TSX runs higher on rate cut expectations

Wolverine Worldwide (NYSE:WWW) shares jumped 3.83% in premarket trading to $24.40 following the release of its second quarter 2025 investor presentation on August 6, 2025, which showcased accelerating revenue growth and expanding margins. The footwear company, whose brands include Merrell, Saucony, and Sweaty Betty, reported results that exceeded guidance across all key metrics.

Quarterly Performance Highlights

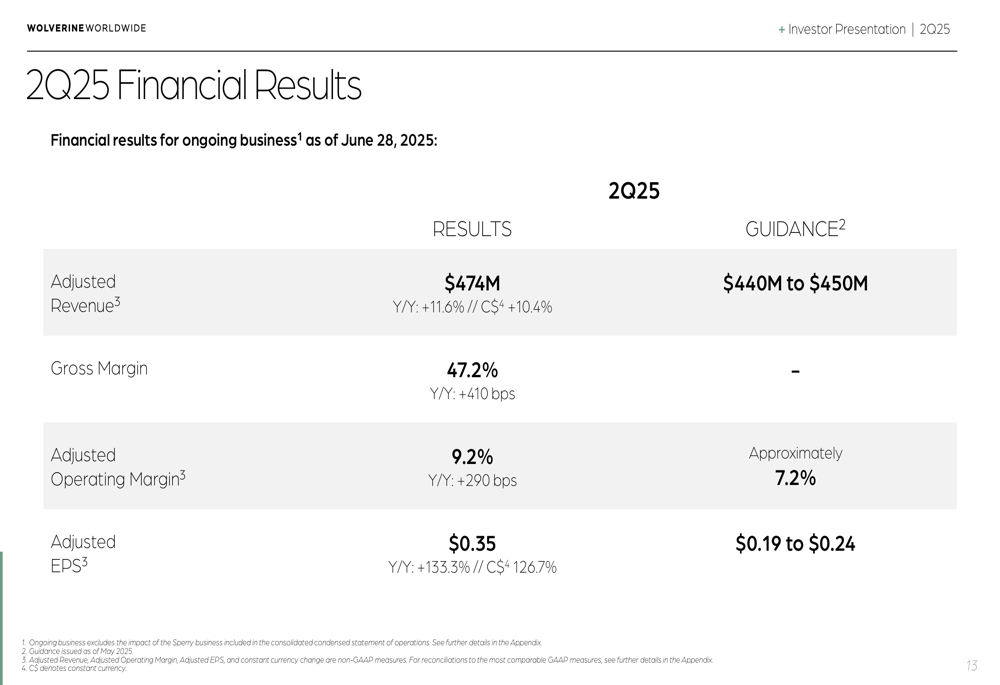

Wolverine reported second quarter adjusted revenue of $474 million, representing 11.6% year-over-year growth (10.4% in constant currency), significantly exceeding the company’s guidance range of $440-450 million. Adjusted earnings per share reached $0.35, a 133.3% increase from the prior year and well above the guided range of $0.19-$0.24.

Gross margin expanded 410 basis points year-over-year to 47.2%, while adjusted operating margin improved 290 basis points to 9.2%, surpassing guidance of approximately 7.2%. The company also reported inventory of $316 million and net debt of $568 million, representing a 15% reduction compared to the second quarter of 2024.

As shown in the following financial results summary:

Brand Performance Analysis

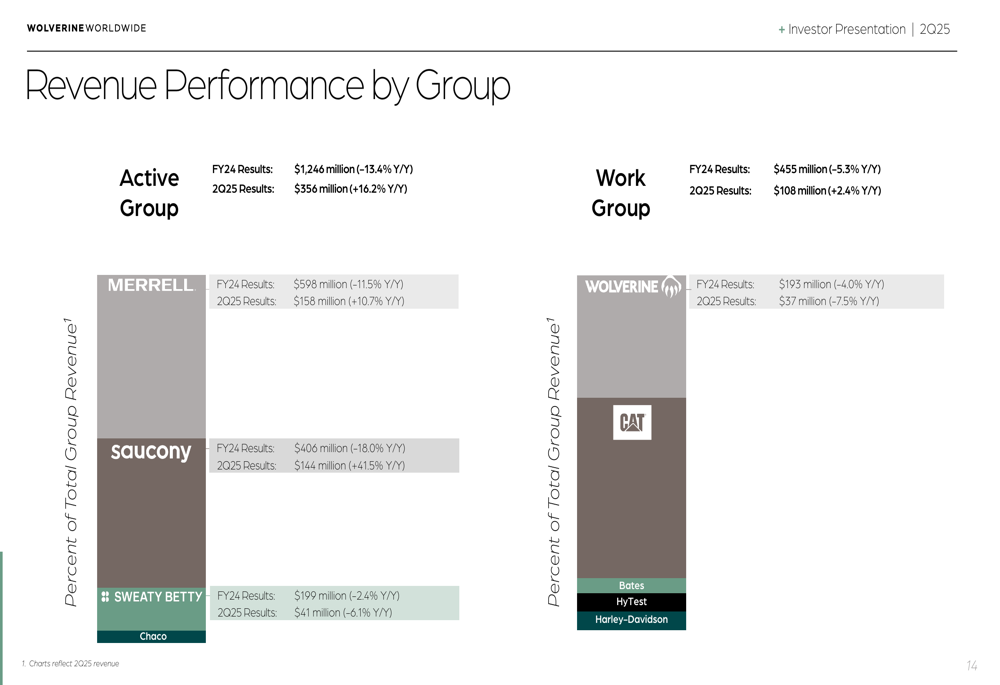

The company’s Active Group, which represents 71% of total revenue, drove much of the growth with a 16.2% year-over-year increase to $356 million in Q2. Saucony was the standout performer with 41.5% growth to $144 million, while Merrell grew 10.7% to $158 million. However, Sweaty Betty, the company’s premium women’s activewear brand, declined 6.1% to $41 million.

The Work Group, representing 26% of revenue, showed modest improvement with 2.4% growth to $108 million, though the flagship Wolverine brand within this group declined 7.5% to $37 million.

The following chart illustrates the revenue performance across brands:

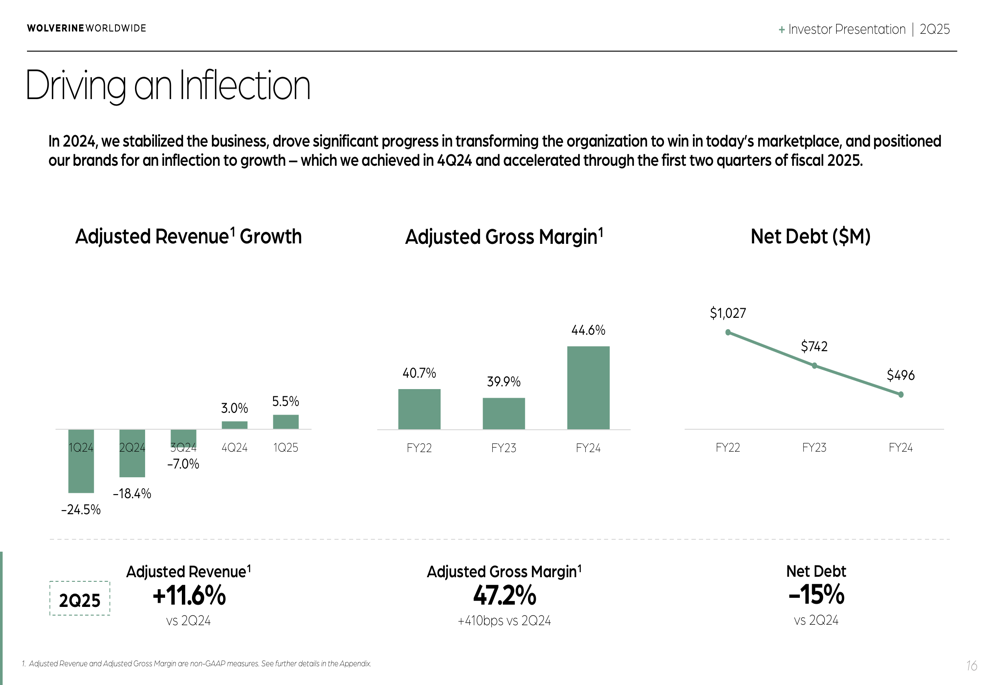

The presentation highlighted a clear inflection point in the company’s performance trajectory, with revenue growth steadily improving from -24.5% in Q1 2024 to +11.6% in Q2 2025. Similarly, adjusted gross margin has strengthened from 39.9% in FY23 to 47.2% in Q2 2025.

