Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

ACM Research, Inc. (NASDAQ:ACMR), a supplier of wafer processing solutions for semiconductor and advanced wafer-level packaging applications, presented its first quarter 2025 earnings results on May 8, 2025. The company reported continued revenue growth but faced margin pressure as it pursues ambitious expansion plans in both product offerings and geographic reach.

The semiconductor equipment manufacturer’s performance comes amid a period of cautious optimism in the semiconductor industry, with selective capital spending by chipmakers and ongoing geopolitical tensions affecting global supply chains. ACM Research’s focus on the Chinese market, which contributed significantly to its revenue, positions it uniquely among semiconductor equipment providers.

Quarterly Performance Highlights

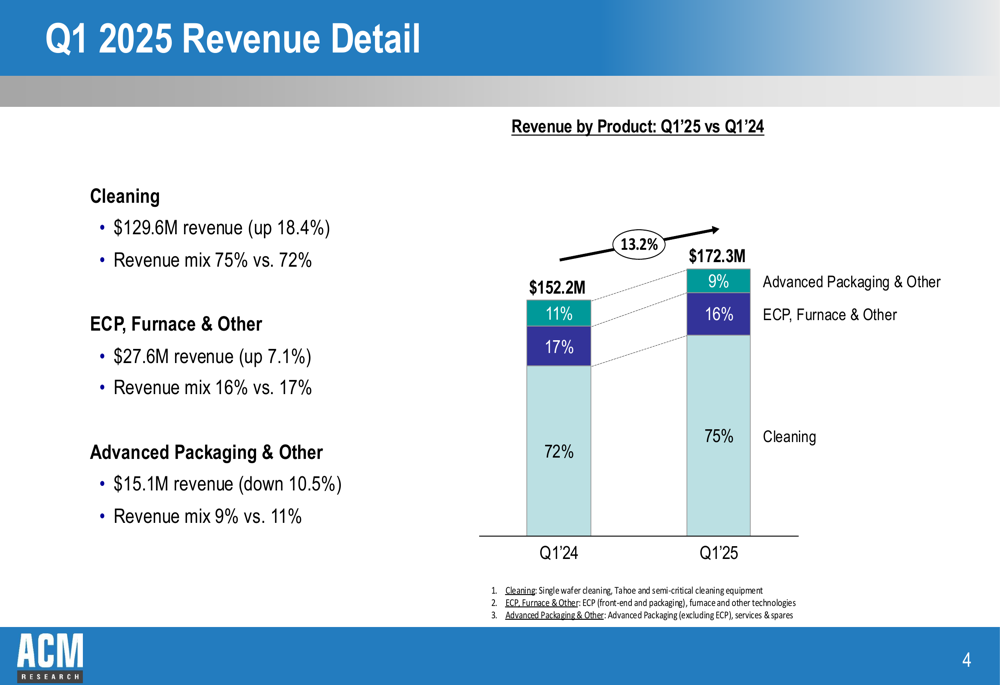

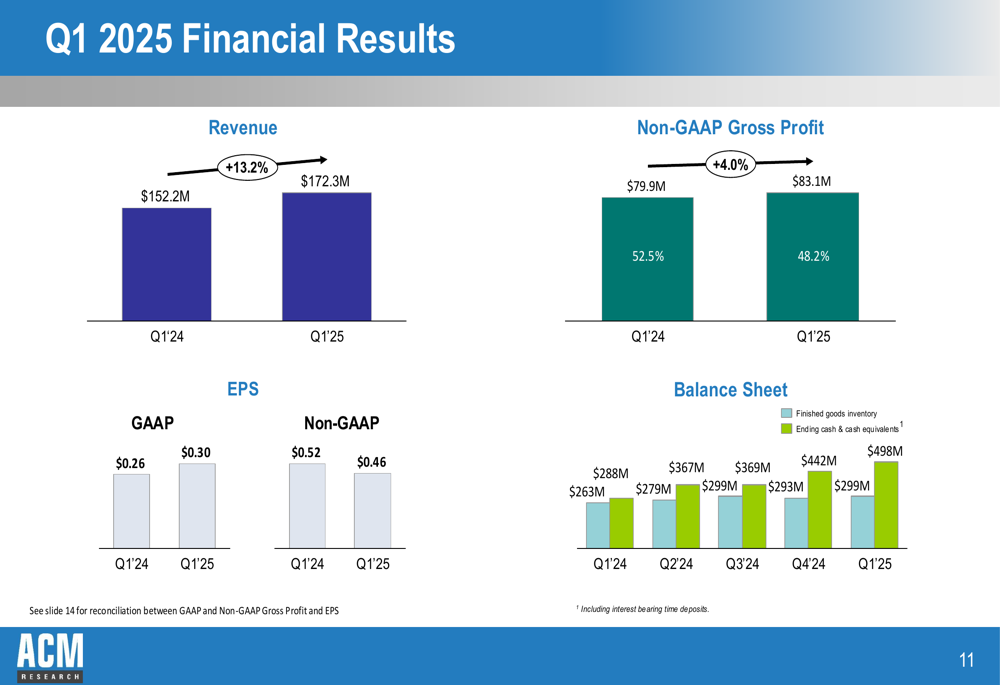

ACM Research reported Q1 2025 revenue of $172.3 million, representing a 13.2% increase year-over-year from $152.2 million in Q1 2024. However, this growth rate marks a deceleration from the 31.2% year-over-year growth reported in Q4 2024. Total (EPA:TTEF) shipments for the quarter were $157 million, down 36% year-over-year, suggesting potential challenges in converting orders to recognized revenue.

The company’s product mix continues to be dominated by cleaning tools, which accounted for 75% of revenue ($129.6 million), up from 72% in the same period last year. ECP, Furnace & Other contributed 16% ($27.6 million), while Advanced Packaging (NYSE:PKG) & Other represented 9% ($15.1 million) of total revenue.

