Street Calls of the Week

Introduction & Market Context

3D Systems Corporation (NYSE:DDD) presented its first quarter 2025 financial results on May 13, 2025, revealing continued challenges across its business segments. The additive manufacturing company reported declining revenue and margins while emphasizing bright spots in healthcare and defense markets. The presentation comes after a disappointing fourth quarter 2024 that saw the company miss earnings expectations, and premarket trading shows the stock down over 24% following these latest results.

Dr. Jeffrey Graves, President and CEO, cited global tariff uncertainty and frozen capital expenditure investments as key factors impacting the company’s performance, while highlighting that underlying demand for additive manufacturing remains strong in certain sectors.

Quarterly Performance Highlights

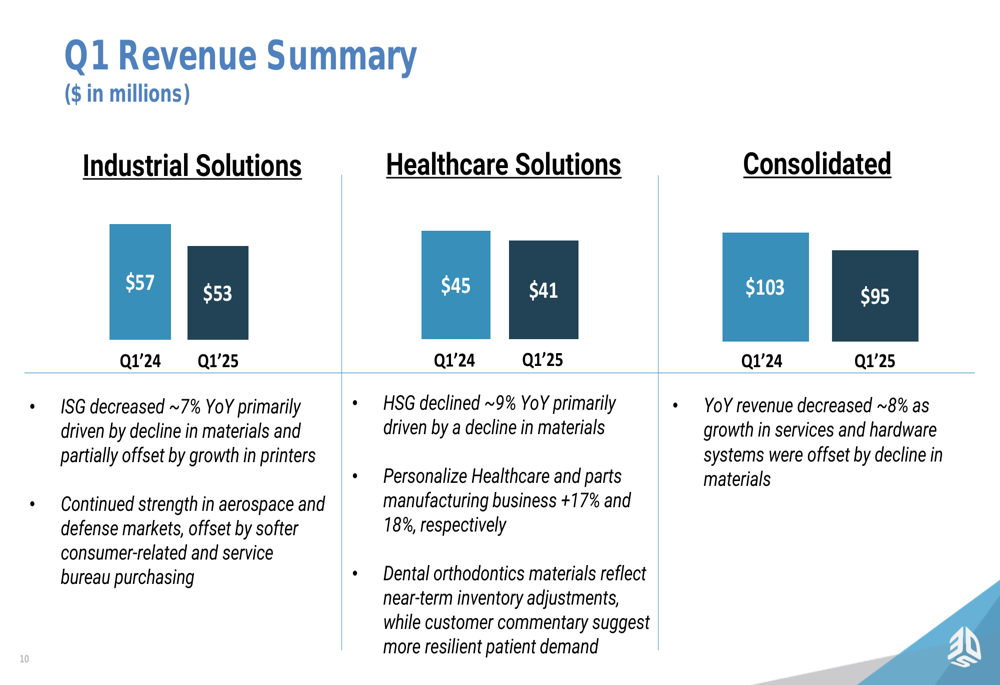

3D Systems reported Q1 2025 consolidated revenue of $95 million, representing an 8% decrease from $103 million in the same period last year. Both business segments experienced declines, with Industrial Solutions falling 7% year-over-year to $53 million and Healthcare Solutions dropping 9% to $41 million.

As shown in the following revenue summary chart:

The company attributed the revenue decline primarily to weakness in materials sales, partially offset by growth in printers and services. While overall performance was down, the company highlighted continued strength in aerospace and defense markets, as well as impressive growth in personalized healthcare (+17% YoY) and medical parts manufacturing (+18% YoY).

