Fed’s Powell opens door to potential rate cuts at Jackson Hole

Introduction & Market Context

ZimVie Inc. (NASDAQ:ZIMV), a global dental leader specializing in premium implants and digital dentistry solutions, presented its Q1 2025 results on May 8, showcasing significant profitability improvements despite ongoing revenue challenges. The company’s stock responded positively, rising 3.26% in aftermarket trading to $9.50, reflecting investor confidence in the company’s operational efficiency initiatives.

The presentation highlighted a substantial market opportunity, with 8 million U.S. patients seeking treatment for tooth loss annually, yet only 25% receiving tooth replacement solutions. This underserved market represents a key growth avenue for ZimVie’s expanding portfolio of dental implants, biomaterials, and digital dentistry technologies.

As shown in the following slide outlining ZimVie’s market position and opportunity:

Quarterly Performance Highlights

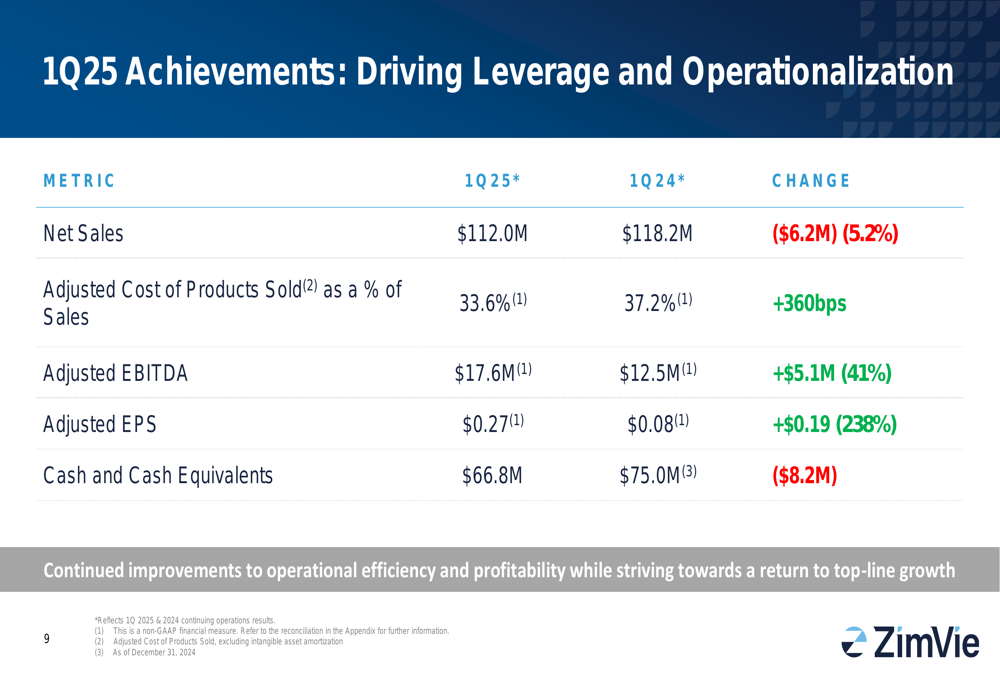

ZimVie reported Q1 2025 net sales of $112.0 million, representing a 5.2% decrease from $118.2 million in the prior year period. However, the company demonstrated remarkable profitability improvements, with adjusted EBITDA increasing 41% to $17.6 million and adjusted earnings per share more than tripling to $0.27 from $0.08 in Q1 2024.

The company attributed these gains to enhanced operational efficiency, with adjusted cost of products sold improving to 33.6% of sales compared to 37.2% in the prior year period. This operational leverage helped offset revenue headwinds and contributed to the significant bottom-line growth.

The following financial summary illustrates ZimVie’s Q1 2025 achievements:

"We’re building a strong foundation for success," CEO Vafa Jamali stated during the earnings call. "Our performance in terms of profitability is coming in better than expected." He also expressed confidence in the dental implant market’s resilience, noting that "dental implants are still very much under adopted."

Product Portfolio and Innovation

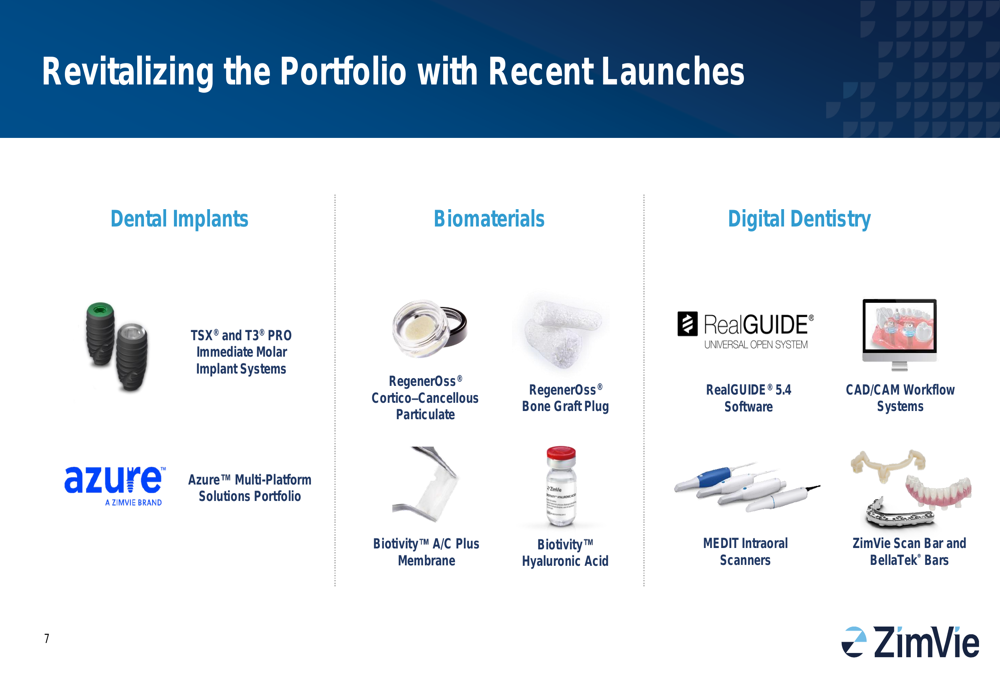

ZimVie’s presentation emphasized its comprehensive dental solutions across three key categories: dental implants, biomaterials, and digital dentistry. The company highlighted recent product launches aimed at revitalizing its portfolio and addressing evolving market needs.

