Bitcoin price today: surges to $122k, near record high on US regulatory cheer

Introduction & Market Context

Xponential Fitness Inc (NYSE:XPOF) presented its Q2 2025 financial results on August 7, 2025, highlighting a return to profitability despite a slight revenue decline. The boutique fitness franchisor, which has been undergoing significant strategic changes, reported improved margins and continued system-wide sales growth.

However, the market’s initial reaction appears negative, with premarket trading showing a 21.08% decline to $7.60, suggesting investors may have expected stronger results or are concerned about other aspects of the company’s performance.

This quarter marks a significant shift from Q1 2025, when the company reported a net loss of $2.7 million. The presentation also introduced Mike Nuzzo as CEO, bringing over 25 years of experience from companies including Eyemart Express, Petco, and GNC.

Quarterly Performance Highlights

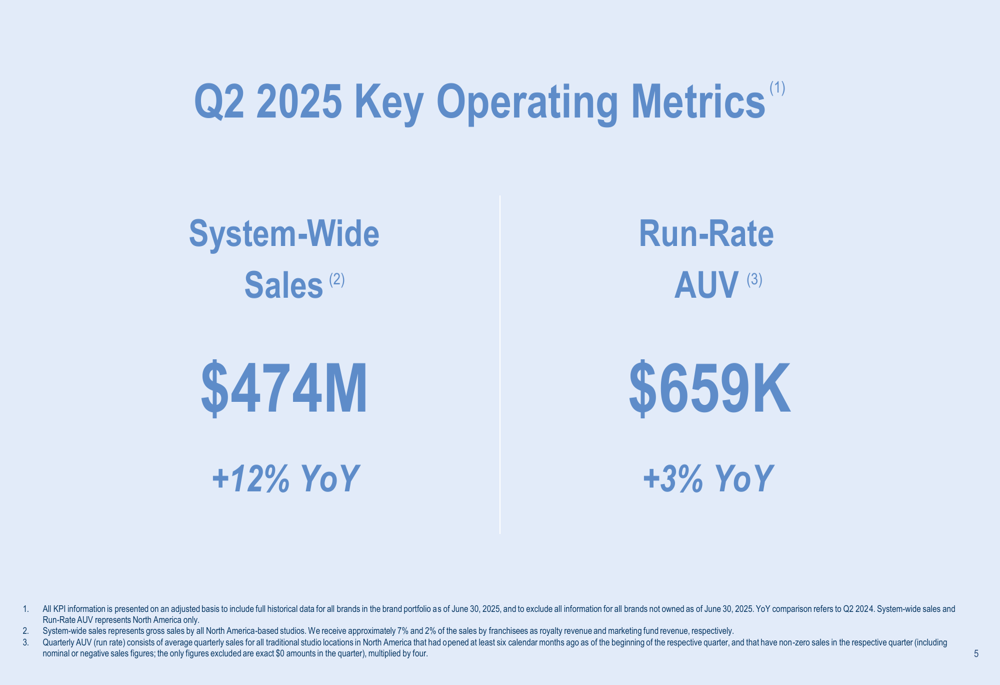

Xponential Fitness reported system-wide sales of $474 million in North America for Q2 2025, representing a 12% year-over-year increase. The company’s average unit volume (AUV) reached $659,000, up 3% compared to the same period last year.

As shown in the following key operating metrics:

Total (EPA:TTEF) membership grew to 863,000, an 8% increase year-over-year, while same-store sales showed modest growth of 1%. Locations open for more than 36 months performed slightly better with 2% same-store sales growth.

