BofA update shows where active managers are putting money

Worldline SA (EPA:WLN) presented its H1 2025 financial results on July 30, revealing significant challenges alongside strategic transformation initiatives. The payment services provider reported a €4.1 billion goodwill impairment and declining revenues while announcing the divestment of its MeTS division and implementing cost-saving measures.

Executive Summary

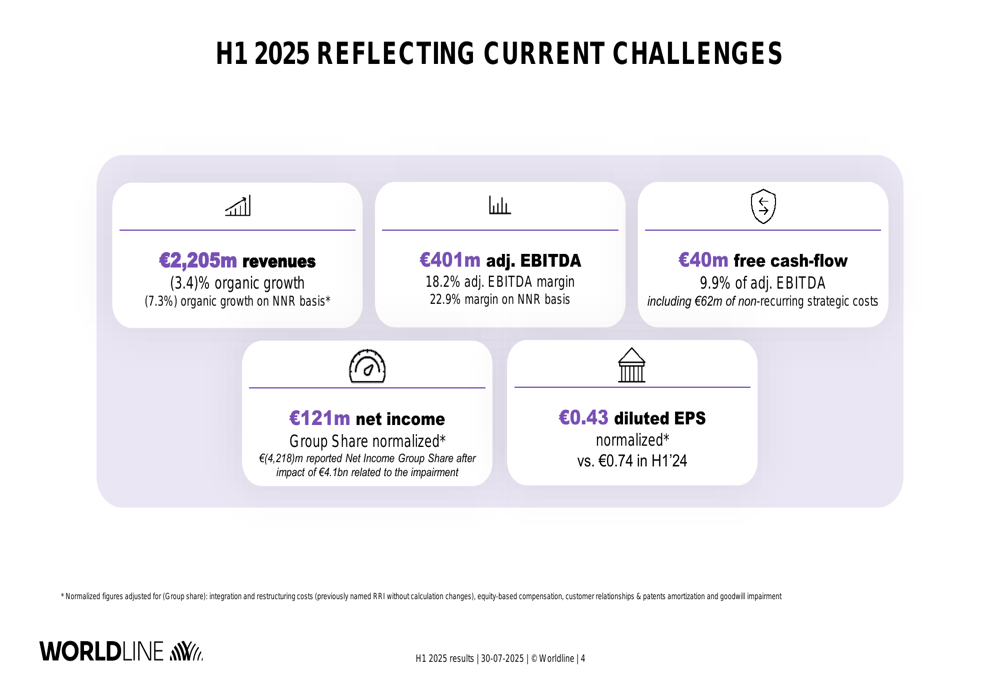

Worldline reported H1 2025 revenues of €2,205 million, representing a 3.4% organic decline compared to the same period last year. The company’s adjusted EBITDA fell to €401 million with an 18.2% margin, down from 22.5% in H1 2024. Most notably, the company recorded a massive €4.1 billion goodwill impairment, resulting in a reported net loss of €4,218 million, though normalized net income stood at €121 million.

As shown in the following key financial results summary:

The company’s performance deteriorated from Q1 to Q2, with the Q1 earnings report having shown only a 1% organic revenue decline. This trend is reflected in Worldline’s stock price, which has fallen from €5.63 after Q1 results to €3.57 currently, representing a 36.6% decline over the period.

