First Brands Group debt targeted by Apollo Global Management - report

ACM Research Inc (NASDAQ:ACMR) released its second quarter 2025 earnings presentation on August 6, showing modest revenue growth but declining profitability. The semiconductor equipment manufacturer’s stock dropped 10.59% in premarket trading to $26.51, suggesting investors were disappointed with the results despite some positive developments.

Quarterly Performance Highlights

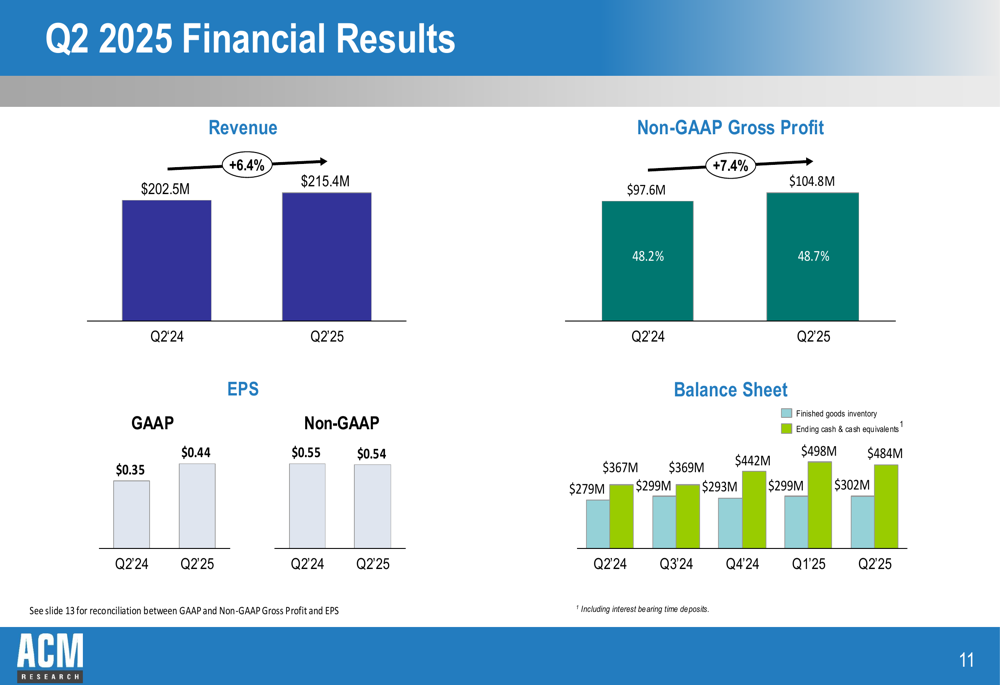

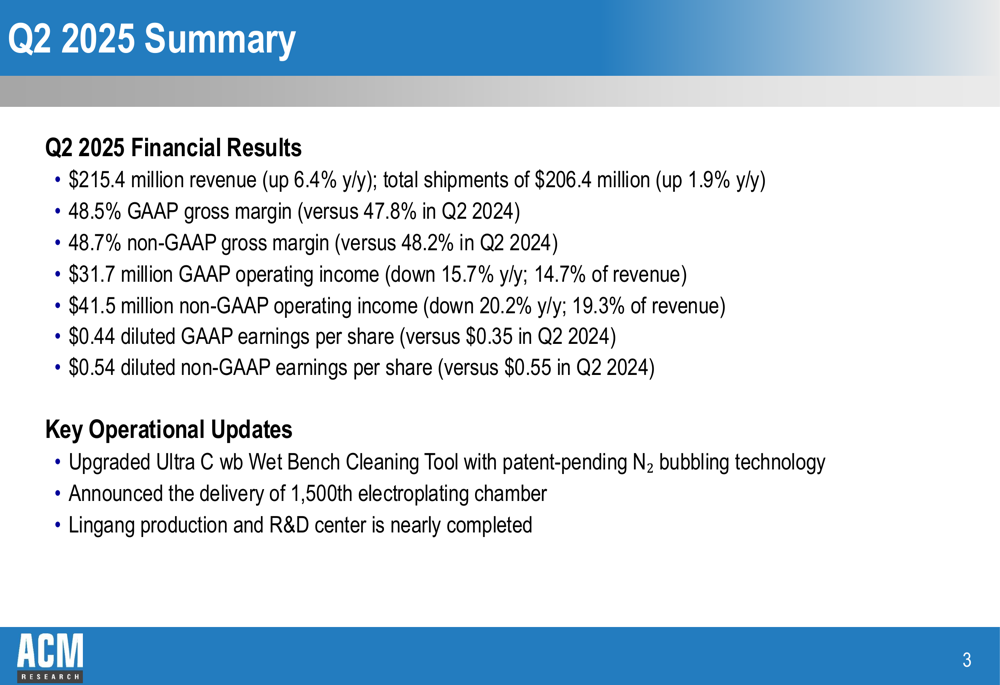

ACM Research reported Q2 2025 revenue of $215.4 million, representing a 6.4% year-over-year increase. However, the company’s GAAP operating income declined 15.7% to $31.7 million, while non-GAAP operating income fell more significantly by 20.2% to $41.5 million. Diluted GAAP earnings per share came in at $0.44, compared to $0.35 in Q2 2024, while non-GAAP EPS was $0.54, slightly down from $0.55 a year earlier.

As shown in the following chart of quarterly financial results:

The company maintained strong gross margins at 48.5% GAAP and 48.7% non-GAAP, exceeding the company’s target range. Cash and cash equivalents reached $302 million at the end of Q2 2025, showing steady improvement from $279 million in the same period last year.

"We continued to make progress on our key operational initiatives during the quarter," said David Wang, CEO of ACM Research, as reflected in the company’s presentation. Notable achievements included upgrading the Ultra C wb Wet Bench Cleaning Tool with patent-pending N2 bubbling technology and delivering the 1,500th electroplating chamber.

Product Mix and Strategic Initiatives

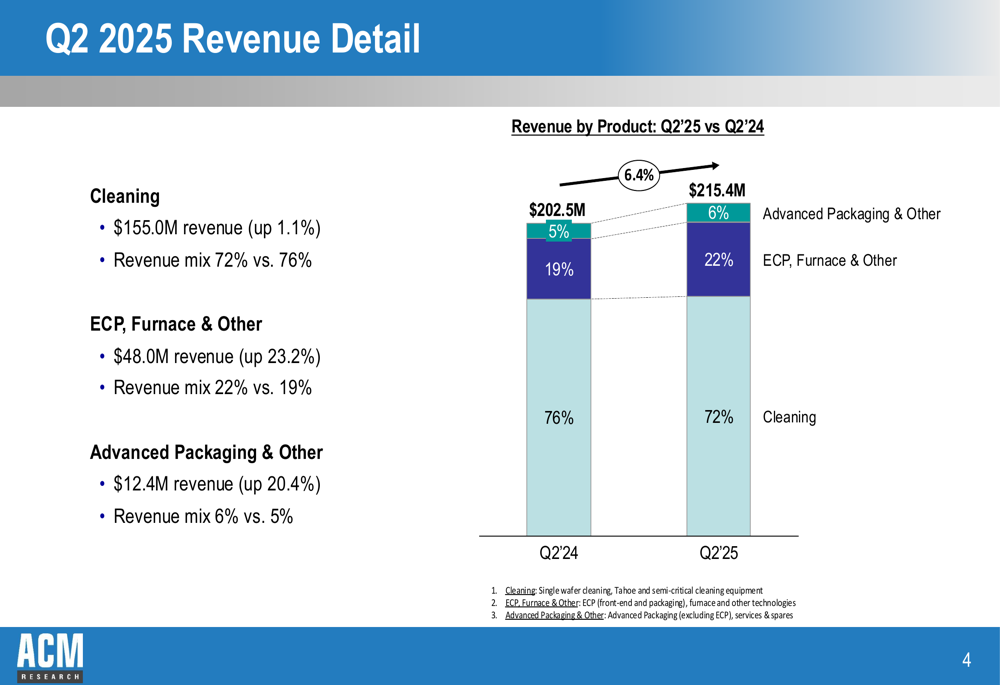

The company’s revenue mix shows a strategic shift toward diversification beyond its core cleaning products. While cleaning tools still represent the majority of revenue at 72%, this is down from 76% in Q2 2024. Meanwhile, ECP, Furnace & Other products grew 23.2% year-over-year to $48.0 million, increasing their share of revenue from 19% to 22%.

