Street Calls of the Week

Introduction & Market Context

Abercrombie & Fitch Co. (NYSE:ANF) delivered record first-quarter sales for 2025, according to its investor presentation released on May 28, 2025. The company reported 8% year-over-year growth in net sales to $1.1 billion, exceeding management’s expectations. This performance comes amid a continued transformation of the retailer, which has seen substantial growth and margin expansion over the past three years.

The stock has responded positively to the results, with shares up 5.44% in the most recent session and showing a dramatic 23.95% jump in premarket trading. This investor enthusiasm reflects the company’s ability to maintain growth momentum despite challenging retail conditions.

Quarterly Performance Highlights

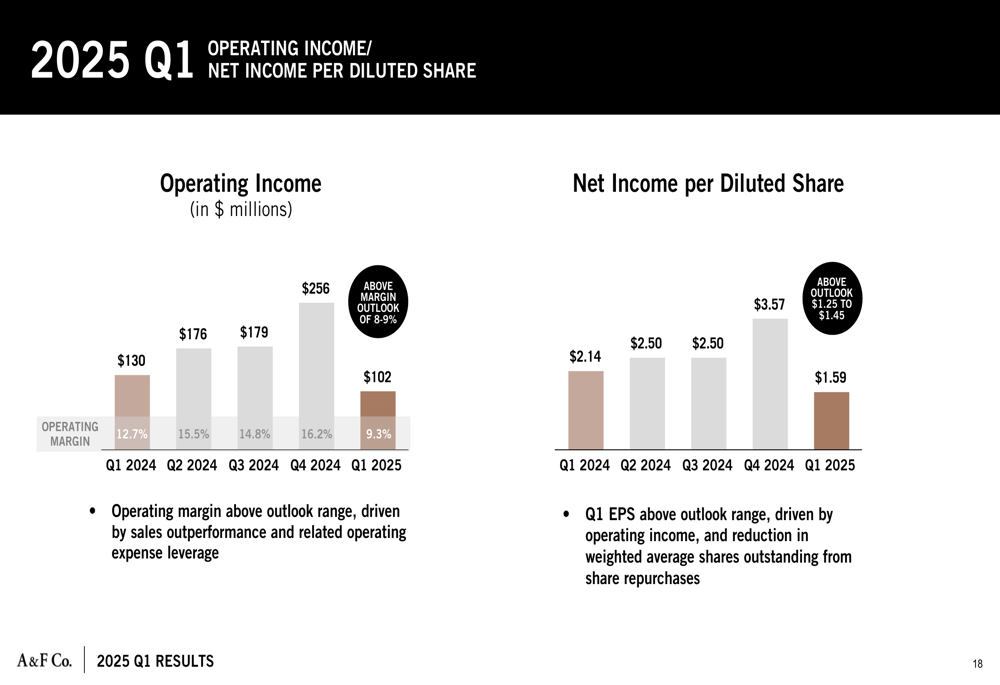

Abercrombie & Fitch reported Q1 2025 net sales of $1.1 billion, representing an 8% increase year-over-year. The company’s operating margin reached 9.3%, exceeding the outlook range of 8-9%, while net income per diluted share came in at $1.59, also above the projected range of $1.25-$1.45.

CEO Fran Horowitz highlighted the company’s performance in the presentation: "We delivered record first quarter net sales with 8% growth to last year. This was above our expectations and was supported by broad-based growth across our three regions."

As shown in the following chart of quarterly operating income and net income per diluted share, the company has maintained strong profitability, though at lower levels than the previous quarter due to seasonal factors:

