Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

Anheuser-Busch InBev (BRU:EBR:ABI) shares rose 3.02% on Thursday after the world’s largest brewer reported solid first-quarter results that showed significant margin expansion and earnings growth despite volume challenges in key markets. The company’s Q1 2025 presentation, delivered on May 8, highlighted how its geographic diversification, premiumization strategy, and digital initiatives are driving growth despite headwinds in certain regions.

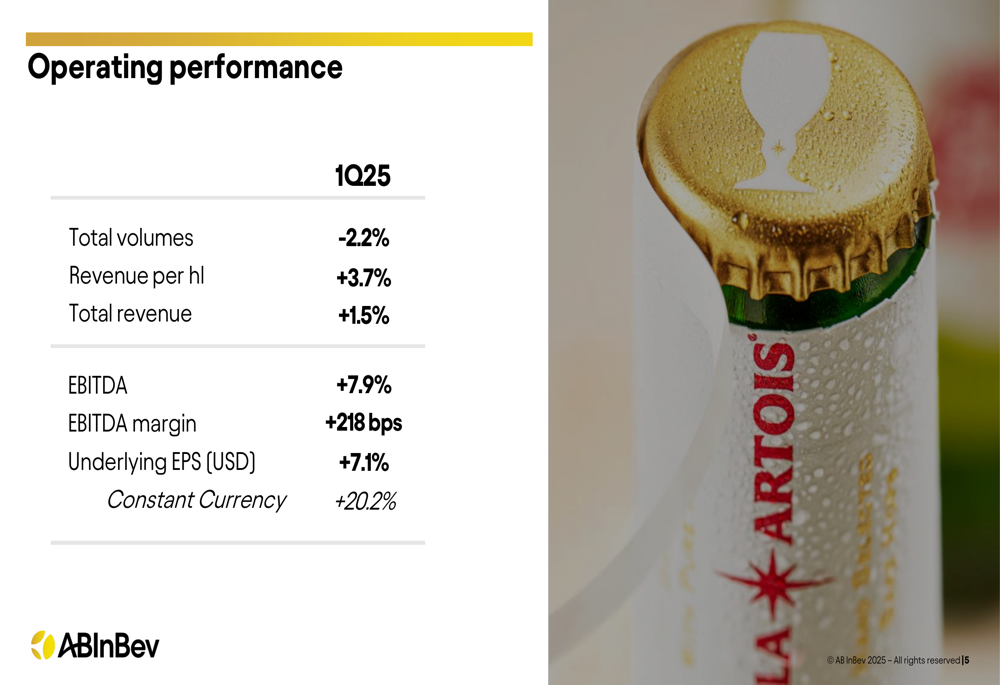

The brewing giant reported EBITDA growth of 7.9%, reaching the upper end of its full-year outlook range, while EBITDA margins expanded by 218 basis points to 35.6%. This performance came despite a 2.2% decline in total volumes, demonstrating the company’s ability to drive revenue per hectoliter growth and operational efficiencies.

Quarterly Performance Highlights

AB InBev’s first quarter showed solid financial performance with total revenue growing 1.5%, driven by a 3.7% increase in revenue per hectoliter that more than offset the volume decline. Underlying earnings per share grew 7.1% to $0.81, or 20.2% on a constant currency basis.

The company’s detailed operating performance revealed strong margin expansion across most regions, with particularly impressive results in Middle Americas and South America.

As shown in the following chart of detailed operating performance:

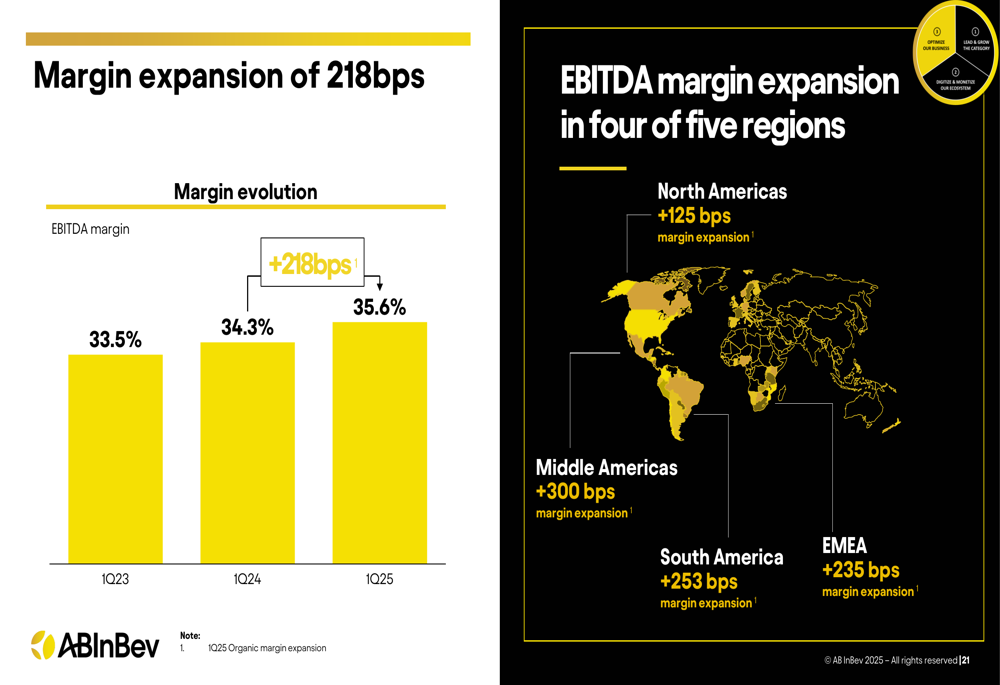

The company’s EBITDA margin expansion was particularly noteworthy, reaching 35.6% in Q1 2025, up from 34.3% in Q1 2024 and 33.5% in Q1 2023. This expansion was driven by premiumization, operational efficiencies, and strong performance in high-margin markets.

The following visualization shows EBITDA margin evolution and regional expansion:

Regional Performance Analysis

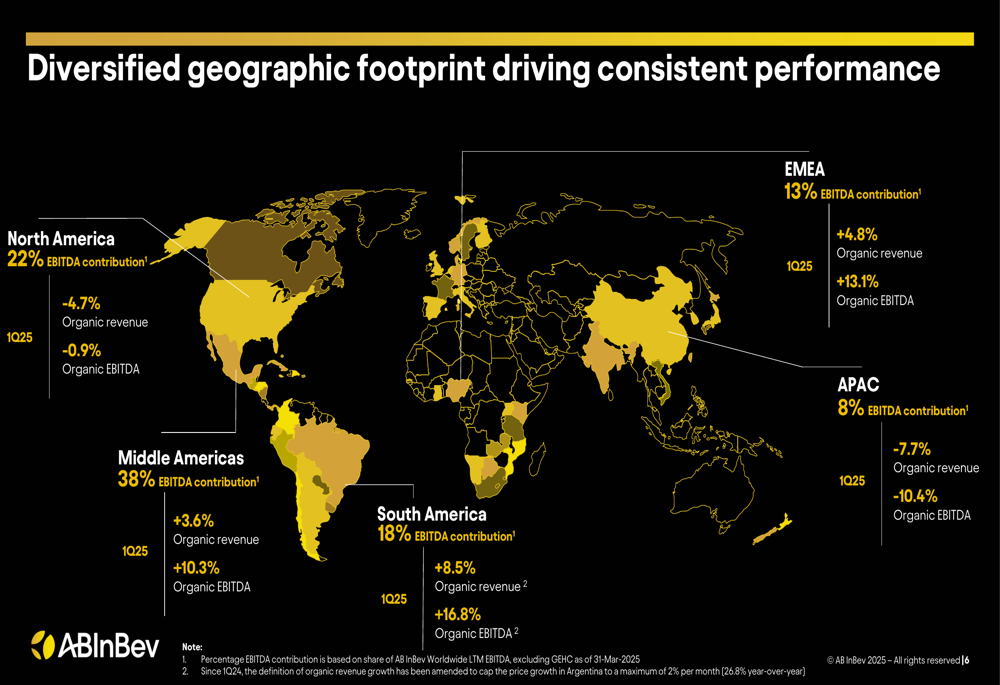

AB InBev’s geographic diversification proved valuable in Q1, with strong performance in Middle Americas and South America offsetting challenges in North America and Asia Pacific. The company’s global footprint shows varying performance across regions:

Middle Americas, which contributes 38% of the company’s EBITDA, delivered 3.6% organic revenue growth and impressive 10.3% organic EBITDA growth. Mexico saw revenue growth and margin expansion driving double-digit bottom-line growth, while Colombia achieved record high volumes.