As shown in the following chart of quarterly revenue breakdown by product category:

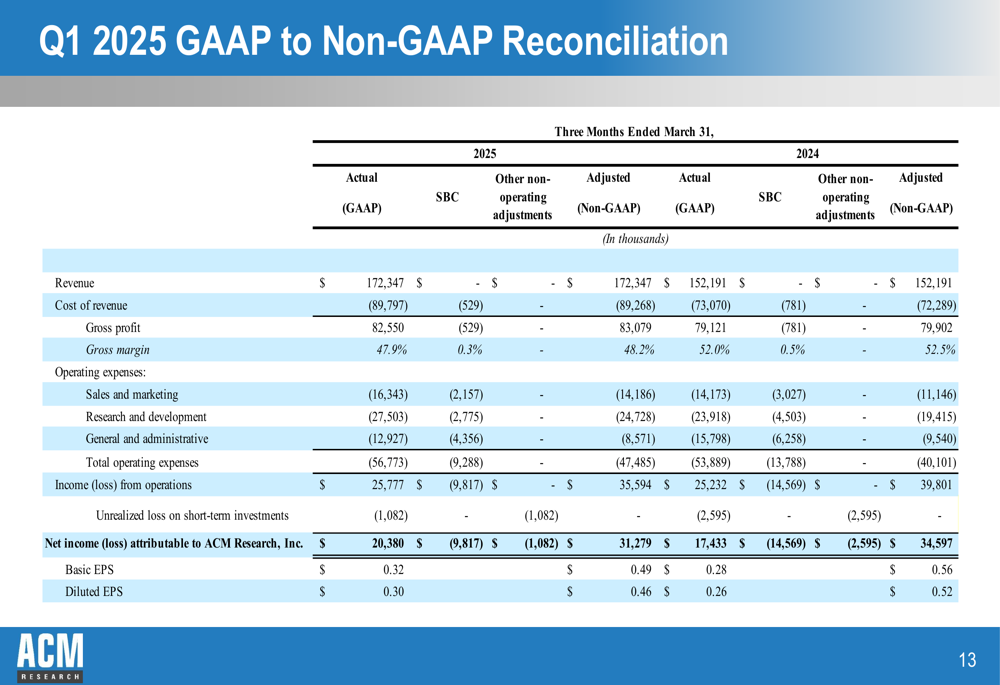

Profitability metrics showed mixed results, with GAAP gross margin declining to 47.9% from 52.0% in Q1 2024, and non-GAAP gross margin falling to 48.2% from 52.5%. GAAP operating income increased slightly by 2.2% year-over-year to $25.8 million, representing 15.0% of revenue. However, non-GAAP operating income decreased by 10.6% to $35.6 million, or 20.7% of revenue.

Diluted GAAP earnings per share improved to $0.30 from $0.26 in Q1 2024, while diluted non-GAAP earnings per share declined to $0.46 from $0.52 in the prior year period.

The following chart illustrates ACM Research’s key financial metrics for Q1 2025:

Detailed Financial Analysis

ACM Research maintained a strong balance sheet, with cash and cash equivalents reaching $488 million at the end of Q1 2025, up from $442 million at the end of Q4 2024 and significantly higher than the $288 million reported in Q1 2024. This robust cash position provides the company with flexibility to fund its expansion plans and navigate potential market uncertainties.

Finished goods inventory increased to $299 million, compared to $293 million in Q4 2024 and $263 million in Q1 2024, reflecting the company’s preparation for anticipated future demand and potentially longer sales cycles.