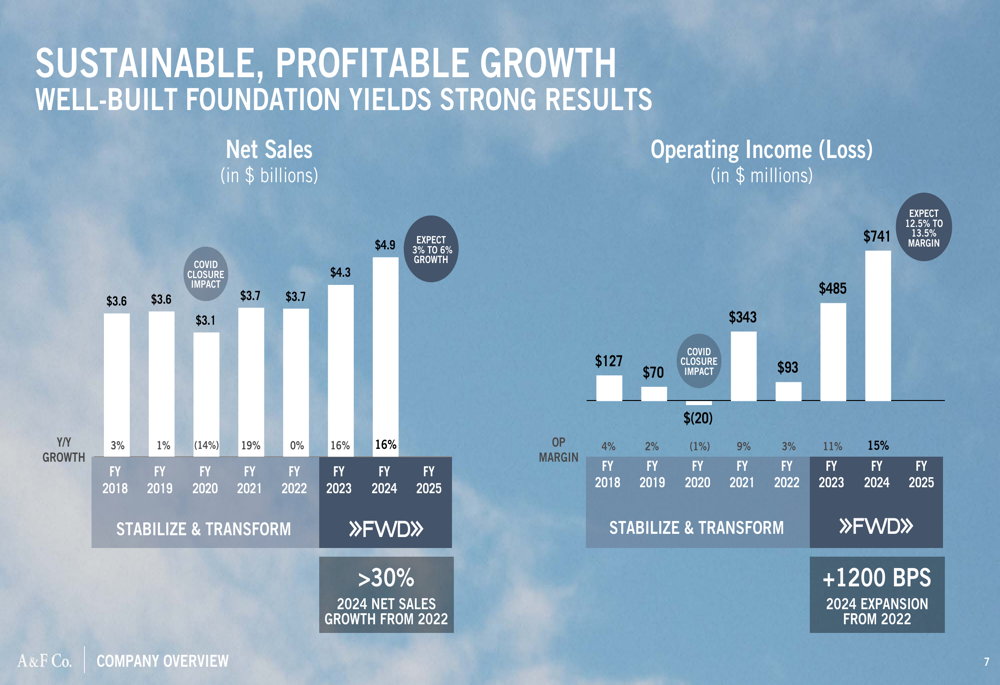

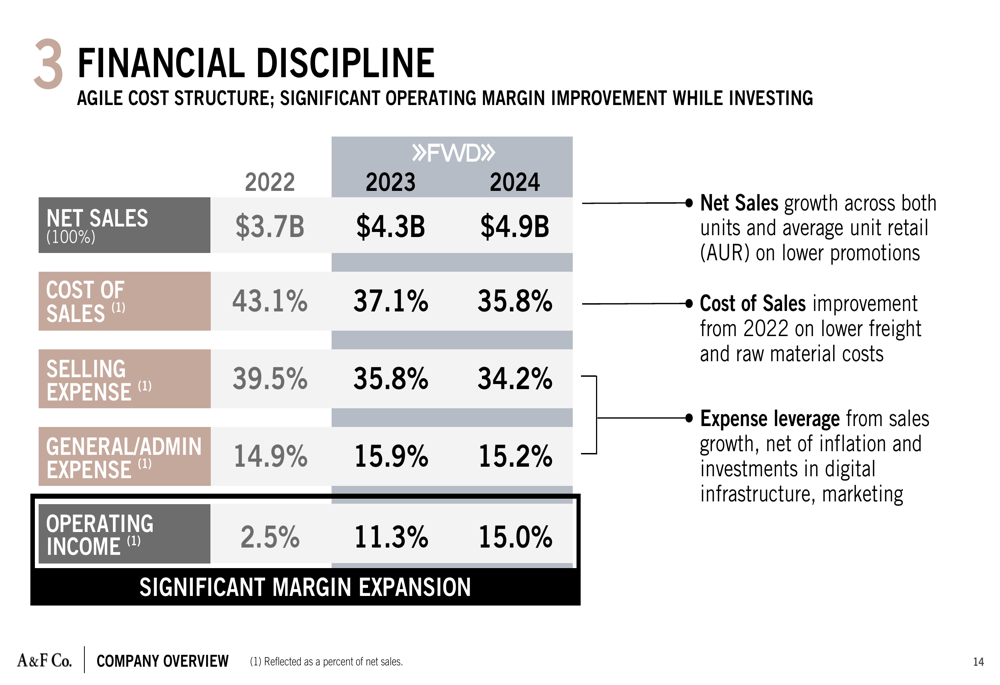

The company’s performance continues a multi-year growth trajectory, with net sales increasing from $3.7 billion in FY 2022 to $4.9 billion in FY 2024, representing a compound annual growth rate of over 15%. Operating margins have expanded dramatically during this period, from 2.5% in FY 2022 to 15.0% in FY 2024.

