Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Worldline SA (EPA:WLN) reported a 2.3% organic revenue decline in its Q1 2025 results presentation on April 23, as the European payment services provider faced challenges across its main business segments. The company’s shares closed at €5.63, up 1.42% on the day, but remain significantly below their 52-week high of €12.83.

The results come as newly appointed Group CEO Pierre-Antoine Vacheron begins implementing a strategic reset aimed at returning the company to "robust growth and free cash-flow generation." This follows a challenging period for Worldline, which had reported modest 0.5% organic growth in Q4 2024.

Quarterly Performance Highlights

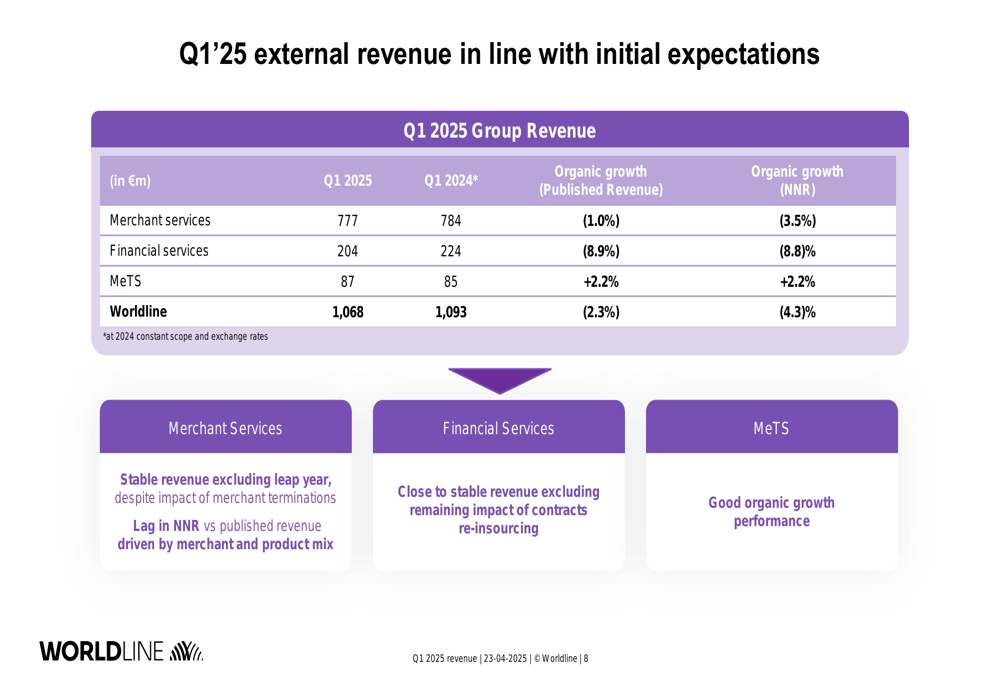

Worldline’s Q1 2025 revenue reached €1,068 million, down 2.3% organically compared to Q1 2024. On a normalized net revenue basis, which adjusts for scheme fees and partner commissions, the decline was more pronounced at 4.3%.

The company’s performance varied across its three business segments:

As shown in the following breakdown of quarterly revenue:

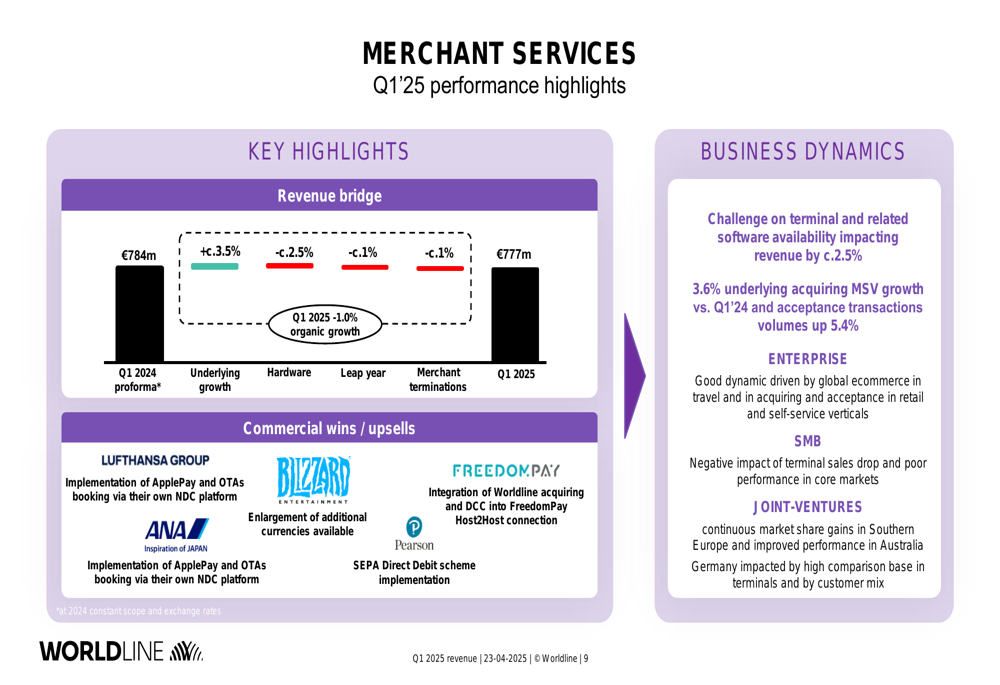

Merchant Services, Worldline’s largest segment, posted revenue of €777 million, representing a 1.0% organic decline. The segment faced multiple headwinds, including hardware availability issues and merchant terminations. Excluding the leap year effect, the company characterized the segment’s performance as "stable."

The segment’s detailed performance revealed mixed results across different verticals:

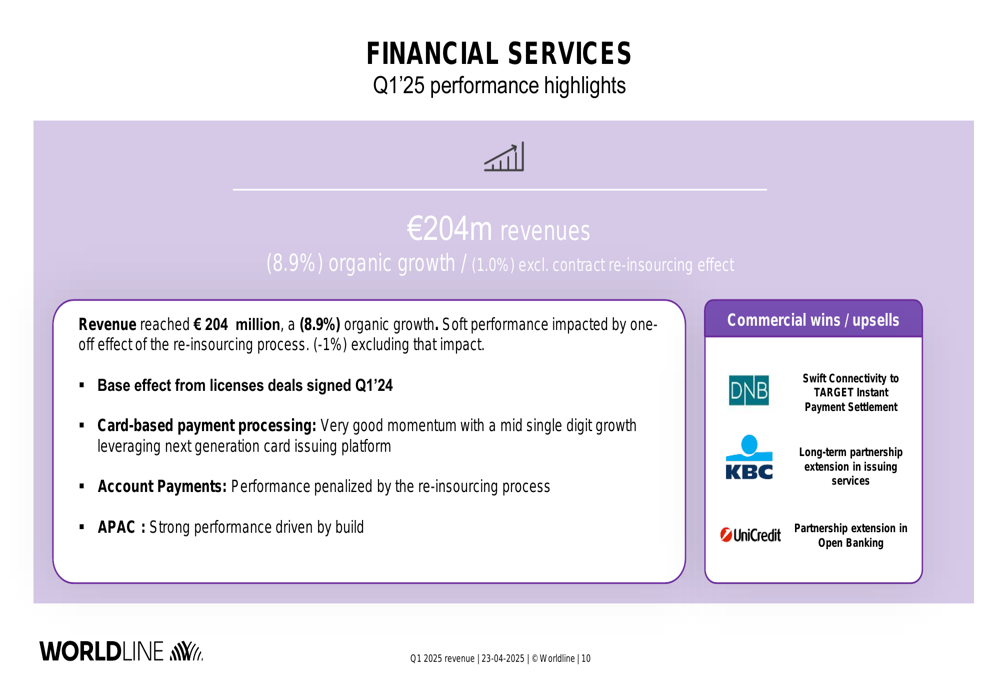

Financial Services experienced the steepest decline, with revenue falling 8.9% to €204 million. The company attributed this primarily to the ongoing impact of contract re-insourcing, noting that excluding this effect, the decline would have been approximately 1.0%.