The reconciliation between GAAP and non-GAAP measures reveals significant adjustments, particularly in operating expenses. For Q1 2025, non-GAAP adjustments reduced total operating expenses from $56.8 million to $47.5 million, primarily through reductions in sales and marketing, research and development, and general and administrative expenses.

Strategic Initiatives

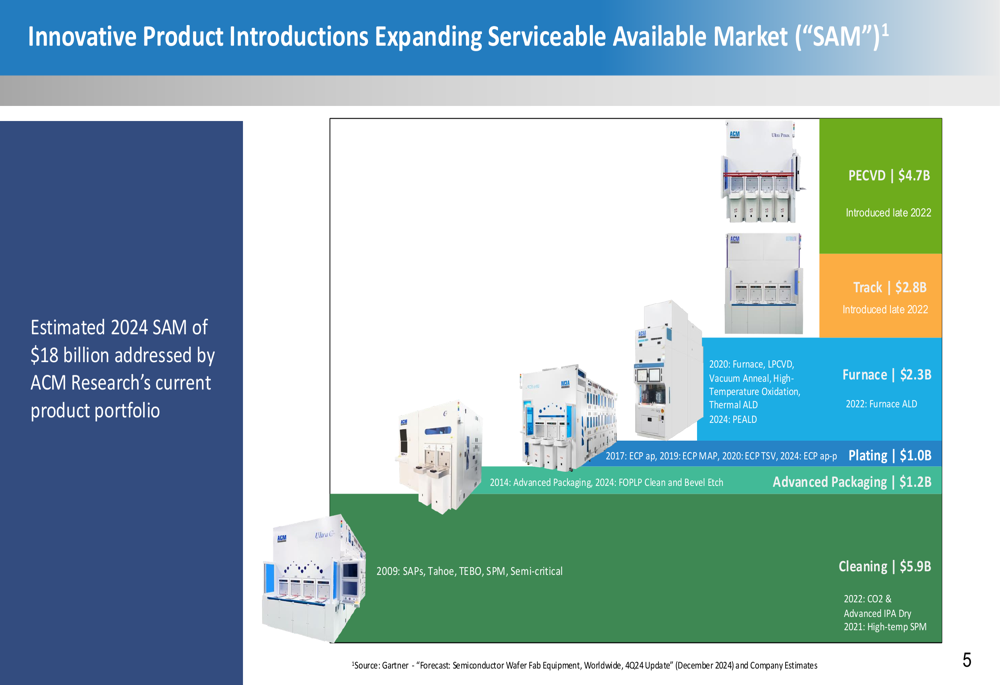

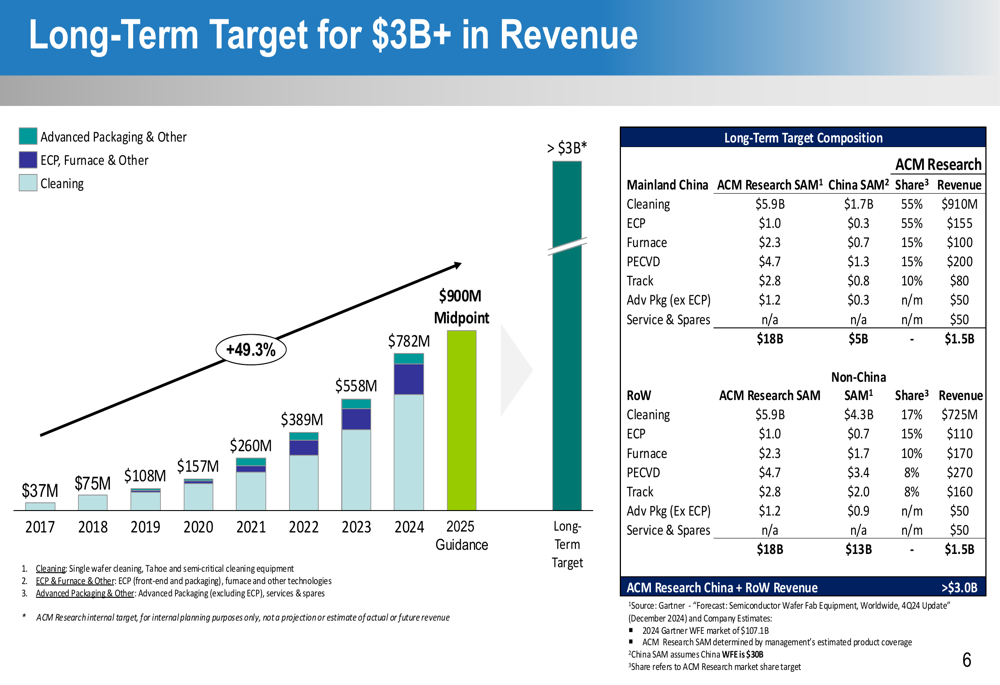

ACM Research continues to expand its product portfolio to address a larger serviceable available market (SAM), which the company estimates at $18 billion for 2024. The company’s diverse product offerings span cleaning, advanced packaging, plating, furnace, track, and PECVD technologies, allowing it to target multiple segments of the semiconductor manufacturing process.

