German construction sector still in recession, civil engineering only bright spot

John Wiley & Sons (NYSE:WLY) presented its fourth quarter and fiscal year 2025 earnings results on June 17, 2025, highlighting strong performance across key metrics and significant margin expansion. The academic and professional publisher’s stock surged nearly 10% following the announcement, reflecting investor confidence in the company’s growth strategy and improving financial position.

Introduction & Market Context

Wiley’s shares closed at $40.72, up 9.96% following the earnings presentation, as investors responded positively to the company’s financial results and outlook. The stock has traded between $36.50 and $53.96 over the past 52 weeks.

The company has positioned itself as a beneficiary of artificial intelligence development, with AI licensing revenue reaching $40 million in fiscal 2025. This strategic pivot comes amid Wiley’s continued focus on authoritative content and data-driven insights for science, innovation, and learning markets.

Quarterly Performance Highlights

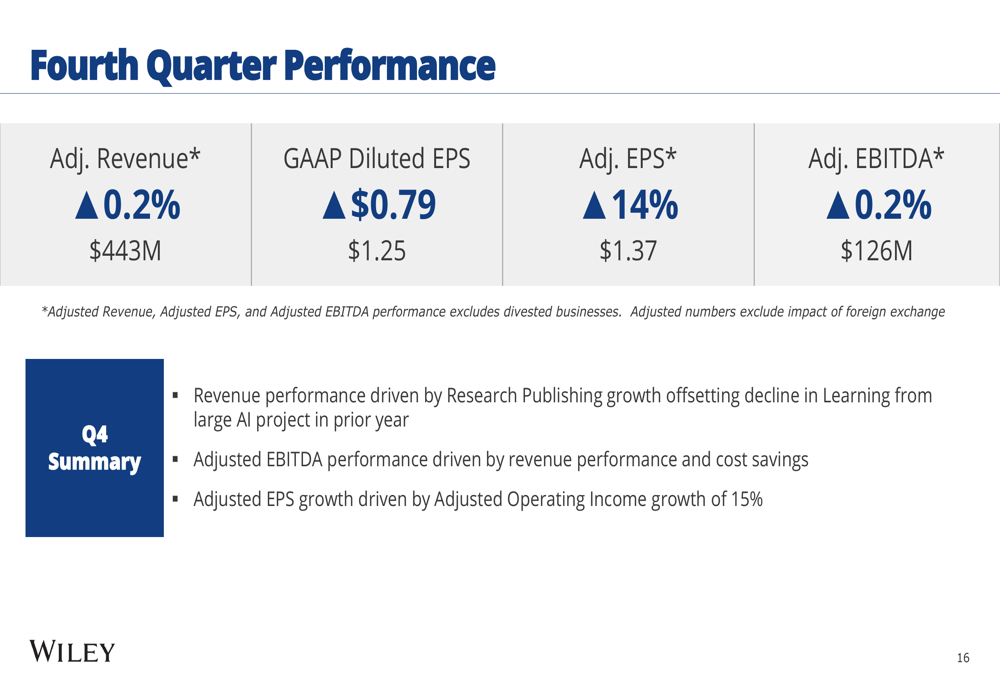

In the fourth quarter of fiscal 2025, Wiley reported adjusted revenue of $443 million, a slight increase of 0.2% year-over-year. Adjusted earnings per share rose 14% to $1.37, while adjusted EBITDA increased marginally by 0.2% to $126 million.

As shown in the following slide detailing Q4 performance, the company exceeded analyst expectations for the quarter:

The Research segment drove Q4 revenue growth with a 4% increase to $281 million, offsetting a 5% decline in Learning revenue, which fell to $162 million. Research Publishing was particularly strong, growing 4% to $243 million, while Professional revenue within the Learning segment declined 13% to $62 million.