This financial progression is clearly illustrated in the company’s sustainable growth chart:

Brand Performance Analysis

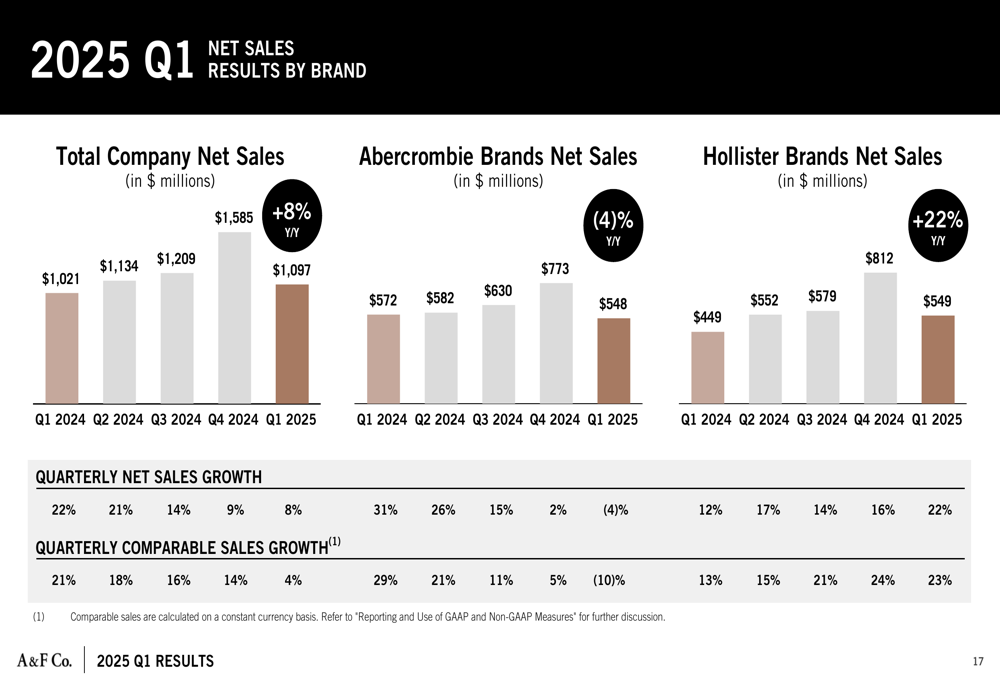

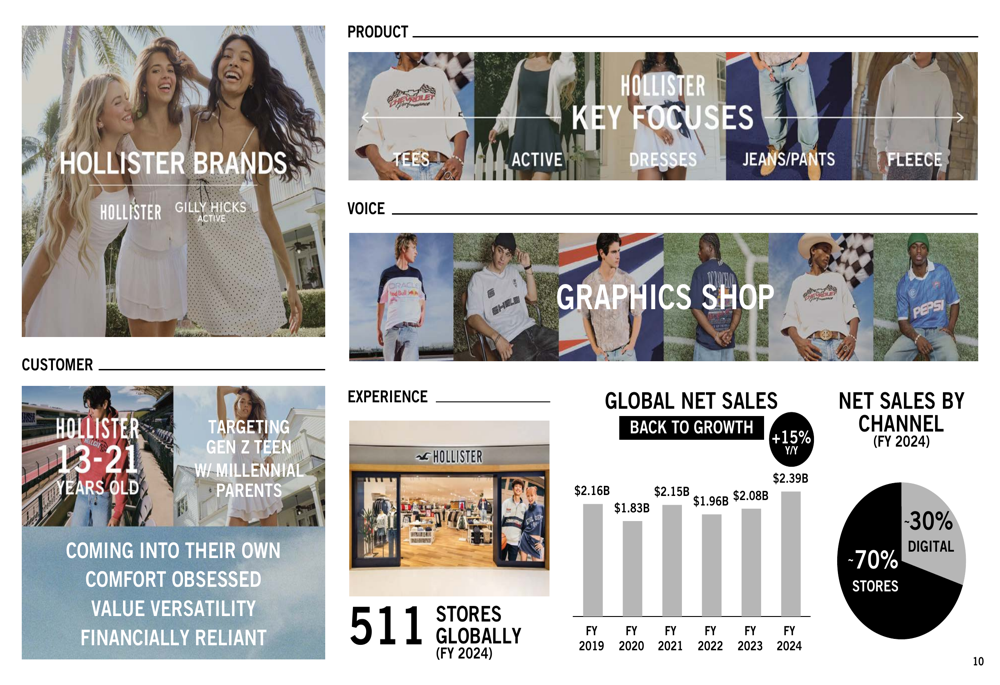

A notable aspect of the Q1 results was the divergent performance between the company’s two brand families. Hollister brands, which include Hollister and Gilly Hicks, delivered exceptional growth of 22% year-over-year. In contrast, Abercrombie brands, comprising Abercrombie & Fitch and abercrombie kids, experienced a 4% decline compared to the same period last year.

