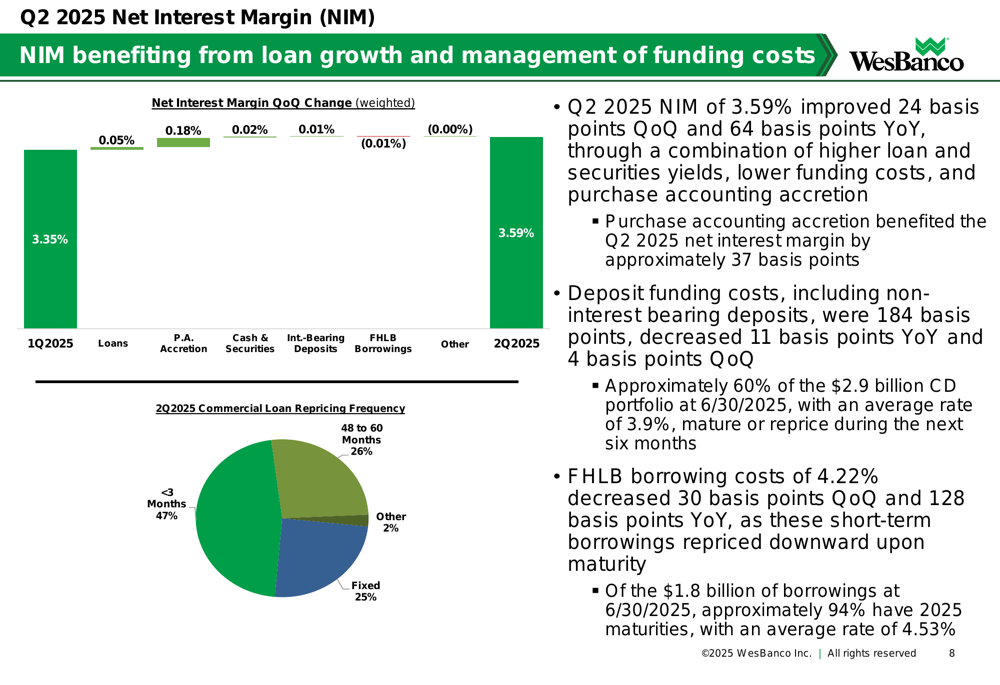

WesBanco’s net interest margin (NIM) expanded to 3.59% in Q2 2025, a 24 basis point improvement from the previous quarter and 64 basis points higher than the same period last year. This exceeded the company’s previous guidance that NIM would exceed 3.5% in Q2. The improvement was driven by a combination of higher loan and securities yields, lower funding costs, and purchase accounting accretion, which contributed approximately 37 basis points to the quarter’s NIM.

The following chart illustrates the components contributing to the sequential NIM improvement:

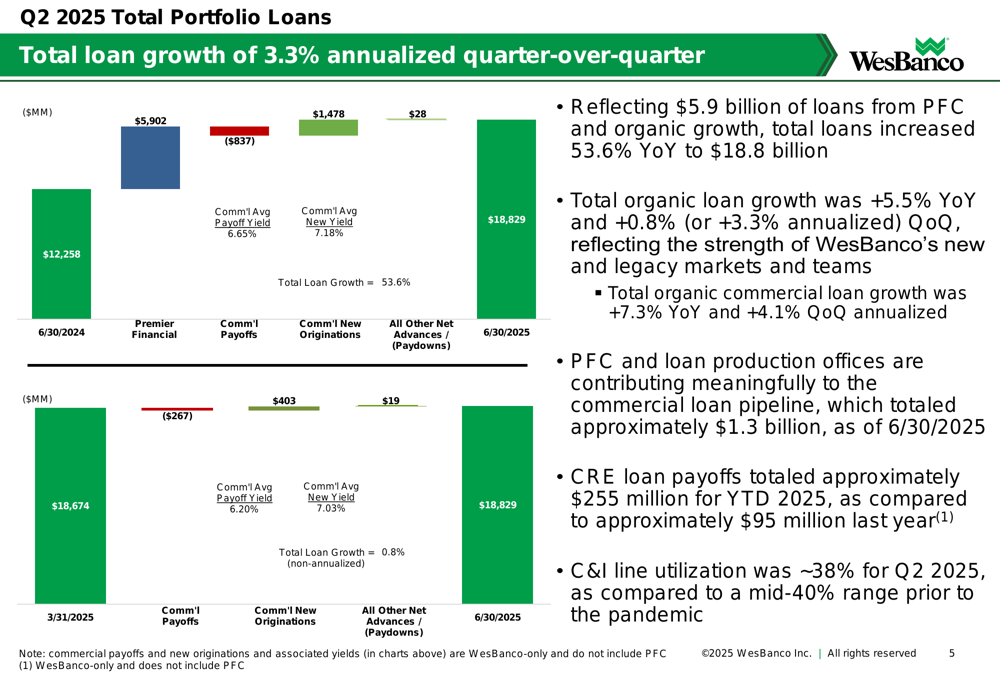

Total (EPA:TTEF) loans increased by 53.6% year-over-year to $18.8 billion, reflecting both the $5.9 billion of loans acquired from PFC and organic growth. On a sequential quarter basis, loans grew at an annualized rate of 3.3%, which aligns with the lower end of management’s previously stated guidance of mid to upper single-digit loan growth for 2025.

