Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

3D Systems Corporation (NYSE:DDD) presented its second quarter 2025 financial results on August 12, 2025, showing signs of stabilization after a challenging first quarter. The company’s stock opened at $1.80 in premarket trading, up 2.27% from the previous close of $1.76, as investors responded to improved profitability metrics and strategic progress despite ongoing revenue challenges.

The presentation, led by CEO Dr. Jeffrey Graves and CFO Jeffrey Creech, highlighted the company’s efforts to strengthen its balance sheet and focus on high-growth segments while implementing significant cost reduction initiatives. This comes after a difficult Q1 2025 when the company missed earnings expectations and saw its stock plummet nearly 30%.

Quarterly Performance Highlights

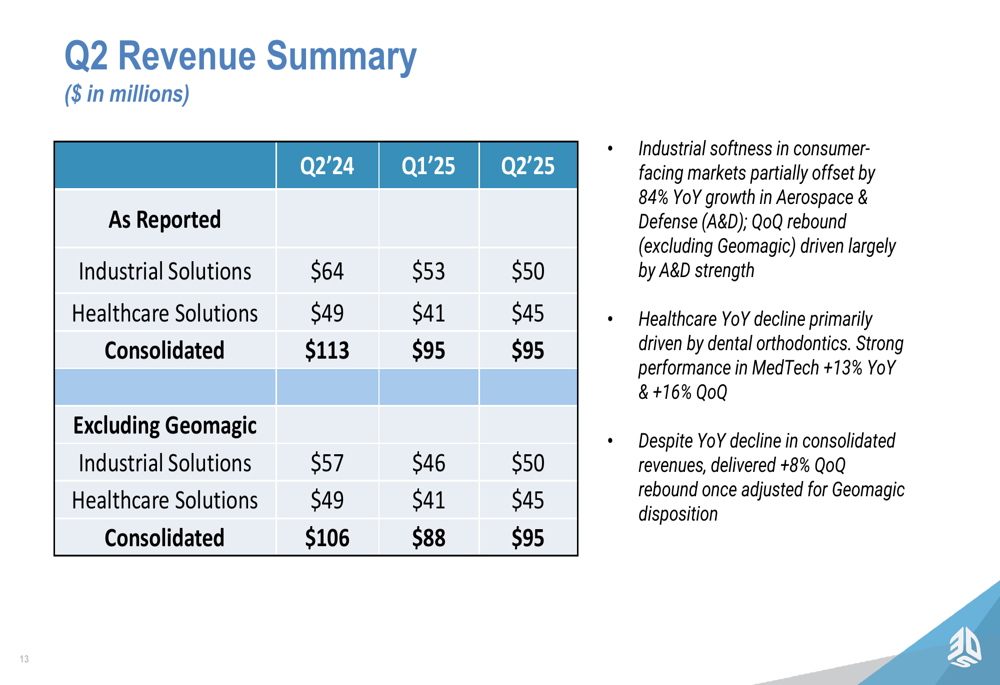

3D Systems reported Q2 2025 revenue of $95 million, unchanged from Q1 2025 but down from $113 million in Q2 2024. However, when adjusting for the April 2025 divestiture of the non-core Geomagic software platform, the company achieved 8% sequential growth.

As shown in the following revenue breakdown:

The company’s Healthcare Solutions segment generated $45 million in revenue, down from $49 million in Q2 2024 but up from $41 million in Q1 2025. Industrial Solutions contributed $50 million, compared to $64 million in Q2 2024 and $53 million in Q1 2025.

Notably, Medical (TASE:BLWV) Technologies grew 13% year-over-year and 16% quarter-over-quarter, while Aerospace & Defense achieved impressive 84% year-over-year growth. These strategic markets partially offset weakness in consumer-facing industrial applications and dental orthodontics.

