NHL signs licensing deals with prediction-market startups Kalshi and Polymarket - WSJ

Investors have been waiting for Dell Technologies Inc (NYSE:DELL) to spin out its shares of VMware Inc (NYSE:VMW) ever since the personal computing giant bought EMC in 2016, and have been waiting for a fully independent VMWare just about since EMC bought it in 2003. That happened last week, with Dell completing a full spin off of VMWare. The companies have an ongoing sales agreement, and Michael Dell is chairman of each company independently, but VMWare is finally on its own.

Dell shares post-VMW are still an attractive investment. Dell combines a legacy storage company – EMC – with a legacy personal computer company, which seems unexciting in a world of cloud software and super powerful phones and wearables. It has also already risen 130%+ over the last couple years in the run-up to the spin-off, outperforming both the Nasdaq and the S&P 500.

And yet, the current pricing of around $56/share is reasonable. Dell is set up to deliver solid shareholder returns.

Note: This Investing Pro chart adjusts for the VMW spin-off, which happened on November 1st.

Revisiting the Dell Stock Story

Dell Technologies combines two main units – Infrastructure Solutions Group (ISG) and Client Solutions Group (CSG). ISG is closer to legacy EMC, providing storage, servers, and networking services. This business has historically produced around 11% operating margins, and has grown at a 2% CAGR since the year ending January 2018, the first full year that Dell had EMC. The growth of cloud storage like Amazon Web Services or Microsoft’s Azure has stolen a lot of the thunder from legacy EMC’s business.

ISG saw more of a hit from the pandemic as infrastructure spending slowed, and thus has more room to rebound – it is up 3.5% so far this year. Dell is targeting stronger growth in this segment, at a 3-5% CAGR starting with the current fiscal year (we are in FY 22, which ends in January).

I’m not going to pretend to have the nuances down of server industry growth, but it seems likely that the need for computing power will increase over time, and that there will be a need for more than public cloud solutions from the top three or four players. This seems like a reasonable target for Dell to hit.

The other segment is the Client Solutions Group, what you most likely interact with by buying a Dell PC. This saw a big Covid-related surge as people went out and bought new laptops and other home office hardware. CSG produces operating margins of around 7%, though it was in the 4-5% range as of a few years ago. This is a fairly mature industry, with established competitors like Lenovo (OTC:LNVGY) and HP (NYSE:HPQ), and the pandemic period seems especially anomalous – CSG grew 23.5% in the first half of this fiscal year (February-July 2021), vs. a CAGR of 6% since 2016. So we should be mindful of the risk for a hangover, since we can only restock our home office so many times. Dell’s target is for 2-3% growth from FY 22-FY 26, which is essentially flat with their H1 runrate (since the growth is from last year as a base).

(Dell has an “other businesses” line that includes Secureworks Corp (NASDAQ:SCWX), Virtustream, and the soon-to-be-divested Boomi, and the results of this unit, “are not material to the company’s overall results.” We’ll come back to Boomi, and only Boomi, in a second).

The bottom line is that Dell is not going to be a fast grower. They spun out both their fastest growing and highest margin business in VMware. Dell is still worth considering as an investment for what it already is and what the spin-off’s effect has on the legacy business.

The Bull Case

- Cleaner Balance Sheet

One of the challenges with understanding Dell before its earnings report (due out November 23rd), and that will still persist until the next 10-K, is sorting out VMWare’s financials from Dell’s legacy financials. Q4 will be the first ‘clean’ quarter.

This wouldn’t be a big deal except Dell’s financials involve a lot of adjusting as is. Take the balance sheet, which should be much better in the near term given that VMWare paid Dell a $9.3B dividend as part of the spin-off. Per the pro forma July 30th numbers, Dell’s net debt (short-term debt + long-term debt – cash & cash equivalents – long-term investments) drops from $30B to $21.15B. But then there’s the Dell financing related debt, debt that is backed by receivables and broken out as not core debt. The company’s investor day pins that at $10.3B in debt. I can back out just the short-term and long-term financial receivables to get more or less the same number. That drops net core debt to $10.9B.

And then there’s Boomi, which Dell agreed to sell for $4B in a deal that was supposed to close by year end (per the original press release) or by October (per the latest 10Q). I haven’t seen a press release announcing the close of the sale, and Dell hasn’t bothered to break out anything related to it in their pro forma accounting, but if it’s not material to the overall results and adding $4B to the balance sheet, all the better. That would drop net core debt to ~$7B, though I suppose it’s at risk of being taxed.

