Palantir shares slip by 7% despite posting record revenue in third quarter

Introduction & Market Context

Xerox Holdings Corporation (NYSE:XRX) presented its Q3 2025 earnings results on October 30, revealing mixed performance with significant revenue growth but disappointing earnings per share. The company’s shares tumbled 9.18% to $3.11 during regular trading hours, following a 5.25% decline in premarket trading, as investors reacted to the earnings miss and downward revision of full-year guidance.

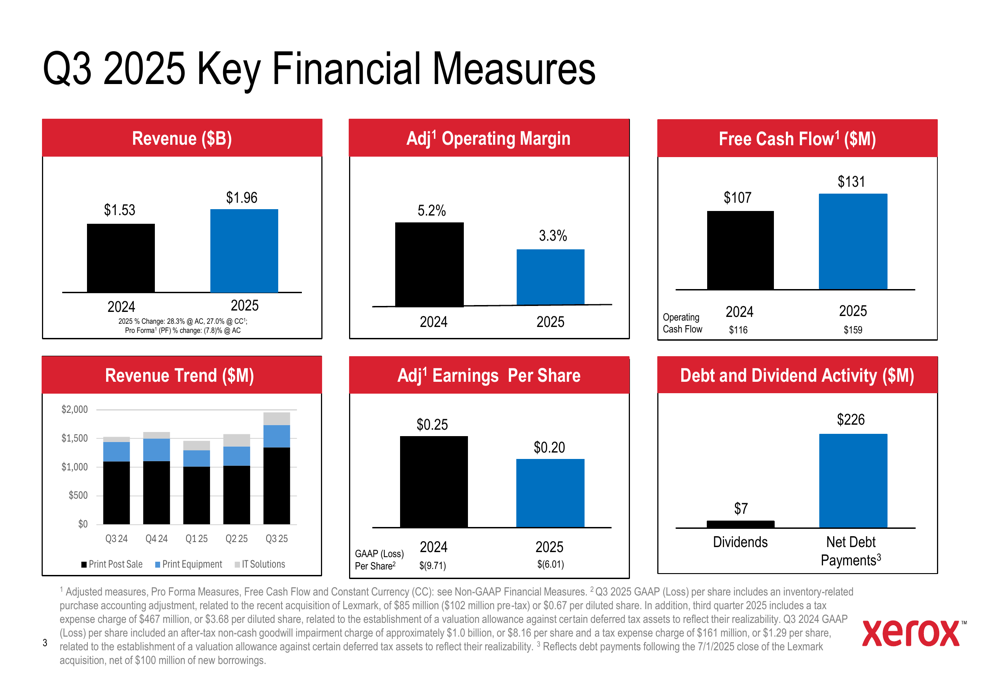

While Xerox reported revenue of $1.96 billion, representing a 28.3% year-over-year increase at actual currency rates, the company missed analyst expectations of $2.04 billion. More concerning to investors was the adjusted earnings per share of $0.20, which fell significantly short of forecasts and declined from $0.25 in the same period last year.

Quarterly Performance Highlights

Xerox’s Q3 2025 results showed strong topline growth but deteriorating profitability metrics. The company reported a 28.3% revenue increase at actual currency rates (27.0% at constant currency), though pro forma revenue declined 7.8% when accounting for acquisitions.

As shown in the following comprehensive financial overview:

The adjusted operating margin contracted to 3.3% from 5.2% in Q3 2024, reflecting integration costs and market pressures. Free cash flow improved to $131 million from $107 million in the prior year, while GAAP loss per share narrowed to $(6.01) from $(9.71) a year earlier.

