Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

AdaptHealth Corp. (NASDAQ:AHCO) released its Q1 2025 financial results presentation on May 6, 2025, revealing significant declines in revenue and profitability metrics compared to both the previous quarter and the same period last year. Despite these challenges, the company’s stock jumped 13.22% in premarket trading to $9.85, suggesting investors may have anticipated even worse results or found positive elements in the company’s outlook.

The home healthcare equipment provider has been working to address operational challenges in its diabetes segment that were highlighted in previous earnings calls, while focusing on debt reduction and operational improvements across its business lines.

Quarterly Performance Highlights

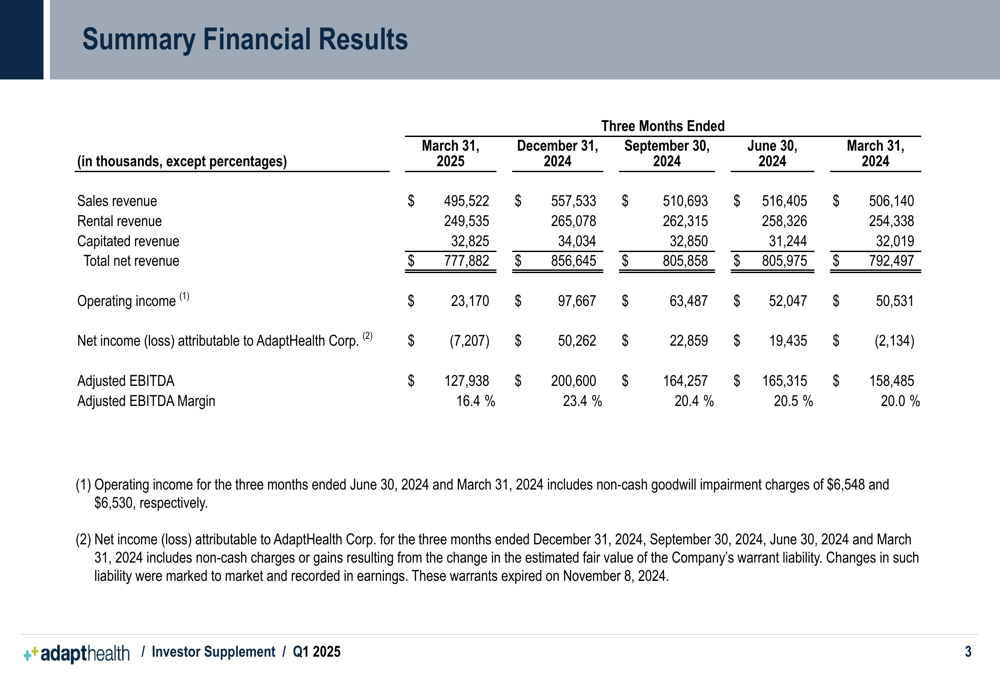

AdaptHealth reported total net revenue of $777.9 million for Q1 2025, representing a 9.2% decrease from $856.6 million in Q4 2024 and a 1.8% decline from $792.5 million in Q1 2024. The company’s operating income saw a dramatic drop to $23.2 million, down 76.3% from $97.7 million in the previous quarter and 54.1% from $50.5 million in the year-ago period.

The company reported a net loss of $7.2 million attributable to AdaptHealth Corp., compared to a profit of $50.3 million in Q4 2024 and a smaller loss of $2.1 million in Q1 2024. This translated to a basic net loss per share of $(0.05) compared to $(0.02) in the same quarter last year.

As shown in the following summary of financial results:

Adjusted EBITDA, a key metric for the company, fell to $127.9 million in Q1 2025 from $200.6 million in Q4 2024 and $158.5 million in Q1 2024. The adjusted EBITDA margin contracted significantly to 16.4% from 23.4% in the previous quarter and 20.0% in the year-ago period, indicating increased pressure on the company’s operational efficiency.