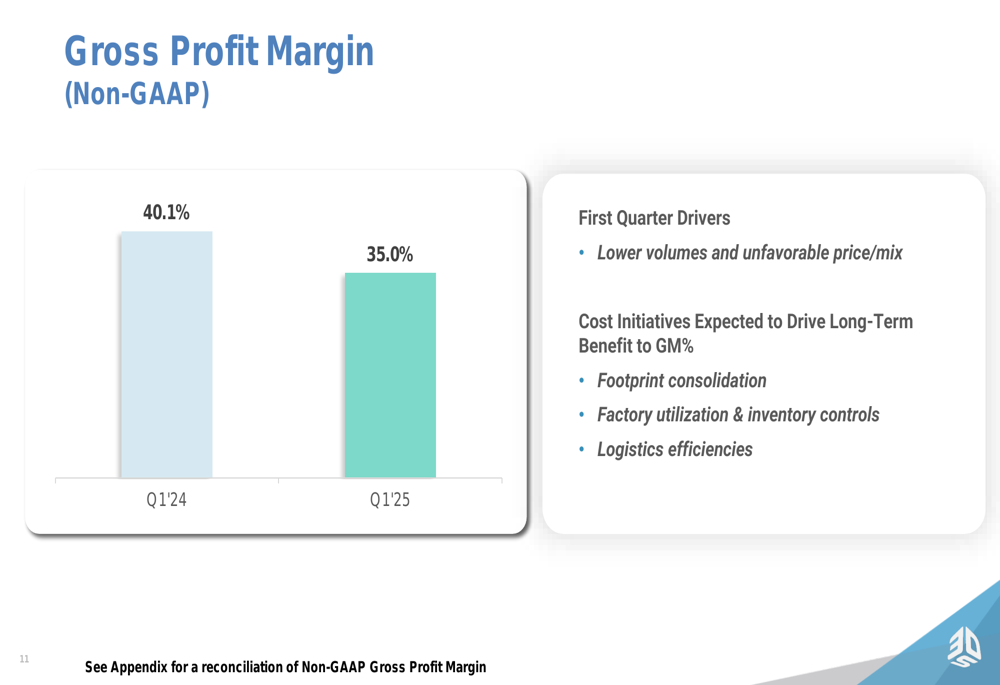

Gross profit margin (non-GAAP) deteriorated to 35.0% in Q1 2025 from 40.1% in Q1 2024, primarily due to lower volumes and unfavorable price/mix. The company expects its cost initiatives to drive long-term benefits to gross margins through footprint consolidation, improved factory utilization, inventory controls, and logistics efficiencies.

The following chart illustrates the margin pressure:

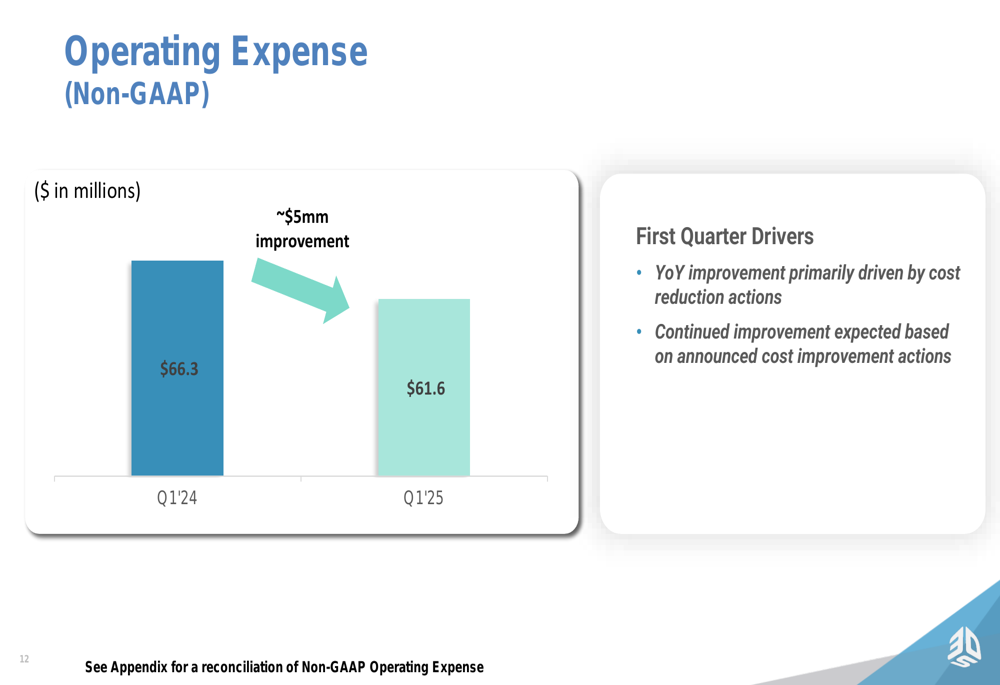

On a positive note, 3D Systems reduced its non-GAAP operating expenses by approximately $5 million year-over-year to $61.6 million, driven by cost reduction actions. Management indicated that further improvements are expected based on announced cost initiatives.

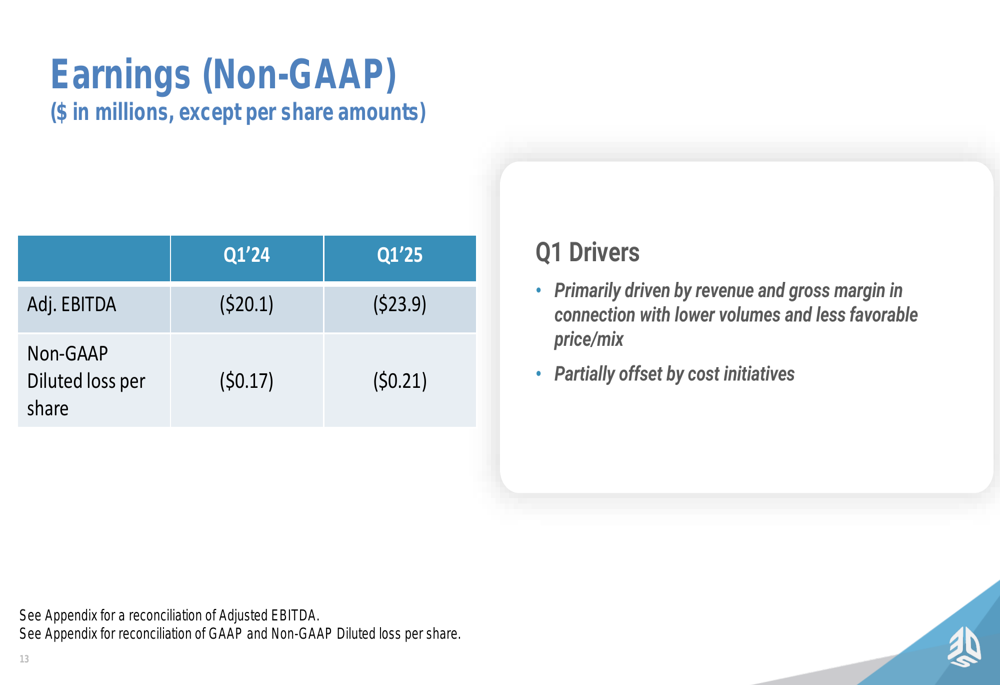

Despite the operating expense improvements, adjusted EBITDA worsened to -$23.9 million in Q1 2025 from -$20.1 million in Q1 2024, and non-GAAP diluted loss per share increased to -$0.21 from -$0.17 in the prior year period.