Fiscal Year 2025 Results

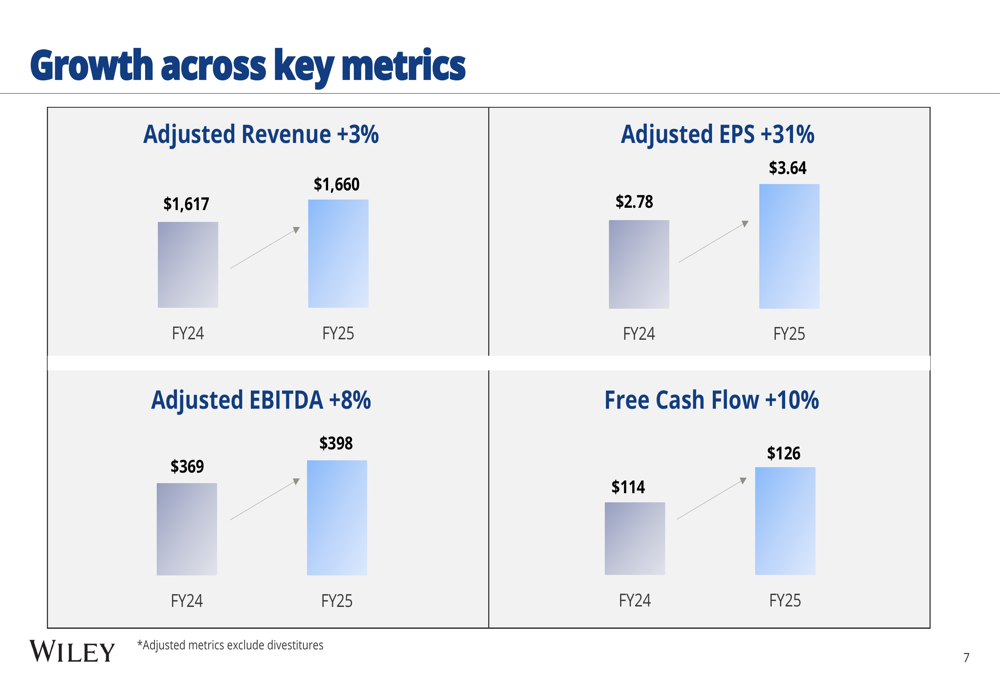

For the full fiscal year 2025, Wiley delivered solid growth across all key financial metrics. Adjusted revenue increased 3% to $1.66 billion, adjusted EPS jumped 31% to $3.64, and adjusted EBITDA grew 8% to $398 million. Free cash flow improved 10% to $126 million.

The following chart illustrates the company’s growth across these key metrics:

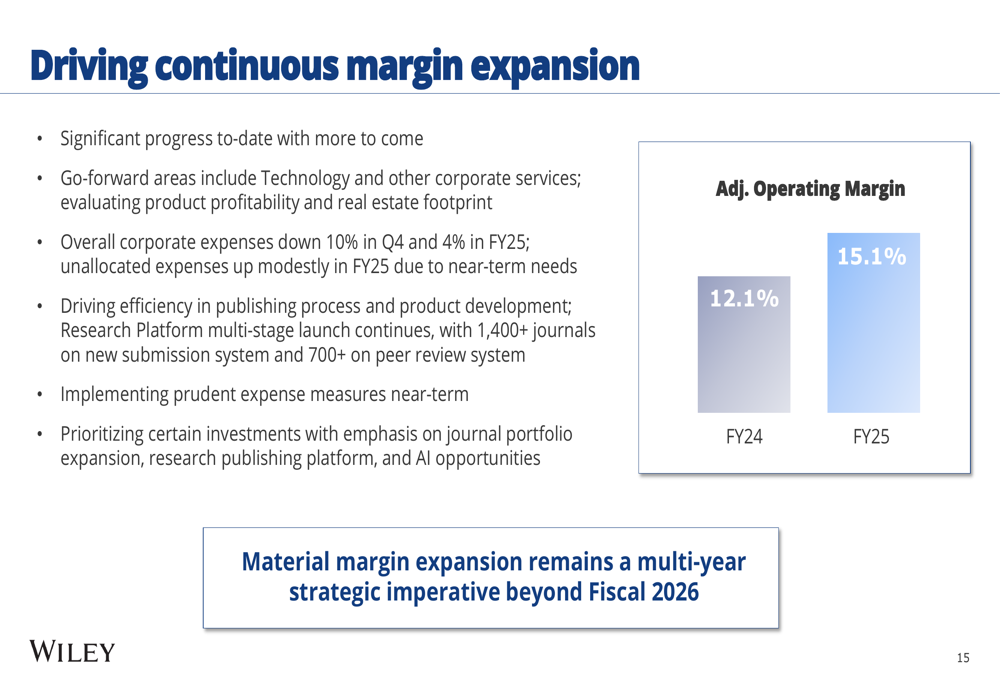

Wiley’s adjusted operating margin expanded significantly, increasing 300 basis points to 15.1%, while adjusted EBITDA margin improved 120 basis points to 24.0%. This margin expansion reflects the company’s focus on operational efficiency and cost management.

The company’s margin improvement strategy is detailed in this slide:

By segment, Research revenue grew 3% to $1.075 billion for the fiscal year, with Research Publishing up 3% to $923 million and Research Solutions up 2% to $152 million. Learning revenue increased 2% to $585 million, with Academic revenue up 3% to $334 million while Professional revenue remained flat at $251 million.

Strategic Initiatives

Wiley has made significant progress in its AI licensing business, securing a third major AI model training customer in Q4 and generating $40 million in AI licensing revenue for the fiscal year. The company is building momentum for vertical-specific licensing and partnerships with R&D-centric corporations.

Research performance has been robust, with article submissions up 19% and article output up 8%, driving a 3% increase in Research revenue. The company continues to benefit from strong demand across key markets, particularly in high-growth regions like India, Brazil, and China.

The following slide highlights the company’s research recovery and growth:

In the Learning segment, Inclusive Access grew 22% and Professional Title Signings increased 16%, contributing to a 2% rise in Learning revenue. Digital content and courseware continue to show steady growth.

The company’s learning growth is illustrated in this slide:

Wiley’s business model demonstrates resilience in an uncertain economic environment, with 48% recurring revenue, 83% digital and services revenue, and 49% of revenue generated outside the United States. This diversification provides stability and reduces exposure to any single market.