All of which to say, $7B for a company that has earned $2.9B in GAAP net income in the last 12 months and over $6B in free cash flow is not a heavy debt load. Dell has been driving towards an investment grade rating, which would lower their interest costs. We should see interest savings already from the debt paydown. And lower interest costs and a strong balance sheet also lead to…

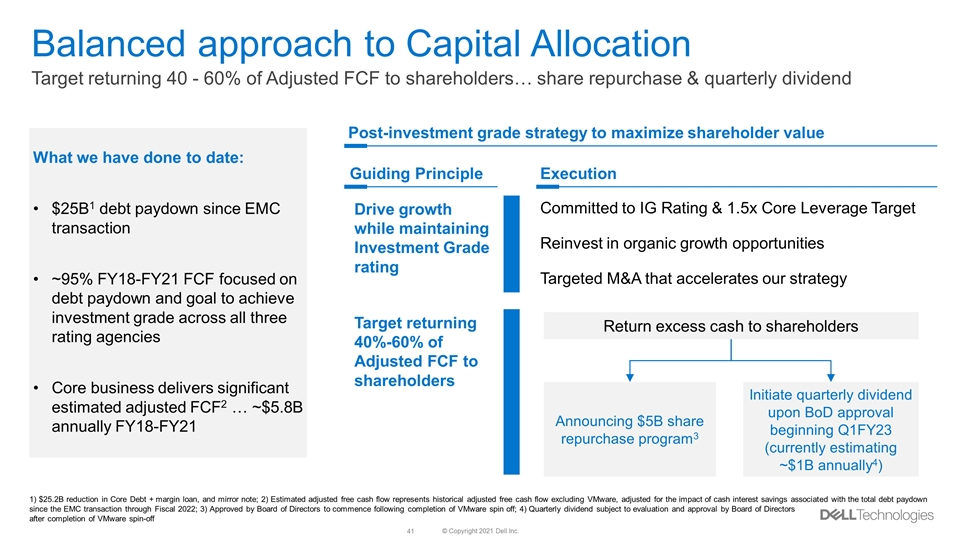

- Capital return

Dell set out two tenets in their Analyst Day pre-spinoff. They plan to issue a dividend that amounts to $1B/year in Q1 2023 (real world February-April 2022), and have already started a $5B buyback plan as of the spin-off. Longer-term, the company aims to return 40-60% of their adjusted free cash flow, while targeting 1.5x leverage and that investment grade rating.

Source: Dell's Analyst Day Presentation

The dividend, at the current share count of 810M, amounts to $1.23/share annually, or around 2.2% at the current ~$56/share range. The buyback is not trivial on a $45B market cap company, either the first slug or the ongoing buyback, which should be $2.5B-$3B a year.

We won't actually see that $7B net core debt number given these efforts, but it’s a sign of what a stronger company can afford.

- Operating leverage

Dell is targeting 6%+ EPS growth with 100%+ conversion to free cash flow, vs. a 3-4% overall revenue growth. As the company’s operations are newly focused, this seems like a reasonable target. The interest cost savings should flow pretty directly to the bottom line, and I would expect some room to improve operations/costs, especially as supply chain issues ease.

- Management

This may be the most controversial. Michael Dell, Dell’s Chairman and CEO, has earned credibility for his business instincts, and also a reputation as one who is always willing to discard shareholders’ interests. His taking Dell private in 2013 and his antics around the VMW tracking stock in 2018 each led to legendary battles with investor/shareholder activist Carl Icahn.

Since bringing Dell public again, though, he has been aligned with shareholders, and the performance has turned out well. Dell’s outperformance can be attributed to pandemic tailwinds in tech to some extent, but the VMWare spin-off played no small role as well. Dell remains a significant shareholder in his eponymous company (and the chairman of VMWare, a separate issue now). Dell is 56 and, with his wife, owns over 50% of overall shares in Dell. I don’t see why he won’t remain incentivized and eager to build on this recent success.

Risks

- Post-Pandemic hangover

I’ve already brought this up. While we can expect tech spending as a whole to grow secularly, the PCs rush of the last 18 months is unlikely to persist. Dell’s longer-term guidance suggests they understand the headwinds for CSG.

But, the market may not have priced it in. Dell’s guidance for Q3 was for high single-digits sequential revenue growth from CSG, defying typical seasonality. It may be that supply chain struggles are helping Dell smooth out the peak of their revenue growth, but at some point they’ll guide for a meaningful slowdown in CSG and the market may not be prepared for this.

- The accounting is funky

Dell reports an adjusted earnings number, with adjustments primarily due to amortizing intangibles (60% of adjustments in last year), share-based compensation (20%), and other issues like purchase accounting (20%). I’m not fond of adjusted earnings, but it’s what both Dell and the street focuses on, so that’s one grain of salt we have to consider, and it makes a big difference: $6.05/share in non-GAAP net income vs. $3.56/share in GAAP income.

