Gold prices edge higher on raised Fed rate cut hopes

Introduction & Market Context

Winnebago Industries (NYSE:WGO) released its fiscal 2025 third quarter earnings presentation on June 25, 2025, revealing continued challenges in its core RV business while highlighting pockets of strength in its diversified portfolio. The company’s stock, which closed at $31.33 on June 24, showed minimal movement in premarket trading, reflecting the mixed nature of the results against a backdrop of ongoing industry headwinds.

The presentation comes after Winnebago’s stock has struggled in recent months, trading near its 52-week low of $28.29, far from its high of $65.65. The outdoor recreation industry continues to face macroeconomic uncertainty, with particular pressure on the motorhome segment where inventory destocking remains a significant factor.

Quarterly Performance Highlights

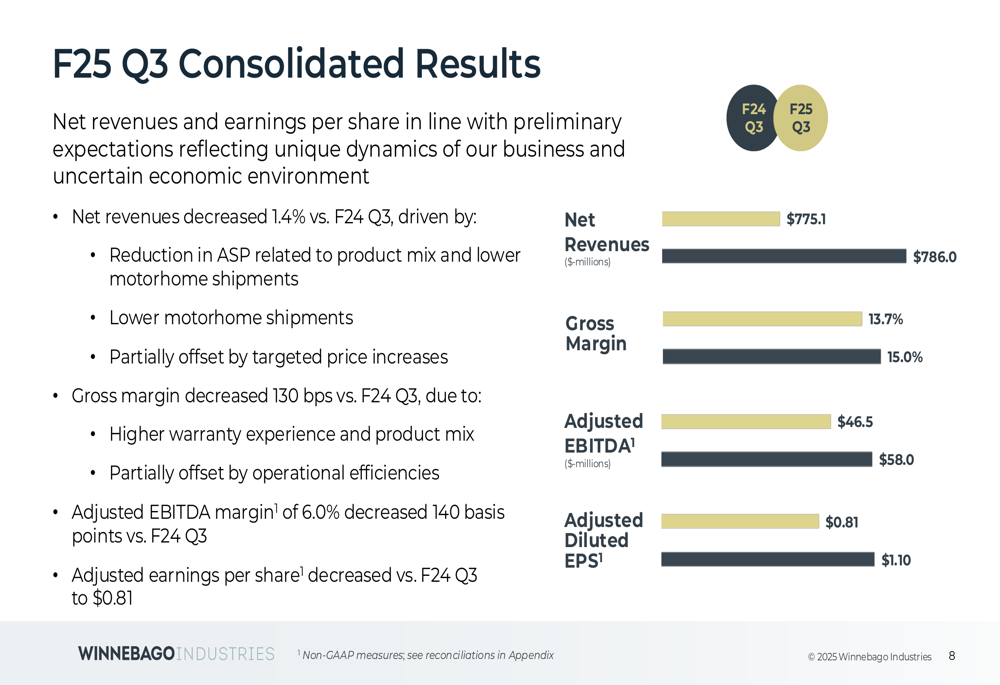

Winnebago reported consolidated net revenues of $775.1 million for the third quarter, representing a 1.4% decrease compared to $786.0 million in the same period last year. The decline was primarily attributed to average selling price (ASP) reductions across segments.

Profitability metrics showed more pronounced weakness, with gross margin decreasing 130 basis points year-over-year to 13.7%. Adjusted EBITDA fell to $46.5 million from $58.0 million in the prior year, with margins contracting 140 basis points to 6.0%. Adjusted earnings per share declined to $0.81 from $1.10 in the third quarter of fiscal 2024.

As shown in the following consolidated results chart:

Free cash flow turned negative at -$81.7 million for the quarter, compared to positive $69.4 million in the same period last year, reflecting working capital challenges and ongoing capital investments.

Segment Analysis

The company’s performance varied significantly across its three main business segments, with Marine standing out as the lone bright spot.