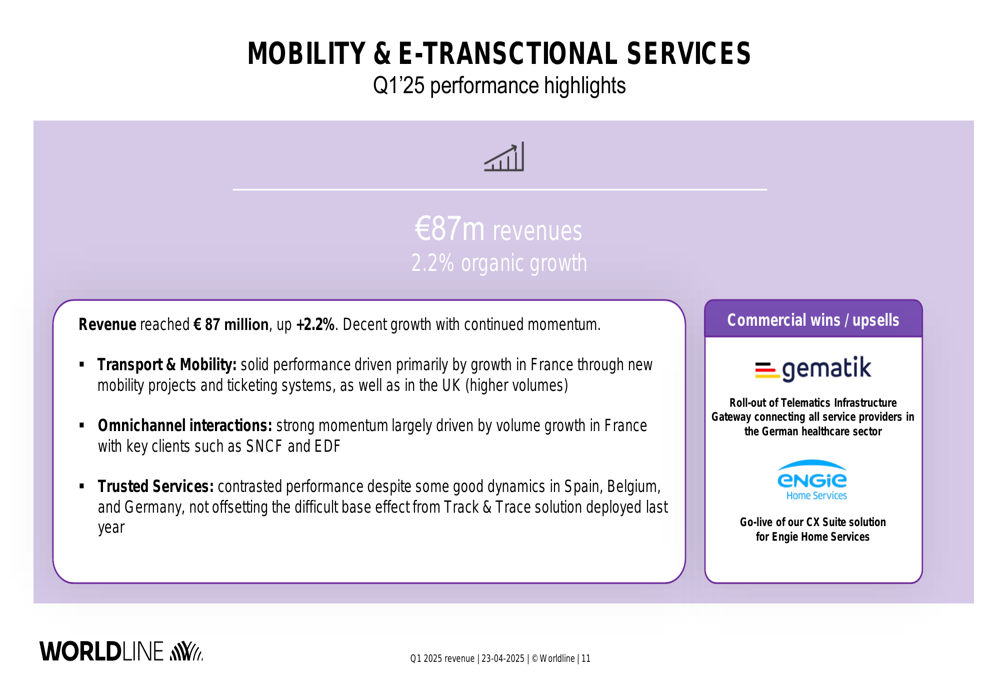

The only segment showing positive growth was Mobility & E-Transactional Services, which increased 2.2% to €87 million, driven by continued momentum across its service offerings.

