Adaptimmune stock plunges after announcing Nasdaq delisting plans

Introduction & Market Context

WSP Global Inc (TSE:WSP) presented its second quarter 2025 financial results on August 6, 2025, showcasing strong double-digit growth across key financial metrics despite facing headwinds in certain regions. The engineering and design services firm’s stock closed at $284.47, down slightly by 0.3% following the earnings release, but remains near its 52-week high of $289.94.

The results build upon the momentum established in Q1 2025, when the company reported robust performance that led to a 1.91% stock price increase. WSP continues to leverage its diversified business model across four core end-markets: Earth & Environment, Transport & Infrastructure, Property & Buildings, and Power & Energy.

Quarterly Performance Highlights

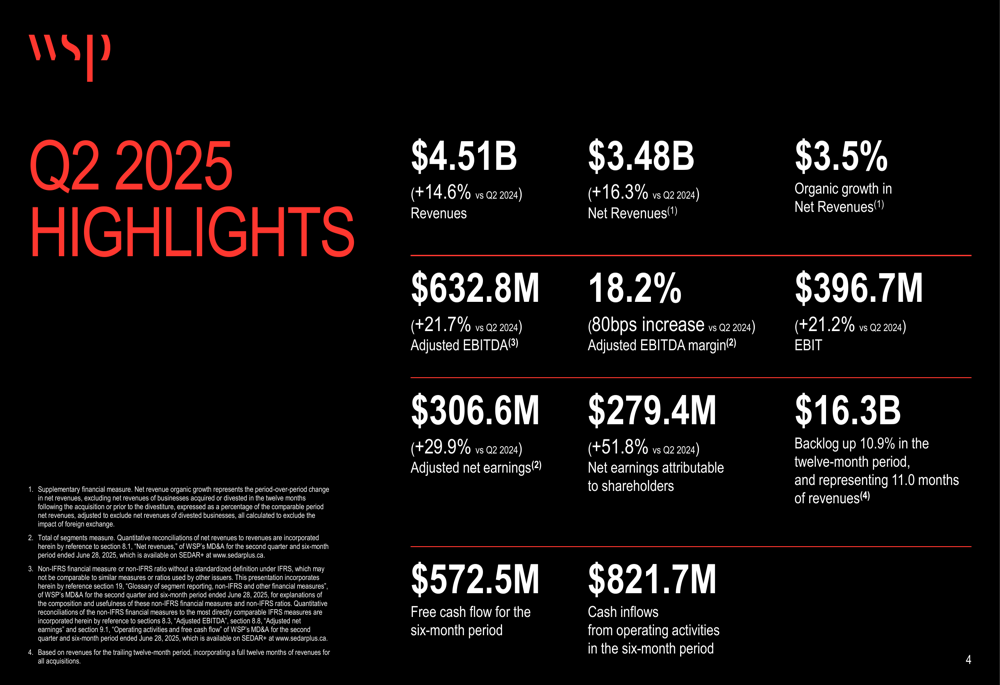

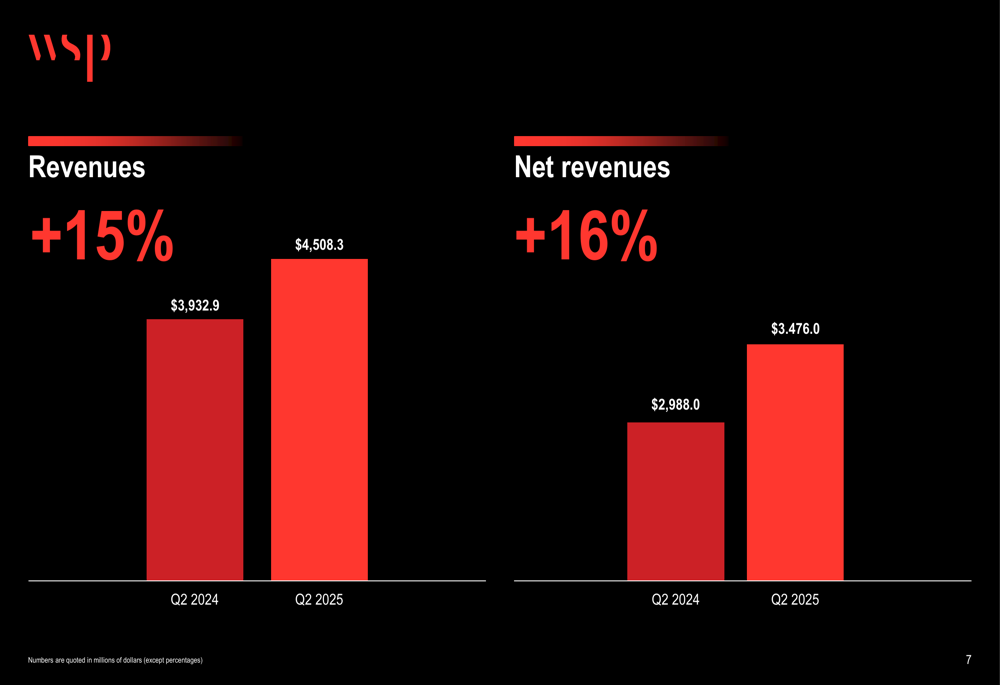

WSP delivered impressive financial results for Q2 2025, with substantial year-over-year improvements across all key metrics. Revenues reached $4.51 billion, representing a 14.6% increase compared to Q2 2024, while net revenues grew by 16.3% to $3.48 billion.

As shown in the following comprehensive overview of WSP’s financial performance:

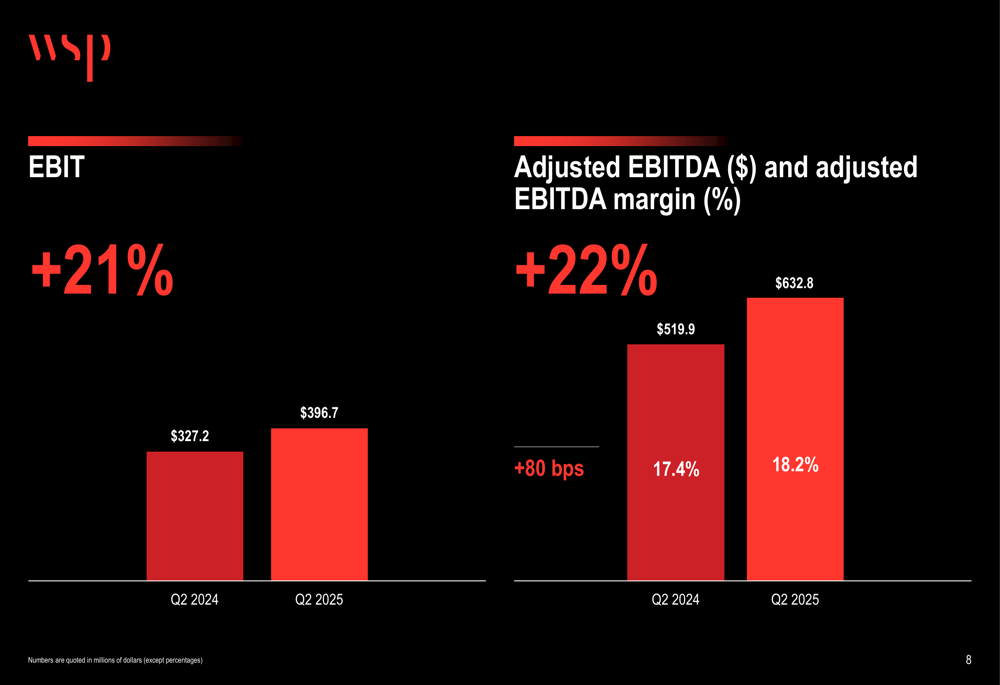

The company achieved organic growth in net revenues of 3.5%, slightly lower than the 3.7% reported in Q1 2025. Adjusted EBITDA rose by 21.7% year-over-year to $632.8 million, with the adjusted EBITDA margin expanding by 80 basis points to 18.2%. This margin improvement demonstrates WSP’s continued focus on operational efficiency and cost management.