The detailed performance of the Middle Americas region is illustrated here:

South America was another bright spot, with 8.5% organic revenue growth and 16.8% organic EBITDA growth. Brazil continued its momentum with all-time high beer and non-beer volumes, while Argentina showed sequential improvement despite ongoing inflationary pressures.

North America, representing 22% of EBITDA, faced challenges with a 4.7% decline in organic revenue, though EBITDA declined by just 0.9%. The company attributed the U.S. industry volume decline to adverse weather and calendar-related factors, with expected improvement in April.

Asia Pacific was the most challenging region, with organic revenue declining 7.7% and EBITDA down 10.4%. Performance in China was impacted by industry weakness in key regions and the on-premise channel, though South Korea showed growth with volumes up by low-teens.

Brand Strategy and Growth Drivers

AB InBev’s brand strategy centers around its megabrands, which grew 4.4% in Q1 2025 net revenue. The company’s premiumization efforts continue to show results, with Corona leading the way with 11.2% net revenue growth.

The following slide illustrates the performance of the company’s megabrands:

Corona, which is celebrating its 100th anniversary, was ranked as the #1 most valuable beer brand globally by Brand Finance for 2024 and 2025. The brand maintains a significant price premium and is present in over 30 markets with double-digit volume growth.

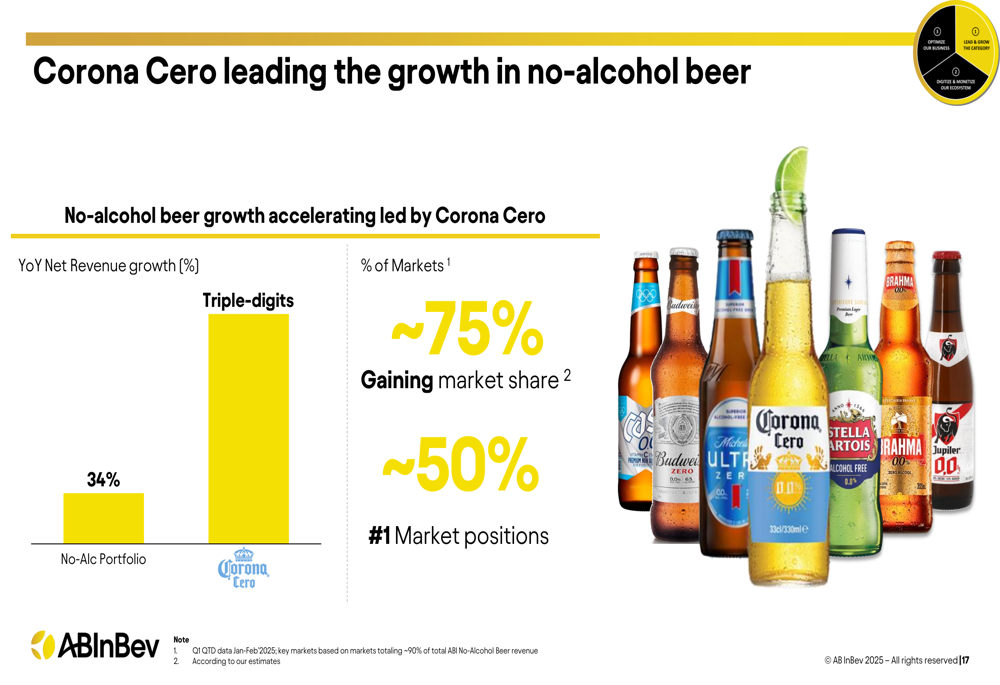

The company is also seeing strong results from its category expansion strategy, with no-alcohol beer revenue growing by 34%, led by Corona Cero, which is achieving triple-digit year-over-year net revenue growth. The beyond beer portfolio, which includes brands like Cutwater and NUTRLL, grew by 16.6%.

