e.l.f. Beauty stock plummets 20% as revenue and guidance fall short of expectations

Introduction & Market Context

WESCO International Inc (NYSE:WCC) reported record quarterly sales in its third quarter 2025 results, exceeding analyst expectations and prompting a significant upward revision to its full-year outlook. The company’s presentation, delivered on October 30, 2025, highlighted accelerating sales momentum across all business segments, with particularly strong performance in data center solutions.

The market responded positively to the results, with WESCO’s stock jumping 10.66% to $228.29 following the announcement. The company’s shares have traded between $125.21 and $258.59 over the past 52 weeks, with the current price reflecting growing investor confidence in WESCO’s strategic positioning.

Quarterly Performance Highlights

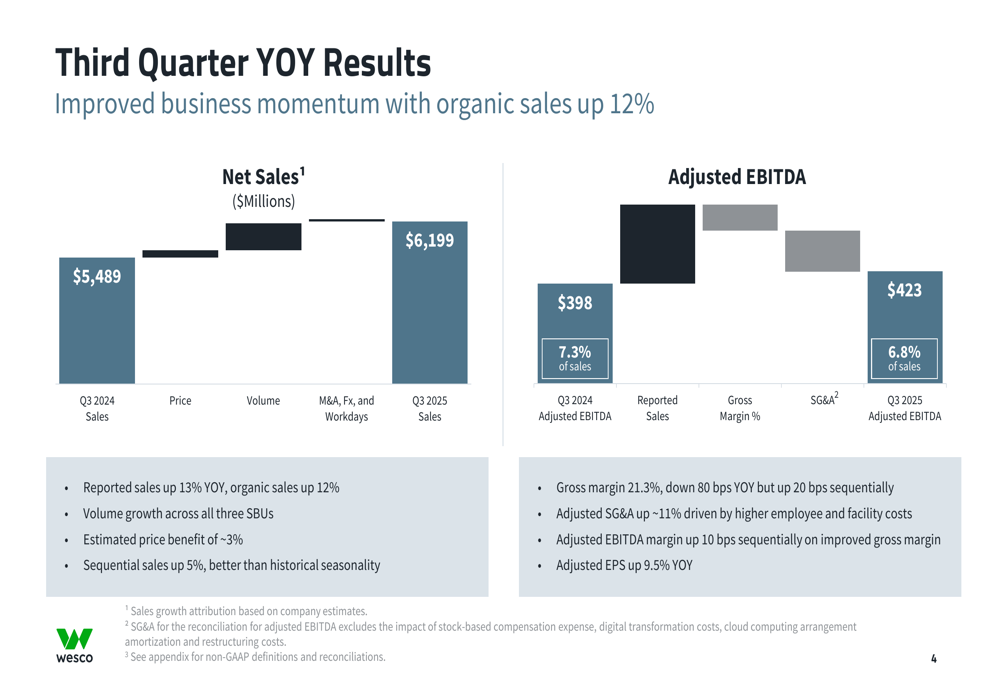

WESCO reported record quarterly sales of $6.2 billion, representing 13% reported growth and 12% organic growth year-over-year. This marks the fourth consecutive quarter of accelerating sales momentum for the company, with all three business units contributing to the growth.

As shown in the following breakdown of third quarter results, WESCO’s performance was driven by strong volume growth across all segments, with an estimated price benefit of approximately 3%:

The Communications & Security Solutions (CSS) segment led the way with 18% organic growth, followed by Electrical & Electronic Solutions (EES) at 12%, while Utility & Broadband Solutions (UBS) returned to growth at 3%. Adjusted EBITDA increased from $398 million in Q3 2024 to $423 million in Q3 2025, with adjusted EBITDA margin improving 10 basis points sequentially to 6.8%, driven by improved gross margin.

Adjusted earnings per share reached $3.92, up 9.5% year-over-year and exceeding the analyst forecast of $3.82. The company’s backlog increased 7% compared to the previous year, indicating strong future demand.

