Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

ABM Industries Incorporated (NYSE:ABM) released its third quarter 2025 earnings presentation on September 5, 2025, reporting broad-based organic revenue growth across all segments but guiding to the lower end of its full-year outlook. The facilities services provider’s stock fell 5.41% in premarket trading to $45.50 following the release, reflecting investor concerns despite the company’s revenue growth and newly announced restructuring program.

The company operates across diverse markets including Business & Industry, Aviation, Manufacturing & Distribution, Education, and Technical Solutions, providing facility maintenance and management services. ABM’s presentation highlighted improvements in prime office space markets and robust demand for electrification-related services, particularly in its Technical Solutions segment.

Quarterly Performance Highlights

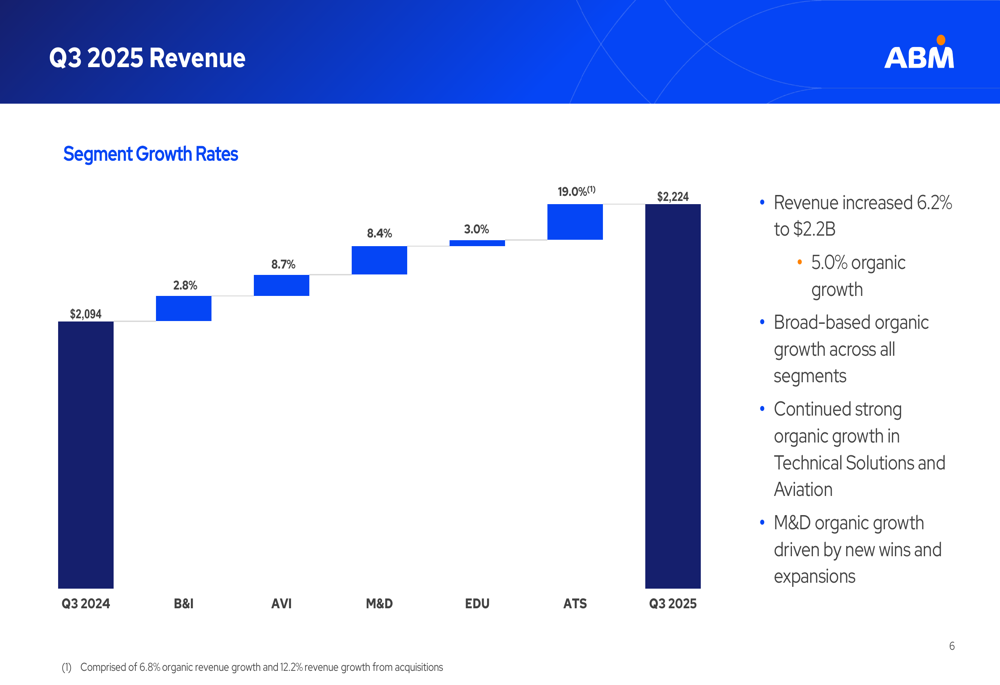

ABM reported total revenue of $2.2 billion for Q3 2025, representing 6.2% growth compared to the same period last year, with organic growth of 5.0%. The company’s GAAP net income rose significantly to $41.8 million from $4.7 million in Q3 2024, while adjusted net income slightly decreased to $51.7 million from $53.6 million. GAAP earnings per share increased to $0.67 from $0.07, while adjusted EPS declined slightly to $0.82 from $0.84 in the prior year.

As shown in the following revenue breakdown by segment:

The Technical Solutions segment showed the strongest growth at 19.0% (including 6.8% organic growth and 12.2% from acquisitions), followed by Aviation at 8.7% and Manufacturing & Distribution at 8.4%. Business & Industry, which represents ABM’s largest segment at 47% of total revenue, grew by 2.8%, while Education increased by 3.0%.

The quarterly revenue performance across segments is illustrated in this chart:

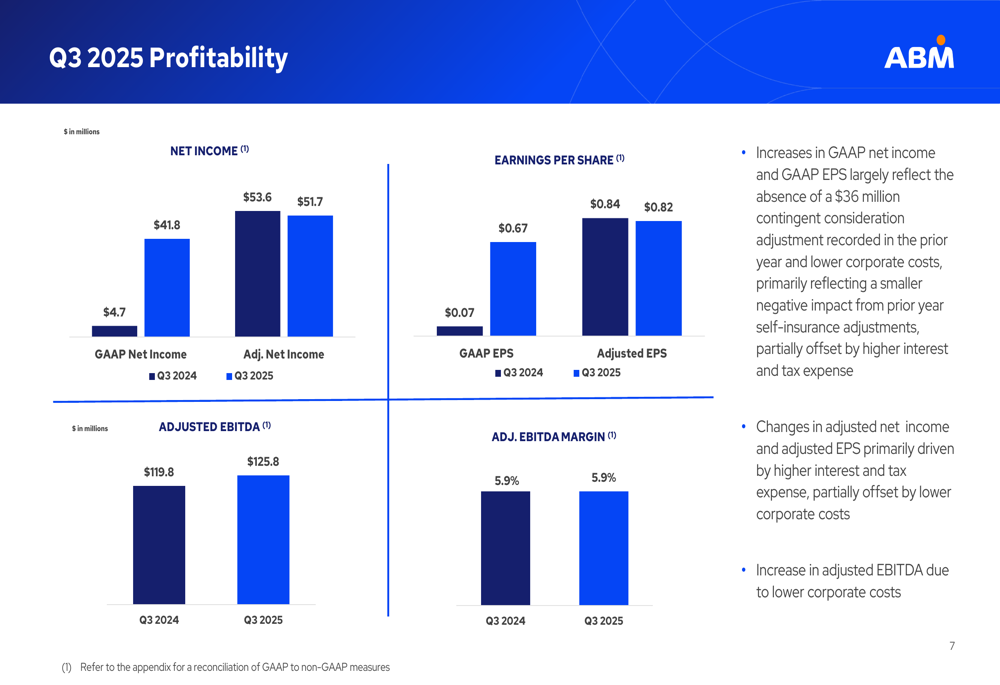

In terms of profitability, ABM maintained its adjusted EBITDA margin at 5.9% year-over-year, with adjusted EBITDA increasing to $125.8 million from $119.8 million in Q3 2024. The company noted that the significant increase in GAAP net income was largely due to the absence of a $36 million contingent consideration expense from the previous year and lower corporate costs.

The following chart illustrates ABM’s profitability metrics for Q3 2025 compared to Q3 2024:

Segment Performance Analysis

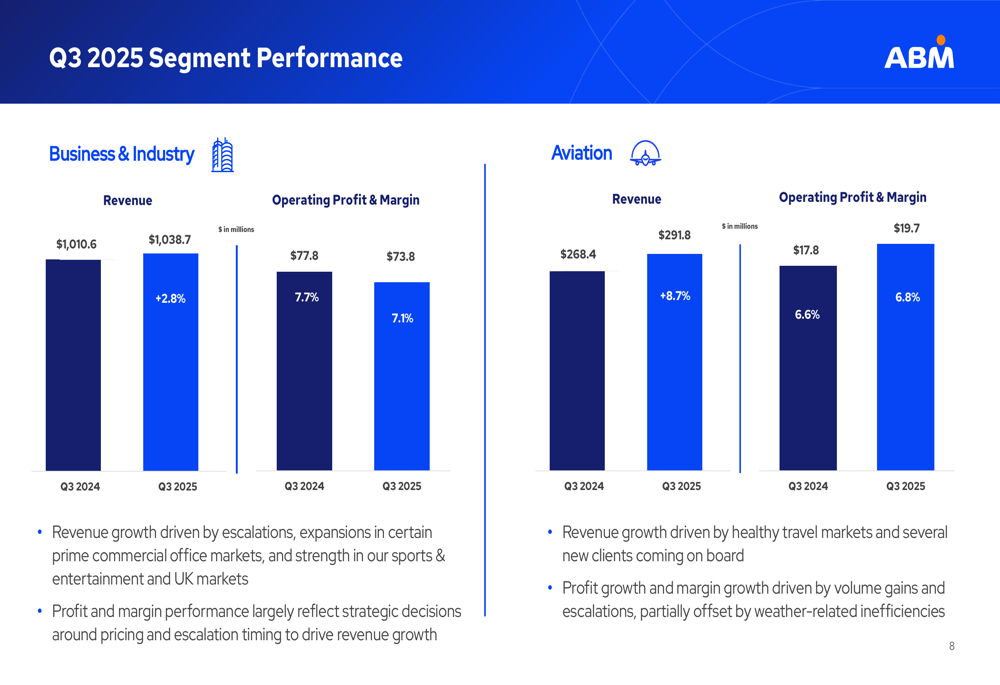

The Business & Industry segment, ABM’s largest revenue contributor, saw operating profit margin decline to 7.1% from 7.7% in the prior year. The company attributed this to strategic pricing decisions and escalation timing to drive revenue growth. Revenue growth in this segment was driven by escalations and expansions in prime commercial office markets and strength in the sports and entertainment sectors.

The Aviation segment showed both revenue growth and margin improvement, with operating margin increasing to 6.8% from 6.6%. This performance was driven by healthy travel markets and the addition of several new clients.