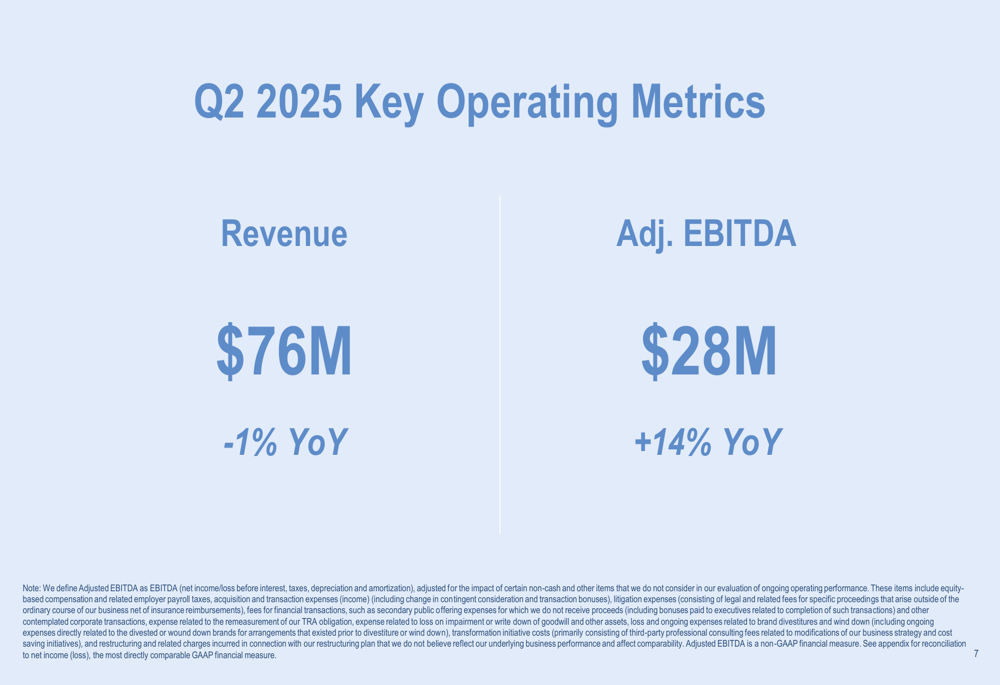

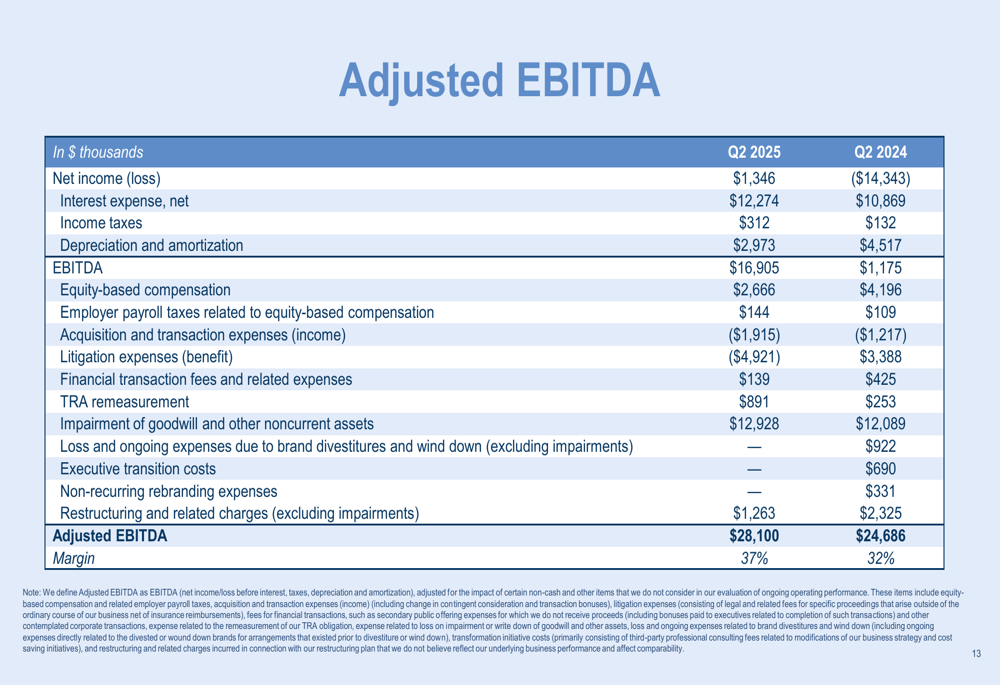

Despite the growth in system-wide sales and membership, revenue declined slightly to $76 million, a 1% decrease compared to Q2 2024. However, Adjusted EBITDA increased significantly to $28 million, representing a 14% year-over-year improvement and a margin expansion from 32% to 37%.

