Trump says Nvidia not allowed to sell advanced AI chips to China- 60 Minutes

Introduction & Market Context

Xior Student Housing BVBA (XIOR) presented its H1 2025 results on August 7, 2025, showcasing strong operational performance and strategic growth initiatives. The company’s shares closed at €31.65, up 0.95% on the day of the presentation, reflecting positive investor sentiment toward the results.

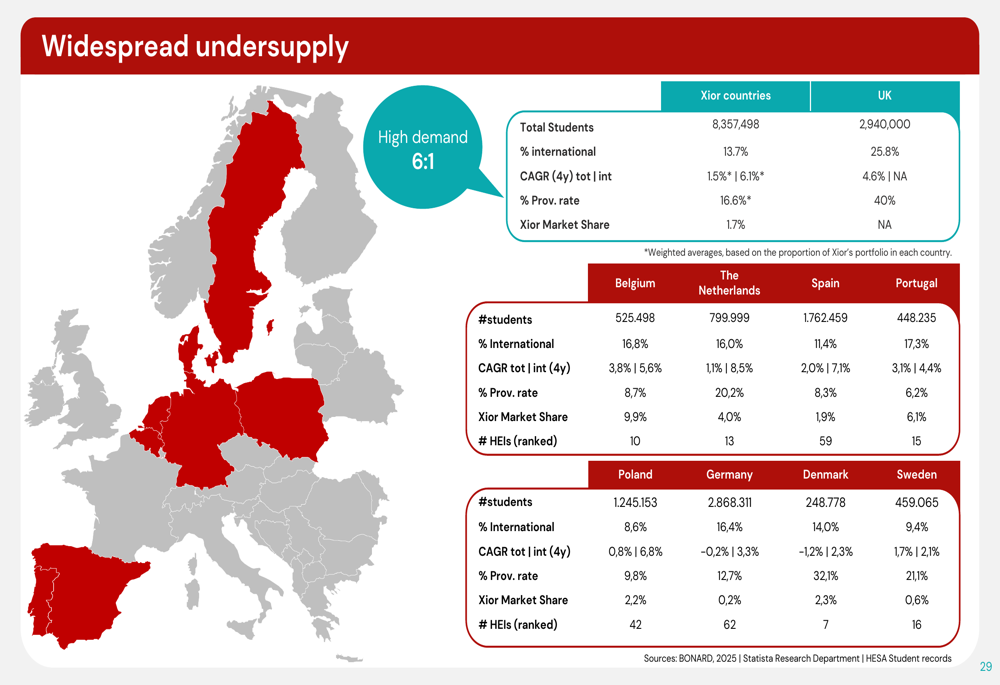

As a leading pan-European student housing provider operating across eight countries with approximately 25,500 units, Xior continues to benefit from structural undersupply in its markets, with an estimated six students competing for each available bed and a low provision rate of 16%.