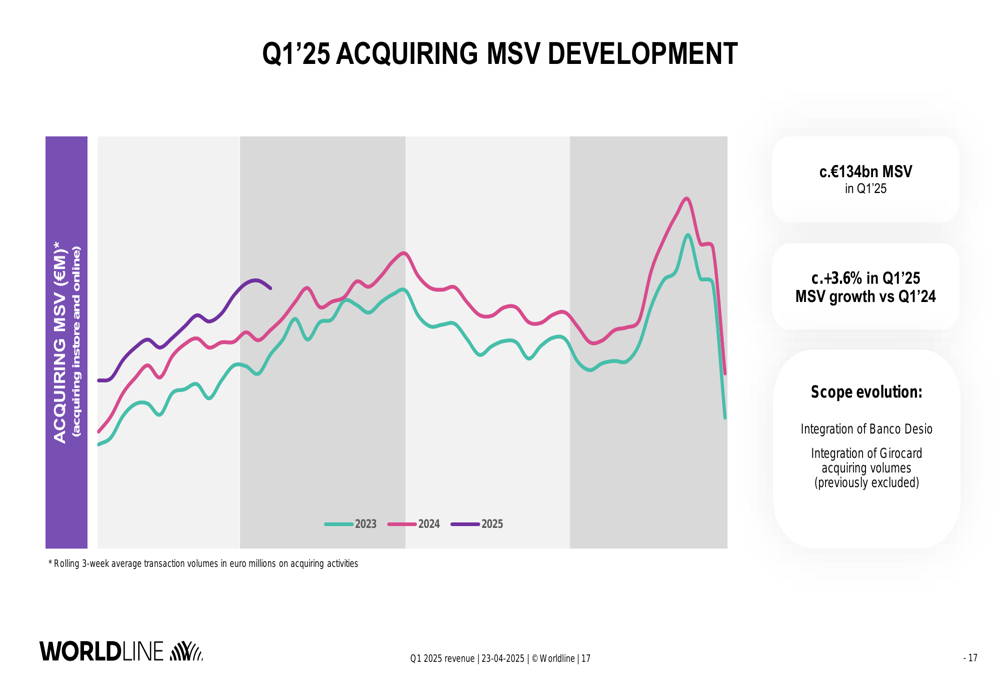

Despite the revenue decline, transaction volumes showed resilience. The company reported merchant acquiring sales volume of approximately €134 billion in Q1 2025, representing 3.6% growth compared to the same period last year. Acceptance transaction volumes increased by 5.4%.

The following chart illustrates the merchant sales volume development:

Strategic Initiatives

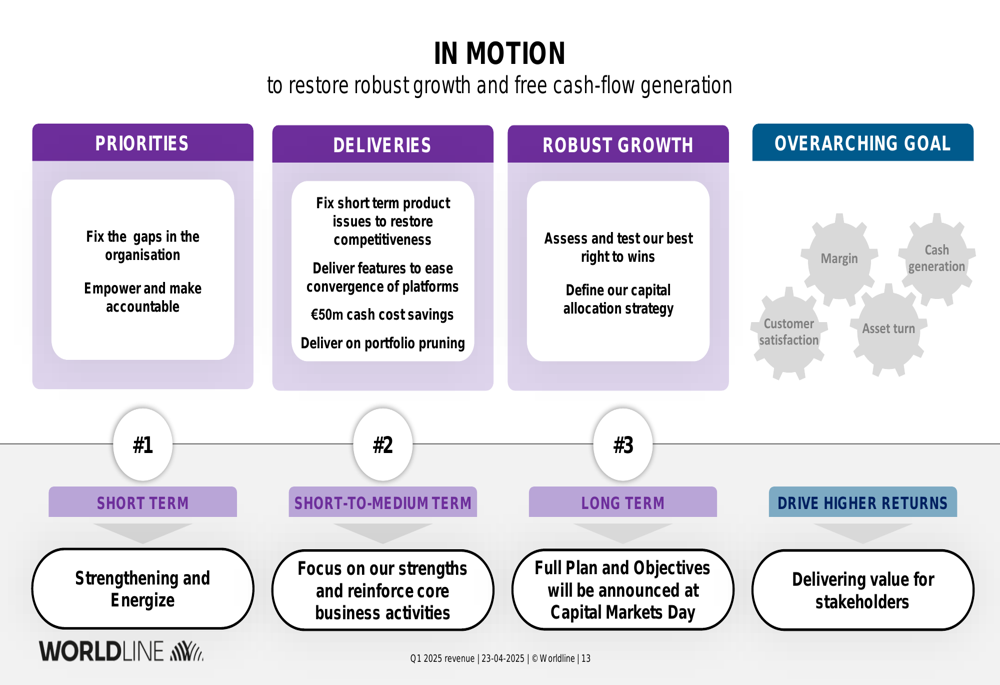

In his first quarterly presentation since taking the helm, CEO Pierre-Antoine Vacheron outlined a three-pronged approach to address the company’s challenges:

The strategy focuses on:

1. Priorities: Fixing organizational gaps and empowering accountable leadership

2. Deliveries: Addressing short-term product issues, platform convergence, achieving €50 million in cash cost savings, and portfolio pruning

3. Robust Growth: Assessing the company’s competitive advantages and defining capital allocation strategy

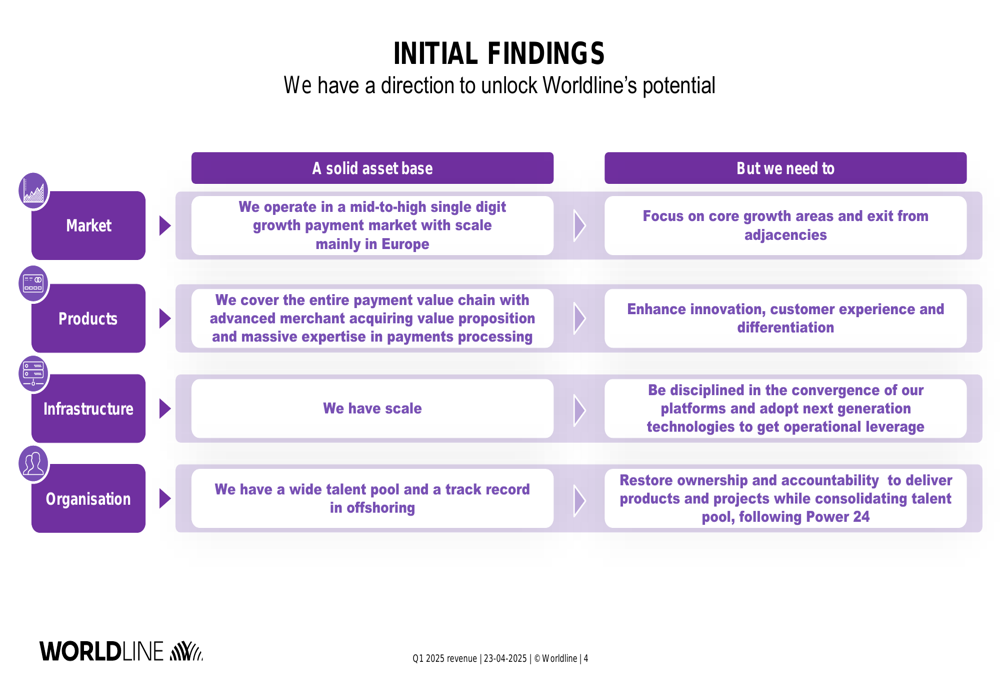

Vacheron acknowledged the company’s solid asset base but emphasized the need to "focus on core growth areas and exit from adjacencies" while enhancing "innovation, customer experience and differentiation."

Forward-Looking Statements

Worldline identified several factors affecting its 2025 outlook, including:

1. End of one-offs on top line: Merchant termination effects and contract insourcing are expected to impact H1 2025 but not H2 2025

2. POS terminals: Delays in shifting to next-generation terminals with late software delivery, with progressive improvement expected

3. Margin development: Unfavorable business mix in Q1 2025 with better dynamics in lower-margin verticals

The company plans to provide an updated FY 2025 outlook during its H1 2025 results publication on July 30, 2025.

Market Reaction & Analyst Perspectives

While Worldline’s stock rose slightly on the day of the presentation, it remains near its 52-week low of €4.77, reflecting ongoing investor concerns about the company’s growth trajectory. The stock has lost significant value since Q4 2024 results, when it traded at €7.42.

According to previous analyst assessments, the company appears undervalued based on fair value metrics, with an EV/EBITDA multiple of 5.77x. However, the continued revenue decline and delayed recovery timeline may test investor patience.

The presentation’s emphasis on "putting the company back on-track" signals management’s recognition of the challenges ahead while highlighting the "significant addressable market opportunity" that remains. With transaction volumes continuing to grow despite revenue headwinds, the company’s ability to execute its strategic reset will be crucial for regaining investor confidence in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.