Data Center Growth Strategy

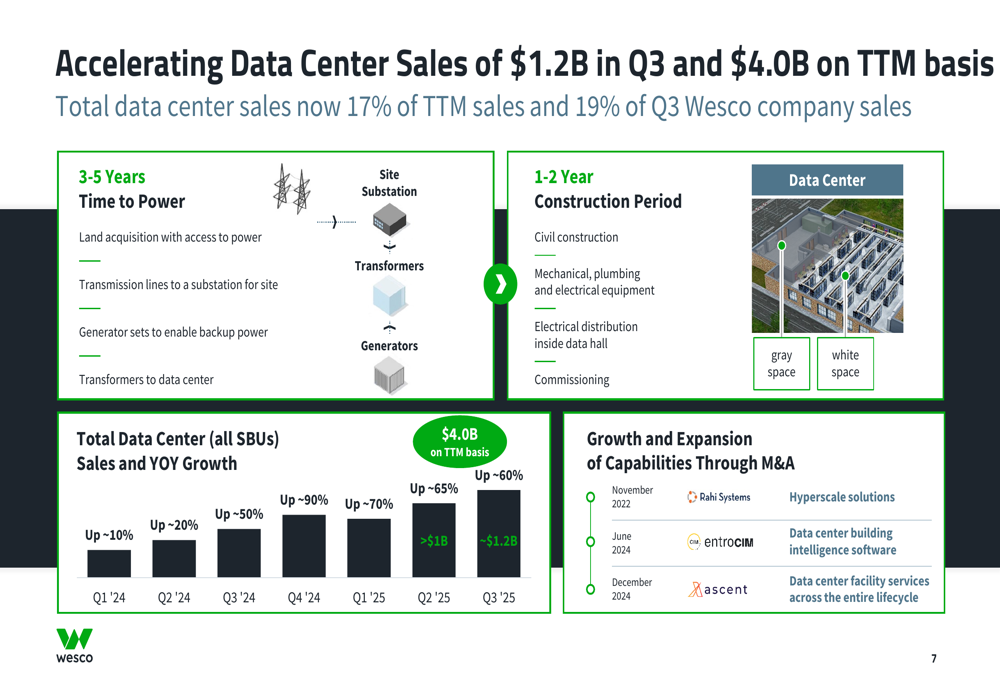

A standout element of WESCO’s third quarter performance was the exceptional growth in its data center business. Data center sales reached approximately $1.2 billion in Q3, representing a 60% increase year-over-year and now accounting for 19% of quarterly sales.

As illustrated in the following chart, WESCO has strategically expanded its data center capabilities through acquisitions, including Rahi Systems, entrocIM, and Ascent:

The company’s comprehensive approach to data center solutions spans both "Gray Space" (electrical infrastructure, mechanical and cooling, MRO safety) and "White Space" (physical security, IoT, communications infrastructure, IT infrastructure). This positions WESCO to capture value across the entire data center lifecycle, from the initial "Time to Power" phase through construction and ongoing operations.

WESCO’s data center sales mix currently stands at 20% Gray Space and 80% White Space, as shown in this breakdown of their offerings:

Segment Performance Analysis

Each of WESCO’s three business segments contributed differently to the quarter’s strong performance:

The Electrical & Electronic Solutions (EES) segment reported sales of $2.36 billion, up 12% year-over-year, with construction up mid-teens, industrial up mid-single digits, and OEM up mid-teens. The segment’s adjusted EBITDA margin improved to 8.4%, up 30 basis points sequentially.

The Communications & Security Solutions (CSS) segment delivered the strongest growth, with sales of $2.41 billion, up 21% year-over-year (18% organic). CSS benefited significantly from data center projects, with backlog up 17% year-over-year. Adjusted EBITDA margin for this segment reached 9.1%, up 30 basis points sequentially.