The chart below breaks down the components of loan growth, showing the significant contribution from the Premier acquisition as well as new commercial originations:

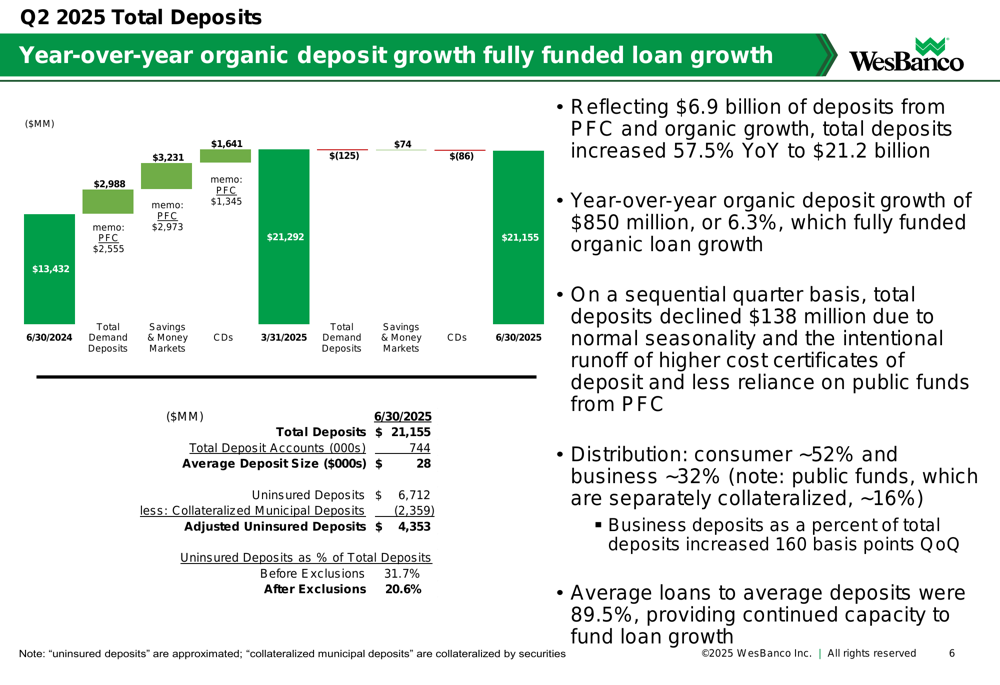

On the deposit side, total deposits increased 57.5% year-over-year to $21.2 billion, including $6.9 billion from PFC. Organic deposit growth of $850 million, or 6.3%, fully funded the bank’s organic loan growth. The average loans to average deposits ratio stood at 89.5%, providing continued capacity to fund future loan growth.

Non-interest income increased 40.2% year-over-year to $44 million, primarily due to the acquisition of PFC, which drove higher service charges on deposits, trust fees, mortgage banking income, digital banking income, and bank-owned life insurance. Trust fees and securities brokerage revenue increased due to the addition of PFC wealth clients, market value appreciation, and organic growth, with trust assets under management reaching a record $7.2 billion.

