Gold bars to be exempt from tariffs, White House clarifies

Introduction & Market Context

Acacia Research Corporation (NASDAQ:ACTG) released its second quarter 2025 earnings presentation on August 6, showing a significant decline in performance following an exceptional first quarter. The company’s stock opened at $3.70 in premarket trading, up 3.06% from the previous close of $3.59, suggesting investors had already factored in the quarterly results.

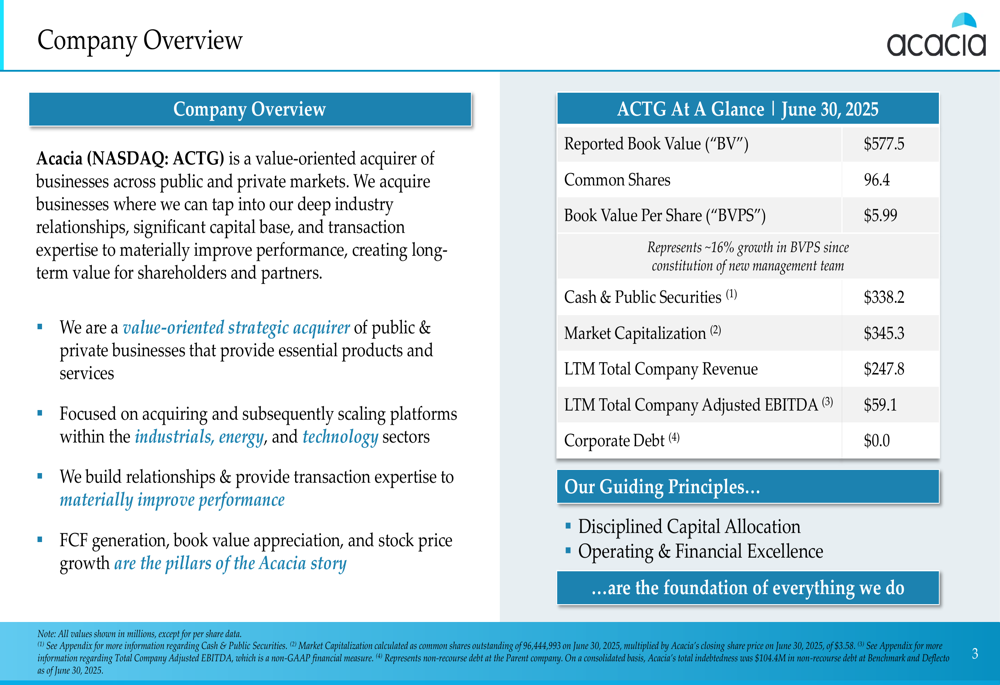

As a value-oriented acquirer focused on industrials, energy, and technology sectors, Acacia continues to maintain a strong balance sheet with zero corporate debt, though its financial performance showed considerable volatility between quarters.