From a global perspective, Xponential continued its expansion, reaching 3,327 studios worldwide (a 7% increase) and 6,344 licenses (a 4% increase).

Strategic Initiatives

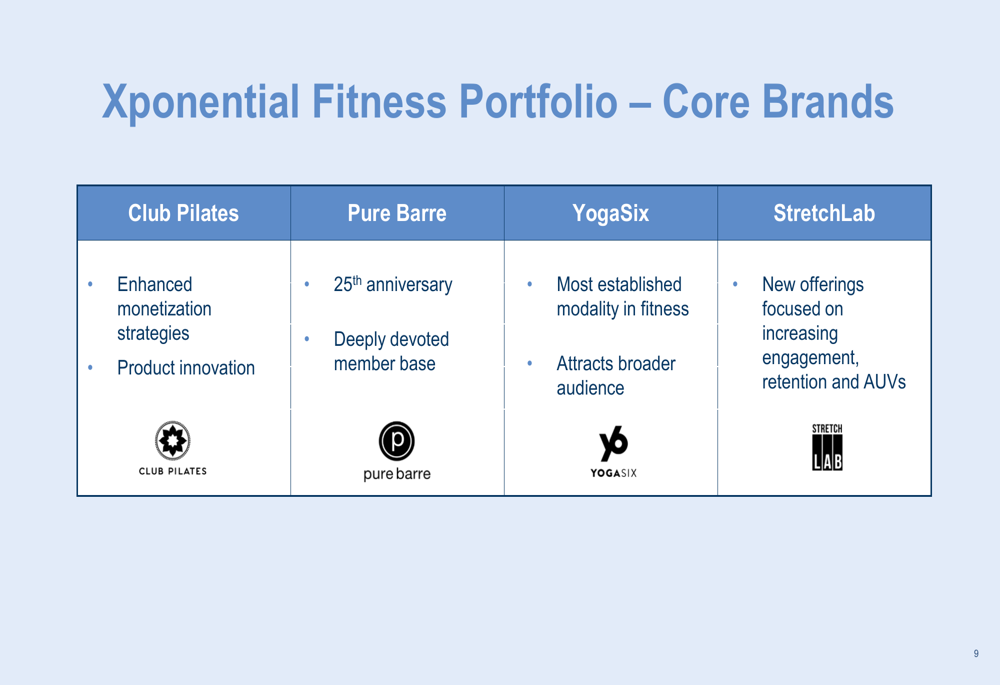

Xponential’s presentation highlighted several key strategic initiatives implemented since its Analyst Day. The company has completed its brand rationalization efforts with the divestitures of Rumble and CycleBar, allowing it to focus on its core portfolio of brands.

The company is now concentrating on four core brands: Club Pilates, Pure Barre, YogaSix, and StretchLab. Each brand has specific strategic focuses, from enhanced monetization strategies for Club Pilates to new offerings designed to increase engagement and retention for StretchLab.

A significant development is the retail transformation through a partnership with Fit Commerce. This initiative outsources Xponential’s wholesale retail business, providing a capital-light, higher-margin strategy with minimum guaranteed commissions of $50 million over a five-year contract.

Additional initiatives include testing unassisted stretch and technology solutions for StretchLab, deploying field operations teams, and implementing franchisee-related initiatives to improve performance across the network.

