Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

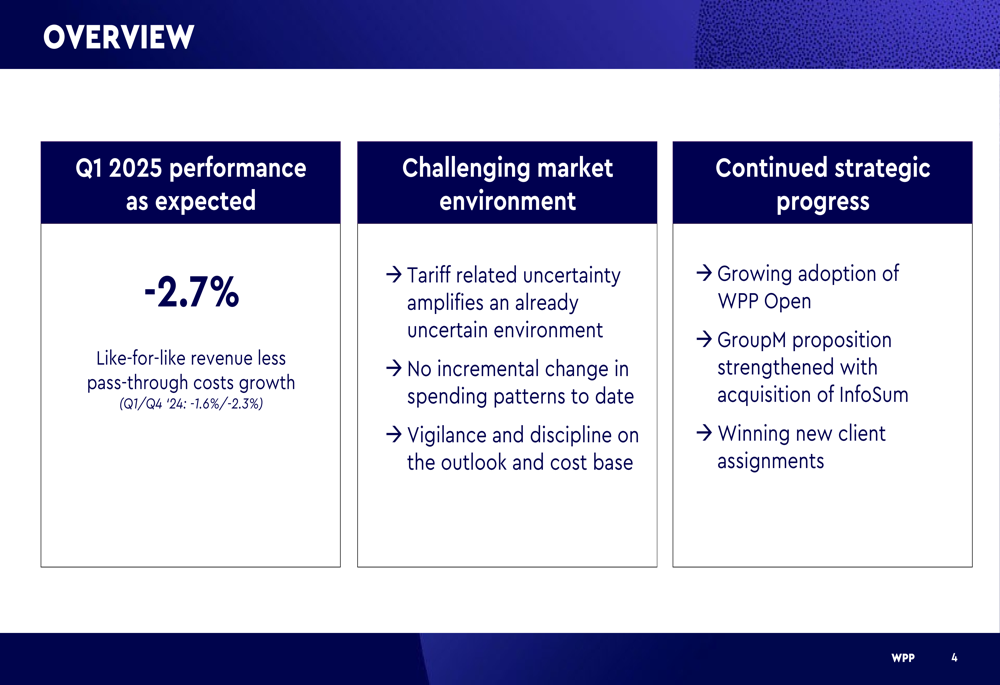

WPP PLC (NYSE:WPP) released its Q1 2025 trading update on April 25, 2025, reporting a 2.7% decline in like-for-like revenue less pass-through costs, in line with the company’s expectations but representing a deterioration from previous quarters. The global advertising giant continues to navigate a challenging market environment characterized by tariff-related uncertainty and cautious client spending patterns.

The results come as WPP’s stock has shown mixed performance, with shares trading at $37.51 at the previous close, down from the 52-week high of $57.37 but above the 52-week low of $31.52. In pre-market trading, WPP shares were down 1.36% to $37.00.

As shown in the following overview of Q1 2025 performance:

Quarterly Performance Highlights

WPP reported revenue less pass-through costs of £2,482 million in Q1 2025, representing a 7.6% decline on a reported basis. This figure was significantly impacted by a 3.7% reduction from M&A activity (primarily the disposal of FGS Global) and a 1.2% headwind from foreign exchange, largely due to Euro weakness.