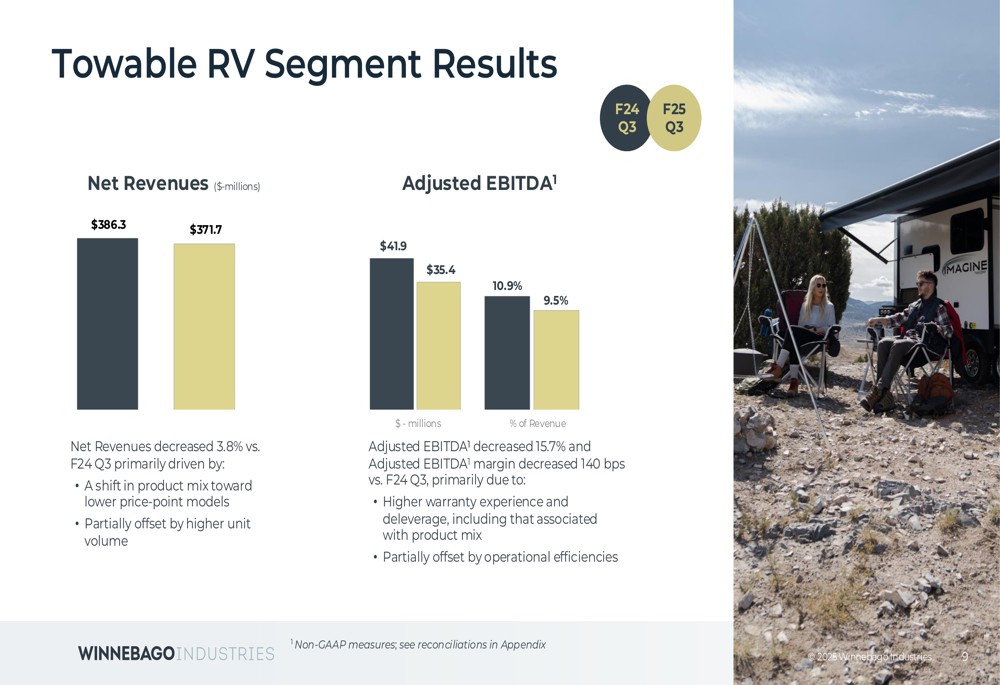

The Towable RV segment, which includes Grand Design and Winnebago branded products, saw net revenues decrease 3.8% to $371.7 million, primarily due to a shift toward lower-priced models. Adjusted EBITDA fell 15.7% to $35.4 million, with margins contracting 140 basis points to 9.5%, largely due to higher warranty expenses.

