Bitcoin price today: surges to $122k, near record high on US regulatory cheer

Introduction & Market Context

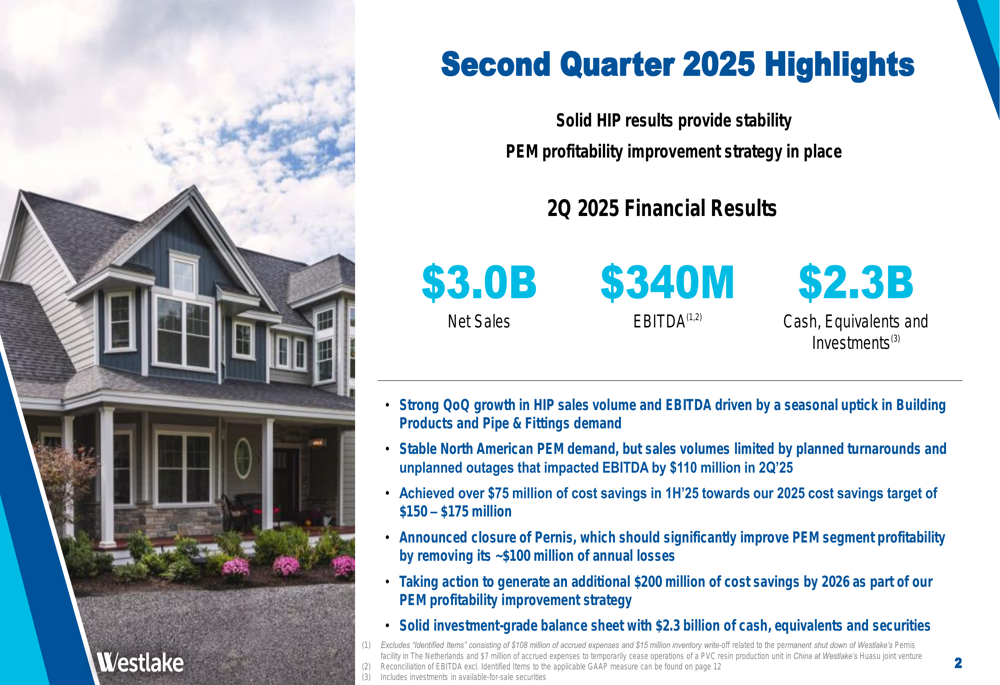

Westlake Chemical Corporation (NYSE:WLK) released its second quarter 2025 earnings presentation on August 5, 2025, revealing a company navigating through challenging market conditions with mixed results across its business segments. The chemical manufacturer reported $3.0 billion in net sales and $340 million in EBITDA, maintaining a solid cash position of $2.3 billion despite headwinds in the housing and chemical markets.

The presentation highlighted how elevated mortgage interest rates and diminished consumer confidence continue to impact single-family housing starts, which are trending below prior year levels. These market challenges were reflected in Westlake’s year-over-year performance decline, though the company showed sequential improvement from the first quarter.