In the dental implants category, ZimVie showcased its TSX® and T3® PRO Immediate Molar Implant Systems, designed to simplify procedures and optimize practice protocols. These premium offerings form the core of the company’s implant business.

As illustrated in the dental implants portfolio overview:

The company’s biomaterials portfolio includes human-donor sourced bone graft materials, custom-shaped allograft bone blocks, and various synthetic bone grafts and barrier membranes. These solutions support bone and tissue regeneration, which is essential for successful dental implant procedures and aesthetic outcomes.

The biomaterials portfolio is detailed in the following slide:

Digital Transformation Strategy

A significant focus of ZimVie’s presentation was its expanding digital dentistry portfolio, which includes RealGUIDE® Software (ETR:SOWGn), BellaTek® Patient Specific Restorative Solutions, and GenTek™ Digital Restorative Solutions. The company reported 39% growth in guided surgery software adoption in FY24, indicating strong market traction for its digital offerings.

The digital portfolio overview demonstrates ZimVie’s comprehensive approach to digital dentistry:

ZimVie emphasized that its AI-facilitated restorative solutions require significantly fewer labor hours, while the ZimVie Encode Emergence workflow reduces chair time and eliminates one restorative impression appointment. These efficiency gains benefit both clinicians and patients, potentially driving greater adoption of the company’s solutions.

The company has continued to expand its digital offerings with recent launches, as shown in the following slide highlighting new products across all categories:

Financial Outlook and Guidance

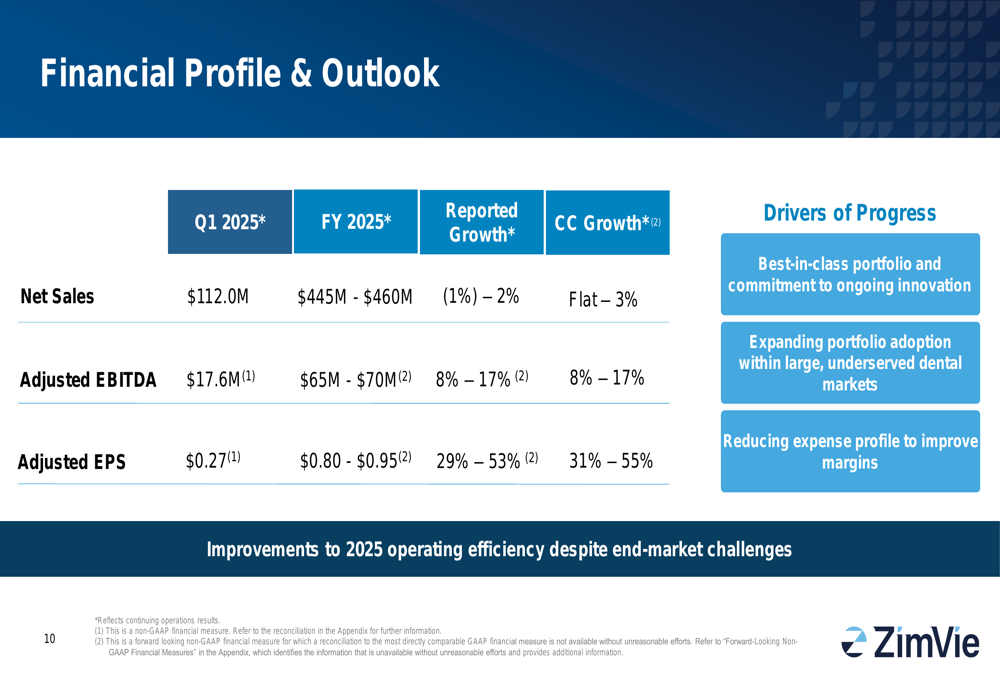

Looking ahead, ZimVie provided a positive outlook for FY 2025, projecting net sales between $445 million and $460 million, representing flat to 3% growth on a constant currency basis. The company expects adjusted EBITDA to range from $65 million to $70 million (8-17% growth) and adjusted EPS between $0.80 and $0.95 (29-53% growth).

This guidance reflects ZimVie’s confidence in its ability to continue improving operational efficiency while working toward a return to top-line growth. The company identified three key drivers for future progress: its best-in-class portfolio and commitment to innovation, expanding adoption within underserved dental markets, and ongoing expense reduction to improve margins.

The detailed financial outlook is presented in the following slide:

For Q2 2025, the company forecasts sales between $112 million and $114 million, suggesting a stabilization of revenue compared to Q1. ZimVie also noted it anticipates absorbing approximately $3 million in tariff costs while maintaining flexibility in its manufacturing strategy.

With a market capitalization of $248 million and a price-to-book ratio of 0.67, ZimVie’s stock is trading near its 52-week low, potentially indicating undervaluation given the company’s improving profitability metrics and positive outlook. However, investors should consider the ongoing revenue challenges and the competitive nature of the premium dental implant market when evaluating the company’s prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.