The following chart illustrates this evolving product mix:

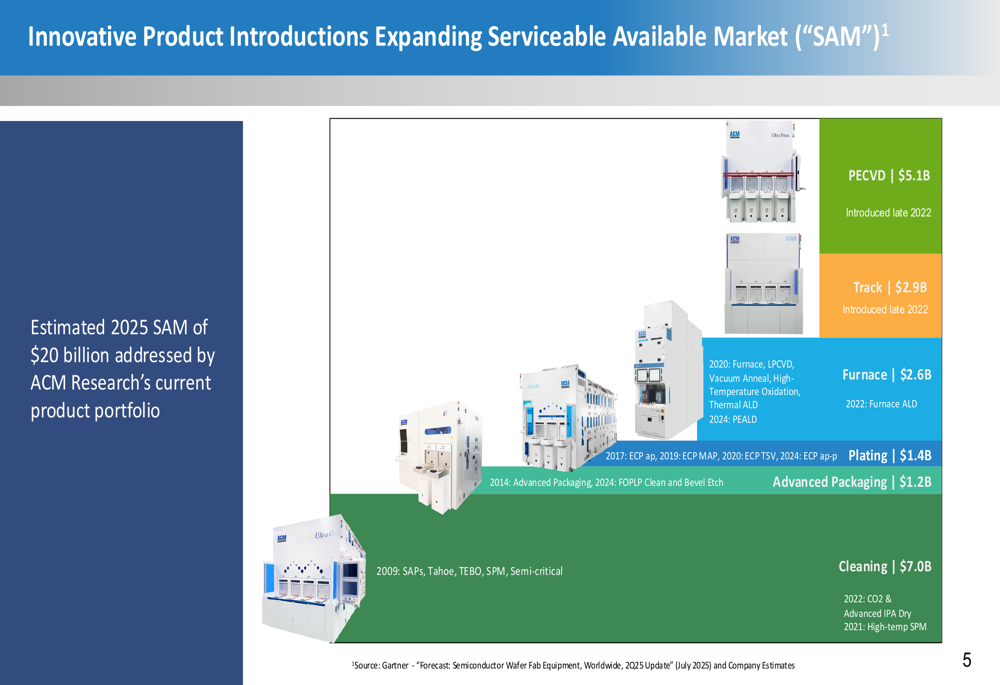

ACM Research continues to expand its Serviceable Available Market (SAM), which now stands at an estimated $20 billion for 2025. The company has strategically introduced new products in recent years, including PECVD and Track products in late 2022, which address markets worth $5.1 billion and $2.9 billion respectively.

The company’s product portfolio expansion is illustrated in this comprehensive overview:

Global Expansion and Customer Base

ACM Research is strengthening its global presence with facilities in both China and the United States. The company’s Lingang R&D and Production Center in Shanghai is nearly completed, while its Oregon R&D and Clean Room Facility, purchased in October 2024, provides 39,500 square feet of space including a 5,200 square foot clean room to support U.S. market expansion.

