BofA update shows where active managers are putting money

Introduction & Market Context

Westport Fuel Systems Inc. (NASDAQ:WPRT) presented its first quarter 2025 results on May 14, highlighting improved profitability metrics despite revenue challenges. The alternative fuel systems provider’s stock closed at $2.85 on May 15, up 1.06% following the presentation, as investors responded to the company’s progress in its strategic repositioning and improved bottom line.

The company is navigating a significant transition period, with the proposed divestiture of its Light-Duty segment for $73.1 million (€67.7 million) announced on March 31, 2025, and its Cespira joint venture becoming an increasingly important revenue contributor.

Quarterly Performance Highlights

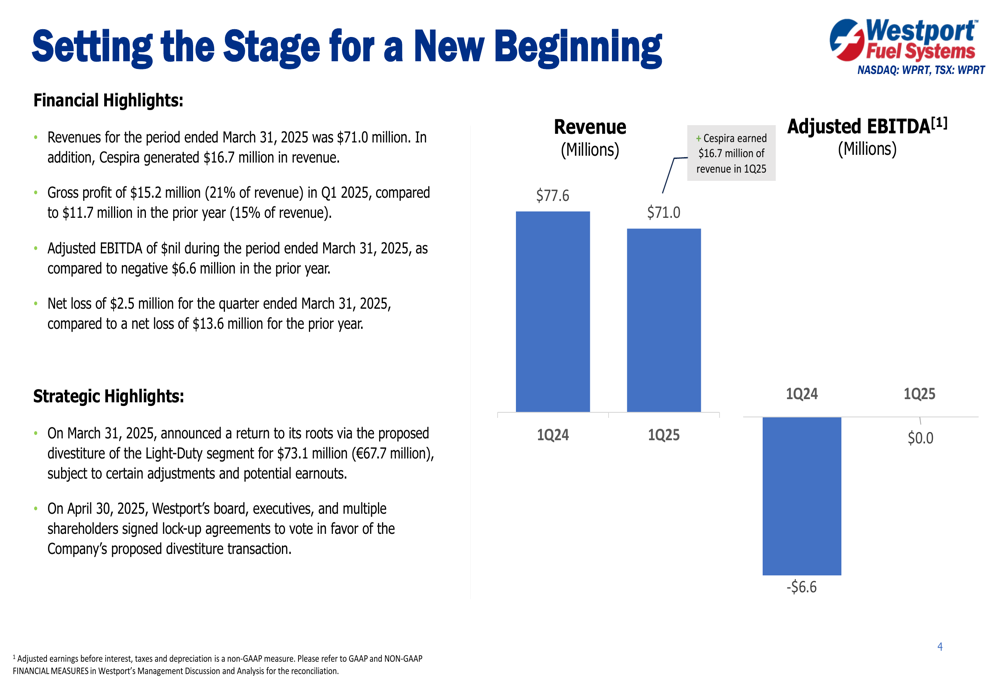

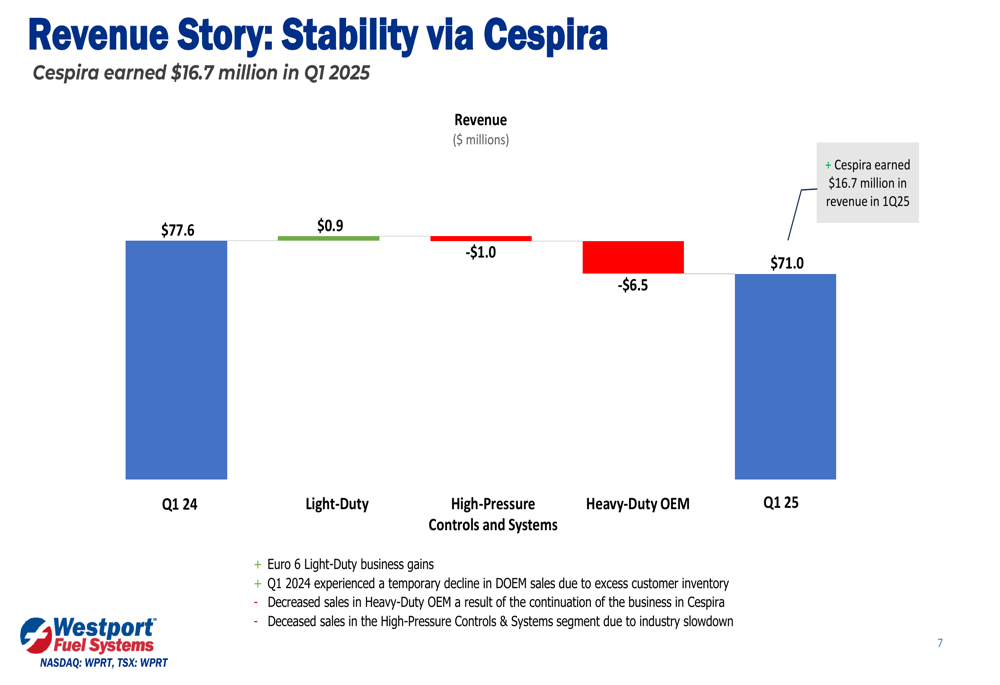

Westport reported revenues of $71.0 million for Q1 2025, plus an additional $16.7 million from Cespira, compared to $77.6 million in the same period last year. Despite the revenue decline in its core business, the company demonstrated substantial improvements in profitability metrics.