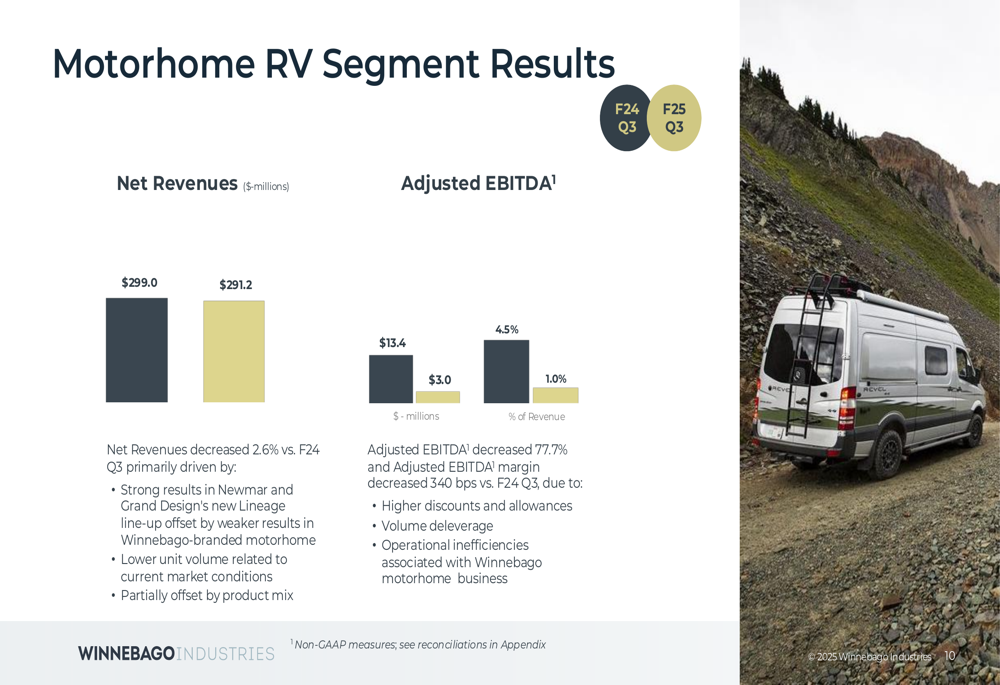

The Motorhome RV segment experienced the most significant challenges, with revenues declining 2.6% to $291.2 million despite strong results from Newmar and Grand Design’s new Lineage product. More concerning was the 77.7% drop in Adjusted EBITDA to just $3.0 million, with margins plummeting 340 basis points to 1.0%. The company attributed this to higher discounts and allowances needed to move inventory.

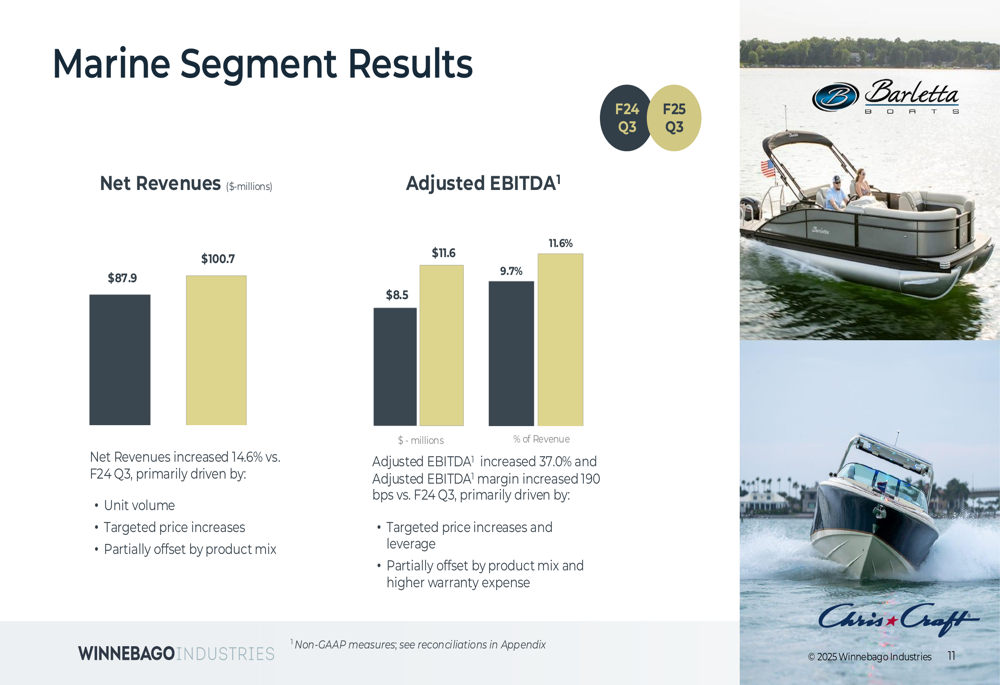

In stark contrast, the Marine segment delivered impressive results, with revenues increasing 14.6% to $100.7 million, driven by higher unit volumes. Adjusted EBITDA grew 37.0% to $11.6 million, with margins expanding 190 basis points to 11.6%. The strong performance of both Barletta pontoons and Chris-Craft luxury boats highlights the success of Winnebago’s diversification strategy.

Strategic Initiatives

Winnebago outlined several key strategic initiatives aimed at addressing current challenges while positioning the company for long-term growth. Management is taking decisive steps to improve performance in the struggling Motorhome segment, including new leadership, working capital improvements, and inventory reduction efforts.