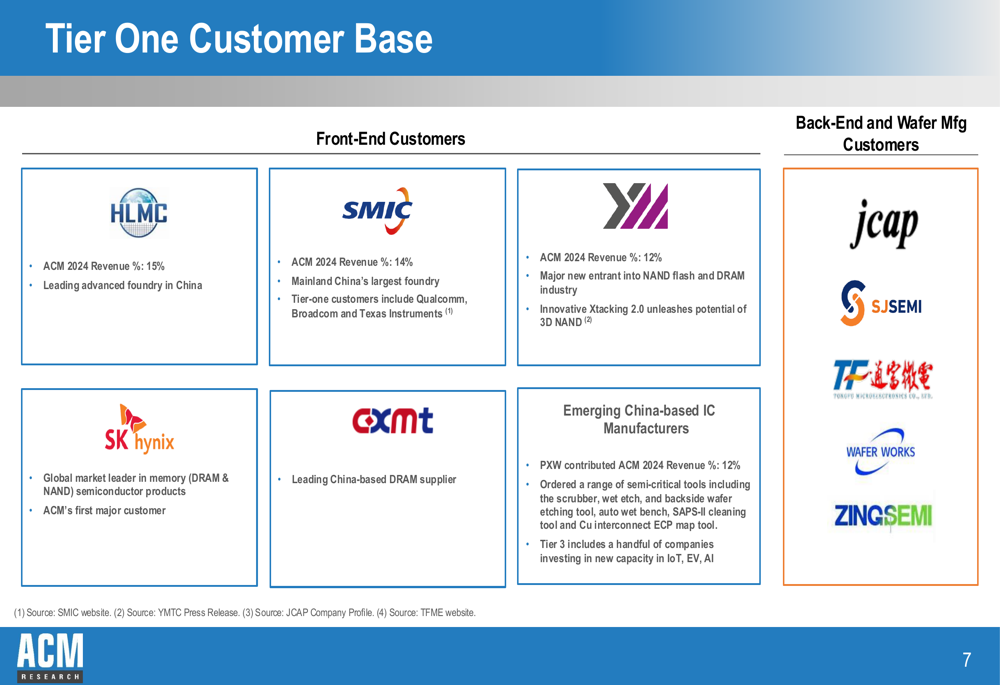

The company maintains relationships with tier-one customers in both front-end and back-end semiconductor manufacturing. Key customers include SMIC (representing 14% of 2024 revenue), HLMC, YMTC, SK Hynix, and CXMT for front-end applications, along with several back-end and wafer manufacturing customers.

The following slide details ACM’s impressive customer portfolio:

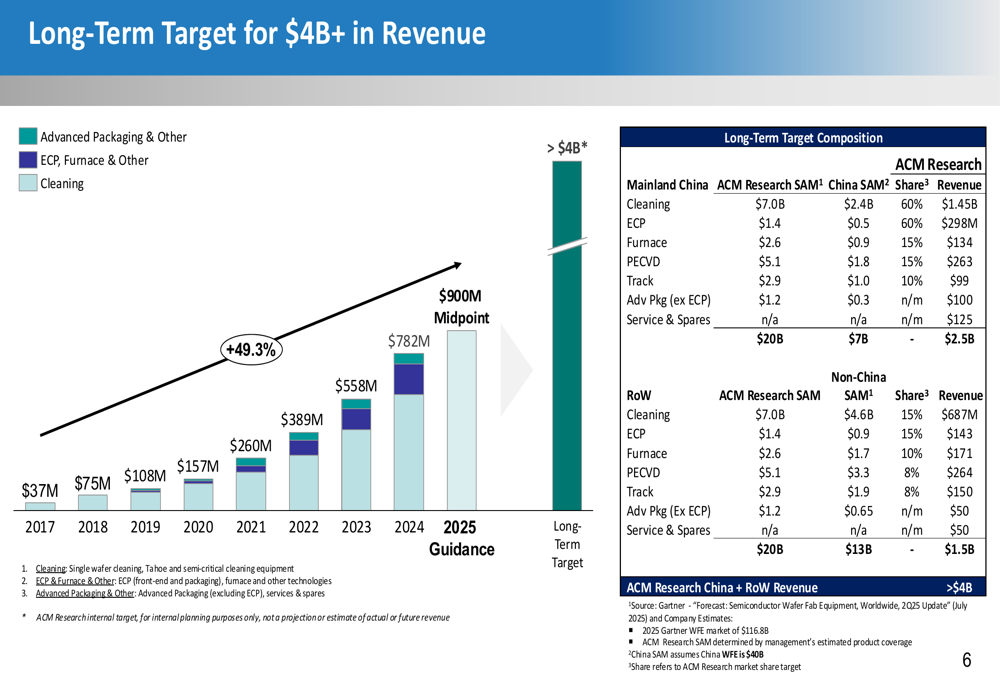

Long-Term Growth Strategy

Despite current challenges, ACM Research maintains ambitious long-term revenue targets exceeding $4 billion. The company’s roadmap shows progression from $37 million in 2017 to its 2025 guidance of $782-950 million, with a clear path toward future growth.