Credit Quality and Capital Position

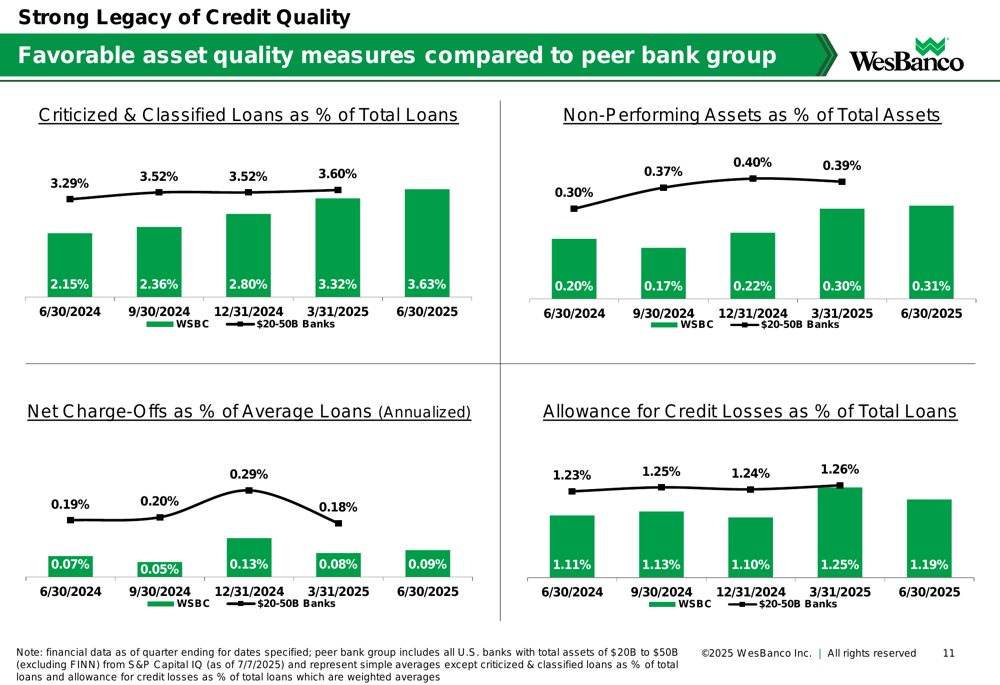

WesBanco maintained its strong legacy of credit quality in Q2 2025, with favorable asset quality measures compared to its peer bank group of institutions with $20-50 billion in assets. The bank’s non-performing assets to total assets ratio was 0.31%, while net charge-offs as a percentage of average loans stood at 0.09% annualized.

The following charts demonstrate WesBanco’s credit quality metrics compared to peers:

The allowance for credit losses on loans was $223.9 million at June 30, 2025, providing a coverage ratio of 1.19%. Excluded from this ratio are fair market value adjustments on previously acquired loans representing 1.74% of total loans.

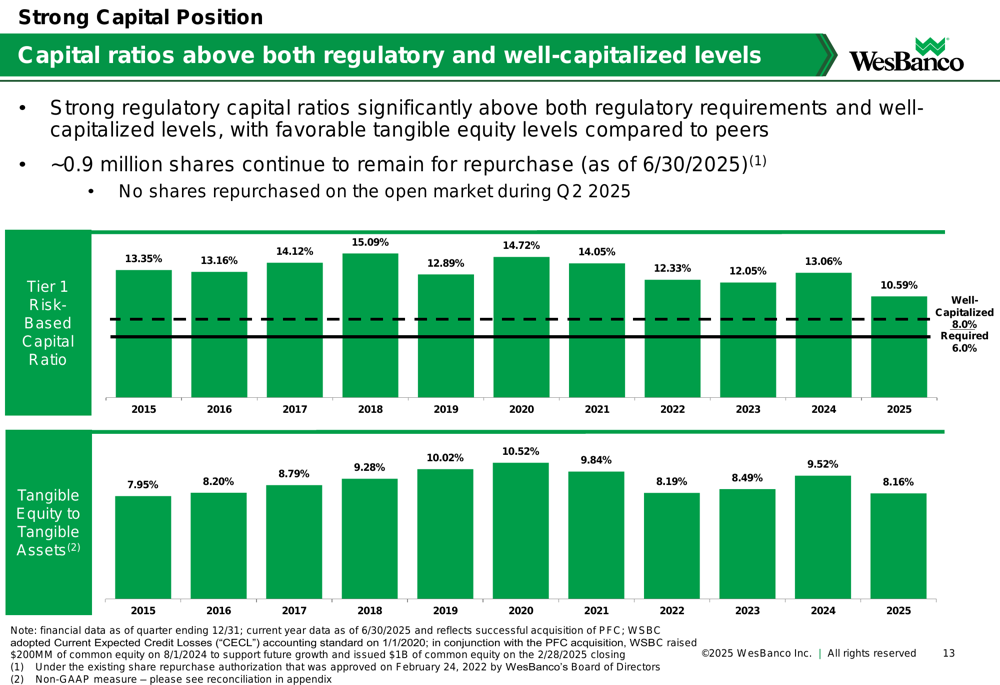

WesBanco’s capital position remains strong, with regulatory capital ratios significantly above both regulatory requirements and well-capitalized levels. The tangible common equity to tangible assets ratio stood at 7.60%, reflecting the impact of the PFC acquisition.

Forward-Looking Statements

Looking ahead, WesBanco management highlighted several positive factors that could support continued growth. The commercial loan pipeline totaled approximately $1.3 billion as of June 30, 2025, with PFC and loan production offices contributing meaningfully to this pipeline.

The bank also noted opportunities for funding cost improvements, with approximately 60% of its $2.9 billion CD portfolio, currently at an average rate of 3.9%, set to mature or reprice during the next six months. Additionally, of the $1.8 billion of borrowings outstanding at quarter-end, approximately 94% have 2025 maturities, with an average rate of 4.53%.

Management indicated that the majority of PFC cost savings had been achieved by June 30, 2025, suggesting that the full benefits of the acquisition should be reflected in coming quarters. The bank continues to have approximately 0.9 million shares remaining for potential repurchase, though no shares were repurchased on the open market during Q2 2025.

WesBanco’s successful integration of Premier Financial has significantly expanded its scale and capabilities, positioning the bank for continued growth while maintaining its strong credit quality and capital position. Investors will be watching closely to see if the bank can continue to leverage these advantages to drive further improvements in profitability and shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.