Quarterly Performance Highlights

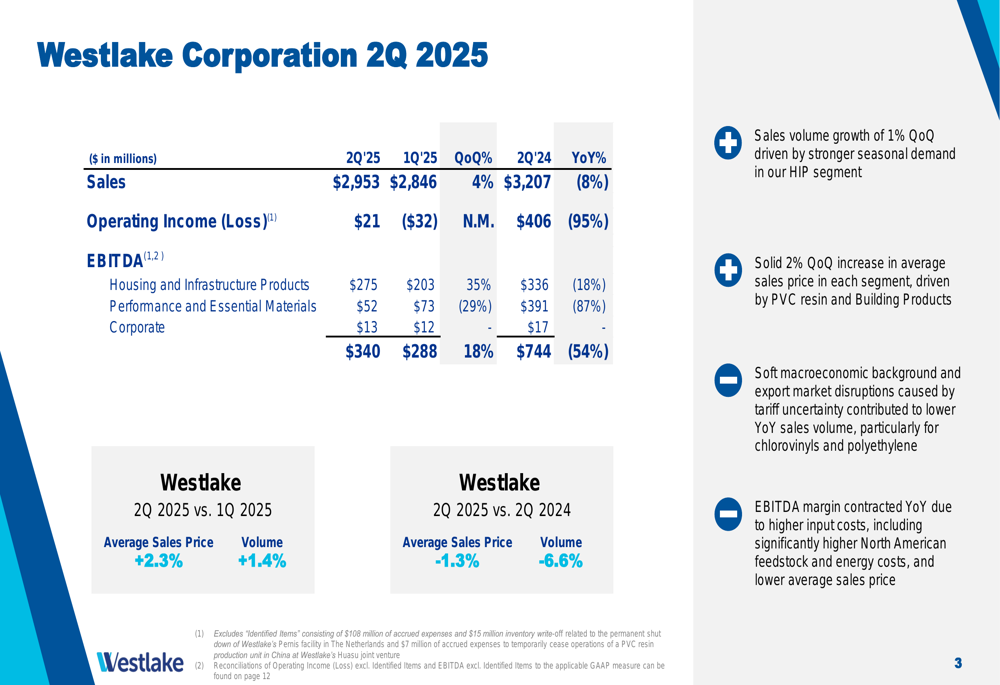

Westlake reported second quarter 2025 net sales of $2.95 billion, representing a 4% increase quarter-over-quarter but an 8% decrease year-over-year. EBITDA reached $340 million, improving 18% from Q1 2025 but declining 54% compared to Q2 2024. The company’s operating income recovered to $21 million from a $32 million loss in the previous quarter, though significantly below the $406 million reported in the same period last year.

According to the earnings call transcript, Westlake actually reported a net loss of $12 million, or $0.09 per share, for the quarter. This discrepancy between positive operating income and negative net income suggests that interest expenses, taxes, or other non-operating items offset the operational gains.

The company’s performance was impacted by $110 million in EBITDA due to planned turnarounds, while sales volume increased 1.4% quarter-over-quarter but decreased 6.6% year-over-year. Average sales prices showed a 2.3% sequential improvement but remained 1.3% lower than the previous year.

Segment Analysis

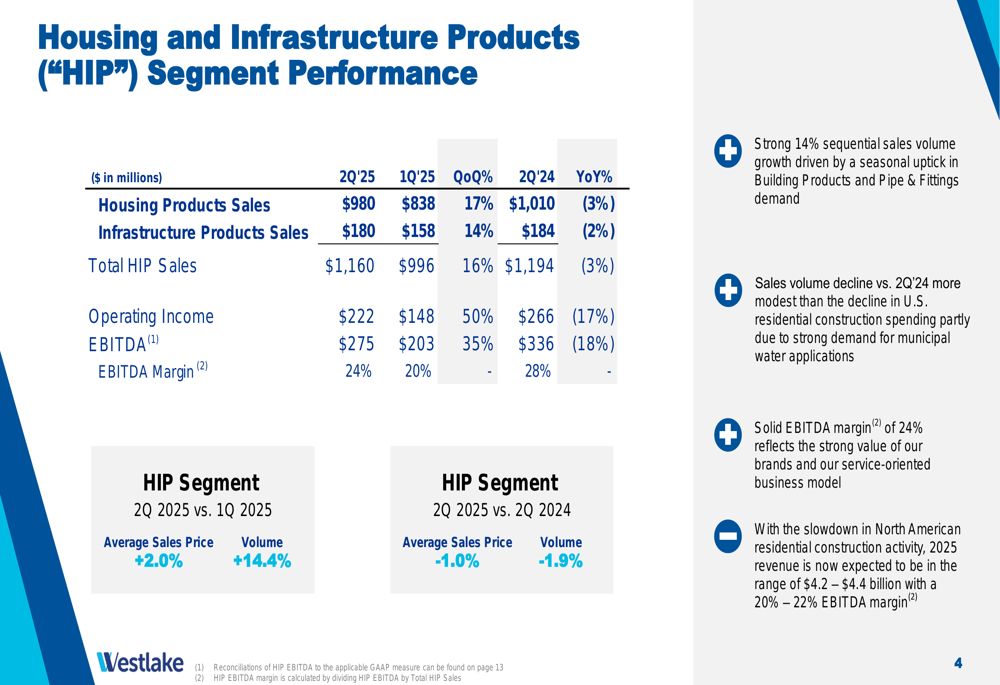

Westlake’s Housing and Infrastructure Products (HIP) segment demonstrated remarkable resilience, generating $1.16 billion in sales and $275 million in EBITDA with an impressive 24% margin. The segment benefited from strong sequential sales volume growth of 14.4%, though volumes were still 1.9% below the previous year.