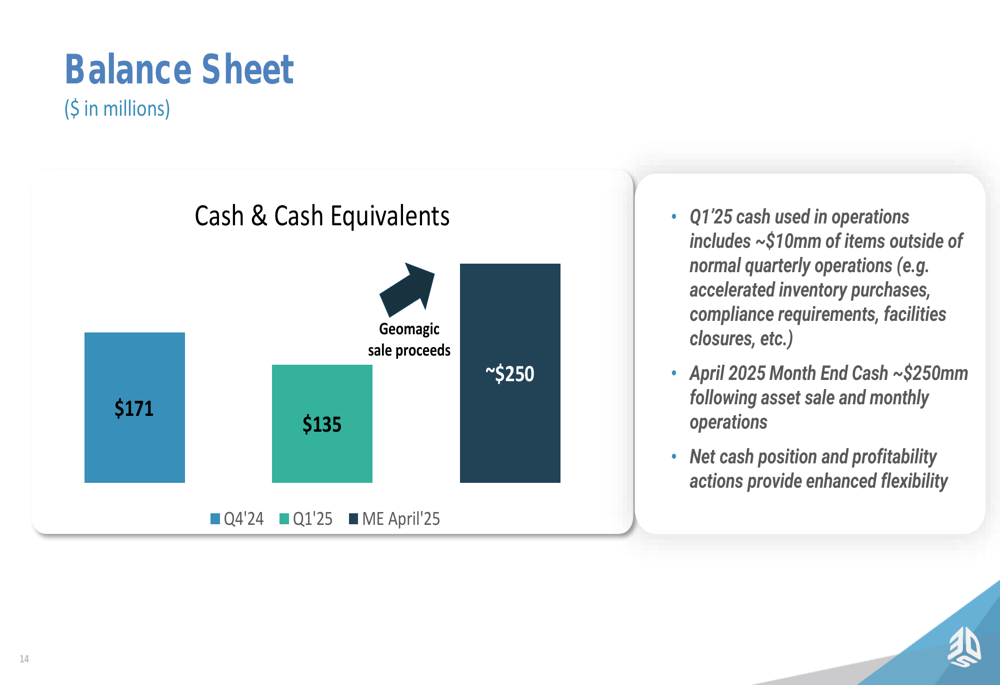

The company’s cash position stood at $135 million at the end of Q1 2025, down from $171 million at the end of Q4 2024. However, following the completion of the Geomagic sale, cash increased to approximately $250 million by the end of April 2025, providing enhanced financial flexibility.

Strategic Initiatives

Despite near-term challenges, 3D Systems emphasized several strategic initiatives aimed at positioning the company for future growth. The presentation highlighted that "short-term revenue pressure masks long-term opportunity" and outlined the revolutionary benefits of additive manufacturing in terms of performance, cost, and supply chain resilience.

The company is focusing on strategic investments in technology refresh of polymer and metal platforms, supported by in-sourced manufacturing. Management also detailed a cost optimization plan targeting approximately $70 million in reductions by proactively aligning operations to current market realities.

As illustrated in the strategic investment highlights:

In the metals segment, 3D Systems is driving growth through innovation and execution, with the Application Innovation Group (AIG (NYSE:AIG)) fueling metal platform success. The company specifically highlighted the DMP Flex (NASDAQ:FLEX) 350 Triple as delivering "exceptionally strong, high-quality, high-purity parts."

The healthcare segment remains a bright spot, with strong growth in personalized healthcare and medical parts manufacturing. The company emphasized deep industry partnerships driving innovation and noted that its solutions have revolutionized personalized healthcare for nearly 250,000 patients worldwide, with over 2 million medical devices manufactured and more than 100 FDA-cleared and CE-marked devices supported.

Forward-Looking Statements

In a significant development, 3D Systems announced it is withdrawing its 2025 guidance due to tariff-related uncertainty. CEO Jeffrey Graves indicated the company is taking a "prudent and conservative approach to planning" given the current market environment.

The company is executing a dual-track cost reduction strategy targeting approximately $70 million in savings, though specific details on the timeline and components of these savings were not fully elaborated. Management emphasized that the company’s strong financial position following the Geomagic sale provides flexibility to navigate the challenging environment.

Market Reaction

The market response to 3D Systems’ Q1 2025 results has been decidedly negative. According to available premarket data, the stock was down 24.34% to $1.93, approaching its 52-week low of $1.71. This follows a 17.83% drop after the company’s Q4 2024 earnings release, reflecting continued investor concerns about the company’s financial performance and uncertain outlook.

The withdrawal of 2025 guidance, combined with declining revenue and margins, appears to have further eroded investor confidence despite management’s emphasis on long-term opportunities and strategic initiatives. The company’s ability to execute its cost reduction strategy while maintaining growth in strategic segments will likely be crucial for any potential recovery in investor sentiment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.