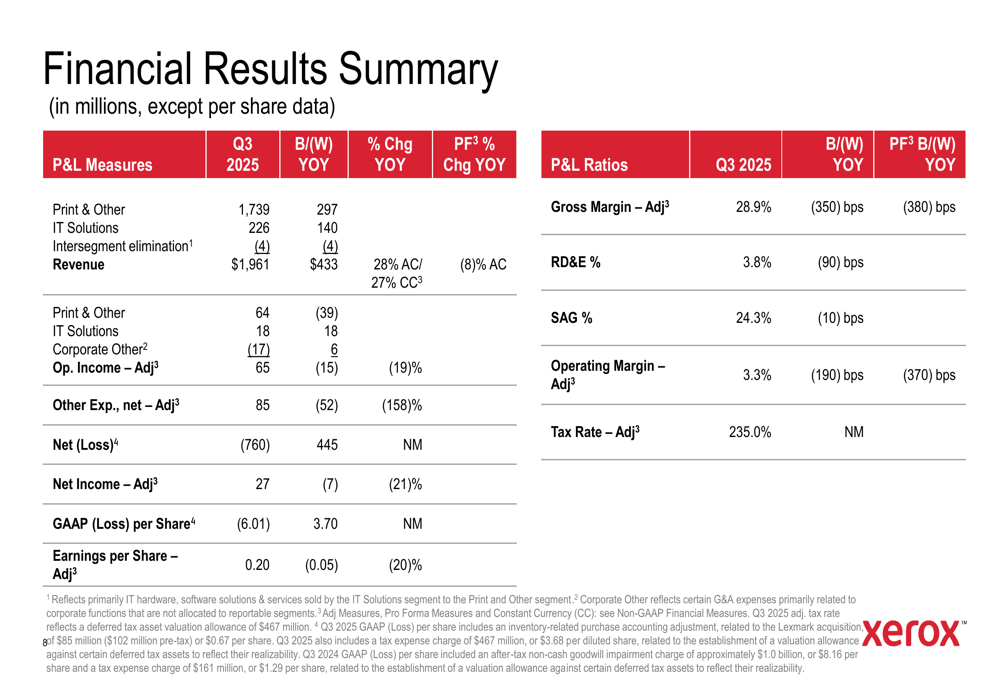

The financial results summary provides additional detail on the company’s performance across segments:

Segment Performance

Xerox’s performance varied significantly across its two primary business segments. The traditional Print & Other segment generated $1.74 billion in revenue, up 20.6% year-over-year, but segment profit declined 37.9% to $64 million with margins contracting to 3.7%.

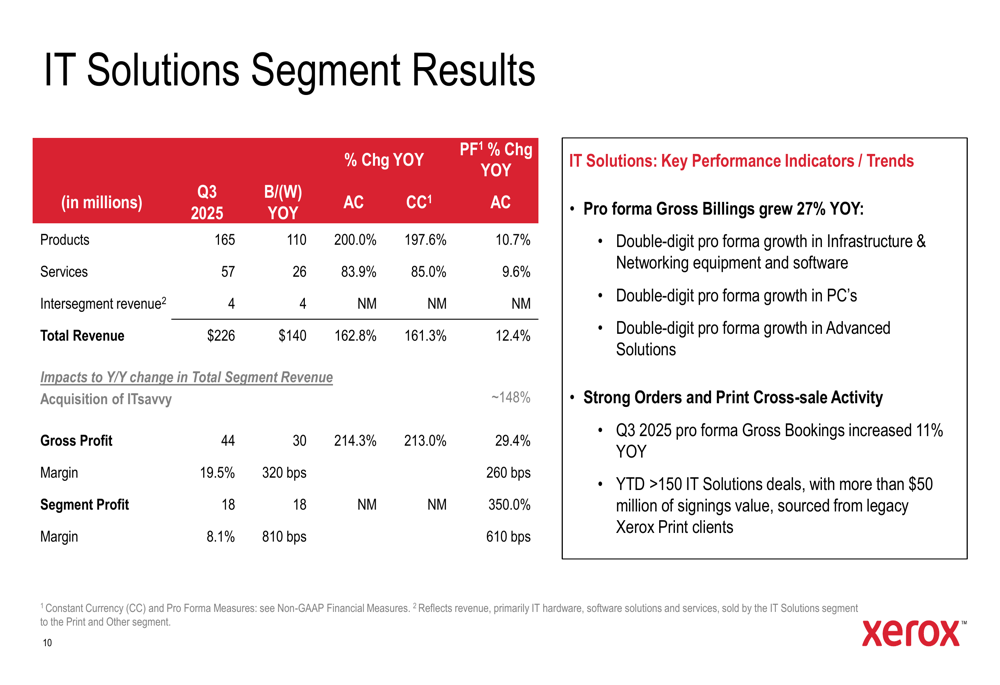

The IT Solutions segment showed impressive growth, with revenue increasing 162.8% to $226 million. This segment delivered $18 million in profit, a substantial improvement from breakeven performance in the prior year. The strong performance in IT Solutions reflects Xerox’s strategic pivot toward higher-growth digital services.