Business Mix Analysis

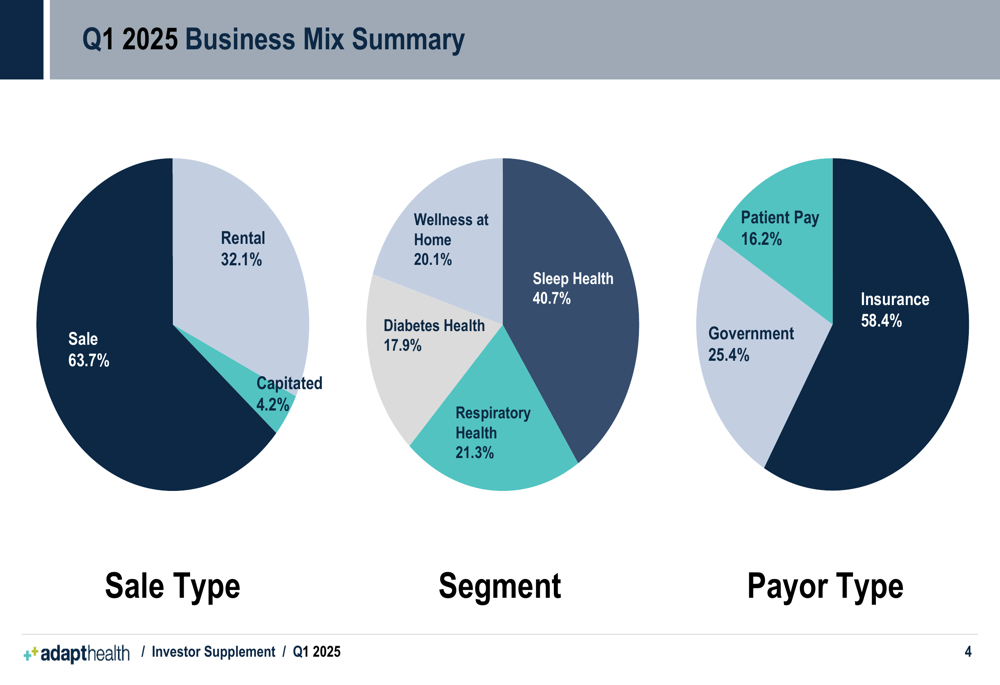

AdaptHealth’s business is diversified across multiple segments and revenue types. The company’s Q1 2025 revenue was primarily derived from product sales (63.7%), with rental revenue accounting for 32.1% and capitated arrangements contributing 4.2%.

By segment, Sleep Health remains the largest contributor at 40.7% of total revenue, followed by Respiratory Health at 21.3%, Wellness at Home at 20.1%, and Diabetes Health at 17.9%. The company’s payor mix is dominated by insurance (58.4%), with government payers accounting for 25.4% and patient pay representing 16.2%.

The following chart illustrates AdaptHealth’s business mix for Q1 2025:

Segment Performance

All of AdaptHealth’s segments experienced revenue declines in Q1 2025 compared to Q4 2024, with the most significant drops in Sleep Health and Diabetes Health. Sleep Health revenue fell to $316.4 million from $356.5 million in the previous quarter, while Diabetes Health revenue declined to $138.8 million from $171.3 million.

The continued challenges in the Diabetes Health segment align with issues highlighted in the company’s Q3 2024 earnings call, where management noted reimbursement pressures and operational challenges that led to an 11.8% decline in diabetes revenue. These problems appear to have persisted into 2025.

Respiratory Health showed the most stability, with revenue holding relatively steady at $165.5 million compared to $165.3 million in Q4 2024. This segment has historically been a bright spot for the company, with the Q3 2024 earnings call noting an 8.6% increase in respiratory revenue at that time.