Detailed Financial Analysis

The company’s revenue and net revenue growth trajectory remained strong in Q2 2025, as illustrated in the following chart:

WSP’s profitability metrics showed significant improvement, with EBIT increasing by 21.2% to $396.7 million compared to Q2 2024. Adjusted EBITDA growth outpaced revenue growth, indicating enhanced operational efficiency:

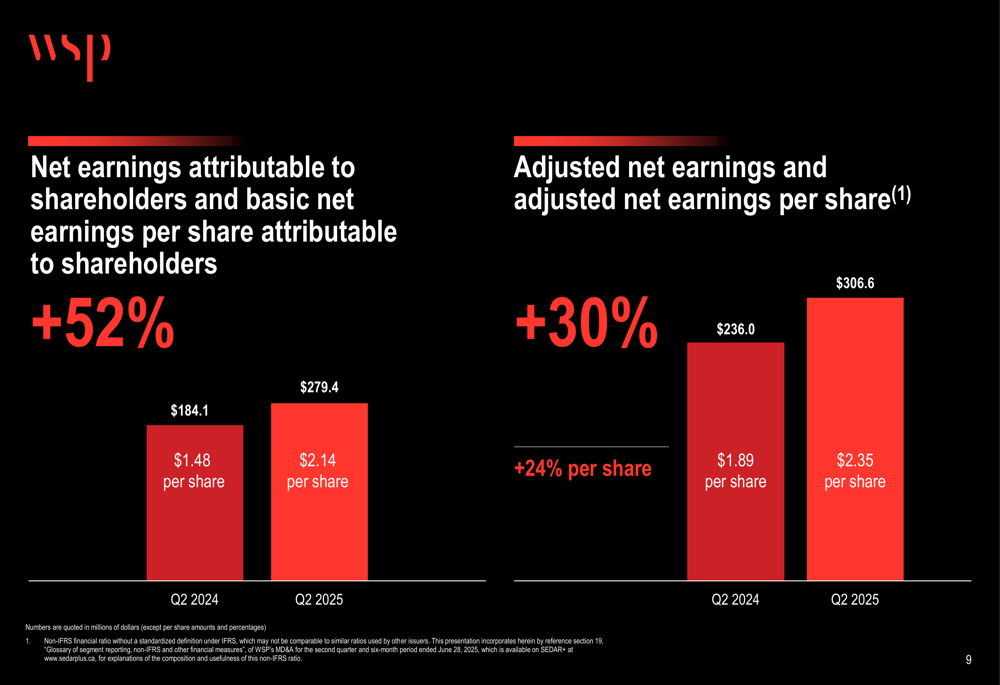

Net earnings attributable to shareholders surged by 51.8% to $279.4 million, while adjusted net earnings increased by 29.9% to $306.6 million. On a per-share basis, adjusted earnings reached $2.35, up from $1.89 in the same period last year:

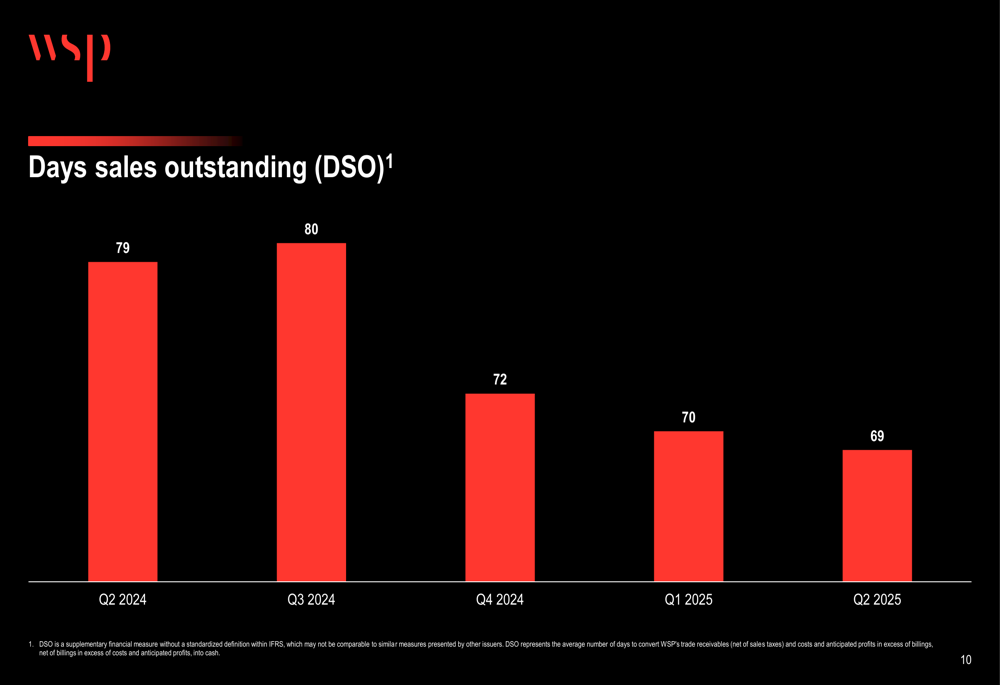

The company’s operational efficiency continued to improve, with Days Sales Outstanding (DSO) decreasing to 69 days in Q2 2025 from 79 days in Q2 2024. This 10-day improvement reflects enhanced cash collection processes and working capital management:

Regional Performance

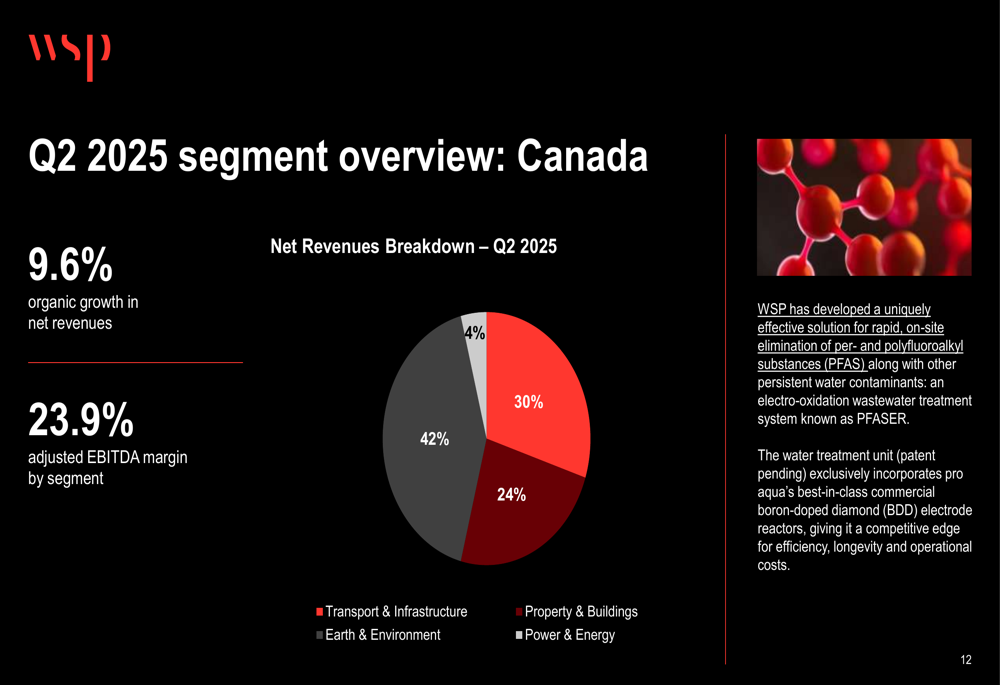

WSP’s performance varied significantly across its geographical segments. The Canadian operations delivered the strongest results with 9.6% organic growth in net revenues and a robust 23.9% adjusted EBITDA margin. The Transport & Infrastructure sector dominated the Canadian revenue mix at 42%:

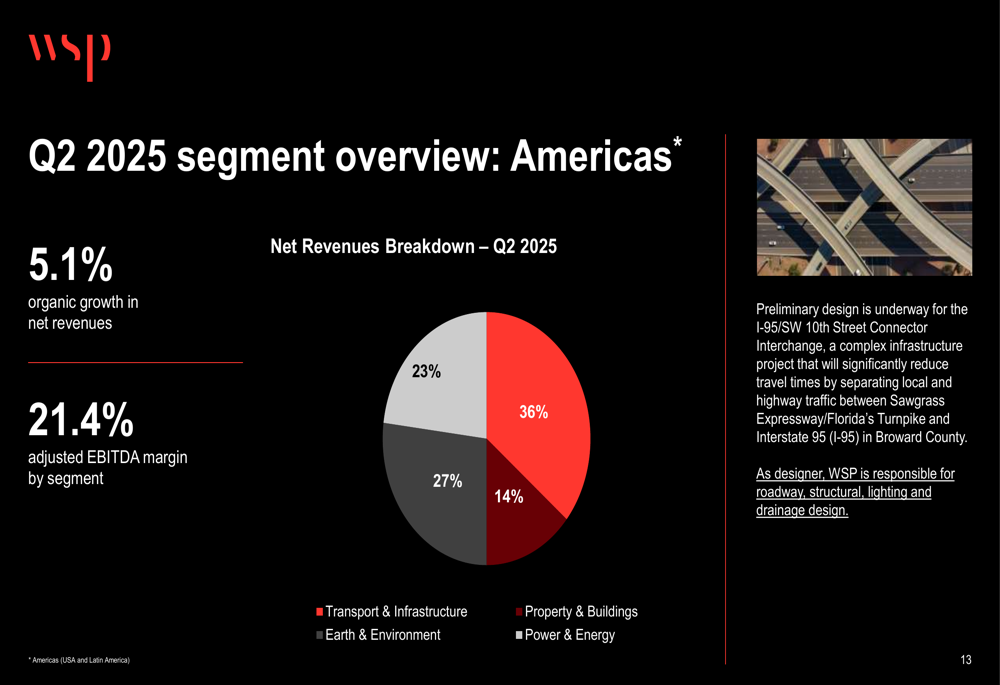

The Americas segment, comprising the USA and Latin America, posted solid 5.1% organic growth with a healthy 21.4% adjusted EBITDA margin. Property & Buildings represented the largest revenue contributor at 36%:

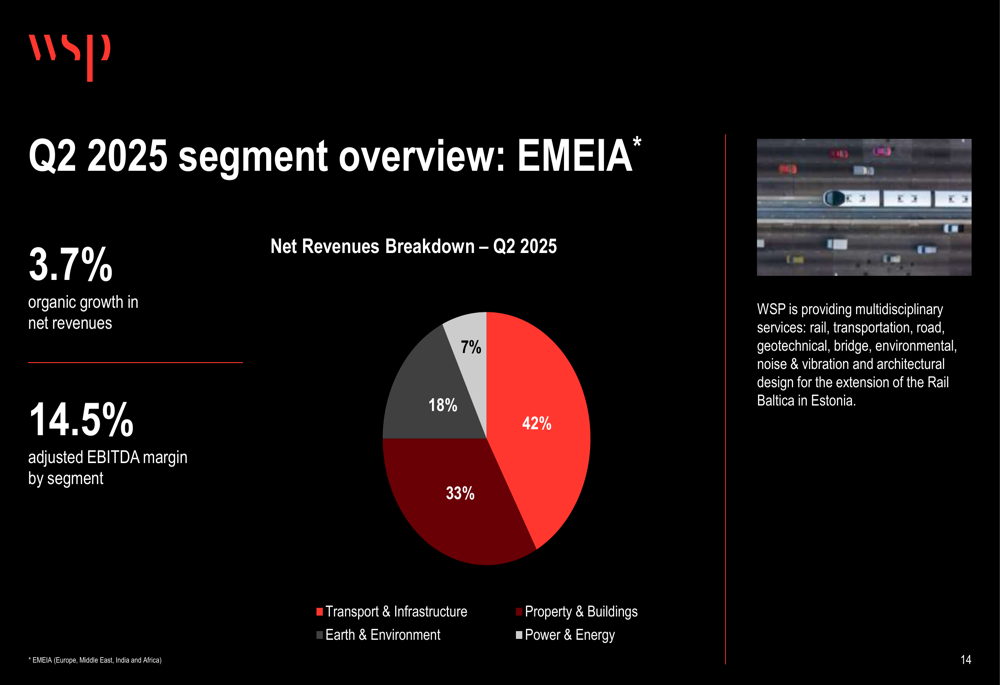

The EMEIA (Europe, Middle East, India, and Africa) region achieved 3.7% organic growth with a 14.5% adjusted EBITDA margin. Similar to the Americas, Property & Buildings was the dominant sector at 42% of net revenues:

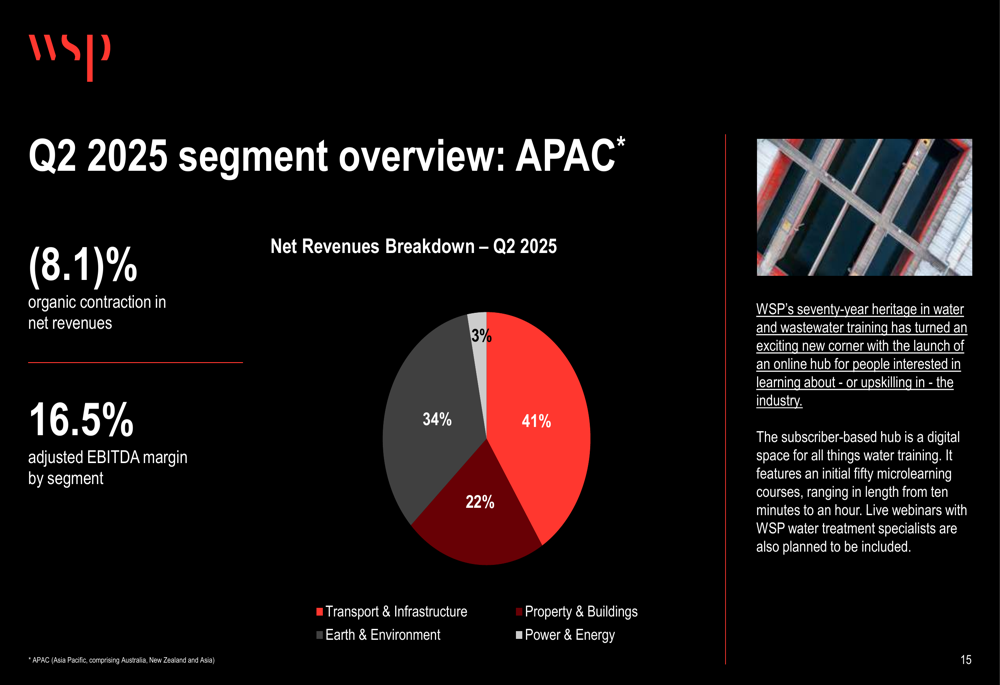

In contrast to other regions, the APAC (Asia Pacific) segment experienced an 8.1% organic contraction, though it maintained a respectable 16.5% adjusted EBITDA margin. This aligns with the cautious outlook for the APAC region mentioned in the Q1 2025 earnings call:

Strategic Initiatives

WSP continues to strengthen its position across its four core end-markets, each supported by secular trends. The company highlighted several significant projects during the presentation, including the Pohénégamook-Picard-Saint-Antonin-Wolastokuk 1 Wind Energy Centre in the Earth & Environment sector, and a memorandum of understanding related to 765 kV technology in the Power & Energy sector.

In the Transport & Infrastructure segment, WSP is working on modernizing the M1 and M2 metro lines in Copenhagen, while in Property & Buildings, the company celebrated the completion of a new hospital in Anacostia.

The company’s backlog remains strong at $16.3 billion, up 10.9% over the twelve-month period, representing approximately 11 months of revenues. This robust backlog provides good visibility for future revenue streams.

Forward-Looking Statements

While WSP did not provide specific updated guidance in the presentation, the strong Q2 2025 results suggest the company is on track to meet or exceed its full-year targets. The continued challenges in the APAC region will require management attention, but the strong performance in North America and steady growth in EMEIA should help offset these headwinds.

The company’s improving operational metrics, particularly the reduction in DSO and expansion of EBITDA margins, indicate that WSP’s focus on efficiency is yielding positive results. However, investors should monitor the organic growth rate, which has slightly decelerated from Q1 2025.

As WSP moves into the second half of 2025, its diversified business model across different geographical regions and market sectors positions it well to navigate varying market conditions while continuing to deliver shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.