As shown in the following detailed breakdown of the HIP segment performance:

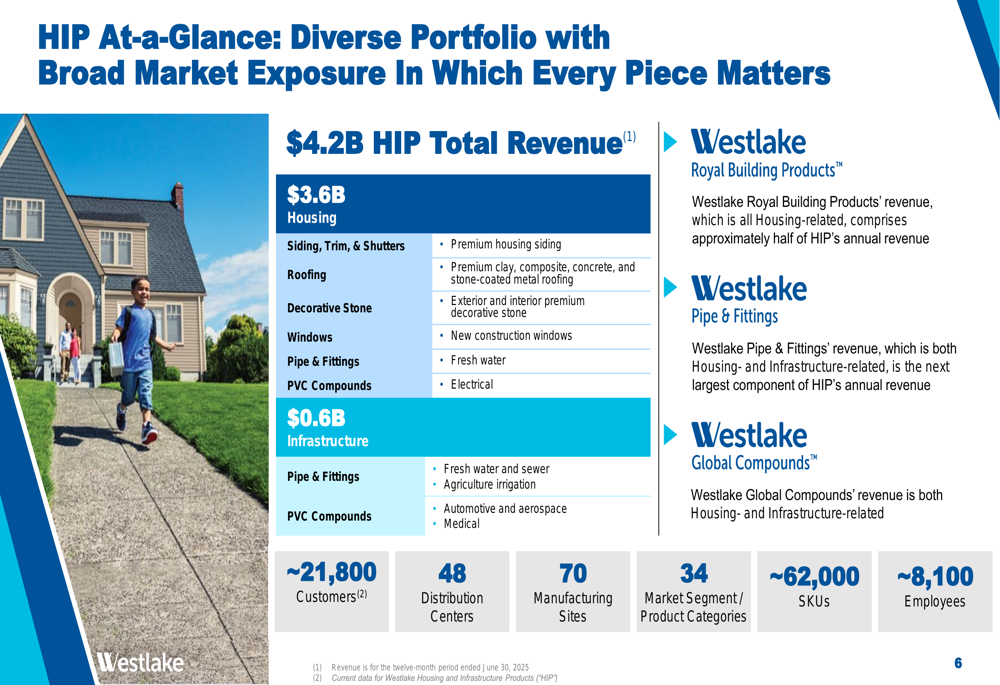

The HIP segment’s strength stems from its diverse portfolio spanning 34 market segments with approximately 62,000 SKUs. The business operates 70 manufacturing sites and 48 distribution centers, serving around 21,800 customers. This diversification has helped shield the segment from some of the broader market challenges.

The following slide illustrates the extensive reach of Westlake’s HIP business:

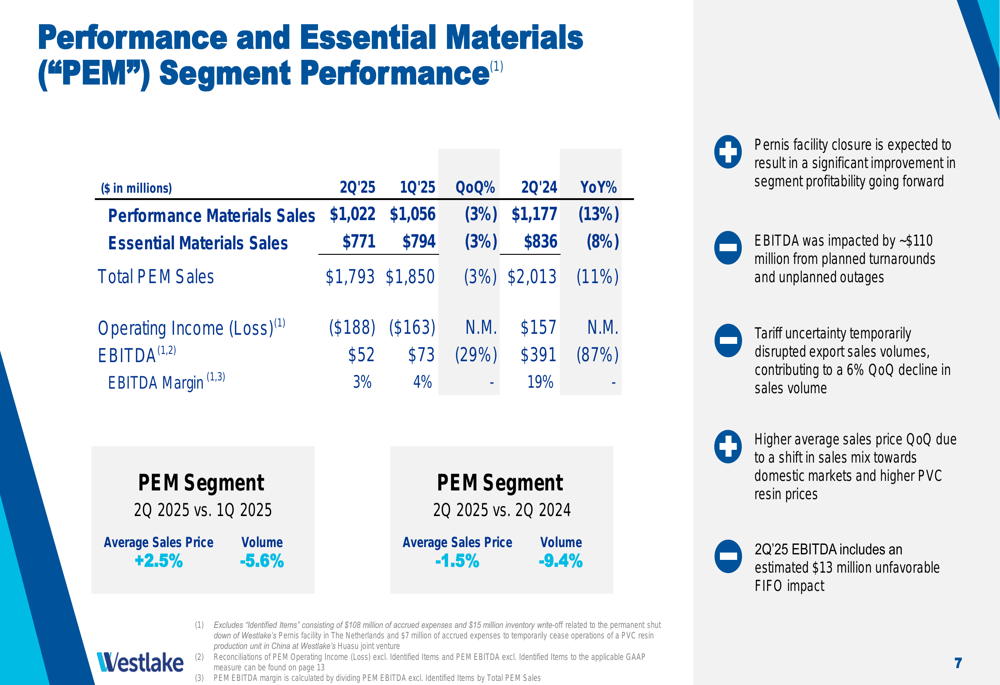

In contrast, the Performance and Essential Materials (PEM) segment continued to struggle, reporting $1.79 billion in sales but only $52 million in EBITDA, resulting in a thin 3% margin. The segment saw a 3% sequential decline in sales and an 11% year-over-year decrease. PEM’s operating income was negative $188 million for the quarter, highlighting the significant challenges in this business unit.