Detailed Financial Analysis

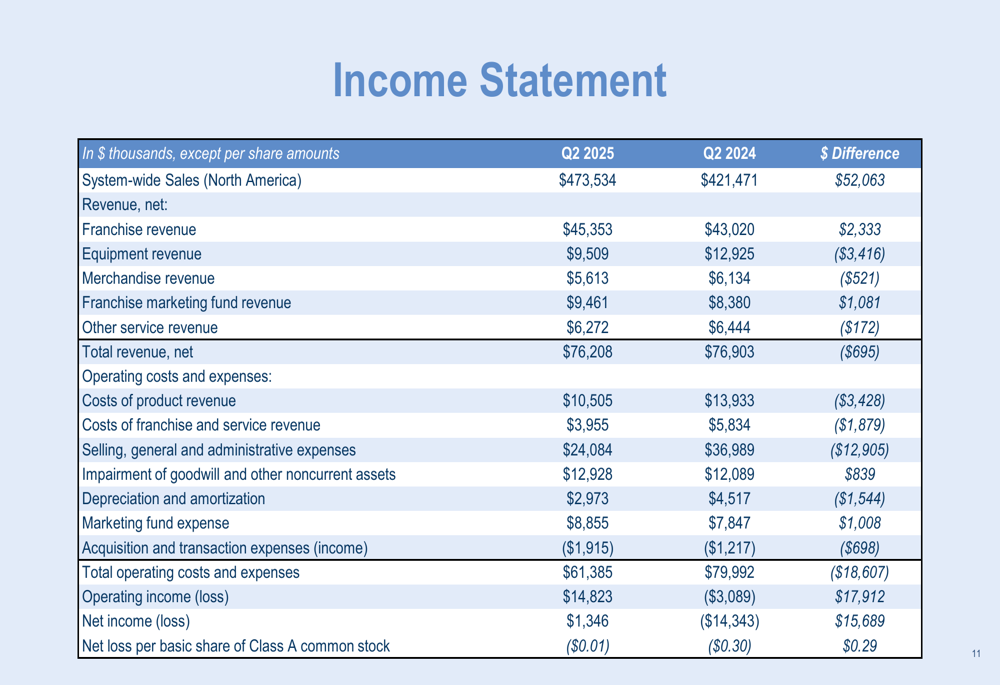

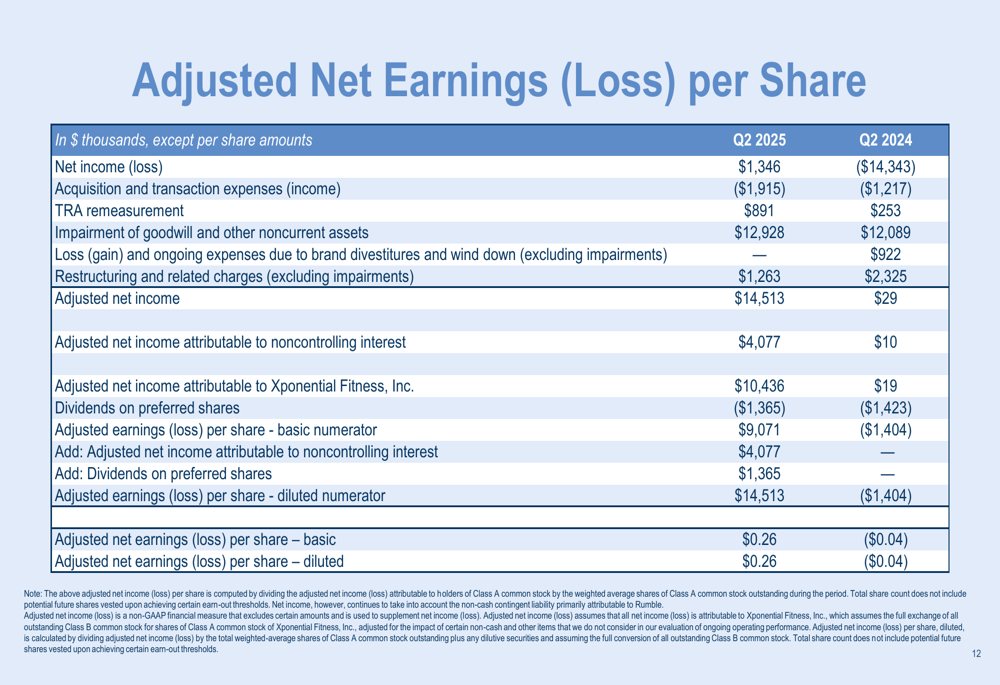

Xponential’s income statement shows a dramatic improvement in profitability. The company reported net income of $1.35 million for Q2 2025, compared to a net loss of $14.34 million in Q2 2024. Operating income also improved significantly to $14.82 million from a loss of $3.09 million in the prior year.