The following chart details the net sales performance by brand over recent quarters:

This divergence highlights the different market dynamics affecting each brand. Hollister, which targets Gen Z consumers aged 13-21, has maintained strong momentum with comparable sales growth of 23% in Q1 2025. Meanwhile, Abercrombie, which focuses on millennials aged 23-40+, saw comparable sales decline by 10% after several quarters of growth.

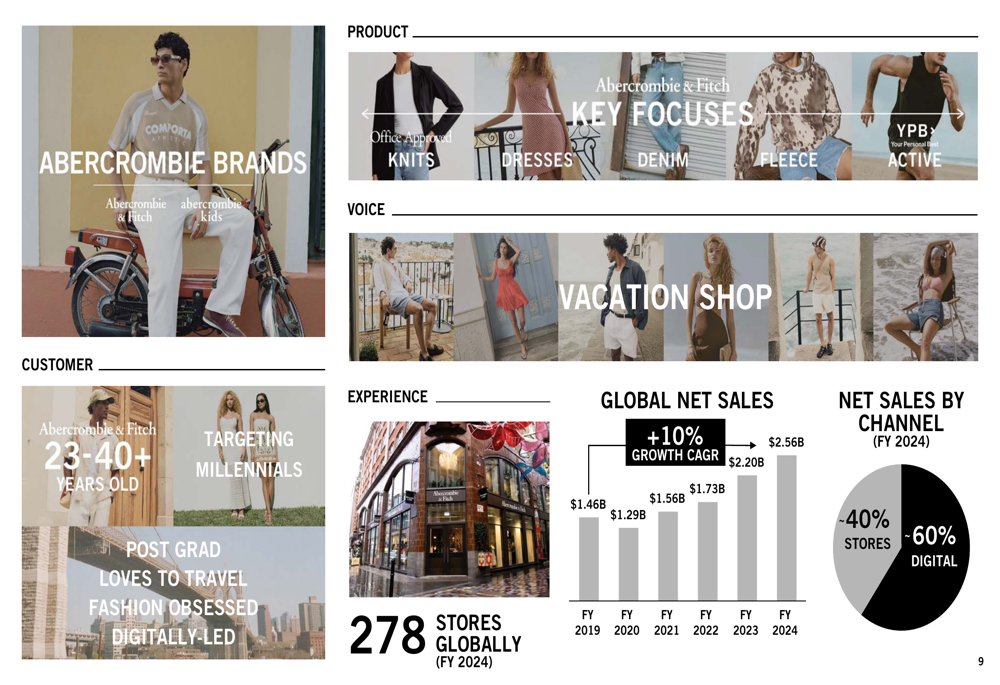

The company’s brand overview slides illustrate the distinct positioning and customer profiles:

The channel mix also differs significantly between the brands, with Abercrombie generating 60% of sales through digital channels, while Hollister remains more store-focused with 70% of sales coming from physical locations.