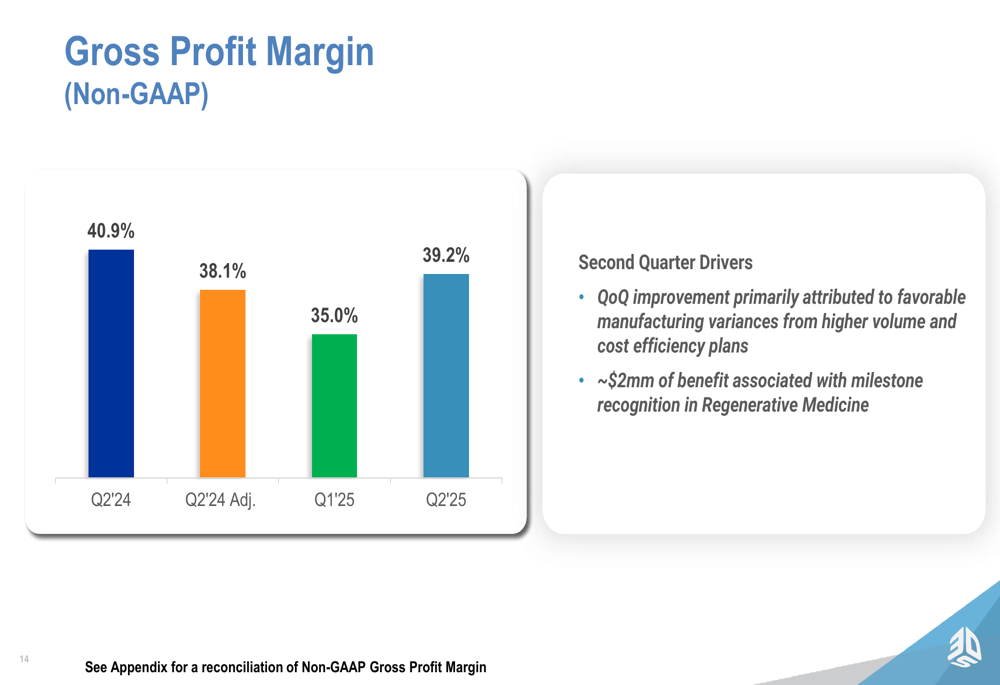

The company’s gross profit margin (non-GAAP) showed sequential improvement to 39.2% in Q2 2025 from 35.0% in Q1 2025, though still below the 40.9% achieved in Q2 2024:

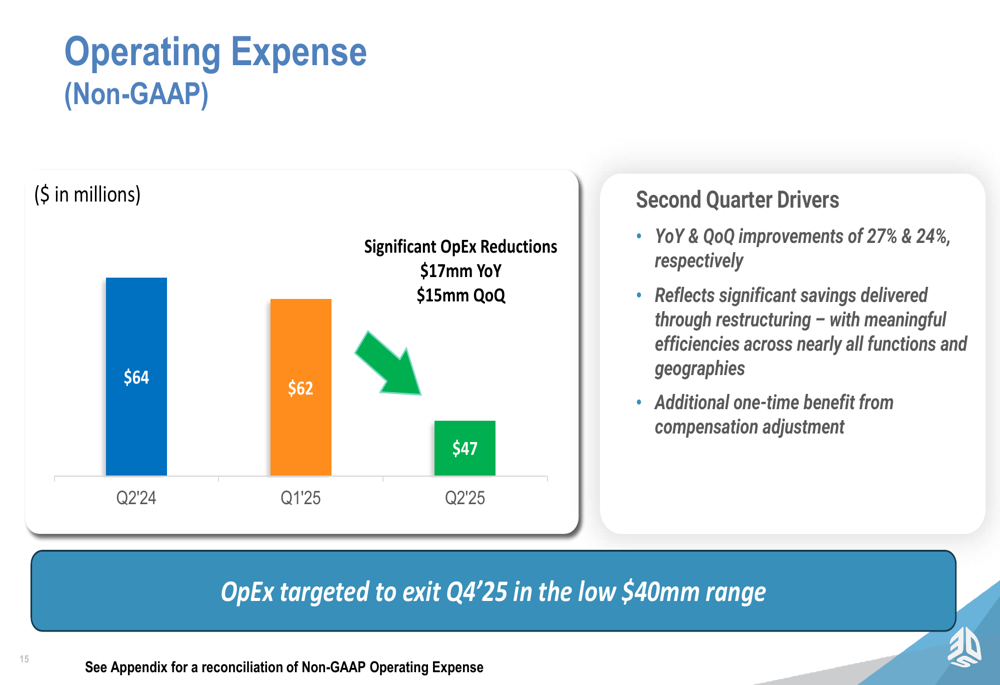

The most significant improvement came in operating expenses, which decreased to $47 million (non-GAAP) in Q2 2025, representing substantial reductions of 27% year-over-year and 24% quarter-over-quarter:

Strategic Initiatives

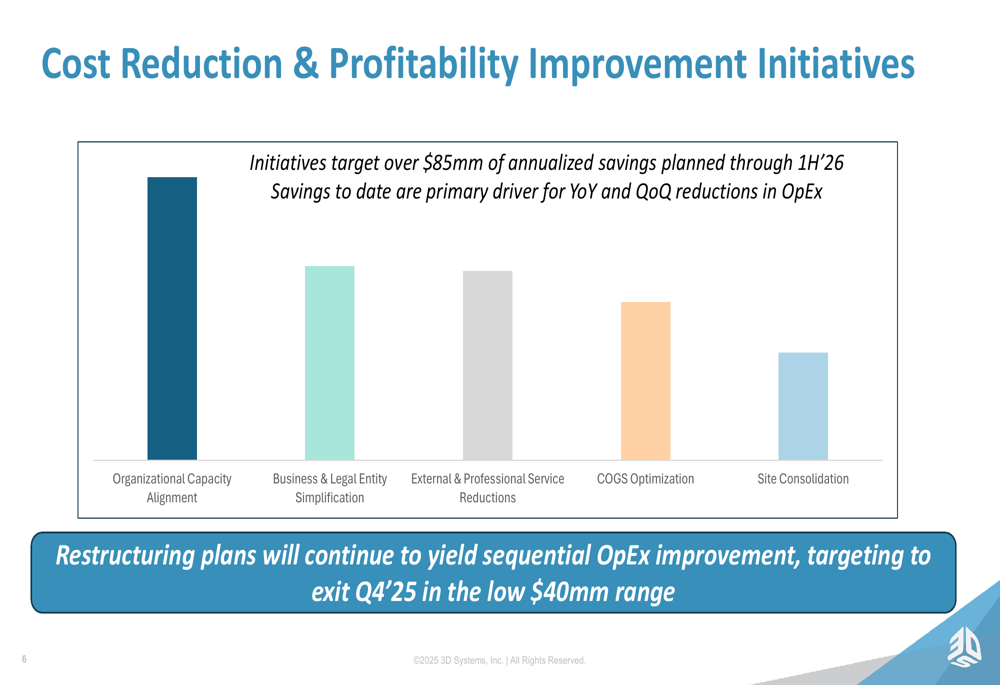

3D Systems outlined its strategic focus on execution and cost control while maintaining investments in high-growth markets. The company is implementing cost reduction initiatives targeting over $85 million in annualized savings through the first half of 2026:

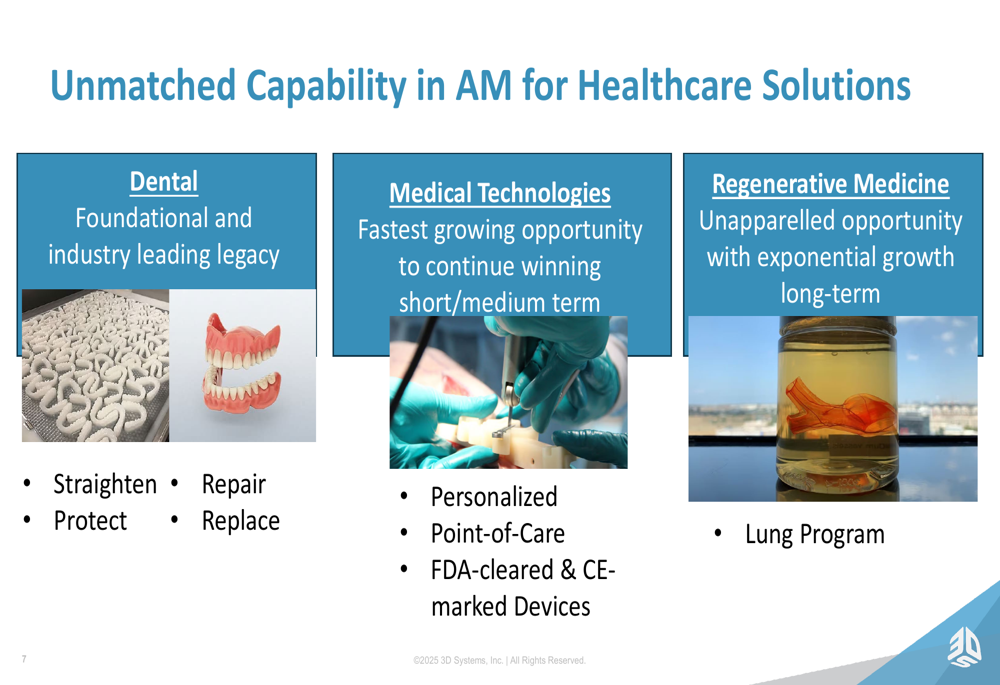

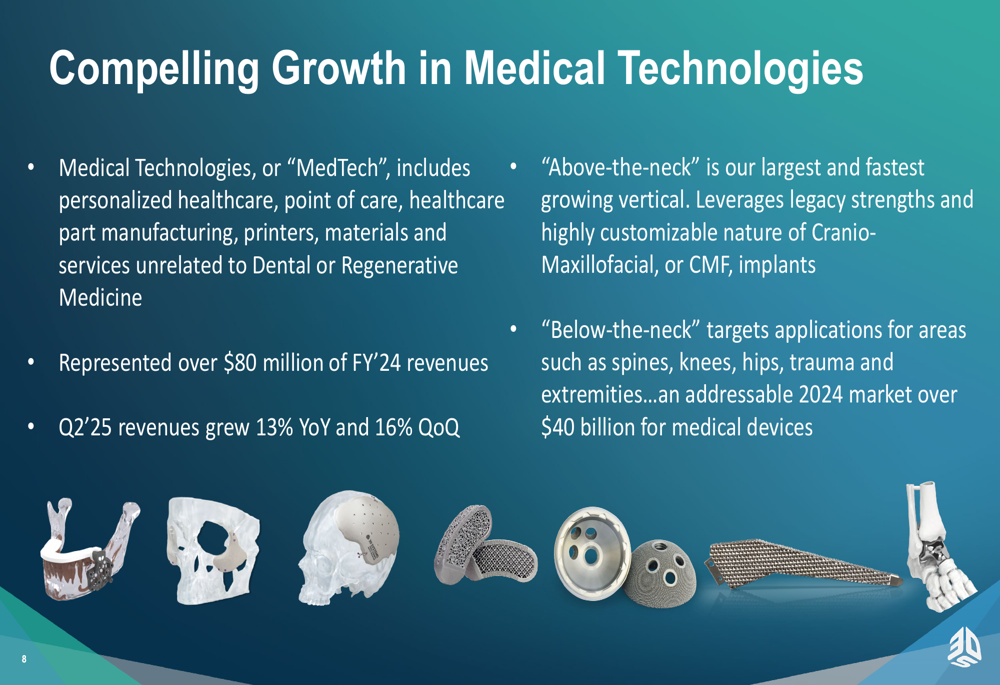

In healthcare, 3D Systems is pursuing opportunities across three segments: Dental, Medical Technologies, and Regenerative Medicine. The company highlighted Medical Technologies as its fastest-growing opportunity:

This segment, which represented over $80 million of FY 2024 revenues, is showing compelling growth particularly in "above-the-neck" applications:

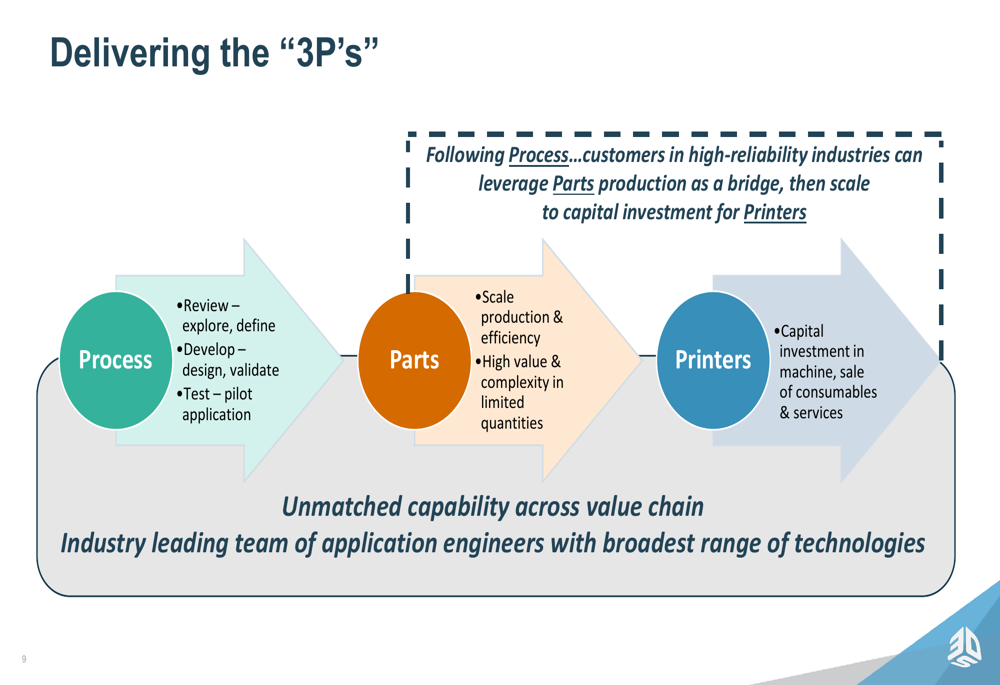

The company also emphasized its strategic approach to industrial markets through what it calls the "3P’s" - Process, Parts, and Printers:

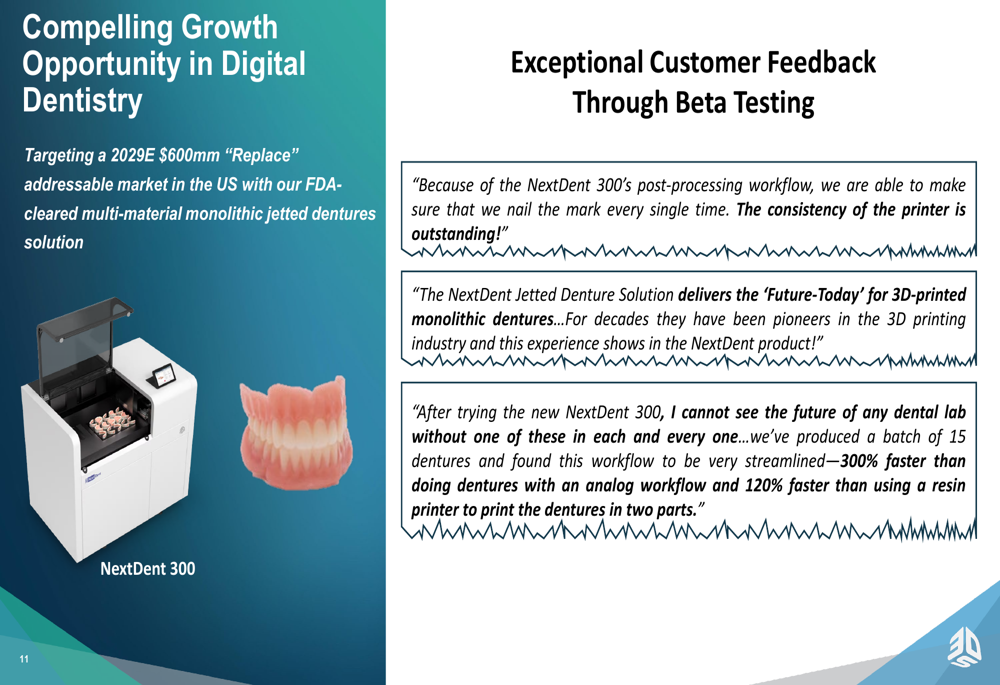

In the dental market, 3D Systems highlighted growth opportunities with its NextDent 300 printer targeting a $600 million addressable market:

Detailed Financial Analysis

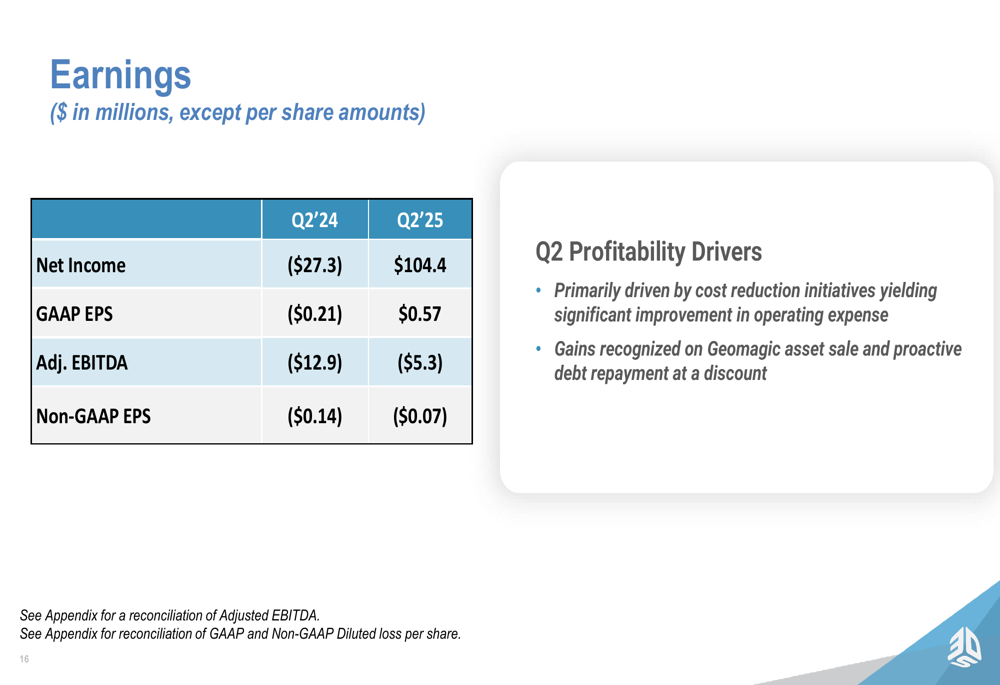

3D Systems reported a dramatic improvement in net income, reaching $104.4 million in Q2 2025 compared to a loss of $27.3 million in Q2 2024. This translated to GAAP earnings per share of $0.57, versus a loss of $0.21 per share in the year-ago quarter:

However, these results were primarily driven by one-time gains from the Geomagic asset sale and debt restructuring rather than operational improvements. Adjusted EBITDA remained negative at $5.3 million, though this represented an improvement from the $12.9 million loss in Q2 2024.

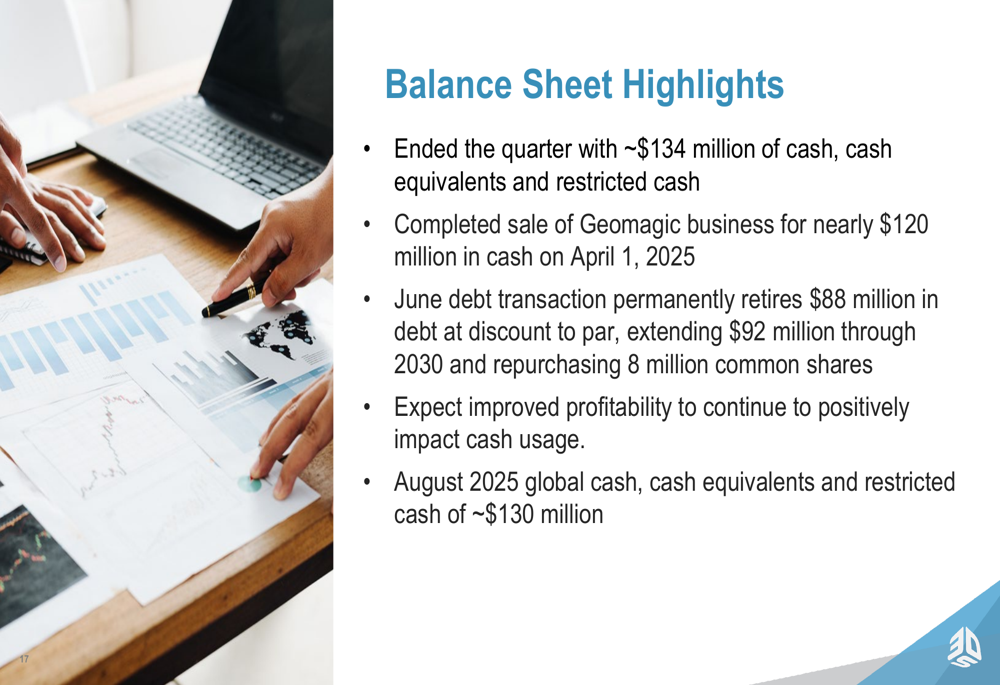

The company significantly strengthened its balance sheet during the quarter:

The April 2025 sale of the Geomagic business for nearly $120 million provided substantial cash proceeds. Additionally, 3D Systems completed a debt transaction in June that permanently retired $88 million in debt at a discount to par, extended $92 million through 2030, and repurchased 8 million common shares. The company ended Q2 with approximately $134 million in cash and cash equivalents.

Forward-Looking Statements

Looking ahead, 3D Systems expects continued sequential improvement in operating expenses, targeting an exit rate in the "low $40 million range" by Q4 2025. Management emphasized controlling costs while maintaining investments in strategic growth areas.

This cautious approach follows the company’s decision to withdraw full-year 2025 guidance after Q1 results due to economic uncertainty. The Q2 presentation suggests a strategy focused on achieving profitability at current revenue levels through aggressive cost management, while positioning for growth in Medical Technologies, Aerospace & Defense, and AI infrastructure markets.

The company faces ongoing challenges in consumer-facing markets and dental orthodontics but appears to be making progress on its restructuring plans. Investors will be watching closely to see if the operational improvements and strategic focus can translate into sustainable profitability in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.