Corona Cero’s performance is highlighted in the following slide:

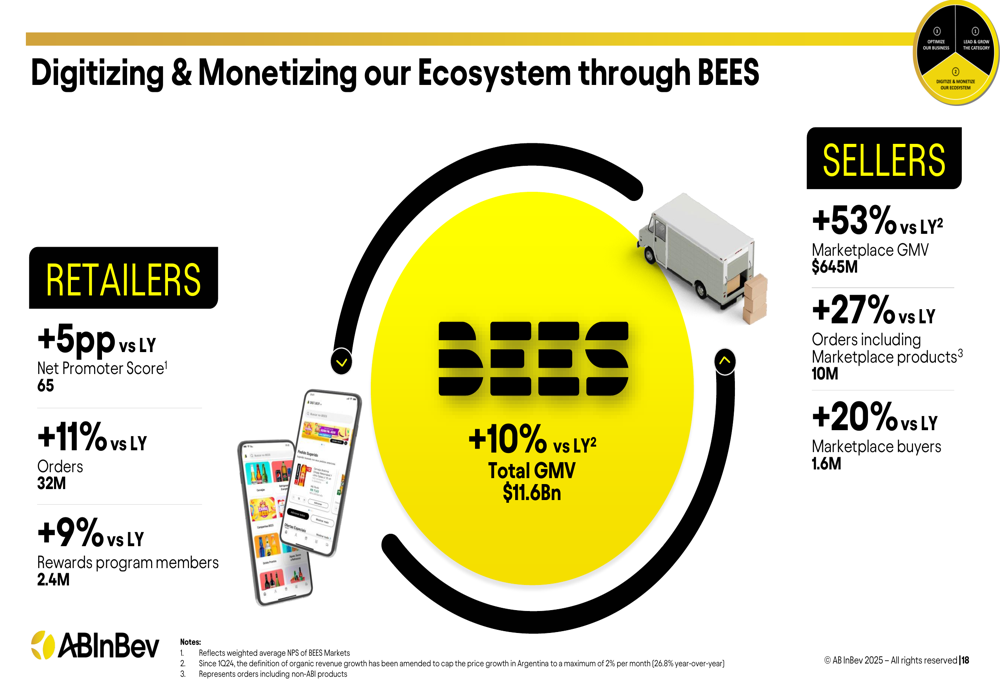

Digital Transformation Progress

AB InBev continues to make significant progress in its digital transformation, with its BEES platform showing impressive growth. The B2B platform achieved $11.6 billion in total GMV, up 10% year-over-year, while BEES Marketplace GMV grew by 53% to $645 million.

The following slide details the performance of the BEES ecosystem:

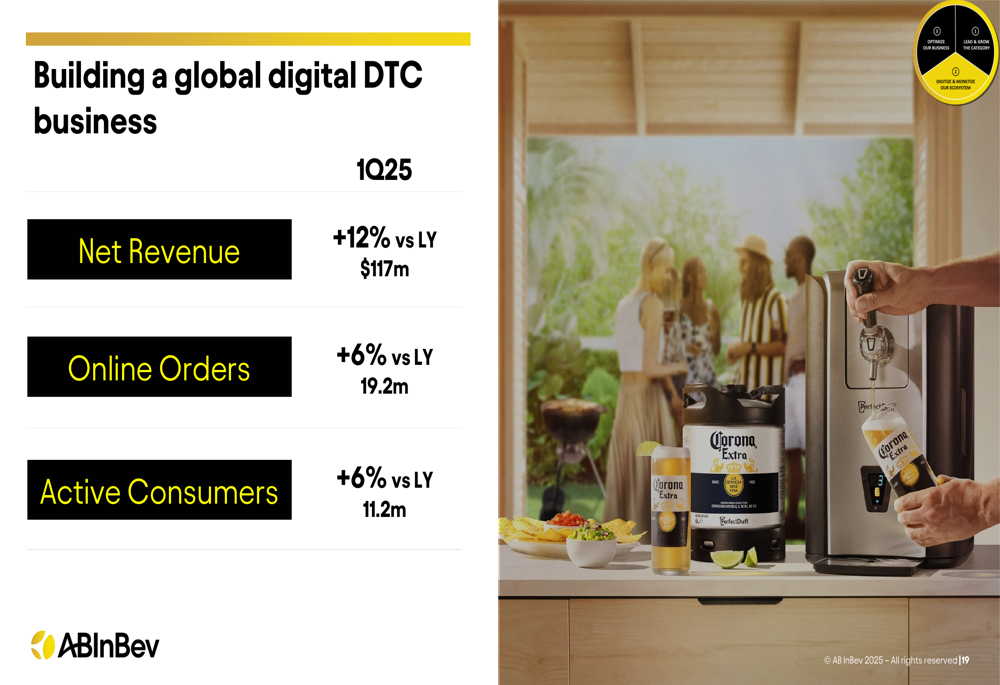

The company’s direct-to-consumer digital business also showed strong growth, with net revenue up 12% to $117 million in Q1 2025, online orders increasing by 6% to 19.2 million, and active consumers growing by 6% to 11.2 million.

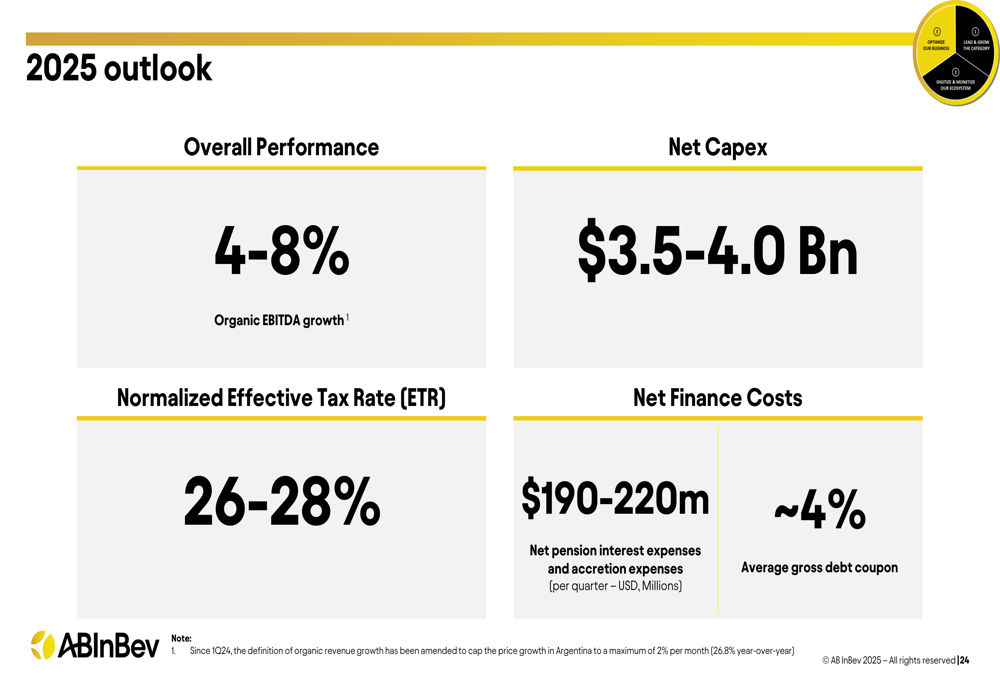

2025 Outlook and Forward-Looking Statements

Looking ahead, AB InBev maintained its full-year 2025 outlook, projecting 4-8% organic EBITDA growth. The company expects net capital expenditure of $3.5-4.0 billion and a normalized effective tax rate of 26-28%. Net finance costs are projected at $190-220 million per quarter.

The company expressed confidence in its ability to deliver on this outlook, citing the resilience of the beer category and opportunities to activate the category with its megabrands and digital platforms. AB InBev also highlighted its strong local presence, with 98% local production globally and 99% in the U.S.

The company summarized its position with the following key points:

AB InBev’s Q1 2025 results demonstrate the company’s ability to drive earnings growth and margin expansion despite volume challenges in certain markets. The geographic diversification, premiumization strategy, and digital initiatives are proving effective in delivering consistent financial performance, positioning the company well for continued growth in 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.