Quarterly Performance Highlights

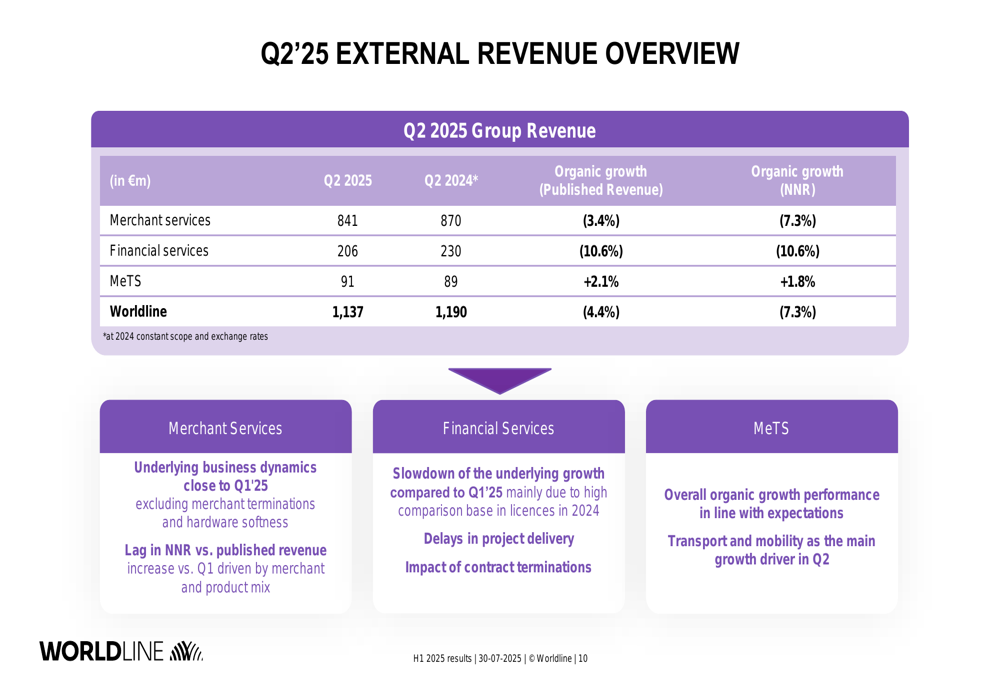

Worldline’s Q2 2025 revenue breakdown shows challenges across its major business segments. Merchant Services, the company’s largest division, saw a 3.4% organic revenue decline in Q2, while Financial Services experienced a more substantial 10.6% drop. Only the Mobility & E-Transactional Services (MeTS) division showed positive growth at 2.1%.

The detailed Q2 revenue breakdown by business line illustrates these trends:

In the Merchant Services segment, terminal sales remained weak, though the acquiring business has stabilized. The company’s acquiring MSV (Merchant Service Volume) reached approximately €145 billion in Q2’25, representing a modest 2.6% growth compared to Q2’24.

Financial Services performance was significantly impacted by contract re-insourcing effects and base effects from license deals signed in Q1’24. Excluding these factors, the organic decline would have been 4.1% instead of 10.6%.