This positive momentum is visualized in the following chart:

Strategic Initiatives and Market Position

Wolverine Worldwide operates in attractive market segments with significant growth potential, including running footwear ($40B), athletic lifestyle footwear (+$150B), outdoor performance footwear ($20B), and women’s activewear ($80B). The company markets its brands in approximately 170 countries through a diverse distribution network that includes both wholesale (73%) and direct-to-consumer (27%) channels.

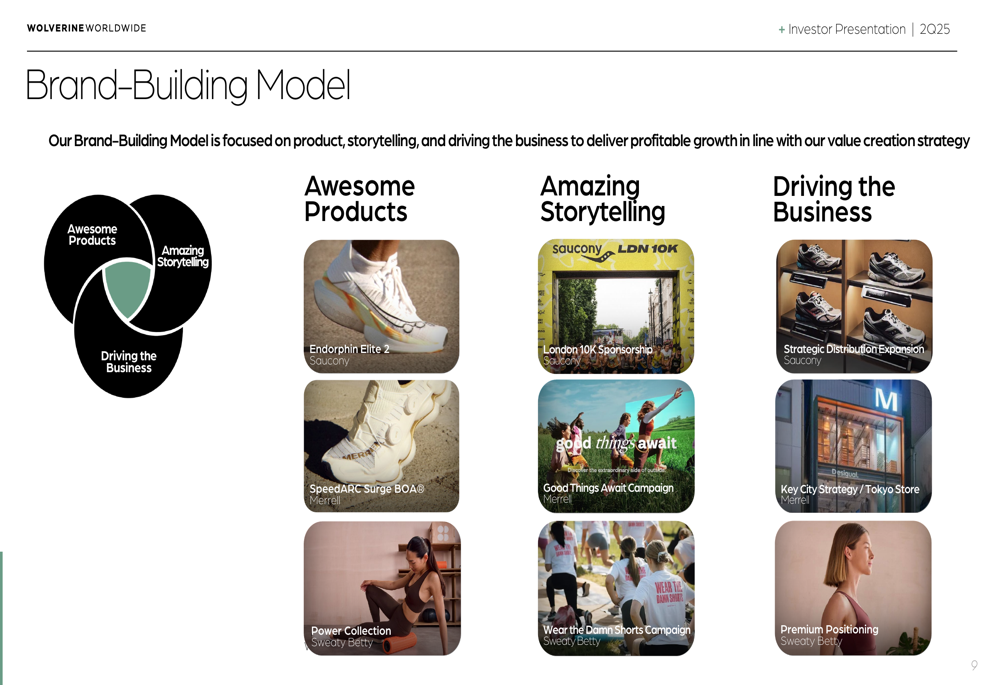

The company’s brand-building model focuses on three key pillars: product innovation, storytelling, and business development. Recent examples include the Endorphin Elite 2 running shoe, the London 10K sponsorship, and strategic distribution expansion.

As illustrated in this brand-building framework:

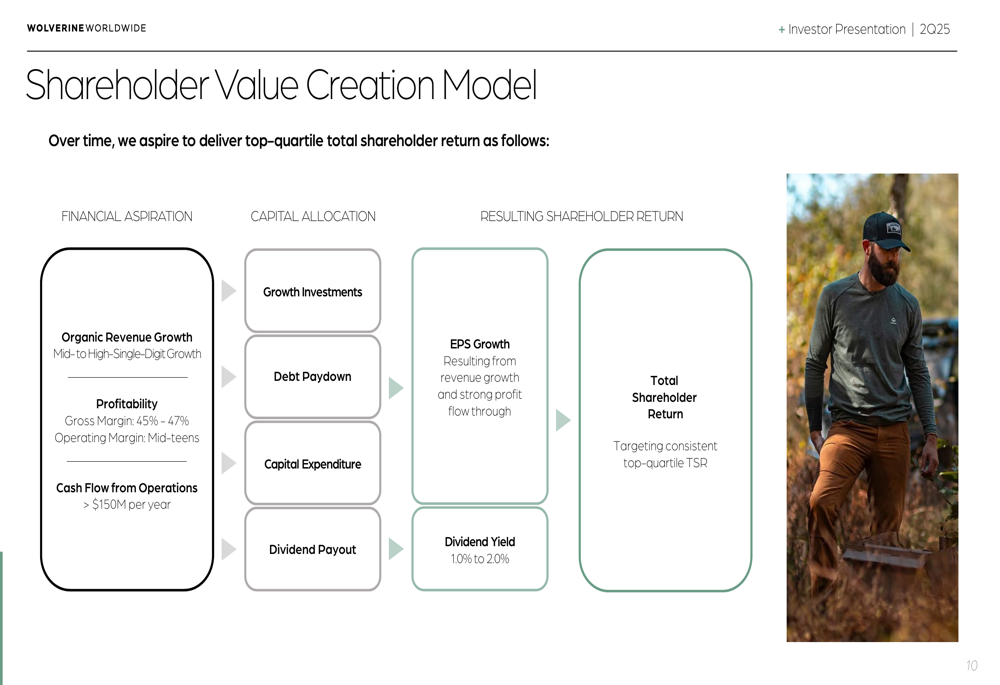

The company’s shareholder value creation model aims to deliver top-quartile total shareholder return through organic revenue growth, improved profitability, and strategic capital allocation:

Outlook and Tariff Challenges

For the third quarter of 2025, Wolverine provided guidance of $450-460 million in revenue (3.3% growth), approximately 47.0% gross margin (170 bps improvement), 8.3% adjusted operating margin (60 bps improvement), and adjusted EPS of $0.28-$0.32 (3.4% growth).

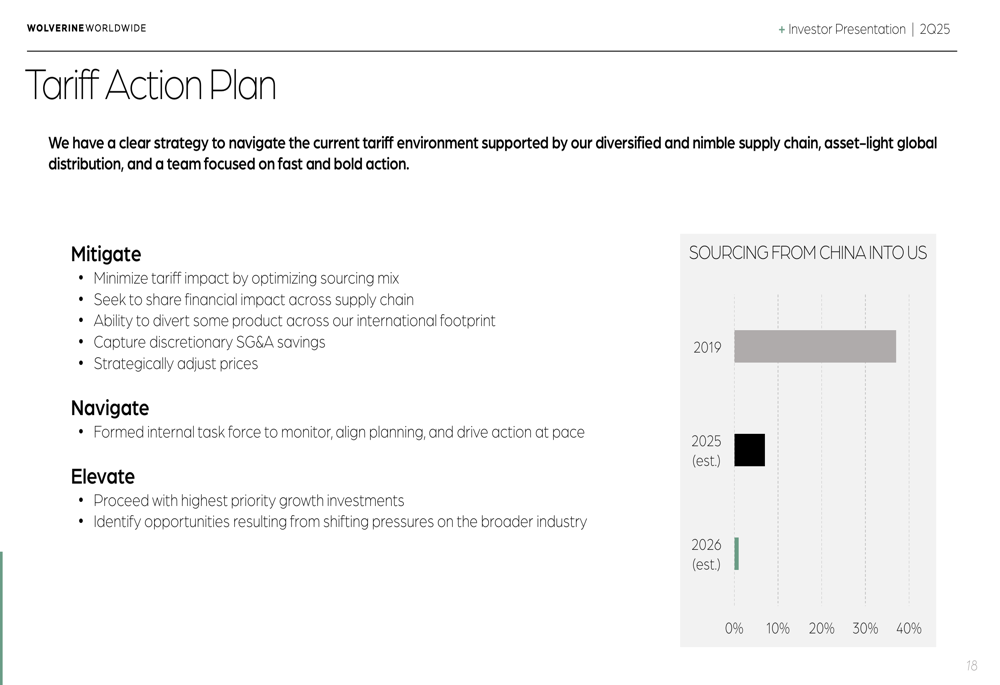

However, the company is navigating potential tariff challenges, having previously withdrawn its full-year 2025 guidance due to tariff uncertainties that could impact profits by $30 million, according to the Q1 earnings call. The Q2 presentation outlined a comprehensive tariff action plan based on the company’s diversified and nimble supply chain.

The plan includes mitigating actions (minimizing tariff impact, diverting product, capturing SG&A efficiencies, adjusting prices), navigating strategies (internal task force), and elevating initiatives (proceeding with high-priority investments, identifying opportunities). The company is also reducing its sourcing from China for U.S. imports.

As detailed in the tariff action plan:

Market Context

Wolverine’s strong Q2 performance builds on the momentum seen in Q1 2025, when the company reported EPS of $0.18 versus guidance of $0.11 and revenue of $412 million versus guidance of $395 million. The stock has been on an upward trajectory, gaining 12.55% in the week leading up to the Q2 presentation.

With the stock trading at $24.40 in premarket, Wolverine shares are approaching their 52-week high of $24.64, having recovered substantially from their 52-week low of $9.58. The company’s portfolio of global performance brands, improving financial metrics, and strategic initiatives appear to be resonating with investors despite ongoing tariff concerns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.