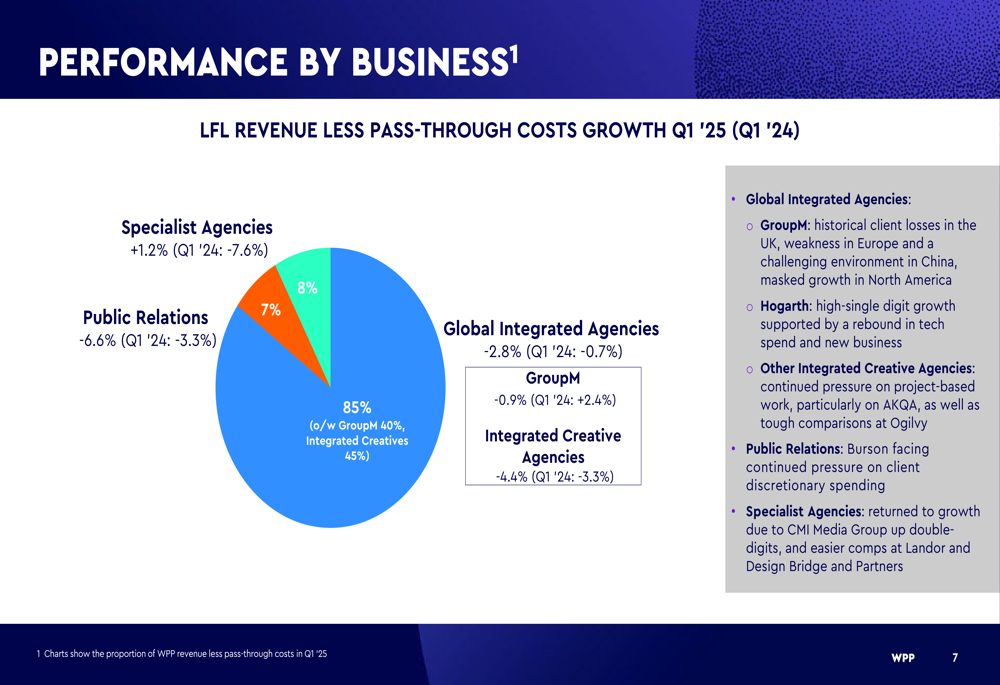

The company’s performance varied significantly across business segments. Specialist Agencies showed the strongest performance with 1.2% growth, a substantial improvement from the 7.6% decline in Q1 2024. However, Public Relations saw a 6.6% decline, while Global Integrated Agencies, which represent 85% of WPP’s business, declined by 2.8%.

The breakdown of performance by business segment reveals the varying fortunes across WPP’s portfolio:

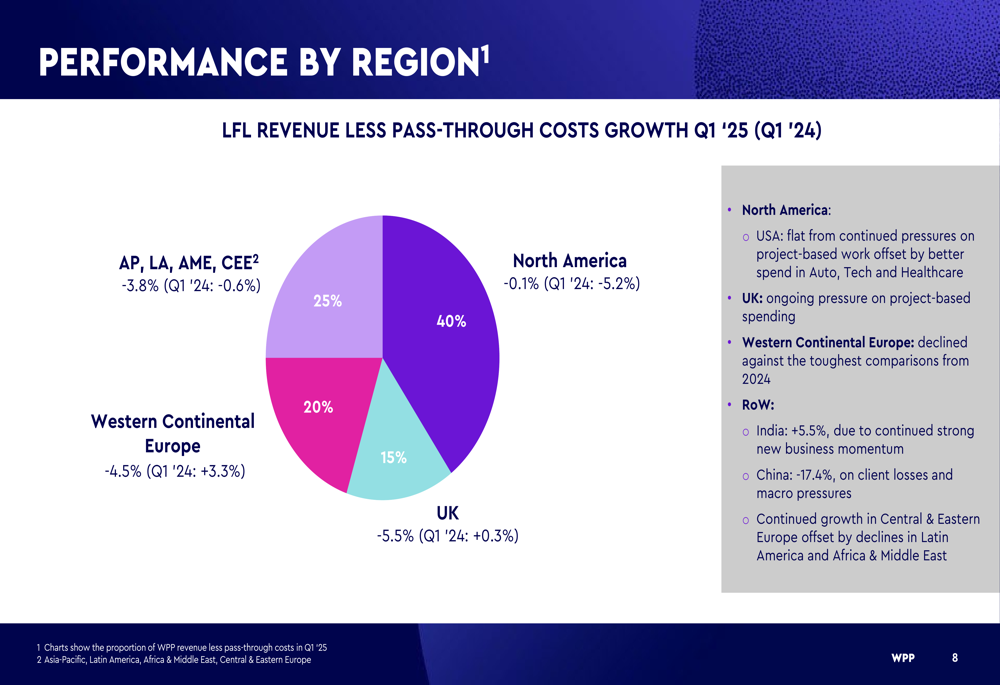

Regional performance also showed significant variation. North America nearly reached stability with a modest 0.1% decline, showing recovery from a 5.2% decline in the same period last year. However, the UK market was challenging with a 5.5% decline, reversing from 0.3% growth in Q1 2024. Western Continental Europe also struggled with a 4.5% decline after 3.3% growth in the prior year.