The following illustration demonstrates how ACM’s expanding product portfolio addresses its growing serviceable market:

The company has set an ambitious long-term revenue target of over $3 billion, representing significant growth from its 2024 guidance of $782 million and 2025 guidance of $850-950 million. This target is supported by expected growth in both mainland China and the rest of the world markets.

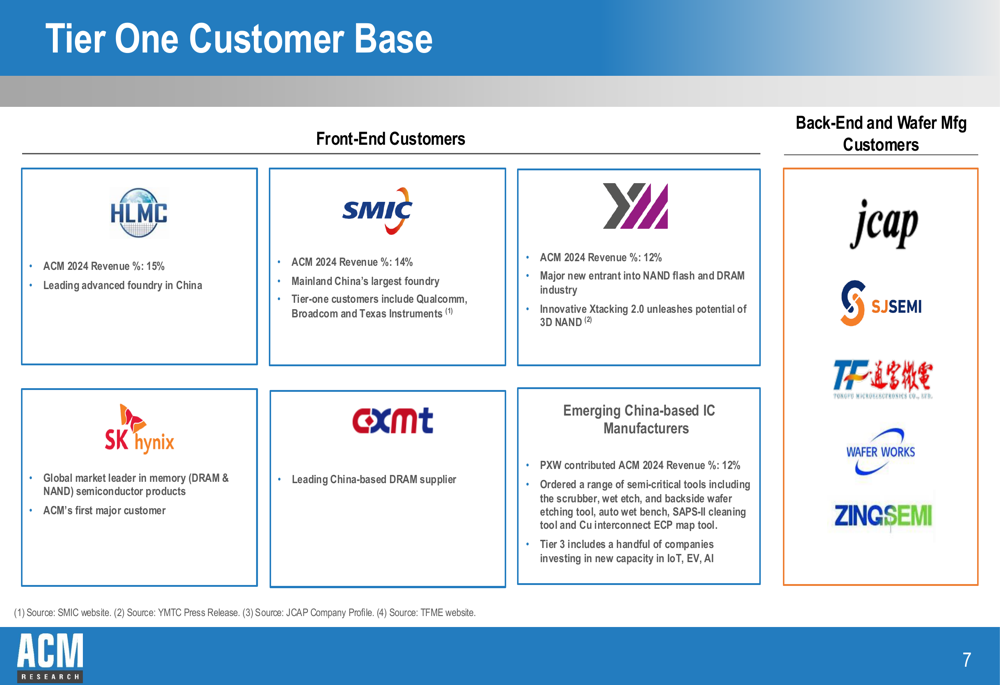

ACM Research maintains a strong customer base of tier-one semiconductor manufacturers, primarily in China. Key customers include HLMC (15% of 2024 revenue), SMIC (14%), YMTC (12%), and PXW (12%), along with other prominent players in the front-end, back-end, and wafer manufacturing segments.

Geographic expansion remains a key focus, with the company’s Lingang production and R&D center in Shanghai nearing completion. This facility will provide approximately 1 million square feet of space, significantly enhancing ACM’s manufacturing capabilities in China.

Additionally, ACM Research is establishing a foothold in the United States with its Oregon R&D and clean room facility in Hillsboro, which was purchased in October 2024. This 39,500 square foot facility, including a 5,200 square foot clean room, will support the company’s efforts to expand its presence in the U.S. market.

Forward-Looking Statements

ACM Research maintained its 2025 revenue guidance range of $850-950 million, which represents approximately 15% year-over-year growth at the midpoint compared to 2024 revenue of $782 million. This outlook reflects the company’s assessment of ongoing international trade policy impacts, various customer spending scenarios, supply chain constraints, and the timing of acceptances for first tools under evaluation.

The company highlighted several operational achievements that position it for future growth, including the qualification of its single-wafer high-temperature SPM tool by a key logic device manufacturer in mainland China and its Ultra ECP ap-p tool winning the 2025 3D InCites Technology Enablement Award for innovation in horizontal plating for panel-level packaging.

While ACM Research faces challenges including margin pressure and a complex geopolitical environment, its expanding product portfolio, strong customer relationships, and robust balance sheet provide a foundation for continued growth as it pursues its long-term revenue target of over $3 billion.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.