The Utility & Broadband Solutions (UBS) segment returned to growth after previous challenges, with sales of $1.43 billion, up 3% year-over-year. This improvement was driven by stronger performance in Investor-Owned Utilities, while broadband sales increased over 20%. The segment maintained a double-digit adjusted EBITDA margin at 10.4%.

Financial Position and Cash Flow

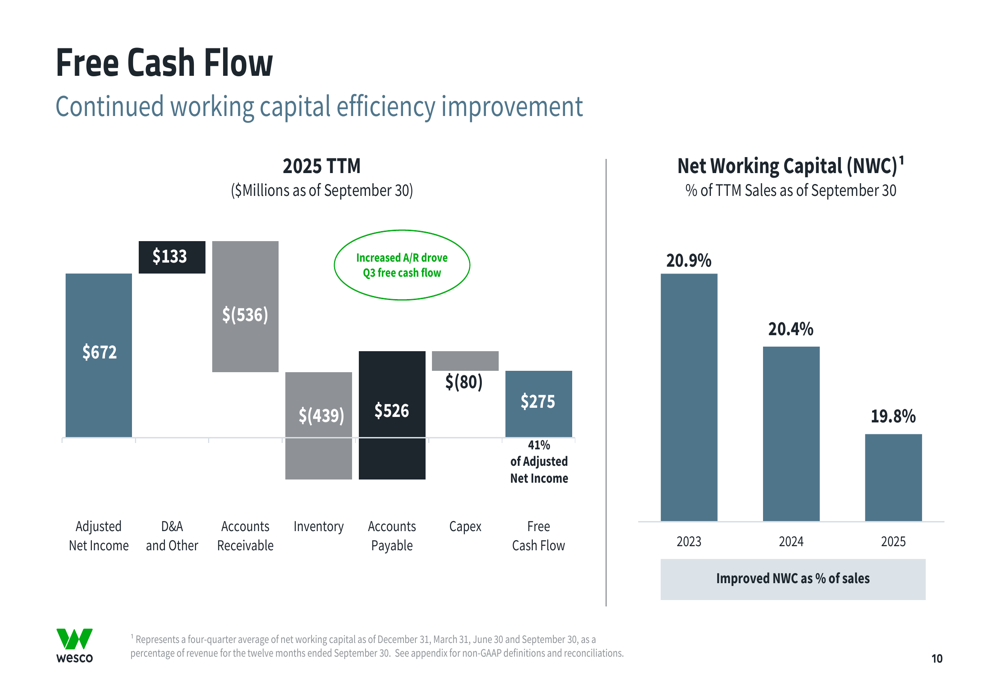

WESCO’s free cash flow on a trailing twelve-month basis was $275 million, with increased accounts receivable driving the Q3 free cash flow dynamics. The company has improved its working capital efficiency, with Net Working Capital as a percentage of TTM Sales decreasing from 20.9% in 2023 to 19.8% in 2025.

The following waterfall chart illustrates the components affecting free cash flow:

In June 2025, WESCO redeemed its high-cost $540 million preferred stock (10.625% dividend rate), replacing it with new 6.375% senior notes due 2033. This strategic refinancing is expected to provide approximately $32 million in annualized benefit to net income and cash flow, translating to approximately $0.65 annualized benefit to EPS.