The company is also implementing broader cost reduction measures and manufacturing optimization to build organizational resilience. Innovation remains a priority, with recent product launches including the Grand Design Lineage Series VT, Chris-Craft Catalina 31, Winnebago Thrive, and Newmar Freedom Aire Compact C.

As illustrated in the key messages slide:

Market Position & Competitive Landscape

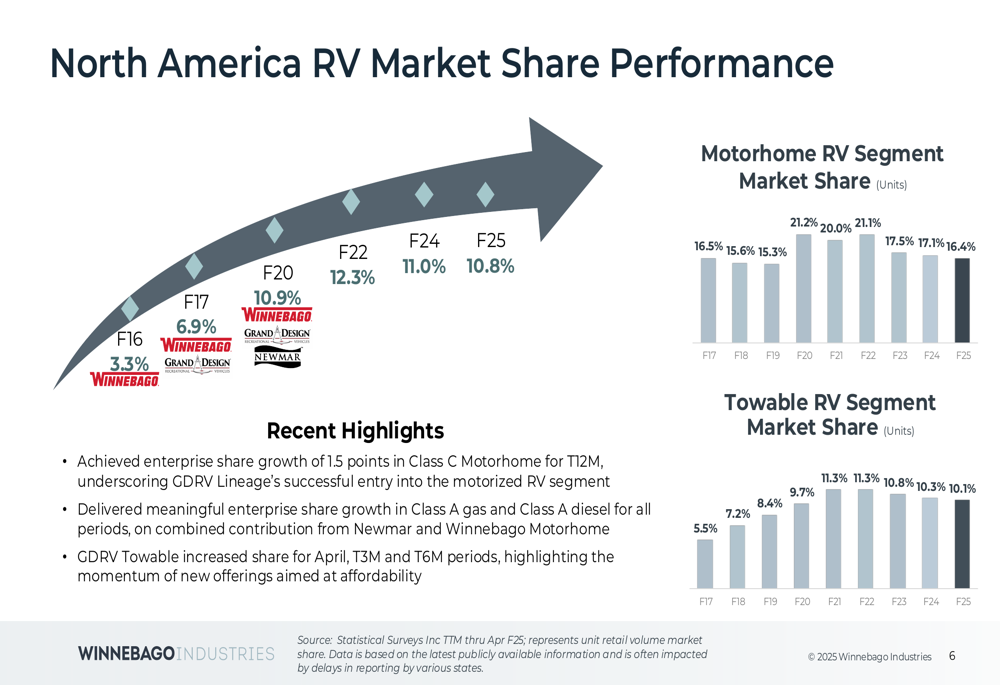

Despite current challenges, Winnebago has maintained or improved its market position across key segments. In the Motorhome RV segment, market share has remained relatively stable at 16.4% compared to 16.5% in fiscal 2017. The company achieved 1.5 percentage points of growth in the Class C Motorhome category, partly due to Grand Design Lineage’s successful entry into motorized RVs.

The Towable RV segment has seen more significant gains, with market share growing from 5.5% in fiscal 2017 to 10.1% in fiscal 2025. Grand Design Towable increased share for the April, trailing three-month, and trailing six-month periods.