The following map illustrates the regional performance breakdown:

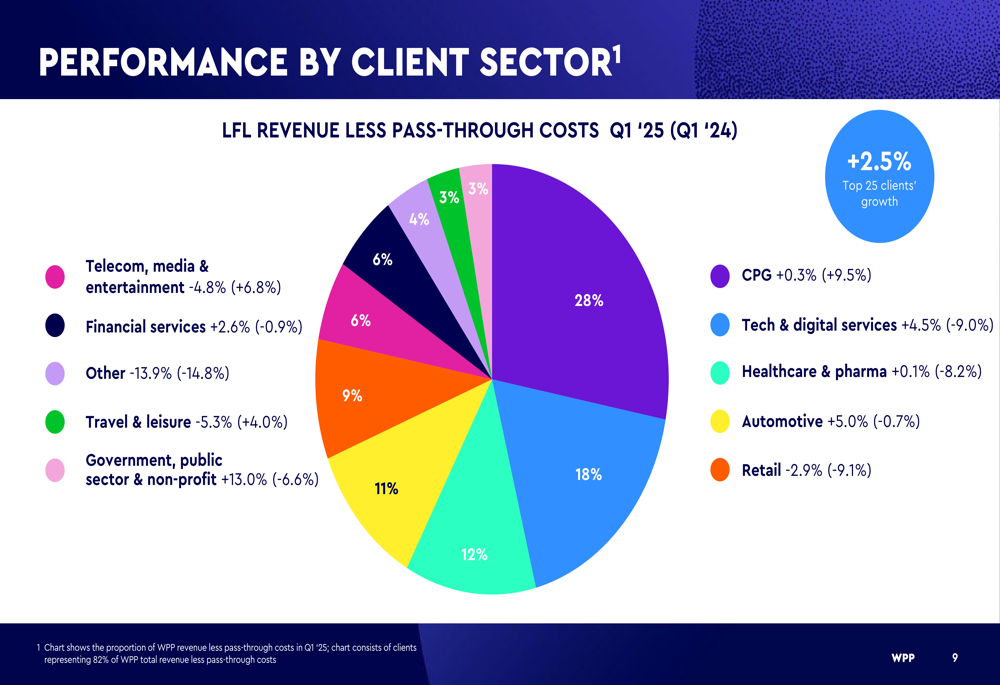

Client sector performance revealed interesting patterns, with Government, Public Sector & Non-profit showing the strongest growth at 13.0%, while Automotive (+5.0%) and Tech & Digital Services (+4.5%) also performed well. However, sectors like Telecom (BCBA:TECO2m), Media & Entertainment (-4.8%) and Travel & Leisure (-5.3%) faced significant headwinds.

The client sector breakdown provides insight into where WPP is finding growth opportunities:

Detailed Financial Analysis

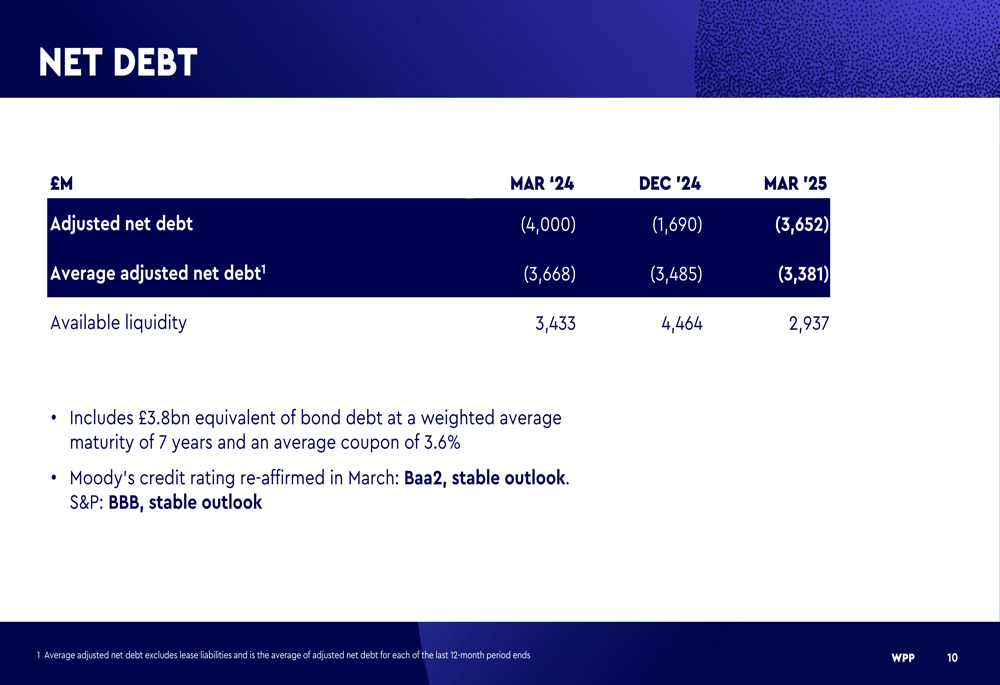

WPP’s net debt position has improved year-over-year, with adjusted net debt at £3,652 million as of March 2025, compared to £4,000 million in March 2024. The company maintains a solid liquidity position of £2,937 million, though this is down from £3,433 million a year earlier. Credit ratings remain stable, with Moody’s affirming a Baa2 rating and S&P maintaining a BBB rating, both with stable outlooks.

The following table details WPP’s debt position:

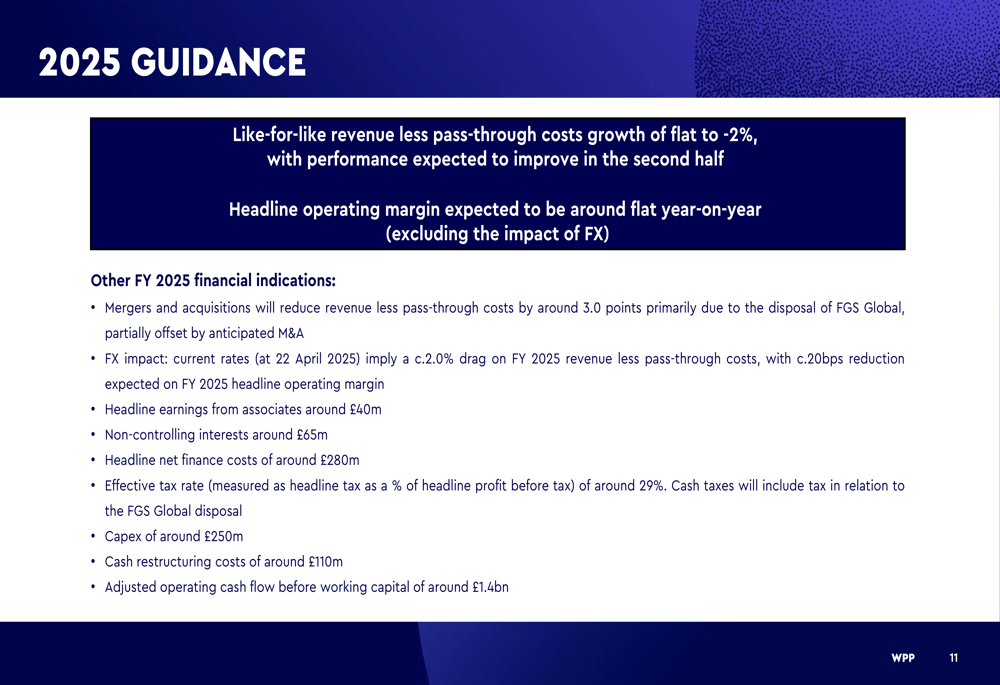

For the full year 2025, WPP is guiding for like-for-like revenue less pass-through costs growth of flat to -2%, with performance expected to improve in the second half of the year. Headline operating margin is projected to be around flat year-on-year, excluding the impact of foreign exchange.