On an adjusted basis, the company’s performance was even stronger. Adjusted net income reached $14.51 million, compared to just $29,000 in Q2 2024. This translated to adjusted earnings per share of $0.26, a substantial improvement from the loss of $0.04 per share in the same period last year.

The reconciliation to Adjusted EBITDA shows the company achieved $28.1 million in Q2 2025, representing a 37% margin, compared to $24.69 million (32% margin) in Q2 2024.

Forward-Looking Statements

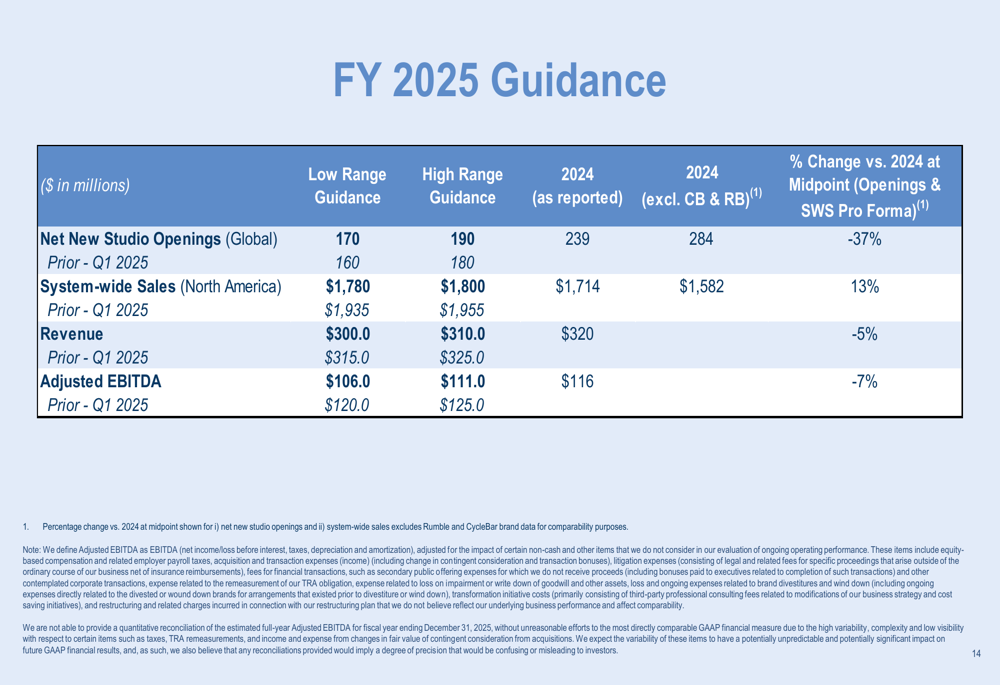

For the full fiscal year 2025, Xponential provided guidance that includes:

- 170-190 new studio openings globally

- System-wide sales (North America) of $1.78-1.8 billion

- Revenue of $300-310 million

- Adjusted EBITDA of $106-111 million

This guidance reflects the company’s strategic shift following the divestitures of CycleBar and Rumble. When comparing to 2024 figures excluding these brands, the guidance suggests continued growth in system-wide sales and Adjusted EBITDA, though revenue is expected to remain relatively flat.

The company’s transition from a sales-focused organization to one prioritizing long-term growth appears to be yielding initial positive results in terms of profitability, though revenue growth remains a challenge. The significant drop in premarket trading suggests investors may be concerned about the slight revenue decline despite the improved bottom line, or may have had higher expectations for the company’s guidance.

As Xponential continues to implement its strategic initiatives and focus on its core brands, investors will be watching closely to see if the improved profitability can be sustained while returning to top-line growth in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.