Executive Summary

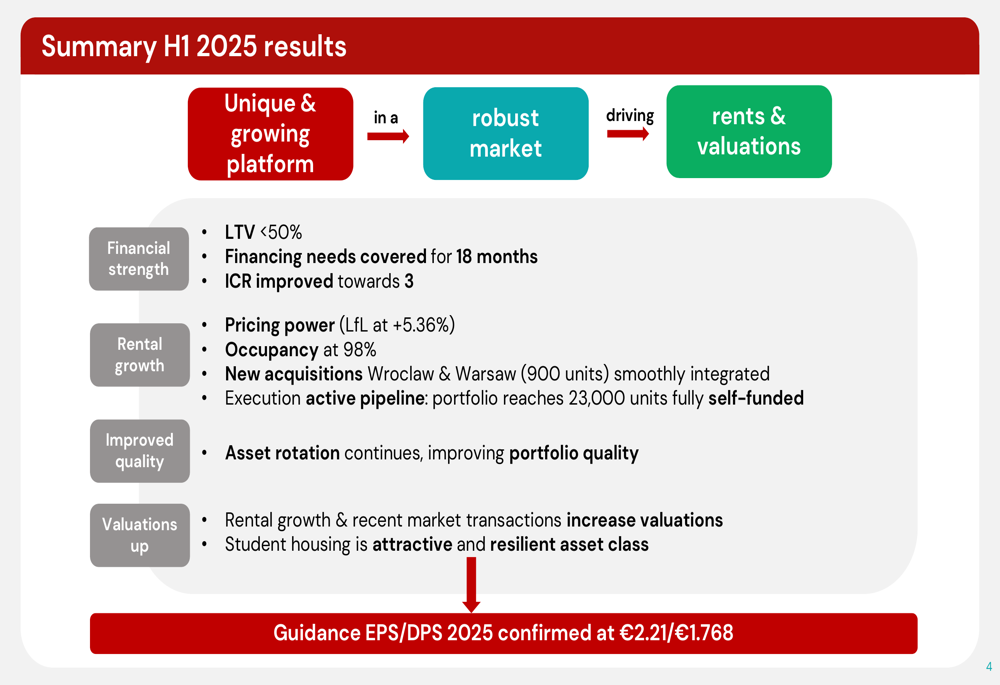

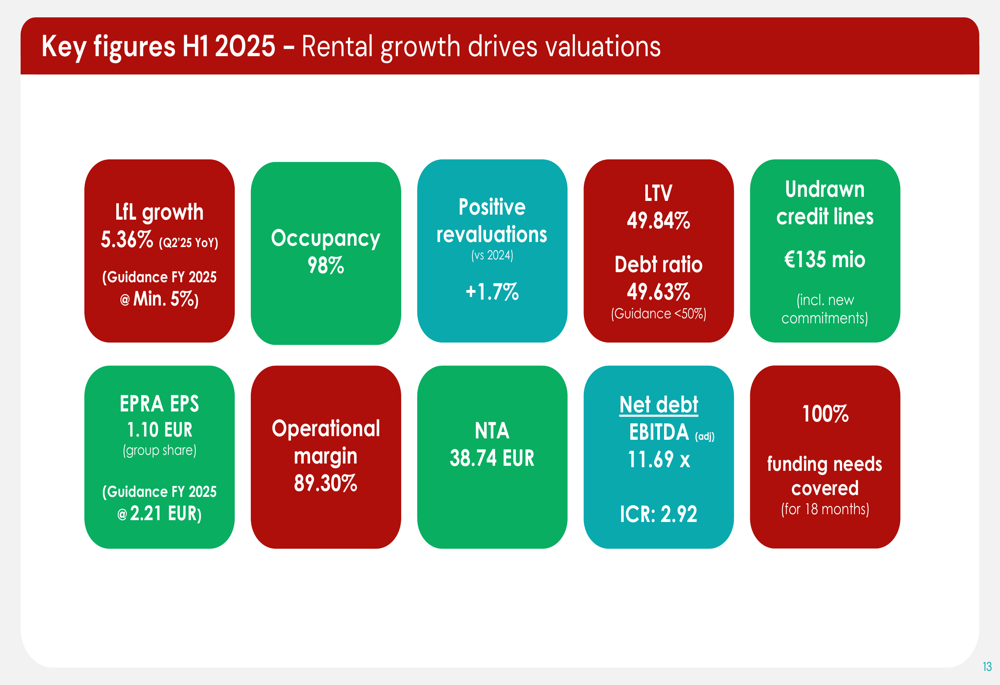

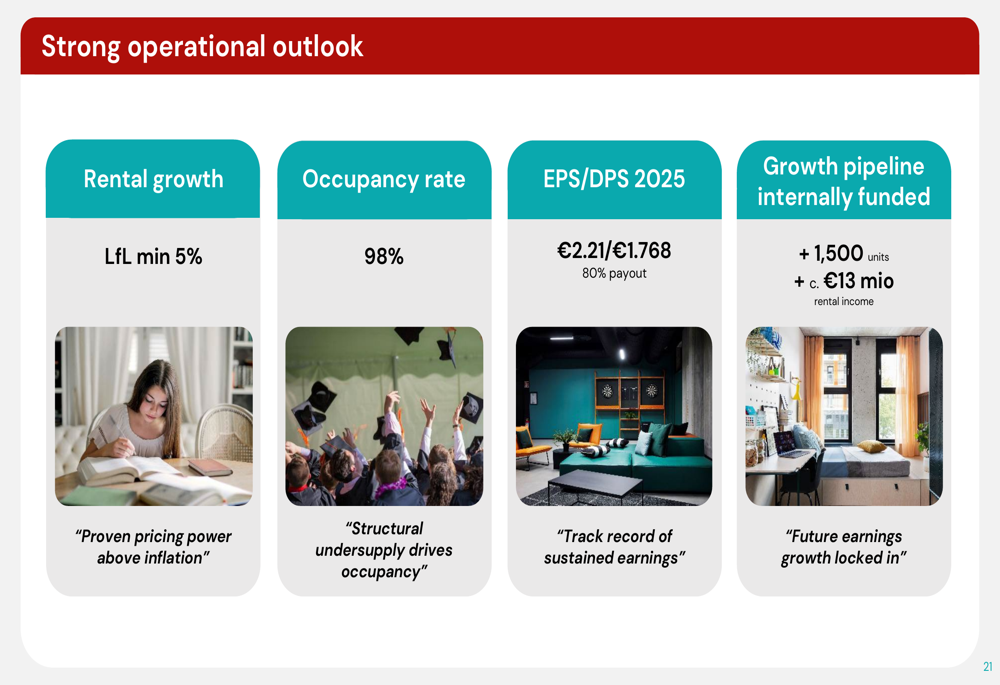

Xior reported robust H1 2025 results, highlighted by like-for-like rental growth of 5.36% and maintained high occupancy of 98% despite implementing higher rental prices. The company confirmed its full-year 2025 guidance for EPRA earnings per share of €2.21 and dividend per share of €1.768, representing an 80% payout ratio.