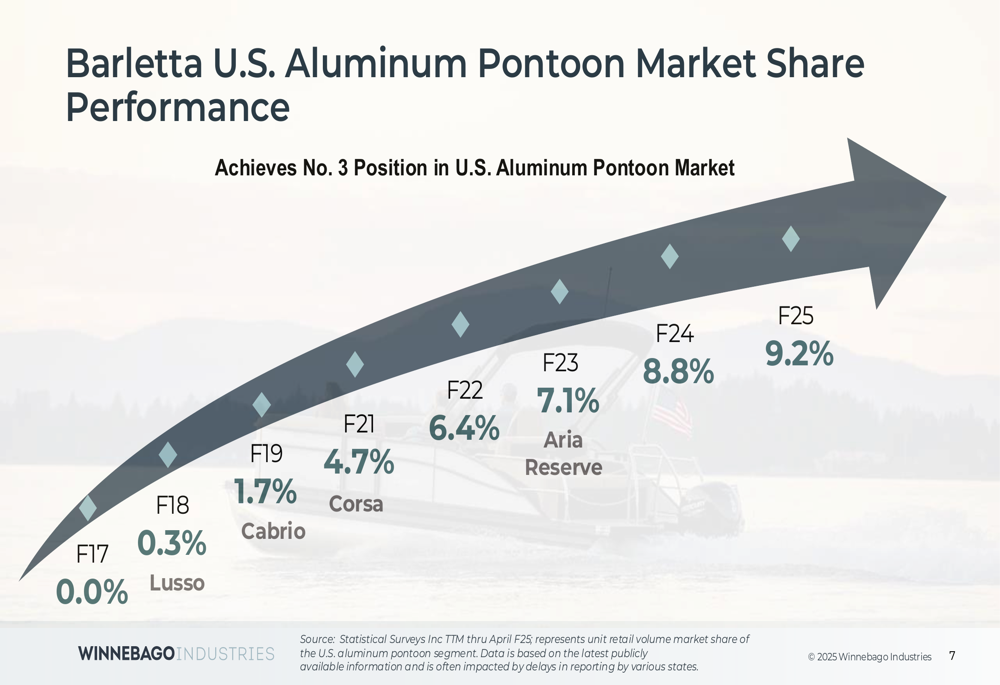

Perhaps most impressive is Barletta’s rise to the No. 3 position in the U.S. Aluminum Pontoon market, growing from zero market share in fiscal 2017 to 9.2% in fiscal 2025.

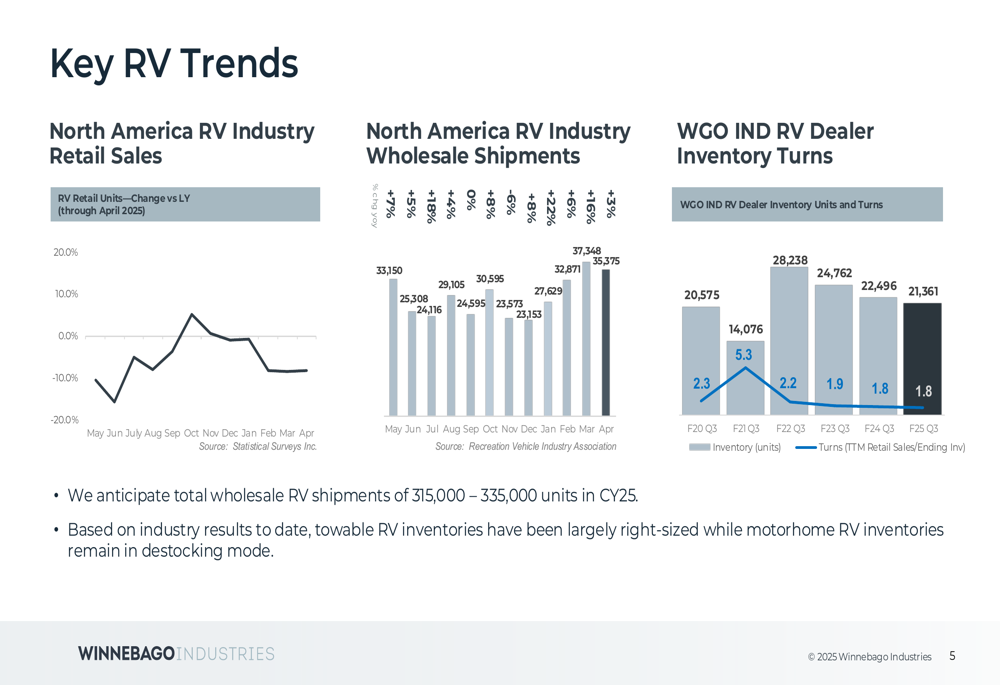

The broader RV industry continues to face challenges, with the company noting that while towable RV inventories have largely normalized, motorhome inventories remain in destocking mode. Winnebago anticipates total wholesale RV shipments of 315,000-335,000 units for calendar year 2025.