All the math in this article is based on Dell’s provided pro forma numbers around VMWare, and there are a lot of puts and takes that will start to manifest in the next 10Q and especially the next 10K. This adds a degree of uncertainty to the analysis as these pro forma numbers translate into actual operating performance.

- Free Cash Flow Uncertainty

Which rolls into the free cash flow number. On Dell’s Investor Day presentation, their adjustments to free cash flow were few – they started with their filings' reported cash flow statements, took out VMW’s numbers, made a small adjustment around operating leases, and added in a benefit from lower interest savings. I wouldn’t have added in that last bit the way they did, but it’s fair to call that out.

Dell tends to benefit from working capital as a source of funding, which can be erratic from year to year. Between that fluctuation and the pandemic pull forwards vs. accelerations, it can be hard to tell where to begin a valuation of Dell. The company uses $7.4B adjusted free cash flow as the base, after the set of adjustments in the previous paragraph. I start with $6.5B, which is Dell’s free cash flow less VMW’s. Whether that is further inflated by current conditions remains to be seen for our valuation.

Valuation

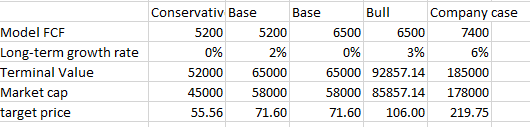

Given how slowly Dell is expected to grow and the various moving parts around its baseline, I don’t think it’s necessary to build out a full discounted cash flow model. Dell would like to point you to its 8x TTM earnings multiple, which is great but non-GAAP, so I’d rather not use that either.

Instead, I just want to capitalize the free cash flow number. If I use my $6.5B, and assume zero growth, a 10% discount rate gets me a terminal value of $71/share, above 27% upside before you factor in share count reduction or dividends (while using the $7B in core debt). If I use $5.2B, the company’s FY 2021 number, and zero growth, I get the current share price. You can work out the scenarios from there.

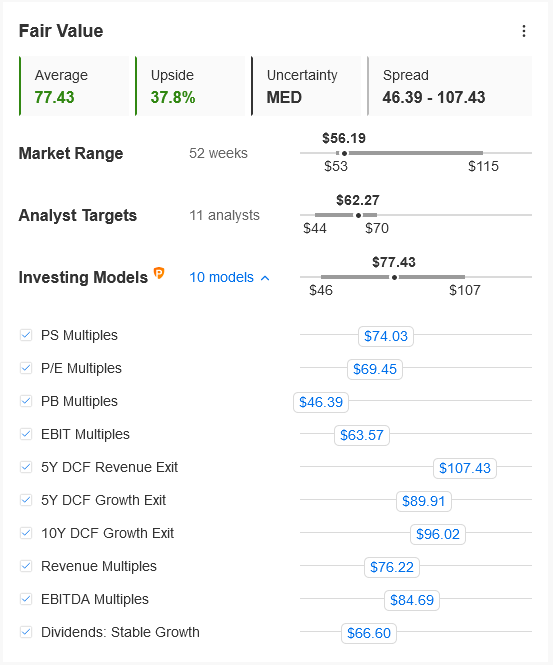

To sanity check, I also pulled up Dell’s fair value in Investing Pro. While analysts are a little more conservative, the quantitative models in Pro point to upside as well:

P/B multiples make sense since Dell does not have positive equity value. The 5Y DCF Growth Exit is closest to what I would build on my own, though every modeler will use slightly different inputs.

As a last check, if you draw out the company’s midpoint targeted revenue growth in each segment, and apply 11% operating margins to ISG and 7% to CSG, you get $8.2B in operating income. Use Dell’s $1.2B estimate of cash interest at current levels and we have $7B pre-tax income; apply a 25% tax rate to be conservative and we get to $5.25B in income. That’s $6.47/share GAAP income in 2025/FY 2026, with some conservatism built into the estimate on interest, tax rate, and share count.

Maybe that doesn’t get a huge multiple, but the current GAAP multiple is 15.7; apply that to $6.47 and you get $102/share.

Conclusion

Dell’s spin-off of VMWare closes a 5-year chapter of the company’s history that saw it return to public markets, annoy Carl Icahn and thousands of shareholders once more, and then deliver solid, if macro-fueled, results.

Having released its crown jewel to market independence, Dell is still a reasonably priced stock with promising prospects. Those prospects do not involve Day 1 growth and excitement, but instead a lot of free cash flow that should accrue to the equity and be paid out to shareholders. At the current price, I think Dell has an attractive risk/reward, and I’m looking forward to getting more Dell stock if it gets to the low $50s.