As shown in the following summary of H1 2025 results, Xior has positioned itself as a unique and growing platform in a resilient market:

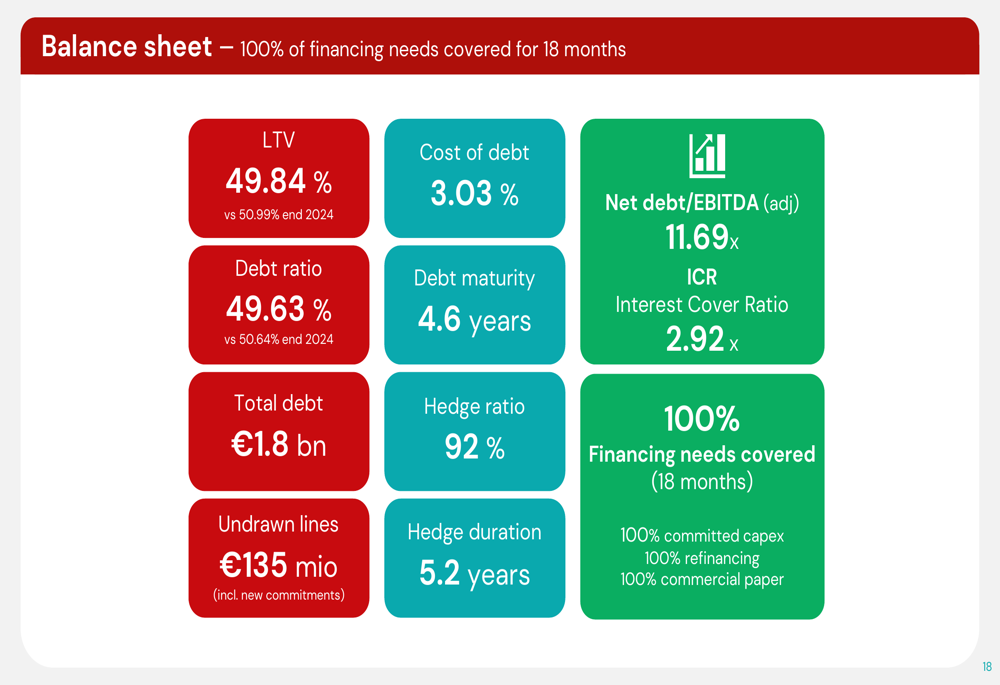

The company’s financial position improved during the first half, with LTV reduced to 49.84% (from 50.99% at end 2024) and debt ratio improved to 49.63% (from 50.64% at end 2024), while maintaining 100% coverage of financing needs for the next 18 months.