Revised Full-Year Outlook

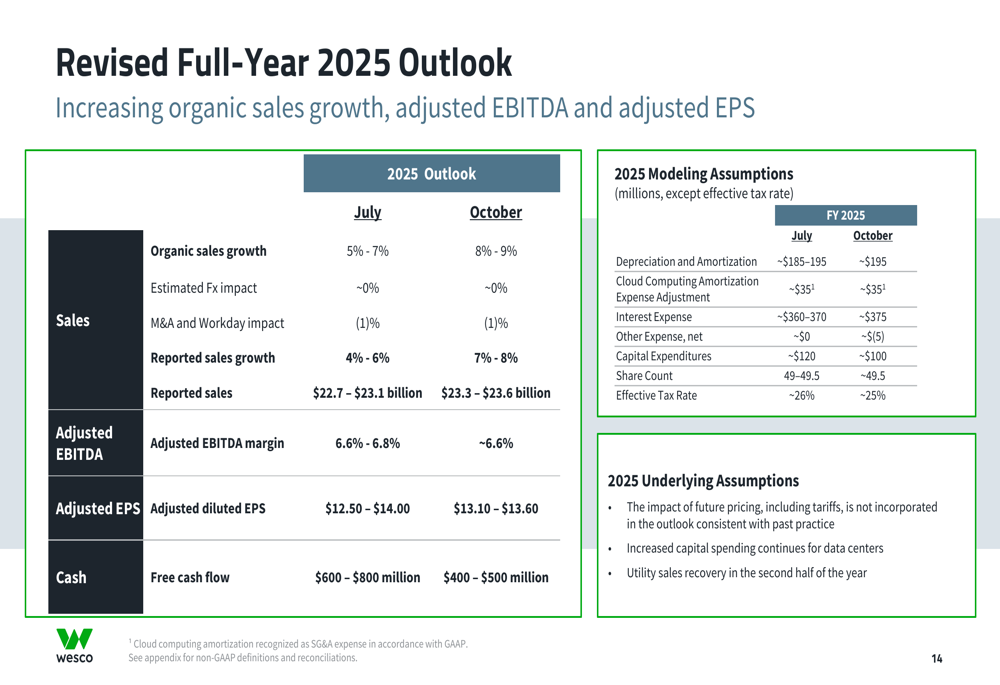

Based on the strong third-quarter performance and continued positive momentum, WESCO has raised its full-year 2025 outlook. The company now expects organic sales growth of 8-9% (up from 5-7% previously) and reported sales growth of 7-8% (up from 4-6%).

The detailed revised outlook is presented in the following table:

The revised guidance projects reported sales of $23.3-$23.6 billion (up from $22.7-$23.1 billion) and adjusted diluted EPS of $13.10-$13.60 (narrowed from $12.50-$14.00 previously). However, the company reduced its free cash flow outlook to $400-$500 million (down from $600-$800 million), citing increased working capital requirements due to the rising demand curve and higher sales growth rate.

Looking ahead to the fourth quarter, WESCO noted that positive momentum continued into October, with preliminary sales per workday up approximately 9%. The company’s organic sales growth has been accelerating throughout 2025, as shown in this trend chart:

Challenges and Opportunities

While WESCO’s overall performance was strong, the company faces several challenges. Gross margin was 21.3% in Q3 2025, down 80 basis points year-over-year, though it improved 20 basis points sequentially. This reflects the impact of continued large project wins, which typically carry lower margins.

The company is also navigating the impact of tariffs, with significant supplier price increases expected in the coming quarters. WESCO noted that supplier price increase notifications through October are up over 60% in count compared to all of Q4 2024. The company’s strategy includes passing through price increases, leveraging scale to provide locally sourced products, reducing imports from high-tariff countries, and optimizing supply chain logistics.

Despite these challenges, WESCO remains well-positioned to benefit from secular growth trends including AI-driven data centers, increased power generation, electrification, automation, and reshoring. The company’s strategic business unit sales growth drivers for 2025 indicate continued strong performance in Communications & Security Solutions (expected up mid-teens) and moderate growth in Electrical & Electronic Solutions (expected up mid-single digits plus).

Executive Summary

WESCO’s third quarter 2025 results demonstrate the company’s ability to capitalize on high-growth markets while navigating industry challenges. The exceptional performance in data center solutions, returning growth in utility markets, and successful debt refinancing highlight management’s strategic focus on long-term value creation.

With four consecutive quarters of accelerating sales momentum, a strong backlog, and positive early indicators for Q4, WESCO appears well-positioned to deliver on its raised full-year outlook. While increased working capital requirements may pressure free cash flow in the near term, the company’s improved operational efficiency and strategic market positioning suggest continued momentum into 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.