Detailed Financial Analysis

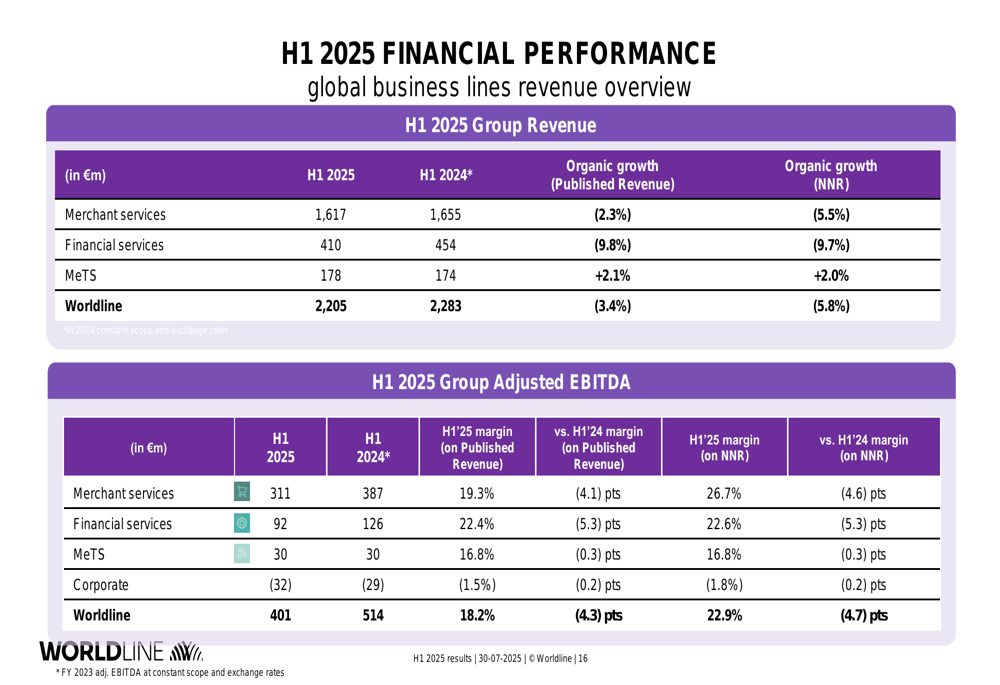

Worldline’s H1 2025 financial performance shows deterioration across most metrics compared to H1 2024. The adjusted EBITDA margin contracted by 4.3 percentage points to 18.2%, with declines observed across all business segments.

The comprehensive financial performance by business line reveals the extent of the challenges:

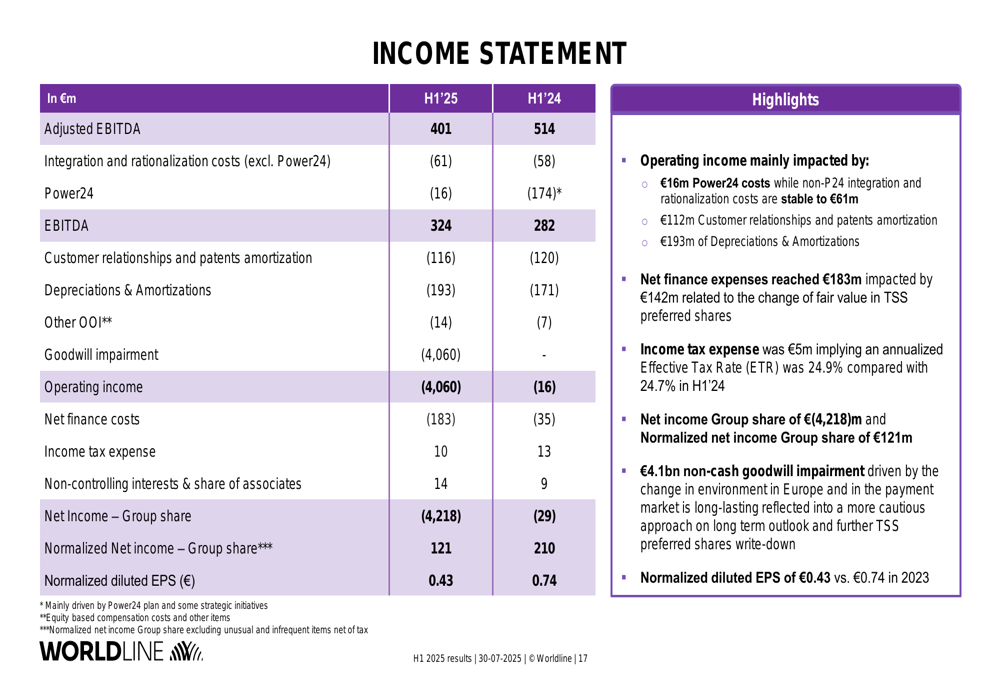

The company’s income statement highlights the significant impact of the €4.1 billion goodwill impairment, which transformed what would have been a modest normalized profit into a substantial reported loss:

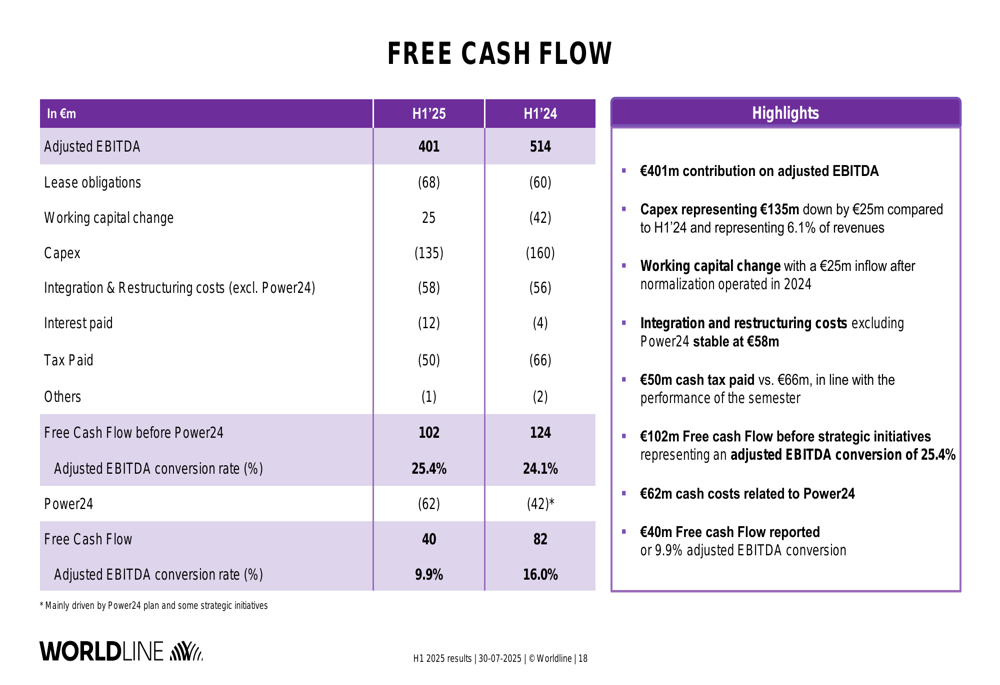

Despite these challenges, Worldline maintained positive free cash flow of €40 million in H1 2025, though this represents a decline from €82 million in H1 2024. The company has implemented cost containment measures, with €34 million in Power24 savings helping to offset cost inflation.

The free cash flow breakdown shows the impact of these measures:

Strategic Initiatives

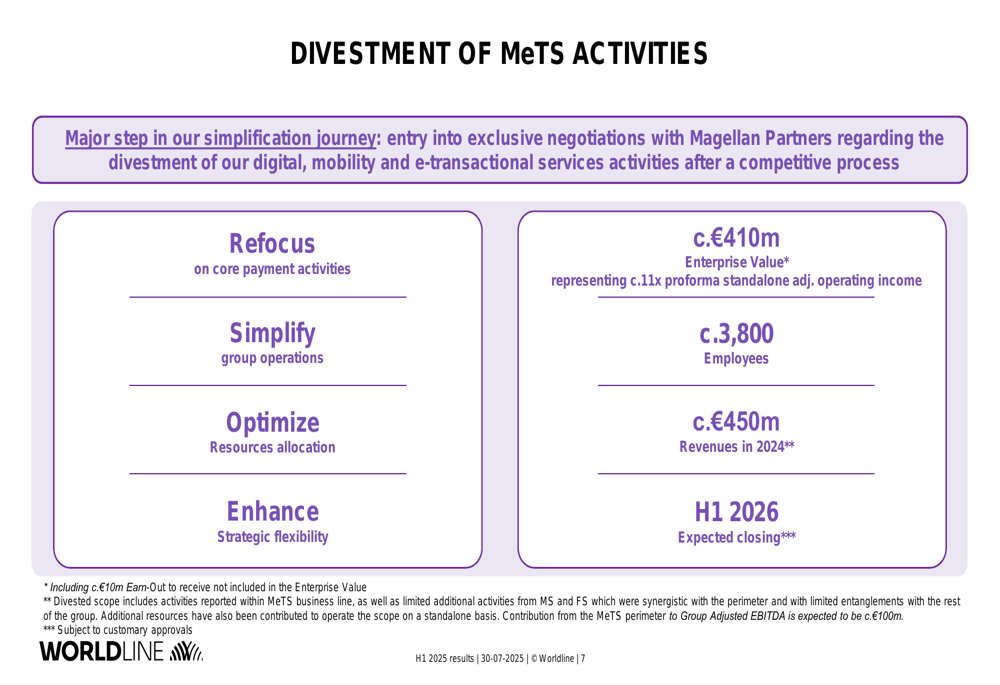

Worldline announced a major strategic move with the divestment of its Mobility & E-Transactional Services (MeTS) division to Magellan Partners. The transaction, valued at approximately €410 million (including a €10 million earn-out), represents a significant step in the company’s portfolio simplification strategy.