Quarterly Performance Highlights

Xior’s operational performance remained strong, with booking rates across all countries in line with or exceeding last year’s levels. The company noted that demand remains robust despite higher rental prices, confirming the resilient nature of the student housing market.

The detailed key figures for H1 2025 demonstrate Xior’s solid performance across multiple metrics:

EPRA earnings reached €1.10 per share (group share) for H1 2025, on track to meet the full-year guidance of €2.21. The company maintained an impressive operational margin of 89.30%, while its net asset value (EPRA NTA) stood at €38.74 per share.

The portfolio saw positive revaluations of 1.7% compared to 2024, reflecting the continued attractiveness of student housing assets in a challenging real estate environment. This valuation growth supports Xior’s strategy of focusing on high-quality assets in undersupplied markets.

Strategic Initiatives

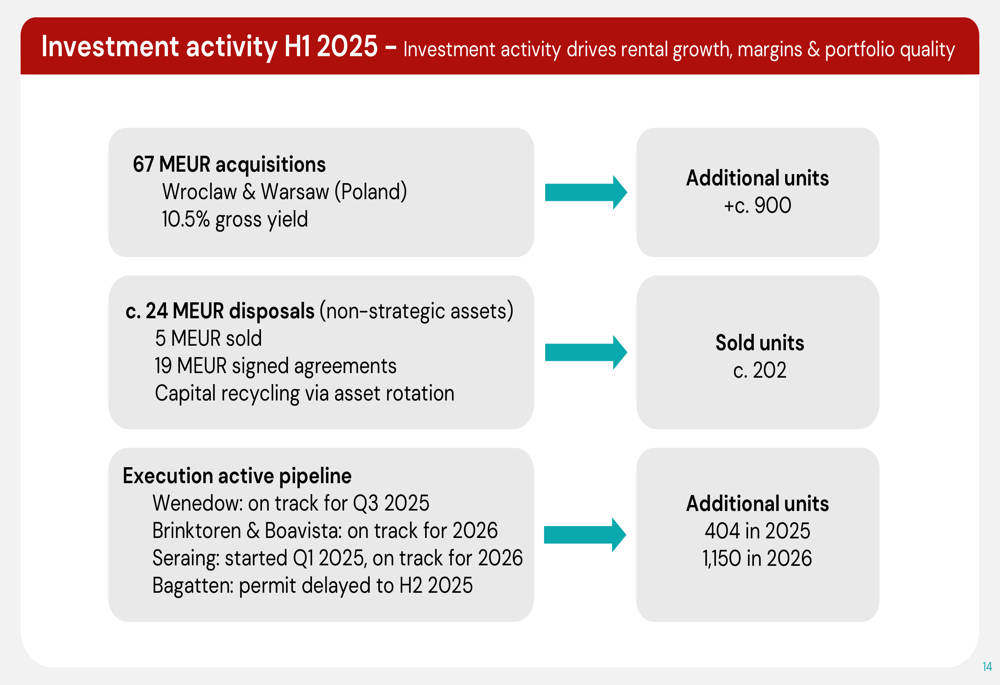

Xior’s investment activity during H1 2025 focused on strategic expansion in Poland and continued execution of its development pipeline:

The company acquired approximately 900 units in Warsaw and Wroclaw, Poland, at an attractive gross yield of 10.5%, representing a total investment of €67 million. These acquisitions strengthen Xior’s position in the growing Polish student housing market.

Simultaneously, Xior continued its asset rotation strategy, divesting approximately €24 million of non-strategic assets, including €5 million already sold and €19 million with signed agreements. This approach allows the company to recycle capital into higher-yielding opportunities.