The company’s IT Solutions segment results demonstrate the progress in this strategic growth area:

Strategic Initiatives

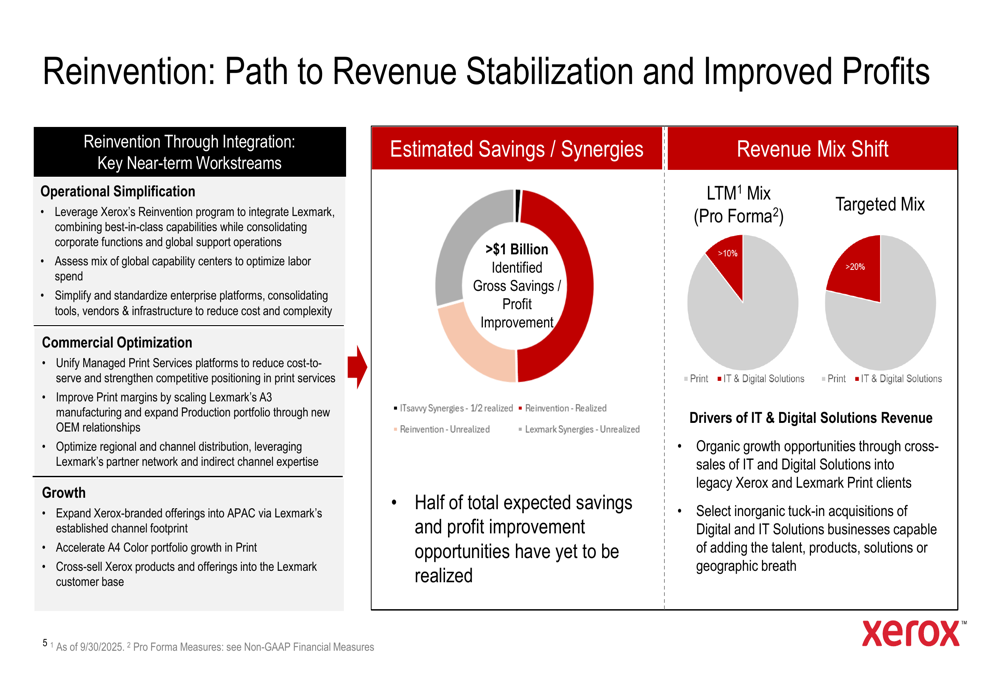

Xerox outlined its strategic priorities focused on executing its reinvention plan, realizing benefits from acquisitions, and strengthening its balance sheet. The company is particularly focused on integrating Lexmark, which it acquired earlier in 2025.

The company’s path to revenue stabilization and improved profitability centers on operational simplification, commercial optimization, and growth initiatives, as illustrated in this strategic overview:

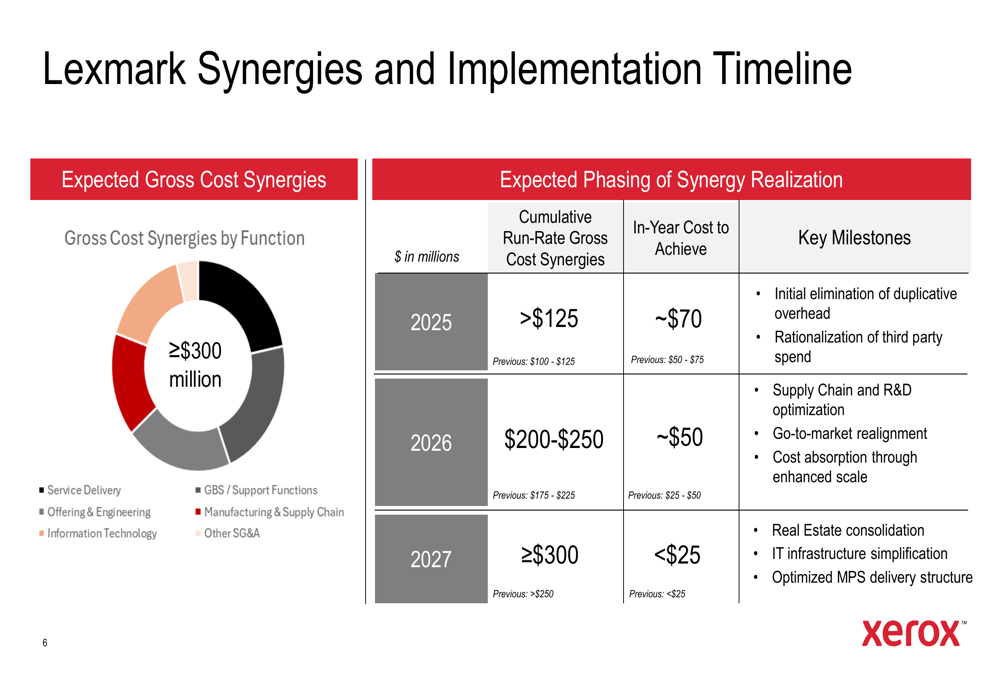

A key component of Xerox’s strategy involves achieving synergies from the Lexmark acquisition. The company has increased its expected gross cost synergies to over $300 million, up $50 million from previous estimates. These synergies are expected to be realized gradually through 2027, with more than $125 million in run-rate gross cost synergies anticipated by the end of 2025.

The detailed implementation timeline for Lexmark synergies shows the phased approach:

Capital Structure and Debt Management

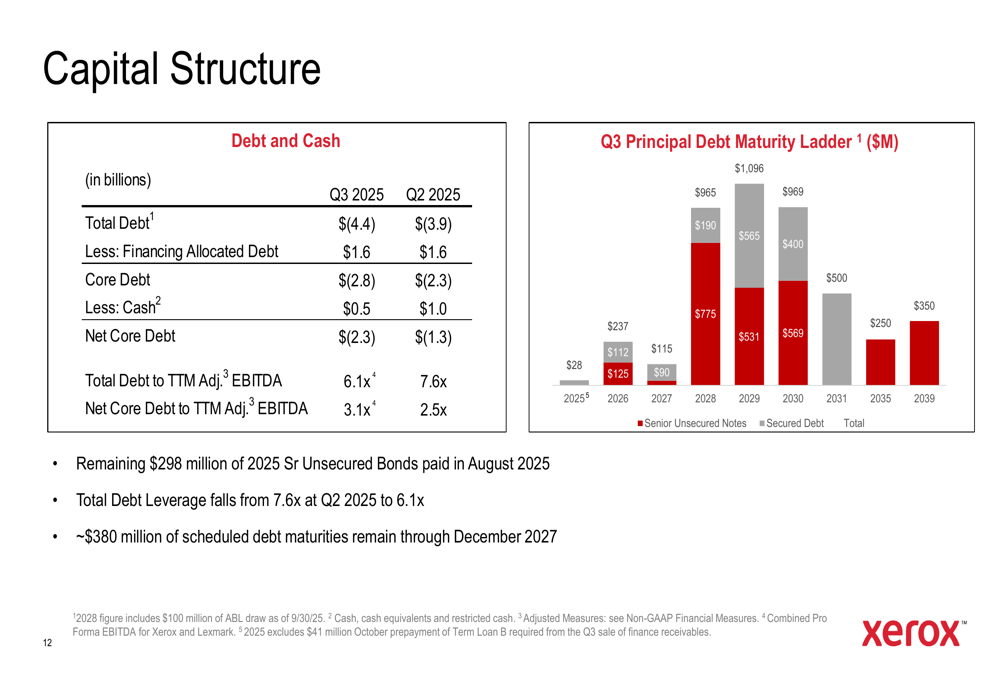

Xerox’s balance sheet reflects the impact of recent acquisitions, with total debt increasing to $4.4 billion in Q3 2025 from $3.9 billion in Q2 2025. The company’s leverage ratio, measured as Total Debt to TTM Adjusted EBITDA, improved to 6.1x from 7.6x in the previous quarter, though Net Core Debt to TTM Adjusted EBITDA deteriorated to 3.1x from 2.5x.

