TSX runs higher on rate cut expectations

Wolverine Worldwide Inc (NYSE:WWW) delivered strong first-quarter 2025 results that significantly exceeded guidance, though the company has withdrawn its full-year outlook due to tariff concerns. The footwear and apparel manufacturer reported a 260% year-over-year increase in adjusted earnings per share, while revenue grew 5.5% compared to the same period last year.

Quarterly Performance Highlights

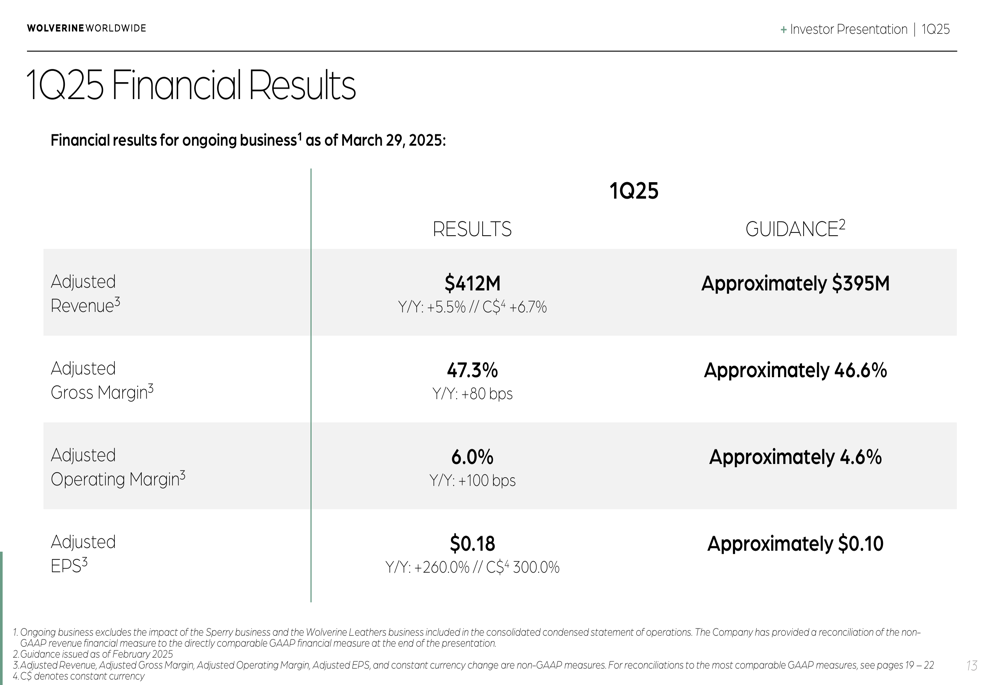

Wolverine Worldwide reported Q1 2025 adjusted revenue of $412 million, representing a 5.5% increase year-over-year (6.7% in constant currency), exceeding the company’s guidance of approximately $395 million. Adjusted earnings per share reached $0.18, up 260% from the prior year and substantially above the guided $0.10.

The company’s profitability metrics also showed improvement, with adjusted gross margin expanding 80 basis points to 47.3% and adjusted operating margin increasing 100 basis points to 6.0%.

As shown in the following financial results summary:

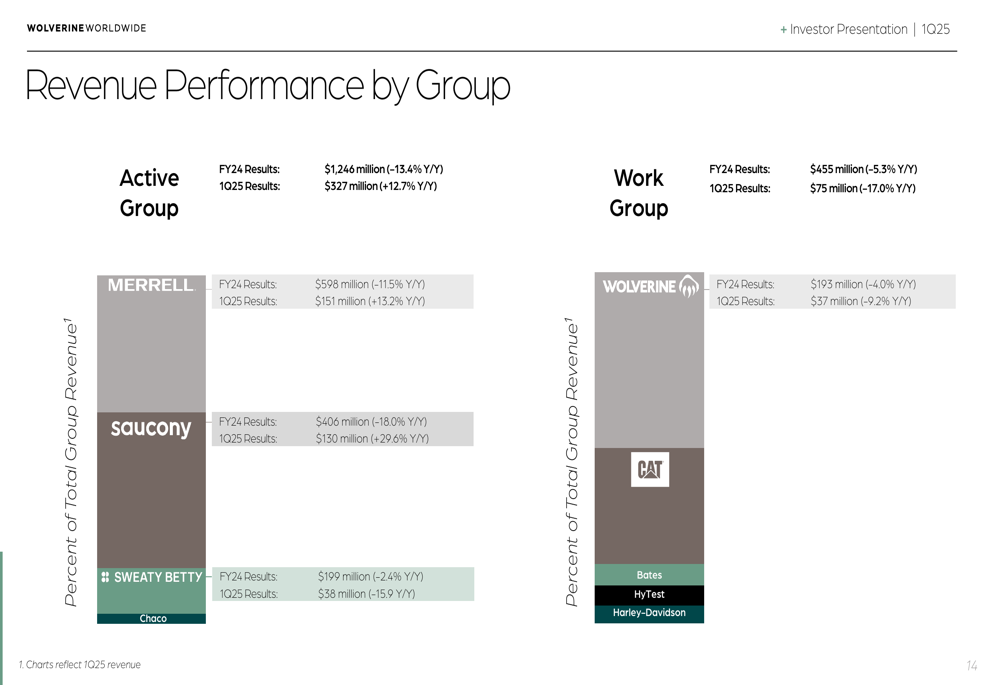

Performance varied significantly across the company’s brand portfolio. The Active Group, which includes Merrell, Saucony, and Sweaty Betty, delivered 12.7% revenue growth to $327 million. Within this segment, Saucony showed particularly strong momentum with 29.6% growth, while Merrell increased 13.2%. However, Sweaty Betty declined 15.9%.

In contrast, the Work Group struggled with a 17.0% revenue decline to $75 million, with the flagship Wolverine brand down 9.2%.

The following chart illustrates the revenue performance by brand group:

Strategic Initiatives

Wolverine Worldwide highlighted its three key strategic advantages: authentic, innovative brands; attractive markets; and an extensive global distribution network. The company’s brands maintain strong category positions, with Wolverine ranked #1 in work boots and Saucony leading in the low-profile running segment.

The company’s brand portfolio and market positioning are illustrated here:

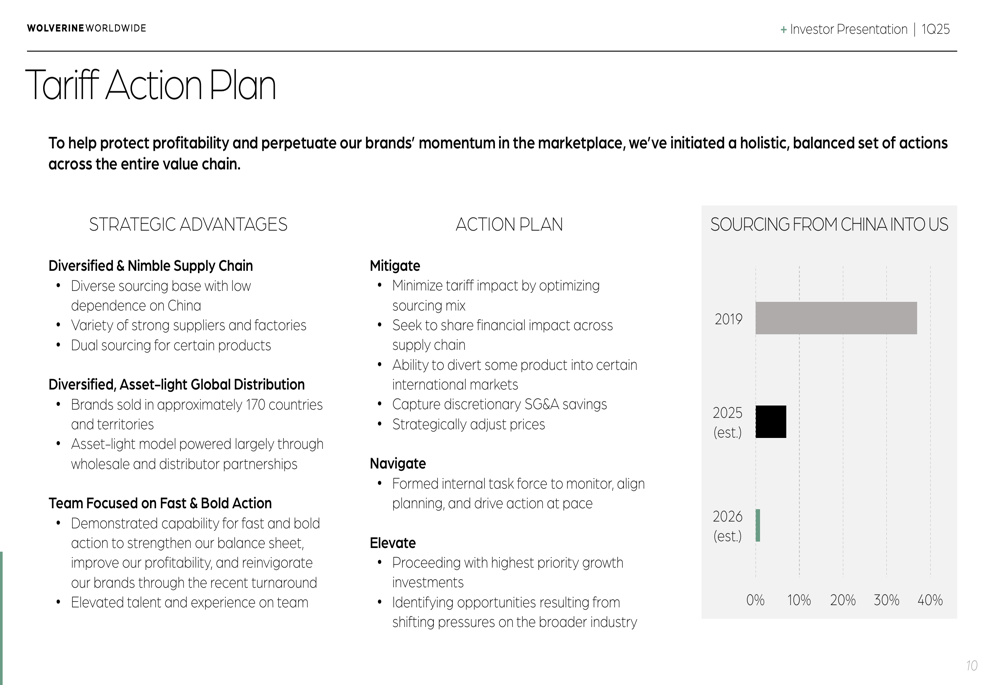

A significant focus of the presentation was Wolverine’s Tariff Action (WA:ACT) Plan, developed to address potential impacts from increased tariffs. The company is rapidly diversifying its supply chain away from China, planning to reduce China-sourced products for the U.S. market to less than 10% in 2025 and closer to zero by 2026.