The company’s 2025 guidance includes several key financial indicators:

Strategic Initiatives

Despite the challenging revenue environment, WPP continues to make progress on strategic initiatives. The company reported significant growth in adoption of WPP Open, its AI-powered platform, with user numbers increasing to 48,000 in Q1 2025 from 33,000 in December 2024. The platform is delivering tangible business benefits, with a reported 10%+ uplift on new business conversion rates.

The following slide illustrates WPP’s progress on its 2025 strategic priorities:

A key strategic development in Q1 was the acquisition of InfoSum, a data collaboration platform that strengthens GroupM’s capabilities. InfoSum’s technology enables clients to unlock the value of first-party data while maintaining privacy, which WPP positions as a strategic step forward for its AI-driven data offering.

The InfoSum acquisition details highlight its strategic importance to WPP’s future:

WPP also secured several new client assignments in Q1 2025, including EA Media (Global), Warner Bros. Discovery (NASDAQ:WBD) Media (Australia), Heineken (AS:HEIN) Commerce (Global), and IONNA Creative, demonstrating the company’s continued ability to win new business despite market headwinds.

Forward-Looking Statements

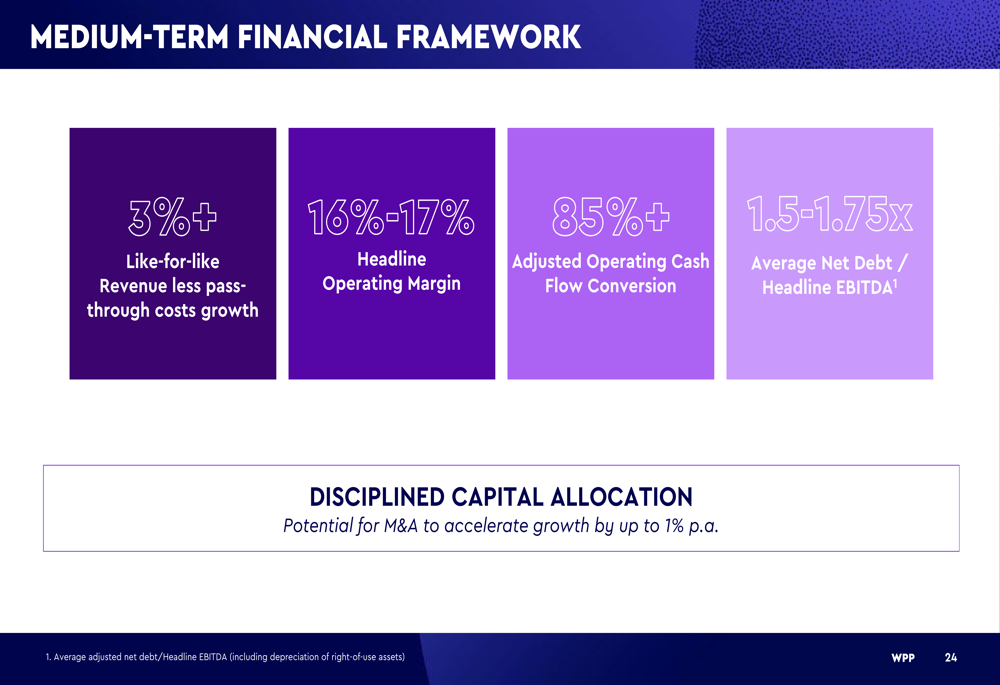

Looking beyond 2025, WPP maintains its medium-term financial framework targeting over 3% like-for-like revenue less pass-through costs growth, a headline operating margin of 16%-17%, and adjusted operating cash flow conversion of 85%+. The company aims to maintain average net debt to headline EBITDA ratio between 1.5-1.75x.

The medium-term financial framework provides insight into WPP’s longer-term ambitions:

Management expects performance to improve in the second half of 2025, though they acknowledge the continued challenging market environment. The company remains focused on executing its strategic priorities, with particular emphasis on scaling WPP Open and leveraging the InfoSum acquisition to enhance its data and AI capabilities.

WPP’s focus on AI adoption and strategic acquisitions suggests the company is positioning itself for future growth despite current headwinds. However, the decline in revenue across most regions and business segments indicates that the company continues to face significant challenges in the near term as it navigates an uncertain global economic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.