The details of this strategic divestment are outlined below:

The company is also addressing concerns around its High Brand Risk (HBR) portfolio, with two external firms engaged to assess the risk framework and audit the remaining portfolio. Interim conclusions show no need for material offboarding of merchants identified in the regulated entities of the Group so far.

Additionally, Worldline has strengthened its management team with several new appointments focused on transformation skills. The renewed leadership team, led by CEO Pierre-Antoine Vacheron, aims to drive the company’s turnaround efforts.

Forward-Looking Statements

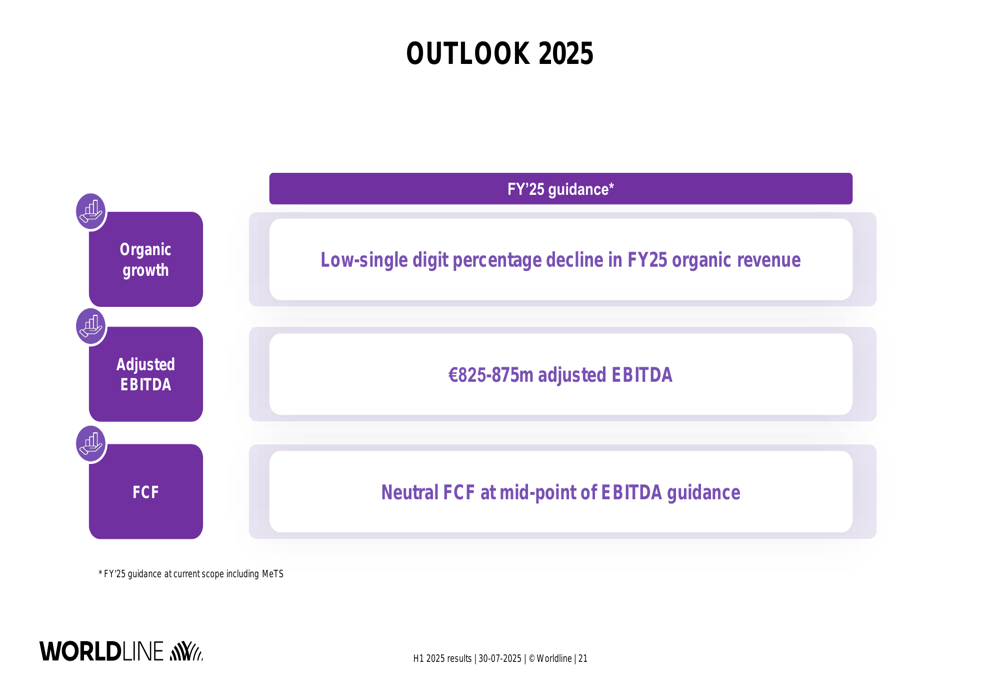

Worldline provided updated guidance for FY 2025, projecting a low-single digit percentage decline in organic revenue, adjusted EBITDA of €825-875 million, and neutral free cash flow at the mid-point of the EBITDA guidance range.

The company’s outlook for the remainder of 2025 is summarized below:

This guidance represents a reset of expectations compared to earlier in the year. During the Q1 2025 earnings call, the company had withdrawn its full-year guidance, indicating it would reassess its outlook at the H1 results announcement.

Management has outlined three key focus areas: fixing challenges impacting short-term performance, laying groundwork for future growth, and leveraging the renewed team to drive transformation. The company also announced a Capital Markets Day scheduled for November 6, 2025, where it will likely provide more details on its long-term strategic plan.

Worldline’s H1 2025 results reflect a company in transition, facing significant financial challenges while implementing strategic initiatives aimed at stabilizing performance and positioning for future growth. The substantial goodwill impairment signals a realistic reassessment of the company’s prospects, while the MeTS divestment and cost-saving measures demonstrate management’s commitment to portfolio optimization and operational efficiency.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.