Quarterly Performance Highlights

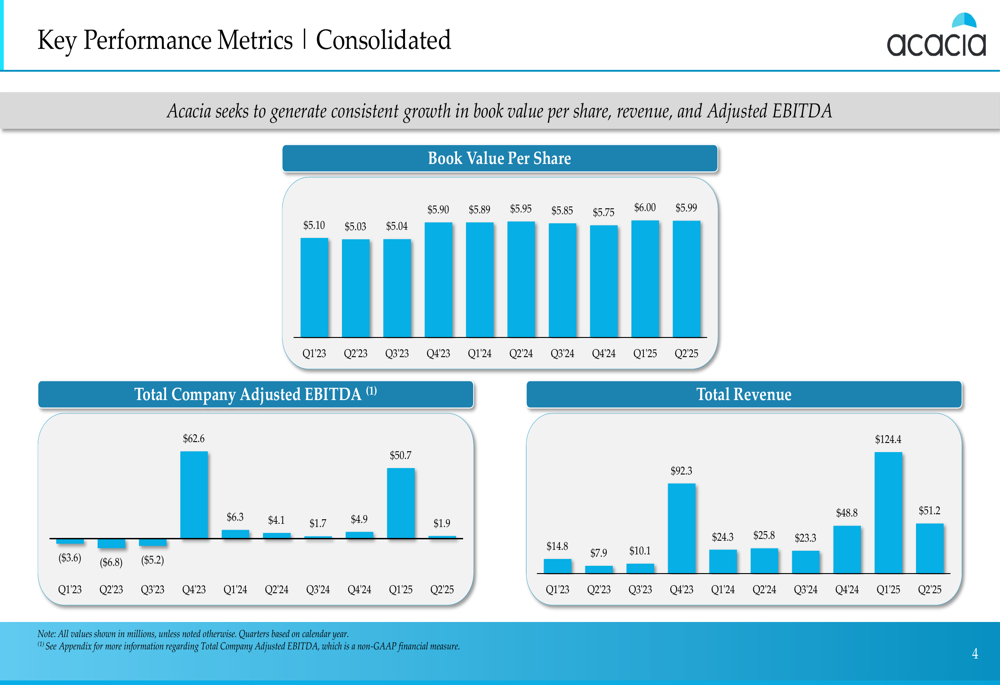

Acacia reported Q2 2025 revenue of $51.2 million, a substantial 58.8% decrease from the $124.4 million reported in Q1 2025. Similarly, Adjusted EBITDA fell dramatically to $1.9 million in Q2 from $50.7 million in the previous quarter.

The company’s consolidated performance metrics over recent quarters reveal this significant volatility, particularly in revenue and Adjusted EBITDA, while Book Value Per Share has shown more consistent growth.

As shown in the following chart of quarterly performance metrics, Acacia’s Book Value Per Share reached $5.99 in Q2 2025, representing approximately 16% growth since the new management team took over:

The sharp quarter-to-quarter fluctuations in revenue and EBITDA are primarily driven by the company’s Intellectual Property Operations segment, which can generate significant but inconsistent income from settlements and licensing agreements.

Segment Performance Analysis

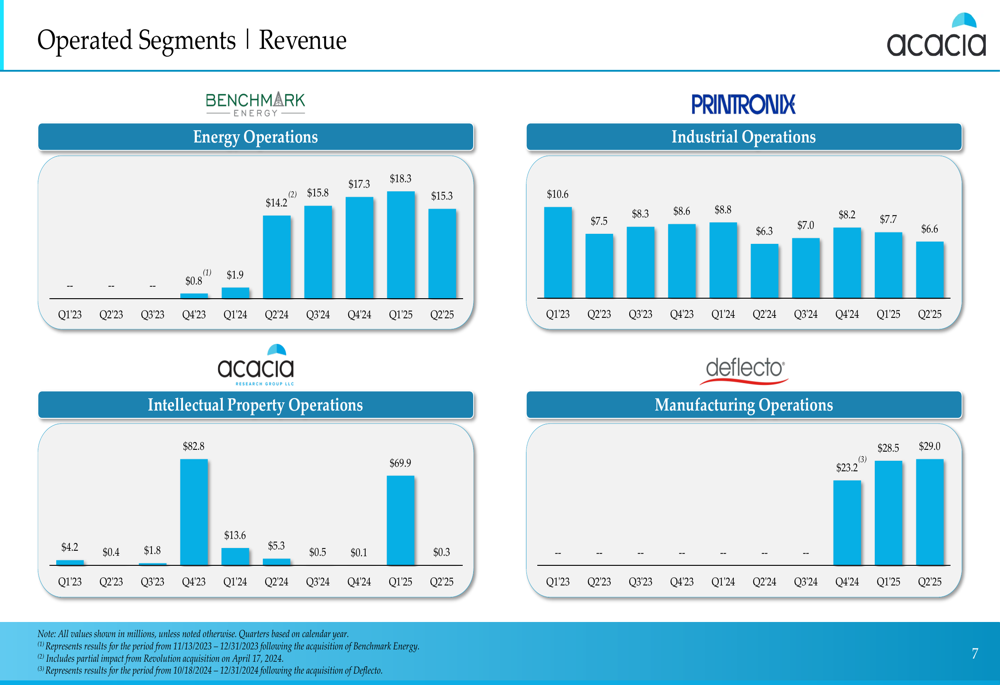

Acacia’s business is divided into several operating segments, each showing different performance patterns. The quarterly breakdown of revenue by segment illustrates these varying trajectories:

The company’s Energy Operations segment, represented by Benchmark Energy, has shown consistent growth, reaching $18.3 million in Q1 2025 before declining slightly to $15.3 million in Q2 2025. The Industrial Operations segment (Printronix) has maintained relatively stable revenue between $6-9 million per quarter.

The most notable performance comes from the Intellectual Property Operations segment, which generated $69.9 million in Q1 2025 but only $0.3 million in Q2 2025, explaining the significant overall revenue drop. The Manufacturing Operations segment (Deflecto), a newer addition starting in Q4 2024, has shown consistent quarterly revenue around $29 million.

