ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

Western Digital Corporation (NASDAQ:WDC) reported strong first-quarter fiscal 2026 results on October 30, 2025, exceeding guidance on both revenue and earnings per share. Despite the positive performance, the company’s stock fell 2.3% in after-hours trading to $137.51, reflecting broader market concerns about future supply constraints in the data storage industry.

The storage solutions provider demonstrated significant year-over-year growth, primarily driven by its cloud segment, which now accounts for 89% of total revenue. This performance comes as data center demand continues to accelerate, particularly for high-capacity drives supporting artificial intelligence applications.

Quarterly Performance Highlights

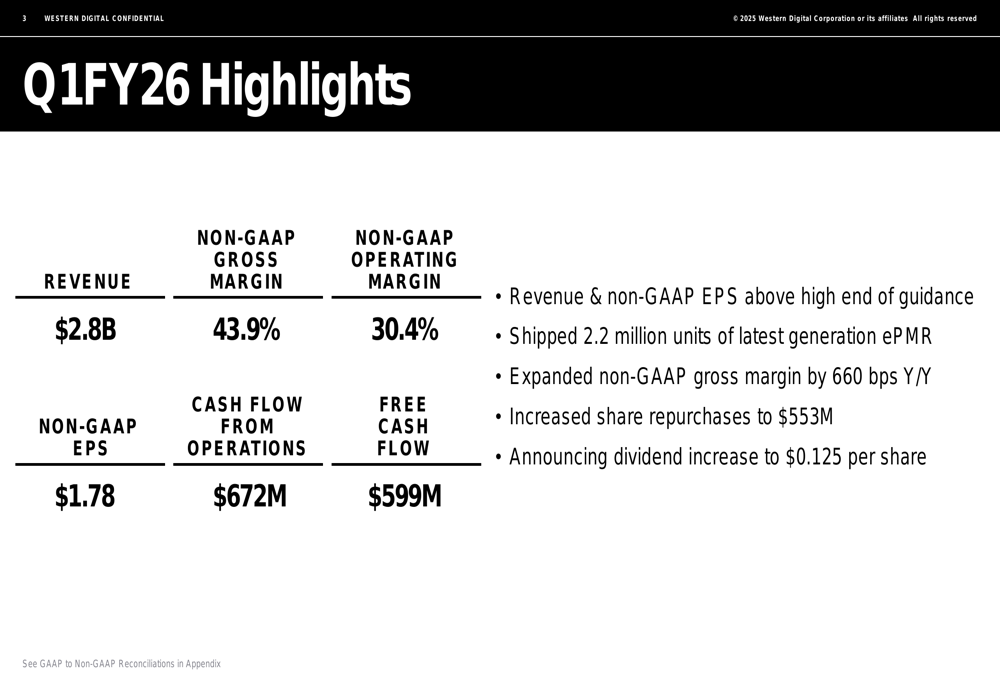

Western Digital reported Q1 FY2026 revenue of $2.8 billion, exceeding the high end of its guidance and representing a 27% increase year-over-year. Non-GAAP earnings per share reached $1.78, significantly outperforming the $1.58 analyst consensus and marking a 137% jump from the $0.75 reported in the same quarter last year.

As shown in the following quarterly highlights slide, the company achieved substantial improvements across all key financial metrics:

Notably, Western Digital expanded its non-GAAP gross margin by 660 basis points year-over-year to 43.9%, while non-GAAP operating margin reached 30.4%. The company generated $672 million in cash flow from operations and $599 million in free cash flow, enabling increased shareholder returns through both share repurchases ($553 million) and a 25% dividend increase to $0.125 per share.