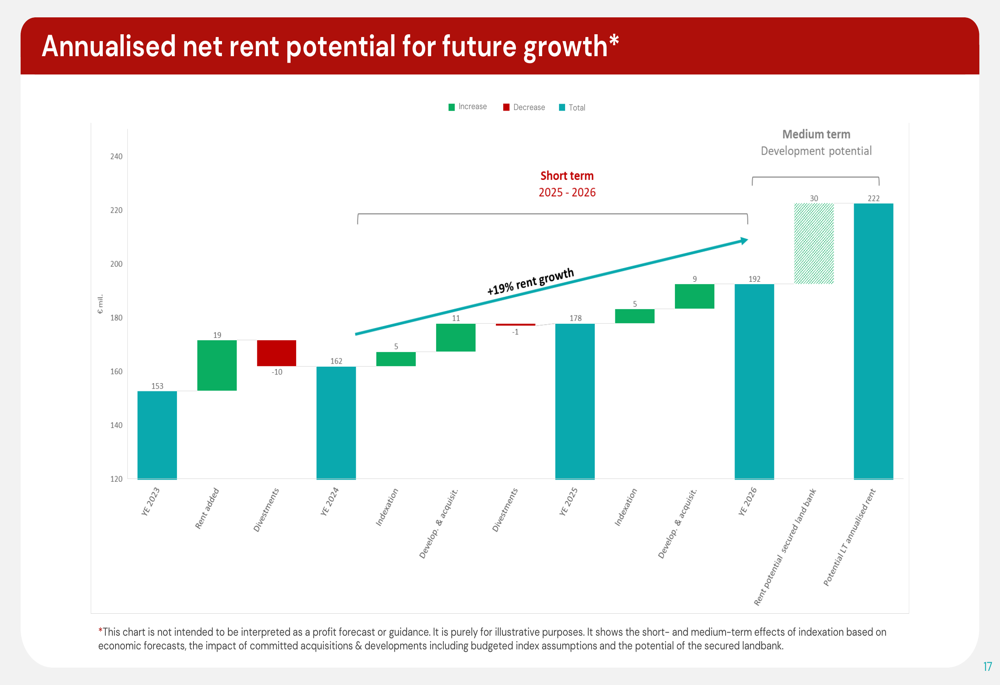

The company’s growth potential is further illustrated by its projected annualized net rent growth:

Xior’s development pipeline is set to deliver significant growth, with 404 additional units expected in 2025 and 1,150 units in 2026. These developments, including projects in Warsaw, Amsterdam, Porto, and Seraing, are projected to generate €13 million in additional rental income with limited remaining capital expenditure of €24 million.

The company is also making progress on its digitization initiatives, with two-thirds of its Dutch units now operating on its new IT platform. The rollout is expected to continue across the portfolio, enhancing operational efficiency and improving the student experience.

Financial Position

Xior’s balance sheet continues to strengthen, with key metrics showing improvement:

The company’s LTV ratio decreased to 49.84% (from 50.99% at end 2024), while its debt ratio improved to 49.63% (from 50.64% at end 2024). With a cost of debt at 3.03%, hedge ratio of 92%, and average debt maturity of 4.6 years, Xior has established a stable financial foundation.

The Interest Cover Ratio (ICR) improved to 2.92x, approaching the company’s target of 3x. Xior has secured 100% of its financing needs for the next 18 months, including committed capital expenditures, refinancing requirements, and commercial paper.

The company’s capital structure was reinforced through a successful accelerated bookbuild offering of €80 million in January 2025 and an optional dividend with 47% take-up, resulting in approximately €25 million of additional capital.

Forward-Looking Statements

Xior’s operational outlook remains strong, with the company confirming its guidance for 2025:

The company expects to maintain minimum like-for-like rental growth of 5% and an occupancy rate of 98% for the full year 2025. EPRA earnings per share are projected at €2.21, supporting a dividend per share of €1.768 (80% payout ratio).

Xior’s growth pipeline is internally funded and expected to add approximately 1,500 units and €13 million in rental income. The company’s focus on maintaining LTV below 50% while executing its growth strategy demonstrates its commitment to balancing expansion with financial discipline.

The widespread undersupply in Xior’s markets continues to provide a favorable backdrop for growth:

With international student growth of 6.1% and provision rates significantly below demand across its operating markets, Xior is well-positioned to benefit from the structural imbalance between supply and demand in the student housing sector.

As Xior continues to execute its strategy of expanding in undersupplied markets while maintaining financial discipline, the company appears well-positioned to deliver sustainable growth and returns to shareholders in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.