Regional Performance

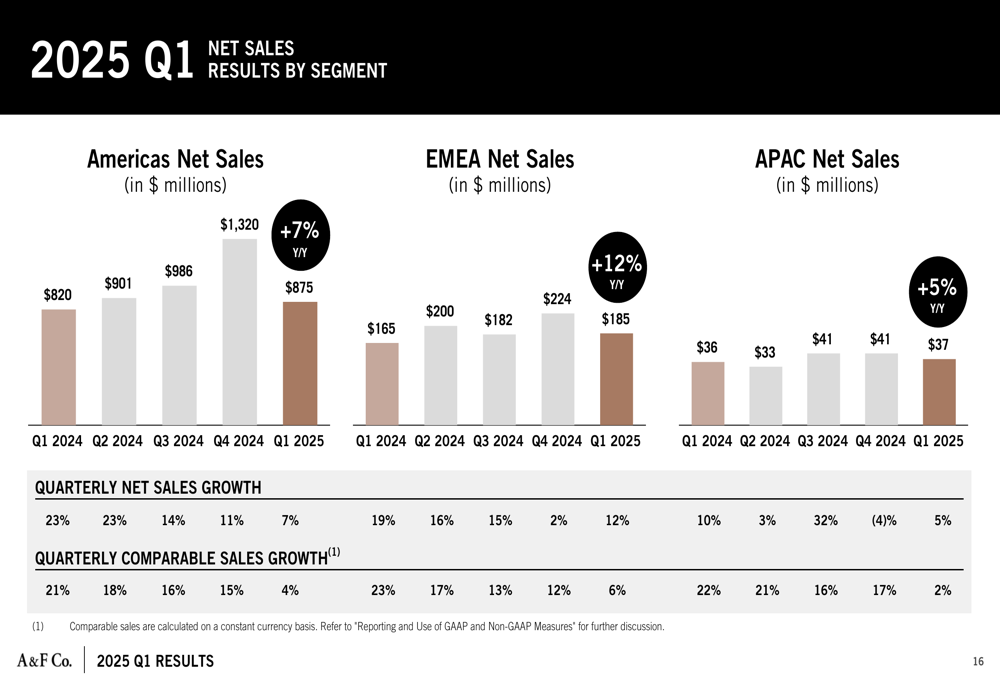

Abercrombie & Fitch reported growth across all three of its geographic regions in Q1 2025. EMEA (Europe, Middle East, and Africa) led with 12% year-over-year growth, followed by the Americas at 7% and APAC (Asia-Pacific) at 5%.

The following chart shows the net sales performance by region:

While all regions showed positive growth, there was a notable deceleration in comparable sales growth across the board. The Americas region saw comparable sales growth slow to 4% in Q1 2025 from 15% in the previous quarter. Similarly, EMEA’s comparable sales growth moderated to 6% from 12%, and APAC to 2% from 17%.

Financial Position and Outlook

The company’s financial position shows some mixed signals. Cash and equivalents stood at $511 million as of May 3, 2025, down significantly from $864 million in the same period last year. Inventories increased by 21% year-over-year to $542 million, outpacing sales growth of 8%.

Management attributes the inventory increase to a 6% rise in units and higher costs primarily from category mix changes. This inventory build warrants monitoring as it could potentially impact margins if promotional activity becomes necessary to move excess stock.

For the full fiscal year 2025, Abercrombie & Fitch provided the following outlook:

- Net sales growth of 3% to 6%

- Operating margin in the range of 12.5% to 13.5%

- Net income per diluted share of $9.50 to $10.50

- Capital expenditures of approximately $200 million

- Approximately 40 net store openings

For Q2 2025, the company expects:

- Net sales growth of 3% to 5%

- Operating margin in the range of 12% to 13%

- Net income per diluted share of $2.10 to $2.30

Strategic Initiatives

Abercrombie & Fitch’s presentation highlighted its "Always Forward Plan," which focuses on three key strategic pillars: Global Brand Growth, Enterprise-Wide Digital Revolution, and Financial Discipline.

The company’s approach to global brand growth encompasses collections and extensions, digital customer acquisition, and geographic expansion. This strategy is designed to leverage the company’s strong brand equity while adapting to evolving consumer preferences and regional market dynamics.

As shown in the financial discipline slide, the company has made significant progress in improving its cost structure and profitability:

Cost of sales as a percentage of net sales has improved from 43.1% in 2022 to 35.8% in 2024, while selling expenses have decreased from 39.5% to 34.2% over the same period. These improvements have contributed to the substantial operating margin expansion.

The company also continues to return capital to shareholders through share repurchases. Since the start of 2022, Abercrombie & Fitch has repurchased approximately 9 million shares for approximately $556 million, with $1.1 billion remaining under its current share repurchase authorization. For fiscal year 2025, the company plans to repurchase $400 million worth of shares.

In conclusion, Abercrombie & Fitch’s Q1 2025 results demonstrate continued momentum in the company’s transformation, with record sales and strong profitability. However, the divergent performance between brands, slowing comparable sales growth, and significant inventory build-up present challenges that management will need to address in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.