Cloud Segment Dominance

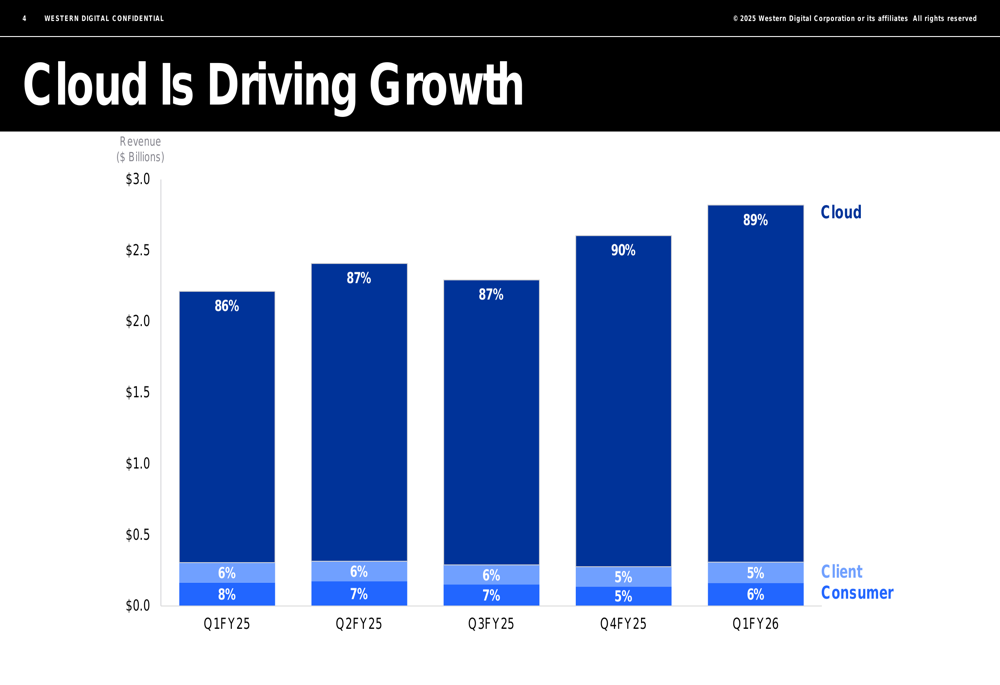

The company’s financial results clearly demonstrate the increasing dominance of its cloud business. The following chart illustrates how cloud services have steadily grown as a percentage of Western Digital’s revenue mix over the past five quarters:

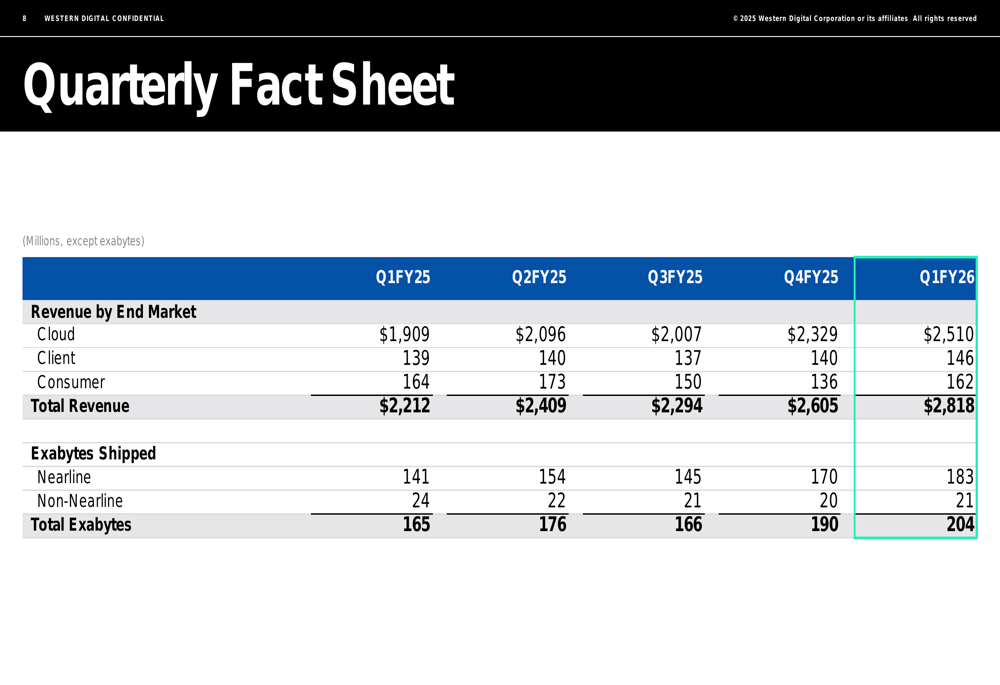

Cloud revenue accounted for 89% of total revenue in Q1 FY2026, compared to 86% in Q1 FY2025. In absolute terms, cloud revenue grew from $1.91 billion to $2.51 billion, representing a 31% year-over-year increase. This growth reflects Western Digital’s strategic focus on data center customers and the increasing demand for high-capacity storage solutions.

Meanwhile, client and consumer segments have diminished in relative importance, now representing just 5% and 6% of total revenue respectively, though both segments showed modest sequential growth.