The company’s capital structure and debt maturity profile are detailed in the following chart:

Forward-Looking Statements

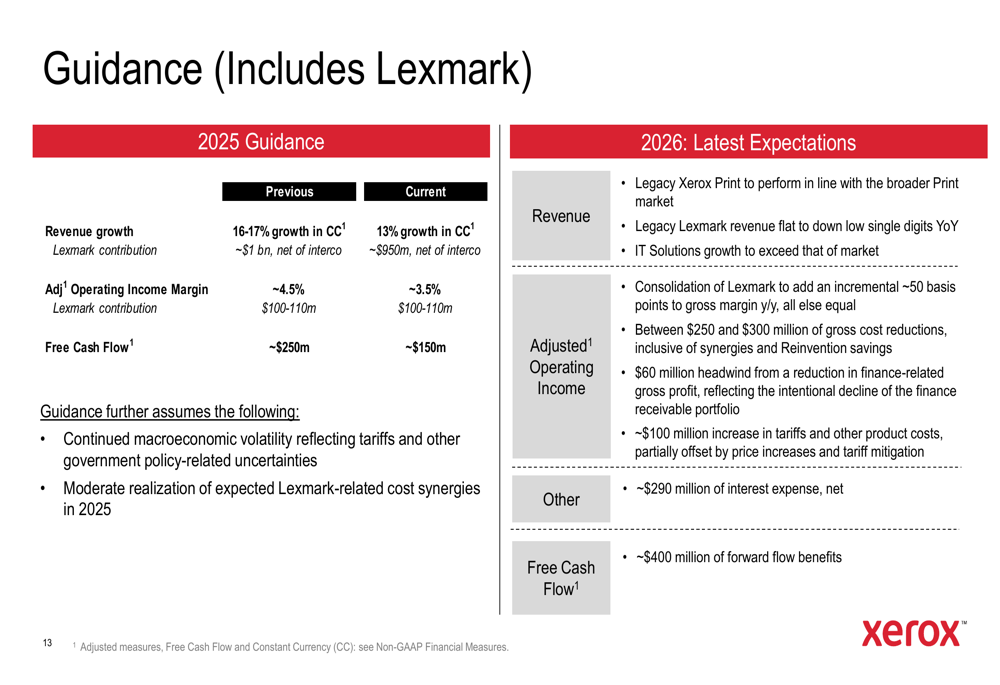

In response to the challenging quarter, Xerox revised its full-year 2025 guidance downward across all key metrics. The company now expects revenue growth of 13% in constant currency, down from the previous guidance of 16-17%. Adjusted operating income margin is projected at approximately 3.5%, reduced from the earlier forecast of 4.5%. Free cash flow expectations were cut to approximately $150 million from $250 million previously.

The comprehensive guidance update, including expectations for 2026, is presented in this overview:

Xerox cited macroeconomic uncertainty, delayed purchasing decisions, and integration challenges as key factors behind the revised outlook. For 2026, the company expects its legacy print business to perform in line with the broader print market, while Lexmark revenue is anticipated to be flat to down low single digits year-over-year. IT Solutions growth is expected to exceed market rates, providing a potential bright spot.

Conclusion

Xerox’s Q3 2025 results reveal a company in transition, balancing the challenges of a declining print business with the opportunities presented by its growing IT Solutions segment. While the significant revenue growth demonstrates progress in the company’s transformation strategy, the deteriorating margins and downward revision of guidance highlight the difficulties in executing this pivot.

Investors appear concerned about the company’s ability to successfully integrate Lexmark while maintaining profitability, as evidenced by the sharp stock decline following the earnings release. However, the increased synergy targets and growing IT Solutions segment provide potential pathways to improved performance in future quarters.

As Xerox continues its reinvention journey, the company’s ability to accelerate cost savings, successfully integrate acquisitions, and grow its digital business will be critical factors in determining its long-term success in an increasingly digital business environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.