The comprehensive tariff mitigation strategy includes:

"We’re taking fast and bold action to protect profitability through our diversified and nimble supply chain," the company stated in its presentation, outlining a three-pronged approach to mitigate, navigate, and elevate through the tariff challenges.

Forward-Looking Statements

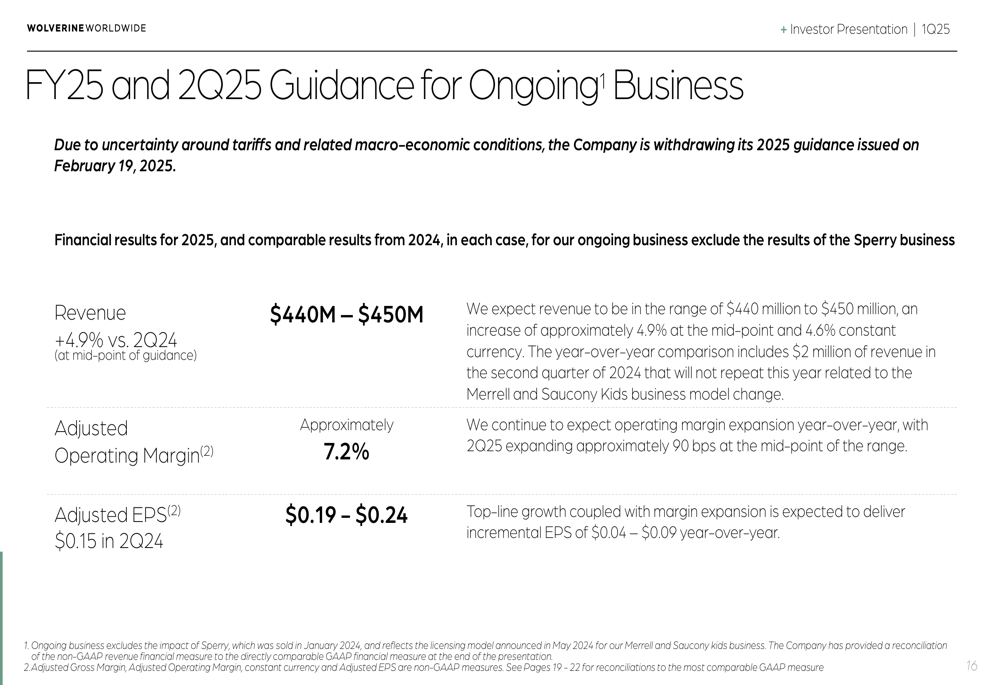

Despite strong Q1 performance, Wolverine Worldwide has withdrawn its full-year 2025 guidance, previously issued on February 19, citing "uncertainty around tariffs and related macro-economic conditions."

For the second quarter of 2025, the company provided the following outlook:

The Q2 guidance projects revenue of $440-450 million, representing approximately 4.9% growth at the midpoint compared to Q2 2024. Adjusted operating margin is expected to be around 7.2%, with earnings per share ranging from $0.19 to $0.24.

Competitive Industry Position

Wolverine Worldwide operates in several large and growing market segments, with significant opportunities for expansion. The company’s presentation highlighted the scale of these markets, including athletic lifestyle footwear (over $150 billion), women’s activewear ($80 billion), and outdoor performance footwear ($20 billion).

The following visualization shows the relative size of the markets where Wolverine competes:

The company’s global distribution network spans approximately 170 countries and territories, with a mix of direct-to-consumer channels, retail partnerships, and distributor relationships. North America remains the largest market, accounting for 51% of the company’s business, followed by EMEA at 33%.

The global distribution footprint is illustrated here:

Market Context

Despite the strong Q1 results, Wolverine’s stock has faced pressure in recent trading. According to the latest data, shares were down 2.57% in pre-market trading to $14.42. This follows a significant 18.63% drop after the company’s Q4 2024 earnings release, despite meeting EPS expectations at that time.

The stock is currently trading well below its 52-week high of $24.64, though above its 52-week low of $9.58. The recent performance suggests investors remain cautious about the company’s prospects amid tariff uncertainties, despite the operational improvements demonstrated in Q1.

Wolverine Worldwide continues to focus on strengthening its balance sheet, reducing net debt by 12% compared to Q1 2024. The company’s shareholder value creation model targets mid-to-high single-digit organic revenue growth, gross margins of 45-47%, and mid-teens operating margins over the long term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.