Strategic Initiatives & Cost Reduction

Westlake’s presentation emphasized several strategic initiatives aimed at improving profitability, particularly in the struggling PEM segment. The company has achieved $75 million in cost savings during the first half of 2025 and announced plans to generate an additional $200 million in savings by 2026.

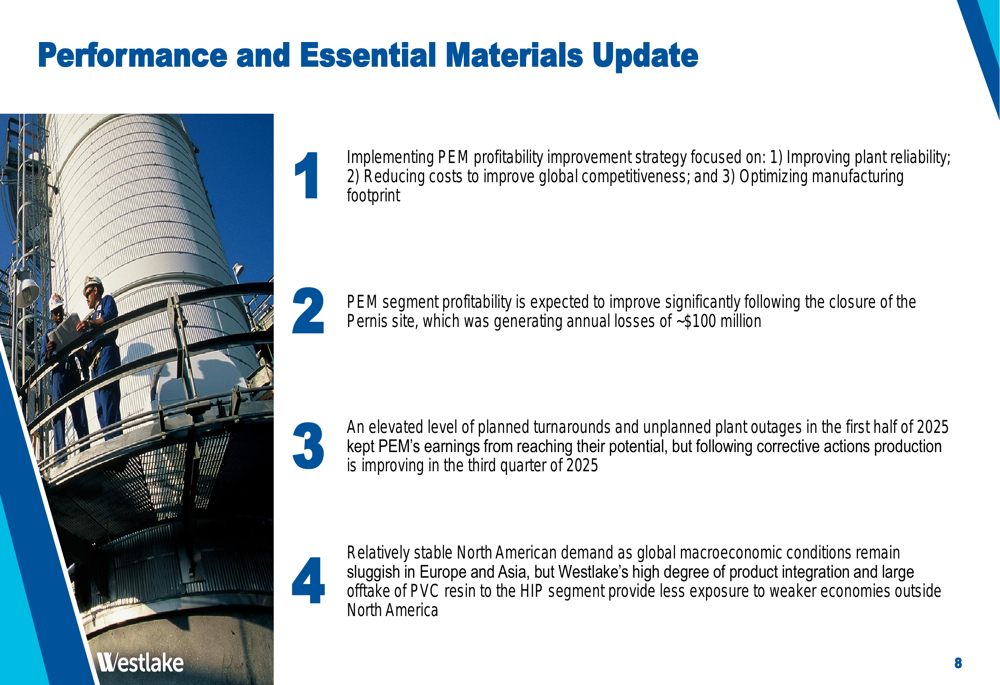

A centerpiece of Westlake’s strategy is the announced closure of its Pernis factory, which has been generating approximately $100 million in annual losses. Management expects this closure to significantly improve the PEM segment’s profitability going forward.

The company outlined its PEM profitability improvement strategy, focusing on three key areas:

"We continue to see a very bright future for HIP," stated Jean Marc Gilson, President and CEO, according to the earnings call transcript. CFO Steve Bender emphasized the structural nature of the company’s cost-cutting measures, noting, "These actions are structural and really sticky."

Forward Outlook

Despite current challenges, Westlake maintains an optimistic outlook for its HIP segment, projecting 2025 revenue between $4.2 billion and $4.4 billion with an EBITDA margin of 20-22%. The company expects PEM sales volumes to improve in the third quarter as production recovers following the completion of planned turnarounds that impacted first-half results.

Westlake emphasized that longer-term housing fundamentals remain strong, providing a positive backdrop for its HIP segment. Meanwhile, the company’s solid investment-grade balance sheet with $2.3 billion in cash and equivalents provides financial flexibility to navigate current market challenges.

For the PEM segment, management expects significant improvement following the Pernis site closure and implementation of its profitability improvement strategy. The company noted that tariff uncertainty temporarily disrupted export sales volumes, but anticipates stabilization as market conditions normalize.

Westlake’s stock remained stable at $66.21 per share following the earnings release, suggesting that investors had already priced in the mixed results and are taking a wait-and-see approach to the company’s strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.