The segment performance for Business & Industry and Aviation is detailed in the following chart:

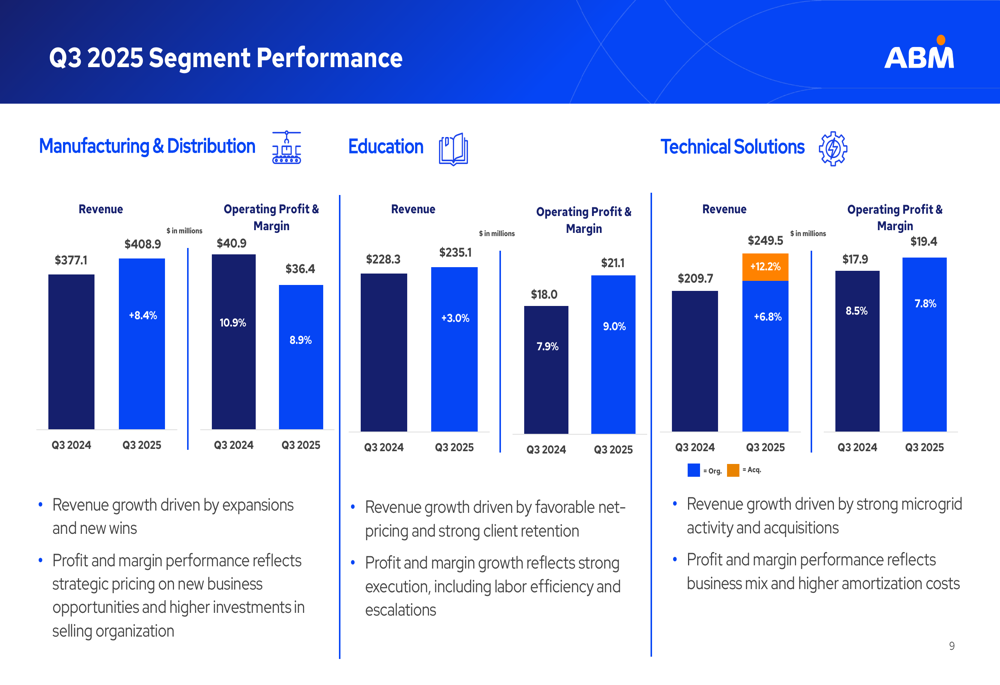

Manufacturing & Distribution revenue increased by 8.4%, but operating margin declined to 8.9% from 10.9% in the prior year. The Education segment showed both revenue growth and margin improvement, with operating margin increasing to 9.0% from 7.9%. Technical Solutions revenue grew by 19.0%, though operating margin declined slightly to 7.8% from 8.5%, with strong microgrid activity driving organic growth.

The performance of these segments is illustrated in the following chart:

Strategic Initiatives & Capital Allocation

ABM announced the initiation of a restructuring program expected to deliver a minimum of $35 million in annual run-rate savings. While specific details about the program were limited in the presentation, this initiative appears to be a key component of the company’s strategy to improve profitability amid rising costs.

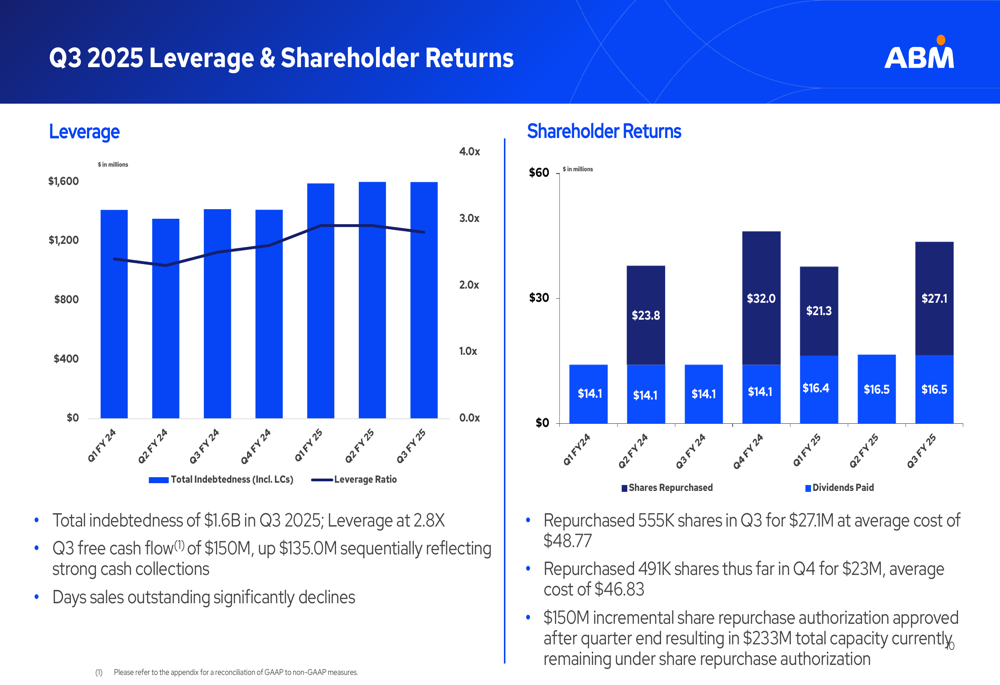

The company reported strong cash flow generation in the quarter, with free cash flow of $150.2 million, up $135.0 million sequentially. Days sales outstanding significantly declined, reflecting improved collections efficiency. ABM maintained a leverage ratio of 2.8x with total indebtedness of $1.6 billion.