This growth strategy is based on expanding both within China (targeting $2.5 billion from a $7 billion SAM) and internationally (targeting $1.5 billion from a $13 billion SAM). The company plans to leverage its technological advantages across multiple product categories to achieve these goals.

The following chart outlines ACM’s long-term revenue targets and composition:

Forward-Looking Statements

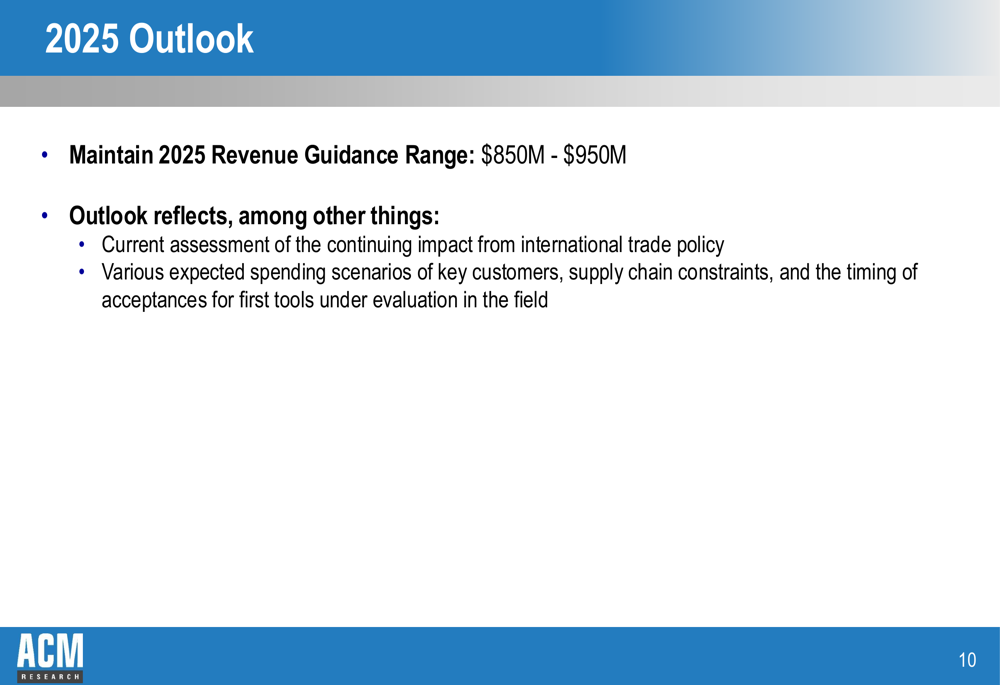

ACM Research maintained its 2025 revenue guidance range of $850-950 million, despite facing headwinds from international trade policies and supply chain constraints. The company acknowledged that its outlook reflects "the continuing impact from international trade policy" and "various expected spending scenarios of key customers."

The maintained guidance suggests management confidence in navigating current challenges, though the significant drop in the stock price following the earnings release indicates investors may have expected more robust results or raised guidance.

According to the previous quarter’s earnings report, ACM Research had exceeded expectations with Q1 2025 EPS of $0.46 compared to the forecasted $0.3186. The sequential decline in EPS from $0.46 in Q1 to $0.44 in Q2, coupled with the significant year-over-year drop in operating income, likely contributed to today’s negative market reaction despite the continued revenue growth.

As semiconductor equipment demand fluctuates amid geopolitical tensions and industry cycles, ACM Research’s strategy of product diversification and geographic expansion will be crucial for achieving its ambitious long-term growth targets while navigating near-term challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.