Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

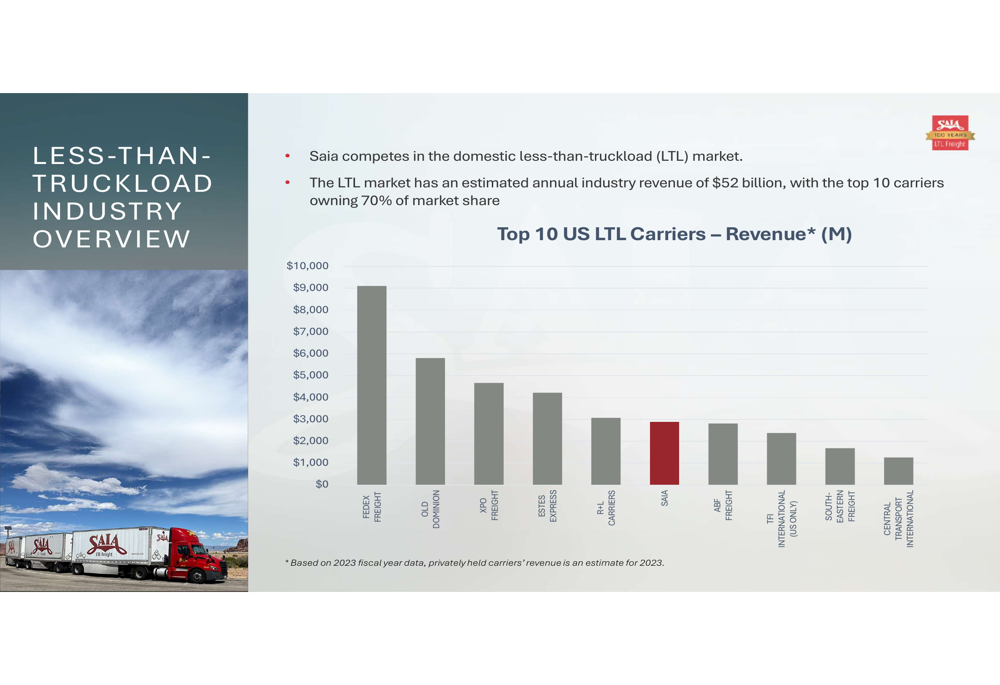

Saia , Inc. (NASDAQ:SAIA), the sixth-largest less-than-truckload (LTL) carrier in the United States, has completed a year of unprecedented expansion in 2024. Operating in a domestic LTL market with an estimated annual industry revenue of $52 billion, Saia has strategically positioned itself for long-term growth through substantial capital investments, despite facing some near-term margin pressures.

The company competes in a concentrated market where the top 10 carriers control approximately 70% of market share. With its recent expansion, Saia now provides direct service to all 48 contiguous states, significantly increasing its addressable market and competitive positioning.

As shown in the following chart of the top LTL carriers by revenue, Saia holds the sixth position in this competitive landscape:

Q4 and Full-Year 2024 Performance Highlights

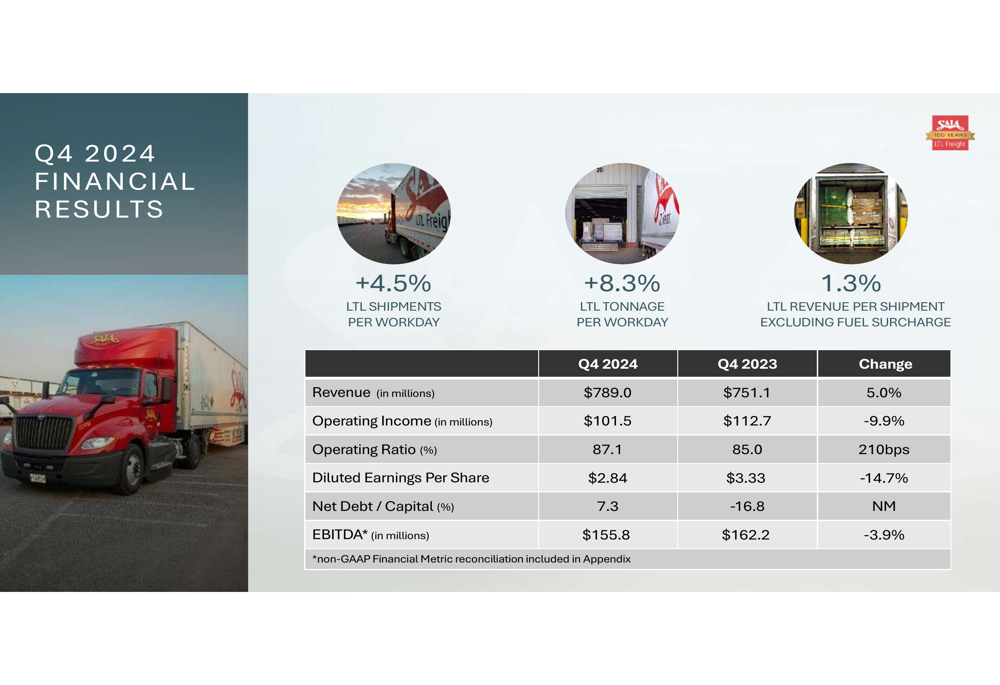

Saia reported mixed results for the fourth quarter of 2024, with revenue growth offset by margin compression. Q4 revenue reached $789.0 million, a 5.0% increase compared to the same period in 2023, driven by higher shipment volumes and tonnage. However, operating income declined 9.9% to $101.5 million, and diluted earnings per share fell 14.7% to $2.84.

The company's operational metrics showed positive momentum with LTL shipments per workday increasing 4.5% and tonnage per workday rising 8.3% in Q4. Revenue per shipment (excluding fuel surcharge) grew modestly at 1.3%. The operating ratio deteriorated to 87.1% from 85.0% in the prior-year quarter, reflecting the costs associated with the company's aggressive expansion strategy.

The quarterly financial performance is summarized in the following slide:

For the full year 2024, Saia delivered more robust results with revenue of $3.2 billion, an 11.4% increase from 2023. Operating income grew 4.7% to $482.2 million, while diluted EPS rose 1.9% to $13.51. The company's operating ratio for the year was 85.0%, compared to 84.0% in 2023, indicating a slight decrease in operational efficiency.

Annual performance metrics showed strong volume growth, with LTL shipments per workday up 11.5% and tonnage per workday increasing 8.0%. The complete annual financial results are illustrated below:

Strategic Investments and Expansion

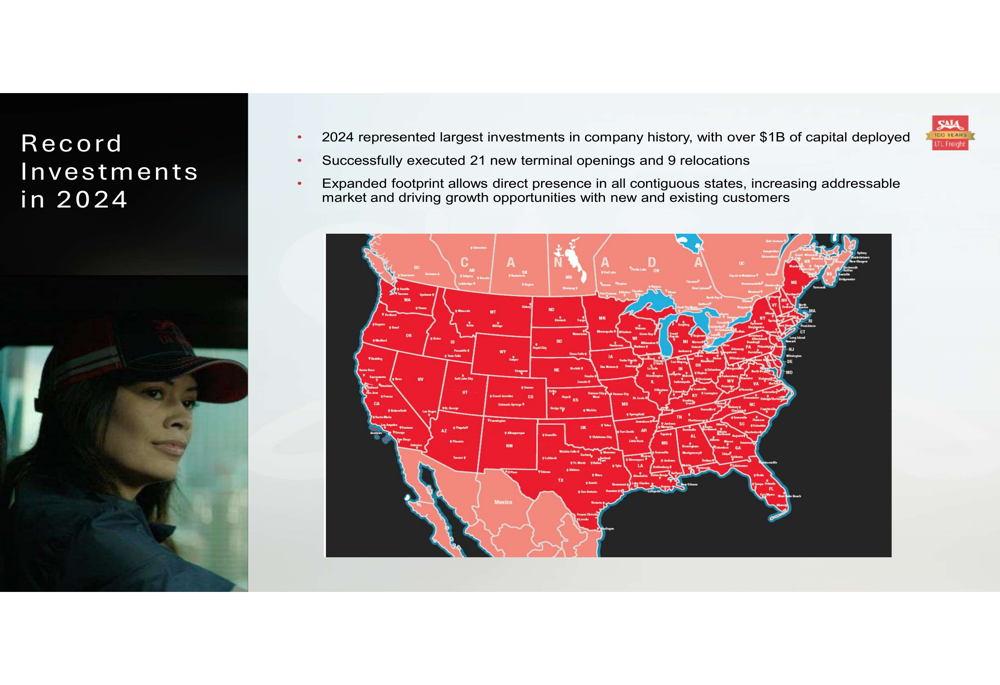

The cornerstone of Saia's 2024 strategy was its record capital deployment, with over $1 billion invested throughout the year. This investment supported the opening of 21 new terminals and the relocation of 9 existing facilities, completing the company's expansion to all 48 contiguous states.

This expanded footprint has significantly increased Saia's market reach, with approximately 61% of U.S. zip codes now within 50 miles of a Saia facility, up from just 35% in 2017. The company now directly services 99% of outbound industry revenue, compared to 84% in 2017.

The following map illustrates Saia's expanded terminal network across the United States:

These investments are part of a longer-term capital allocation strategy, with over $2 billion invested in the business since 2021. The company plans to continue this trajectory with an additional $700 million investment planned for 2025.

The breakdown of capital expenditures and EBITDA growth over recent years demonstrates Saia's commitment to reinvesting in its business:

Long-Term Growth Trends

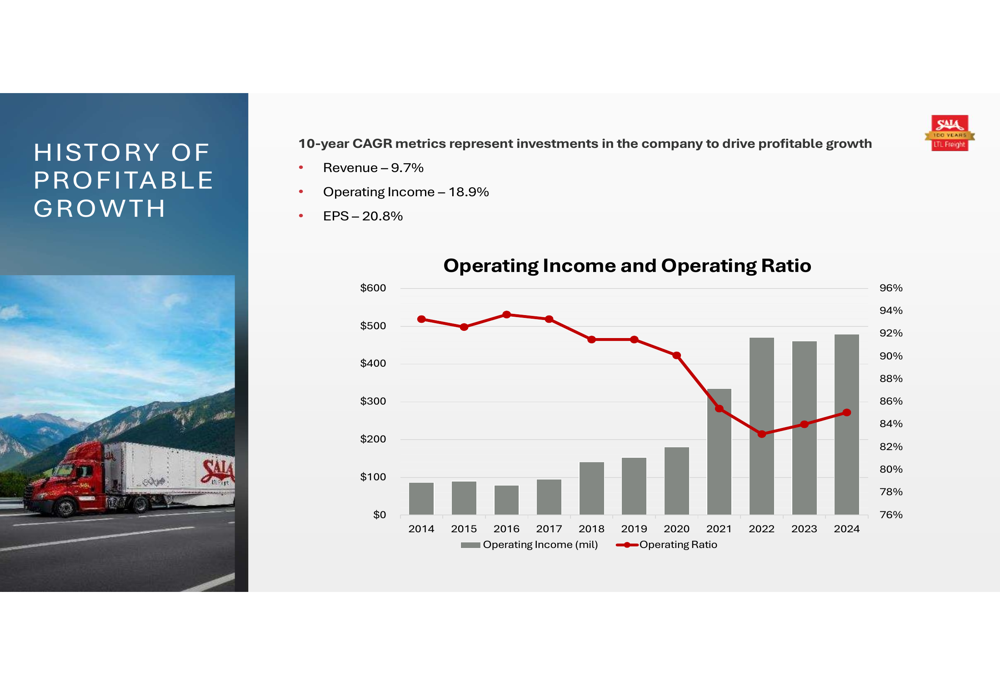

Despite the near-term pressure on margins, Saia's long-term growth trajectory remains impressive. The company has achieved a 10-year compound annual growth rate (CAGR) of 9.7% for revenue, 18.9% for operating income, and 20.8% for earnings per share.