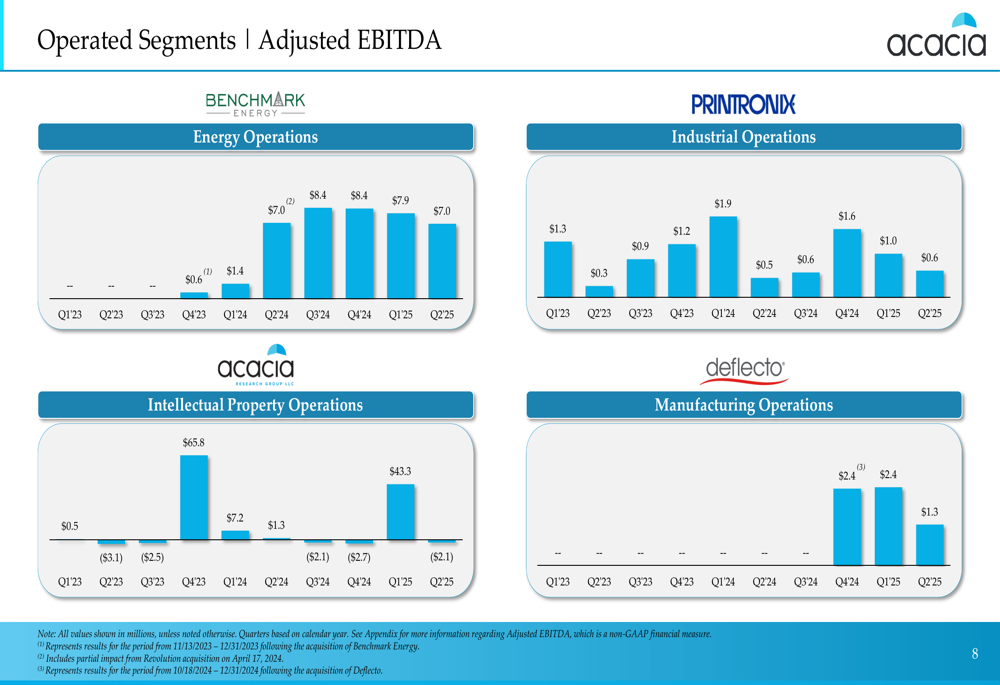

Similarly, Adjusted EBITDA by segment shows parallel trends:

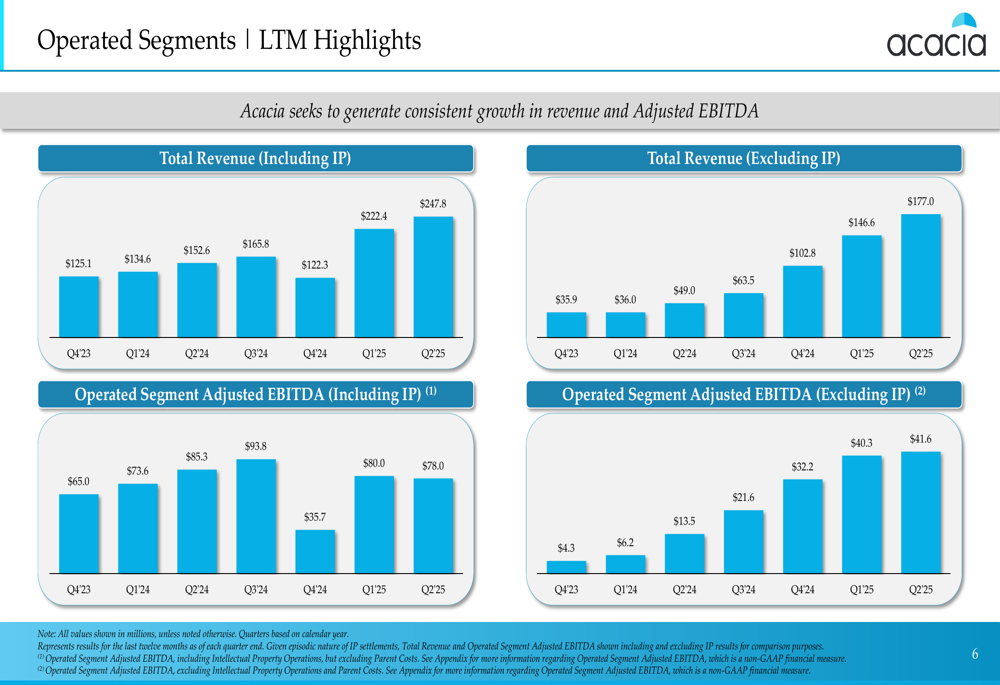

The LTM (Last Twelve Months) view provides a clearer picture of the company’s overall performance trajectory across segments:

Balance Sheet Strength

Despite the quarterly volatility in operating performance, Acacia maintains a strong financial position. As of June 30, 2025, the company reported:

- Book Value: $577.5 million

- Cash & Public Securities: $338.2 million

- Market Capitalization: $345.3 million

- Corporate Debt: $0.0

This strong cash position follows the significant IP settlement reflected in Q1 2025 results. The company’s comprehensive overview highlights its financial standing and strategic positioning:

Detailed Financial Analysis

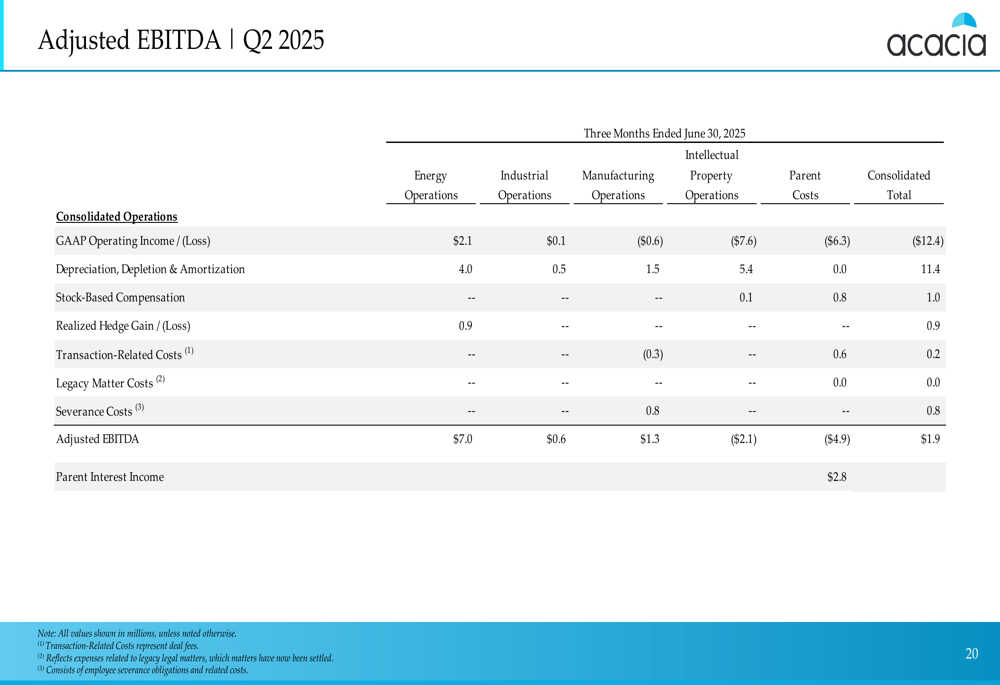

The quarterly breakdown of Adjusted EBITDA reveals the significant contribution from Intellectual Property Operations in Q1 2025 ($43.3 million) compared to a loss of $2.1 million in Q2 2025. Meanwhile, Energy Operations continued to deliver consistent results with $7.0 million in Adjusted EBITDA for Q2 2025.

The detailed reconciliation of Q2 2025 Adjusted EBITDA shows:

This reconciliation highlights how depreciation, depletion, and amortization ($11.4 million) significantly impact the conversion from operating loss to positive Adjusted EBITDA.

Forward Outlook

While the presentation doesn’t provide explicit forward guidance, Acacia’s strategy remains focused on disciplined capital allocation and operational excellence. The company positions itself as a value-oriented acquirer of businesses across public and private markets, with a focus on the industrials, energy, and technology sectors.

The significant cash position of $338.2 million provides Acacia with substantial dry powder for future acquisitions, aligning with CEO MJ McNulty’s previous statement that "this uncertain unique period in capital markets presents compelling opportunities for our business."

Investors should note that while the company’s diversified business model provides some stability, the significant volatility in the Intellectual Property segment makes quarterly performance difficult to predict. The sharp decline in Q2 2025 performance following the exceptional Q1 results underscores this challenge.

As Acacia continues to execute its acquisition strategy, the company’s ability to generate consistent performance across segments while leveraging its strong balance sheet will be key factors for investors to monitor in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.