Detailed Financial Analysis

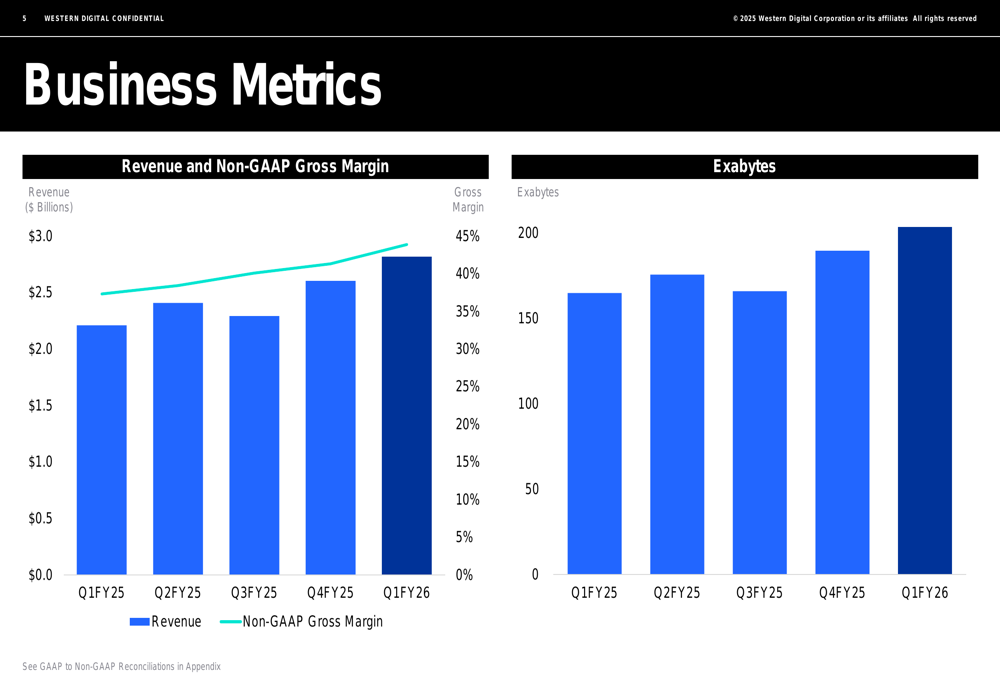

Western Digital’s business metrics reveal positive trends across revenue, margins, and storage capacity shipped:

The company shipped a record 204 exabytes during the quarter, up 23% year-over-year from 165 exabytes in Q1 FY2025. This increase in volume, combined with improved pricing and product mix, contributed to the significant revenue growth.

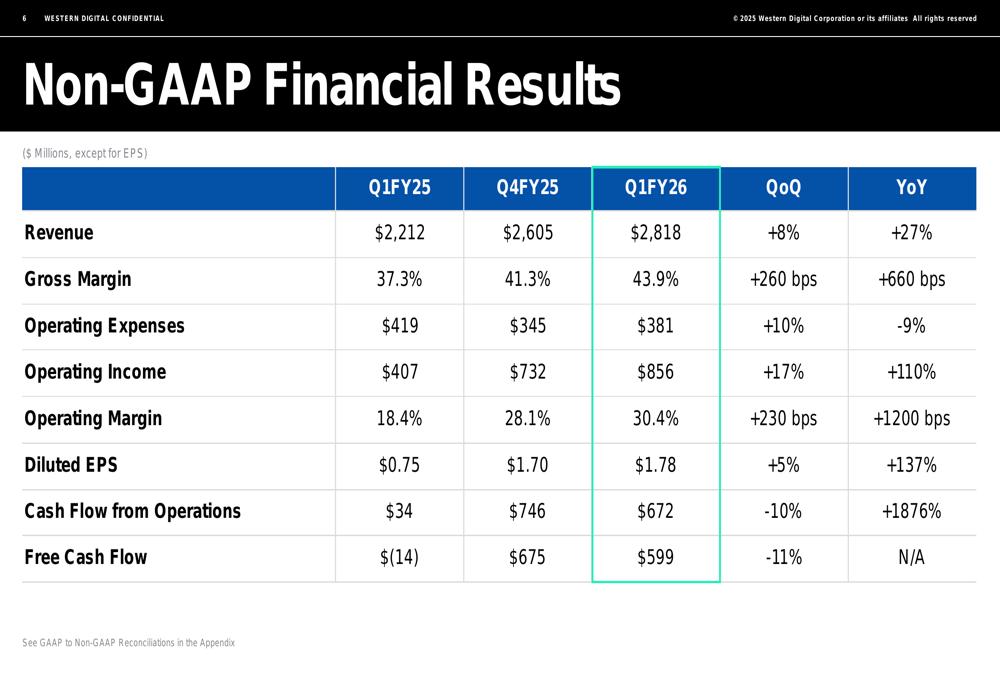

A detailed breakdown of Western Digital’s non-GAAP financial results shows substantial improvements across all key metrics:

Operating expenses increased slightly quarter-over-quarter from $345 million to $381 million but remained below the $419 million reported in Q1 FY2025. This disciplined cost management, combined with revenue growth, resulted in operating income of $856 million, more than double the $407 million from the same quarter last year.