On the capital return front, ABM repurchased 555,000 shares in Q3 for $27.1 million at an average cost of $48.77 per share. The company has continued its repurchase activity in Q4, buying back an additional 491,000 shares for $23 million at an average cost of $46.83. The Board approved a $150 million increase in share repurchase authorization, resulting in $233 million total capacity remaining under the program.

The company’s leverage and shareholder returns are detailed in the following chart:

Forward-Looking Statements & Outlook

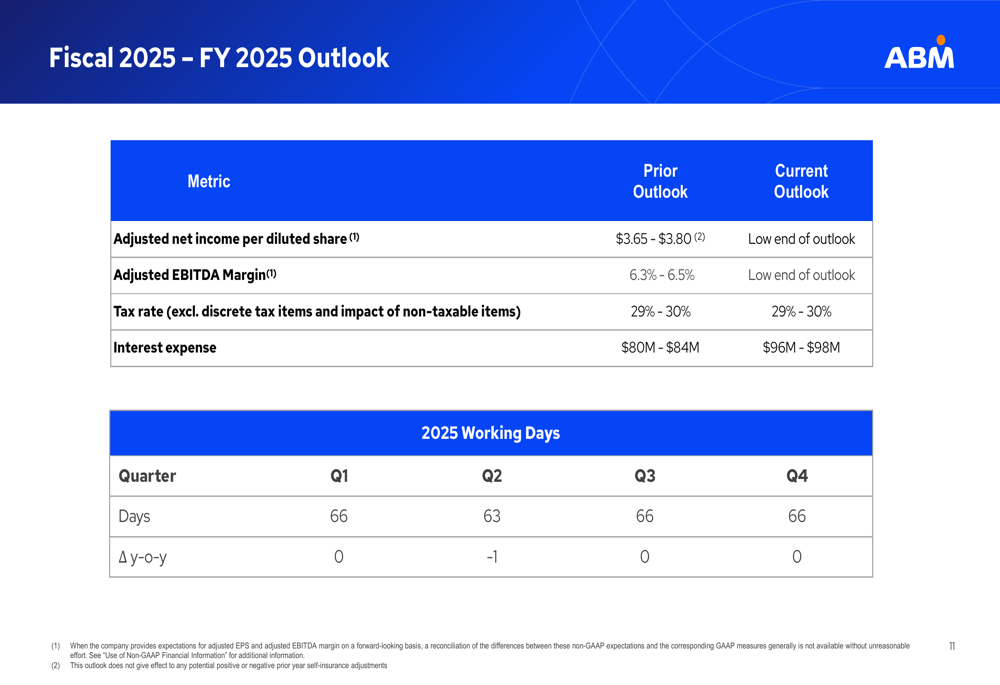

ABM provided an updated outlook for fiscal year 2025, guiding to the low end of its previously announced ranges. The company now expects adjusted net income per diluted share to be at the low end of $3.65 to $3.80 and adjusted EBITDA margin to be at the low end of 6.3% to 6.5%. ABM also projects interest expense of $96-$98 million and a tax rate of 29-30%, excluding discrete tax items and the impact of non-taxable items.

The company’s fiscal 2025 outlook is summarized in the following chart:

Market Reaction

ABM’s stock declined 5.41% in premarket trading following the earnings release, trading at $45.50. This represents a significant drop from its 52-week high of $59.78 and reflects investor concerns about the company guiding to the low end of its full-year outlook despite revenue growth. The slight year-over-year decline in adjusted EPS may also be contributing to the negative market reaction.

This performance follows a pattern seen after the Q2 2025 results, when ABM’s stock fell 5.85% after reporting a slight miss on adjusted EPS expectations. The continued pressure on margins and the need for a restructuring program may be raising questions about the company’s ability to translate revenue growth into increased profitability in the current economic environment.

Despite these challenges, ABM’s broad-based organic growth across all segments, strong bookings growth of 15% for the first nine months of 2025, and improved cash flow generation highlight the company’s operational resilience. The increased share repurchase authorization also signals management’s confidence in ABM’s long-term prospects, even as it navigates near-term profitability challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.