Gross profit increased to $15.2 million (21% of revenue), compared to $11.7 million (15%) in the prior year. Adjusted EBITDA reached breakeven, a significant improvement from -$6.6 million in Q1 2024. Net loss narrowed considerably to $2.5 million, compared to a net loss of $13.6 million in the prior year.

As shown in the following financial highlights chart from the presentation:

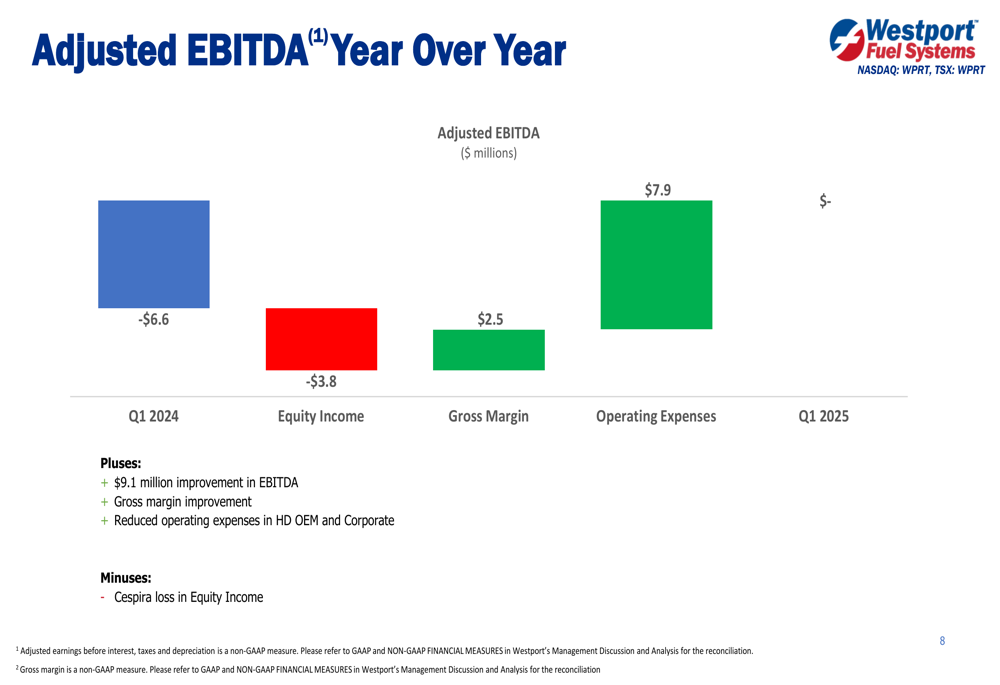

The company’s adjusted EBITDA bridge analysis reveals that the $6.6 million improvement was driven by increased gross margin ($2.5 million impact) and reduced operating expenses ($7.9 million impact), partially offset by equity income impacts (-$3.8 million) related to Cespira:

Segment Performance Analysis

Westport’s segment performance showed mixed results across its business units. The Light-Duty segment, which is slated for divestiture, showed modest growth with revenue increasing 1% to $64.2 million and gross margin improving from 20% to 22%.

In contrast, the High-Pressure Controls and Systems segment experienced a 42% revenue decrease to $1.4 million, with gross margin declining from 17% to 14%. The company attributed this decline to a general slowdown in hydrogen infrastructure development and lower sales volumes increasing manufacturing costs.

The Heavy-Duty OEM segment saw a more dramatic 55% revenue decrease to $5.4 million, with gross margin falling from 19% to negative 9%. This decline reflects the ongoing transition of this business to the Cespira joint venture, which contributed $16.7 million in revenue with a gross margin of 3%.

The company’s revenue breakdown illustrates these shifts across segments:

Strategic Initiatives

Westport outlined three key strategic priorities in its presentation: driving success via the HPDI joint venture, improving operational excellence and reducing costs, and shaping a future powered by alternative fuels.

The company emphasized that its product strategy is "timeline agnostic," meeting current market needs while providing solutions for when hydrogen becomes more widely available. In the near term, natural gas (including renewable natural gas) provides significant opportunities to decarbonize heavy-duty and off-road applications.

As illustrated in the company’s product timeline:

The proposed divestiture of the Light-Duty segment represents a strategic pivot to focus on providing solutions for hard-to-decarbonize applications. Management noted that the board, executives, and multiple shareholders signed lock-up agreements in favor of the divestiture on April 30, 2025, with the shareholder vote expected in late Q2 2025.

CEO Dan Sceli and CFO Bill Larkin, who presented the results, emphasized this strategic repositioning:

Forward-Looking Statements

Westport’s liquidity position showed some changes, with cash decreasing from $37.6 million in Q4 2024 to $32.6 million in Q1 2025, while debt decreased from $33.7 million to $31.1 million in the same period. The company noted that cash was used in operating activities ($4.9 million) and for debt repayment ($3.9 million).

Looking ahead, Westport emphasized that it is delivering practical applications today while positioning for future growth. The company highlighted its continued improvement in key financial metrics, with Cespira generating increased revenue and improving gross profits.

The company’s closing summary emphasized several key points:

The strategic sale of the Light-Duty segment is expected to strengthen the balance sheet and provide focus on strategic growth opportunities, particularly in fuel system solutions for clean, low-carbon fuels. With this repositioning, Westport aims to maintain its leadership in providing solutions for hard-to-decarbonize applications, with natural gas viewed not merely as a bridge to hydrogen but as a foundation for the future of alternative fuels.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.