Forward-Looking Statements

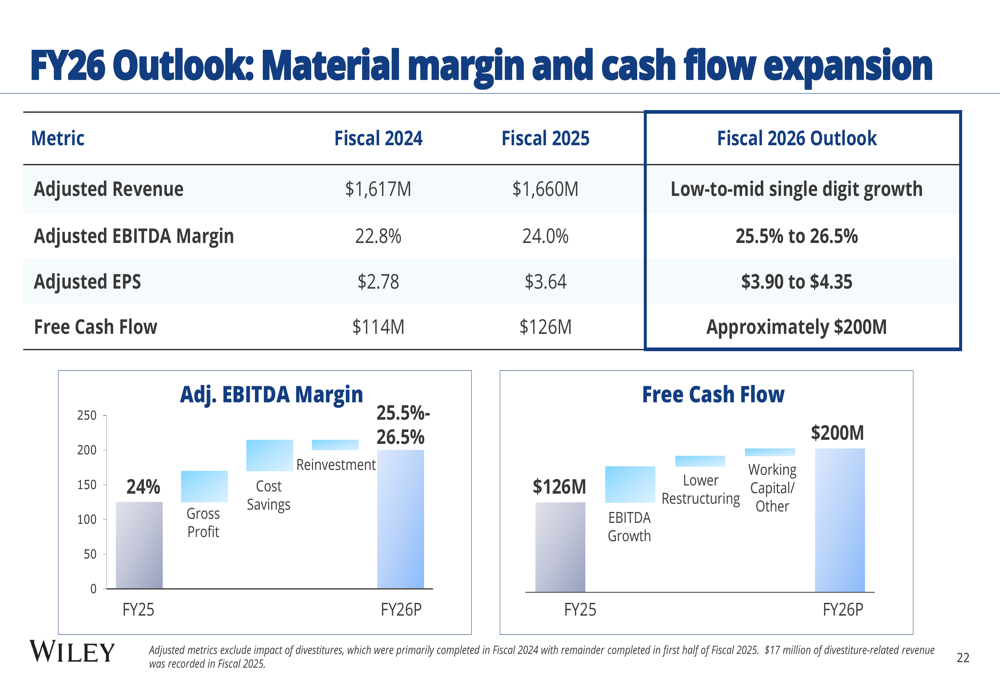

Looking ahead to fiscal 2026, Wiley provided an optimistic outlook, projecting low-to-mid single-digit growth in adjusted revenue, an adjusted EBITDA margin of 25.5% to 26.5%, adjusted EPS of $3.90 to $4.35, and free cash flow of approximately $200 million.

The company’s detailed outlook for fiscal 2026 is presented in this slide:

Wiley expects continued growth in its Research segment, driven by good subscription growth, strong publishing demand, and improved execution in Solutions. In Learning, the company anticipates steady market conditions, a strong Professional frontlist, and a new product launch in Assessments. AI licensing opportunities are expected to continue contributing to revenue growth.

The company remains focused on delivering profitable revenue growth, materially expanding margins, and driving continued momentum in the corporate market. Management emphasized that material margin expansion remains a multi-year strategic imperative beyond fiscal 2026.

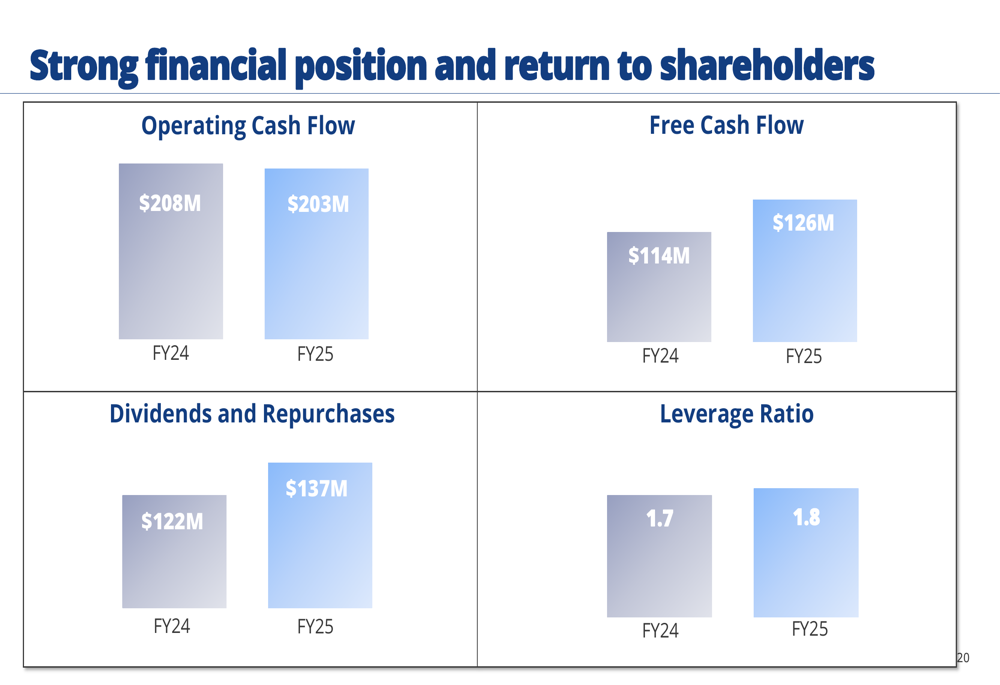

Wiley’s financial position remains strong, with operating cash flow of $203 million and a leverage ratio of 1.8x in fiscal 2025. The company returned $137 million to shareholders through dividends and share repurchases, up from $122 million in the previous year.

The following slide illustrates Wiley’s financial position and shareholder returns:

With its diversified revenue streams, growing AI licensing business, and focus on margin expansion, John Wiley & Sons appears well-positioned to continue delivering value to shareholders in fiscal 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.