The quarterly fact sheet provides additional insight into the company’s performance trends across different market segments:

Nearline storage, which primarily serves cloud data centers, continues to drive the majority of exabytes shipped, reaching 183 exabytes in Q1 FY2026 compared to 141 exabytes in Q1 FY2025. This trend underscores Western Digital’s increasing focus on high-capacity enterprise drives.

Forward-Looking Statements

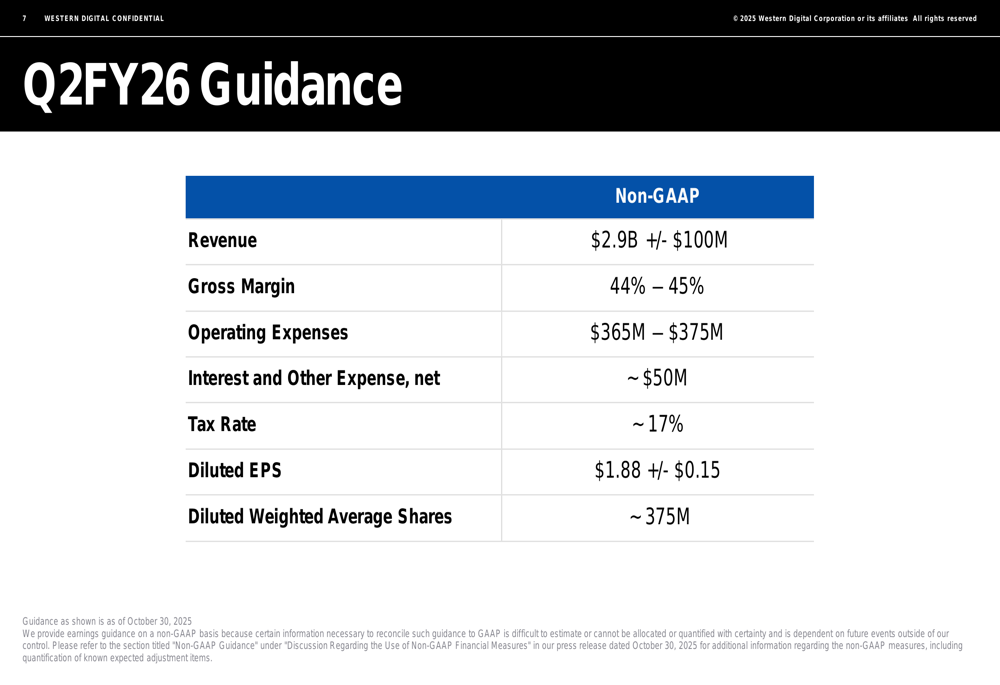

Looking ahead to the second quarter of fiscal 2026, Western Digital provided the following guidance:

The company expects revenue to reach $2.9 billion (plus or minus $100 million) in Q2 FY2026, representing sequential growth from Q1. Gross margin is projected to improve further to between 44% and 45%, while non-GAAP EPS is expected to reach $1.88 (plus or minus $0.15).

During the earnings call, CEO Irving Tan emphasized the strategic importance of data storage for artificial intelligence applications, stating, "Data is the fuel that powers AI, and it is HDDs that provide the most reliable, scalable, and cost-effective data storage solution." He also noted that the company is not currently adding unit capacity, focusing instead on technological advancements like HAMR (Heat-Assisted Magnetic Recording) to increase storage density.

Western Digital shipped 2.2 million units of its latest generation ePMR (Energy-assisted Perpendicular Magnetic Recording) drives during the quarter, with HAMR technology qualification expected to commence in the first half of 2026. However, management acknowledged that supply constraints are likely to persist through 2026, potentially limiting growth despite strong demand.

Market Reaction and Outlook

Despite exceeding analyst expectations, Western Digital’s stock declined 2.3% in after-hours trading following the earnings release. This reaction may reflect investor concerns about ongoing supply constraints and potential market saturation in the high-capacity drive segment.

The stock remains significantly above its 52-week low of $28.83 but below its recent high of $145.68, suggesting that while investors recognize the company’s improved performance, they remain cautious about future growth prospects in an increasingly competitive storage market.

Western Digital’s strategic focus on cloud and data center customers appears well-aligned with industry trends, particularly as AI applications drive demand for massive data storage solutions. However, the company faces challenges in managing supply constraints and maintaining its technological edge in an evolving storage landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.