This consistent performance has been accompanied by steady improvements in service quality. The cargo claims ratio, a key indicator of service reliability, improved to 0.58% in 2024, down from approximately 0.9% in 2015. The company now delivers approximately 60% of shipments within 48 hours, with an average length of haul of 891 miles.

The following chart illustrates Saia's long-term improvement in operating income and operating ratio:

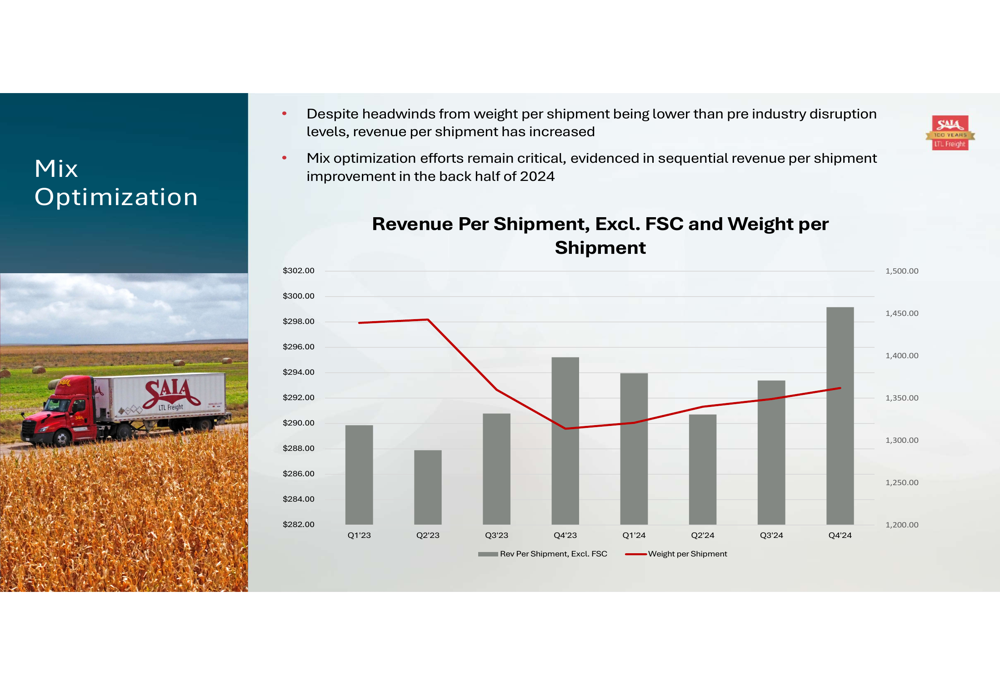

The company has also maintained pricing discipline despite fluctuations in shipment weight. Revenue per shipment (excluding fuel surcharge) has shown a four-year CAGR of 8.3%, increasing from $213.71 in 2020 to $294.23 in 2024. This pricing power has been maintained even as the average weight per shipment has decreased from pre-pandemic levels.

The relationship between revenue per shipment and weight per shipment is shown in the following chart:

Forward-Looking Statements and Outlook

Looking ahead, Saia appears well-positioned to leverage its expanded network and service improvements to drive continued growth. The company maintains a solid financial position with total borrowings of $200.3 million and total liquidity of $493.3 million as of December 31, 2024.

Management emphasized that the significant investments made in 2024 position Saia for volume growth and market share gains in the coming years. The nationwide footprint expands the addressable market and creates opportunities with both new and existing customers.

The company highlighted that each 100 basis points of operating margin improvement would translate to approximately $0.91 per share in additional earnings, underscoring the potential leverage in the business model as recent investments mature.

While near-term margins have been impacted by expansion costs, wage increases, and general inflation, management remains confident that network expansion will ultimately allow for better leverage of fixed costs and drive a best-in-class cost structure over time.

As Saia continues to execute its growth strategy, investors will be watching closely to see if the substantial investments of 2024 translate into the anticipated improvements in market share, revenue growth, and ultimately, operating margins in the quarters ahead.

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.