Revised Guidance & Outlook

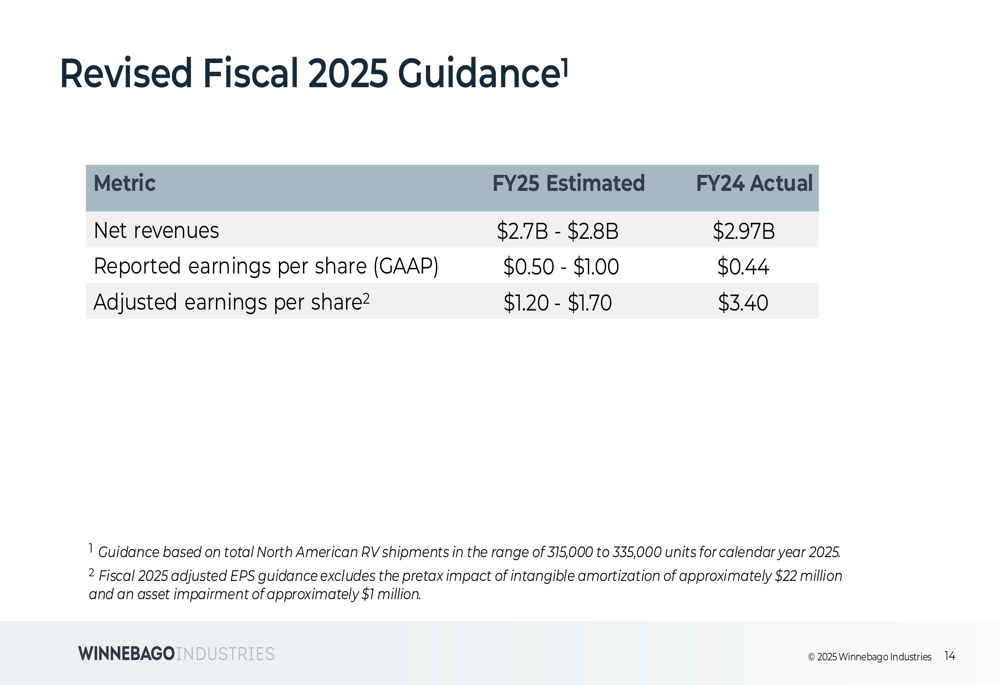

In response to ongoing challenges, Winnebago revised its fiscal 2025 guidance downward. The company now expects net revenues of $2.7-$2.8 billion, compared to the $2.8-$3.0 billion range provided in the previous quarter. Reported earnings per share (GAAP) are projected at $0.50-$1.00, with adjusted earnings per share of $1.20-$1.70.

This represents a significant decline from fiscal 2024 actual results of $2.97 billion in revenue and $3.40 in adjusted EPS.

The company also addressed potential tariff impacts, noting that while mitigation actions are expected to offset the majority of tariff impacts in fiscal 2025, there remains a potential net risk of between $0.50 and $0.75 of diluted EPS for fiscal 2026.

Balance Sheet & Capital Allocation

Winnebago emphasized its disciplined approach to capital allocation, highlighting a track record of reinvesting in profitable growth, making strategic acquisitions, and returning cash to shareholders. Recent financial actions include completing a $100 million tender offer for 6.25% Senior Secured Notes in Q2 and paying off $59 million of convertible debt in Q3.

The company’s differentiated position in the outdoor recreation market is supported by its portfolio of premium brands, enterprise-wide centers of excellence, technology investments, and flexible operating model.

Conclusion

Winnebago’s third quarter fiscal 2025 results reflect a company navigating significant industry headwinds, particularly in its core RV business. While the Marine segment provides a bright spot with double-digit growth, challenges in the Motorhome segment have prompted management to lower full-year guidance and implement strategic initiatives to address performance issues.

The company’s market share gains across segments and product innovation efforts provide some positive indicators for long-term growth, but investors will likely remain cautious given the current profitability challenges and uncertain macroeconomic environment. With the stock trading near 52-week lows, Winnebago’s ability to execute on its strategic initiatives and navigate industry destocking will be crucial for potential recovery in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.