Revenue Growth Trends

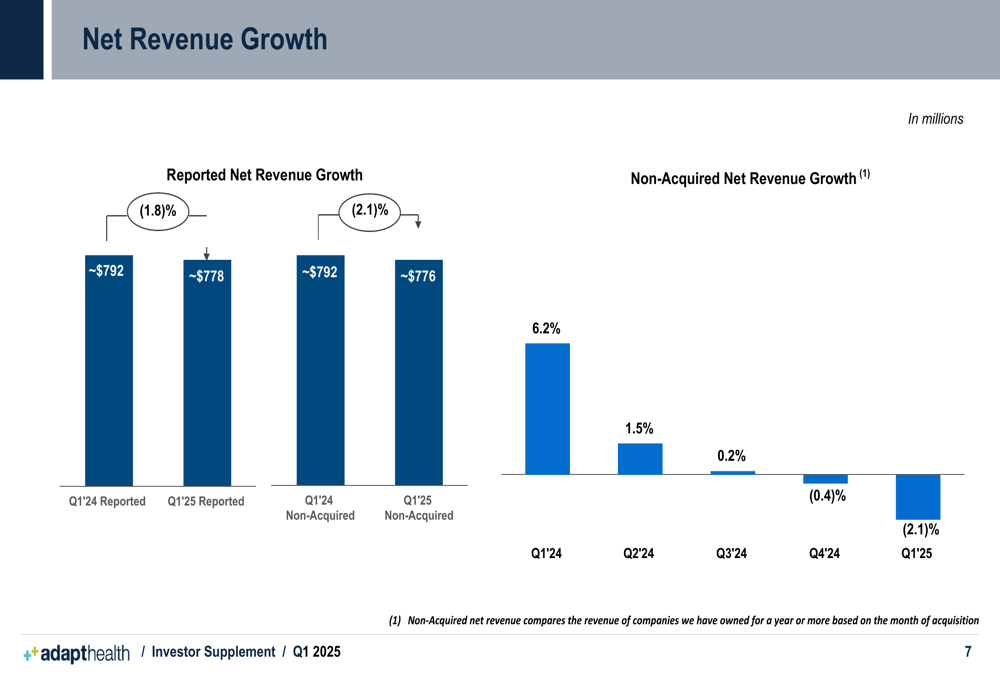

AdaptHealth’s revenue growth has been on a concerning downward trajectory. The company’s reported net revenue declined by 1.8% year-over-year in Q1 2025, while non-acquired revenue (representing organic growth) fell by 2.1%.

This represents a significant deterioration from the company’s growth profile a year ago, when it reported 6.2% non-acquired revenue growth in Q1 2024. The following chart illustrates this declining growth trend:

Debt and Cash Flow Analysis

AdaptHealth’s financial position shows some concerning trends in cash flow generation. The company reported negative free cash flow of $58,000 in Q1 2025, a significant deterioration from positive free cash flow in previous quarters. This decline was driven by capital expenditures of $95.6 million that nearly matched operating cash flow of $95.5 million.

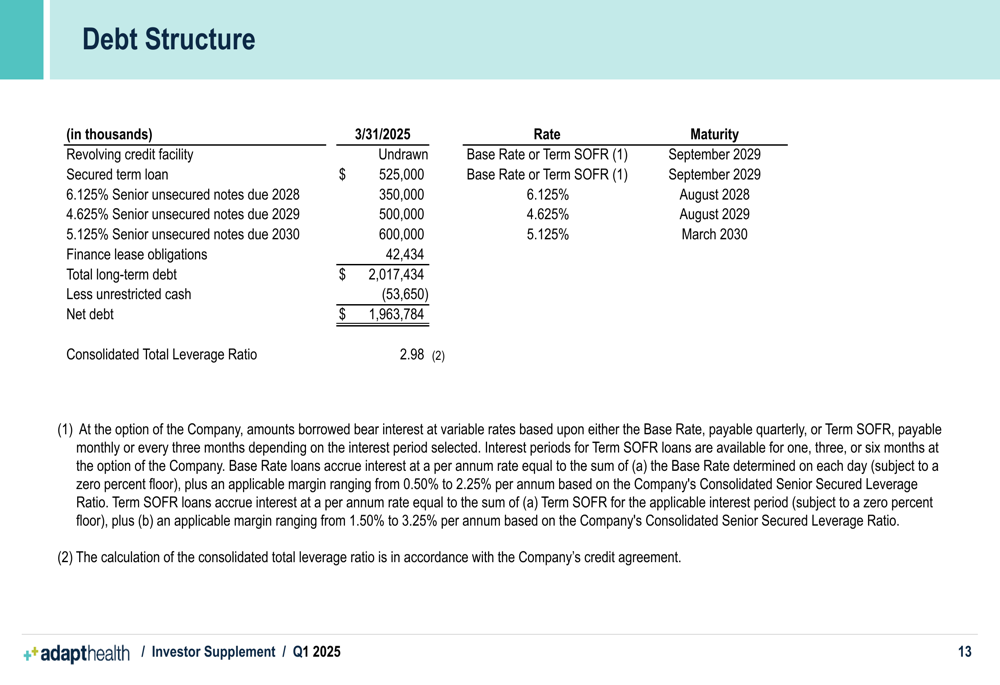

The company’s debt structure as of March 31, 2025, includes:

Total (EPA:TTEF) long-term debt stood at $2.02 billion, with net debt (after subtracting unrestricted cash) at $1.96 billion. The company’s debt includes a secured term loan of $525 million and various senior unsecured notes totaling $1.45 billion with maturities ranging from 2028 to 2030.

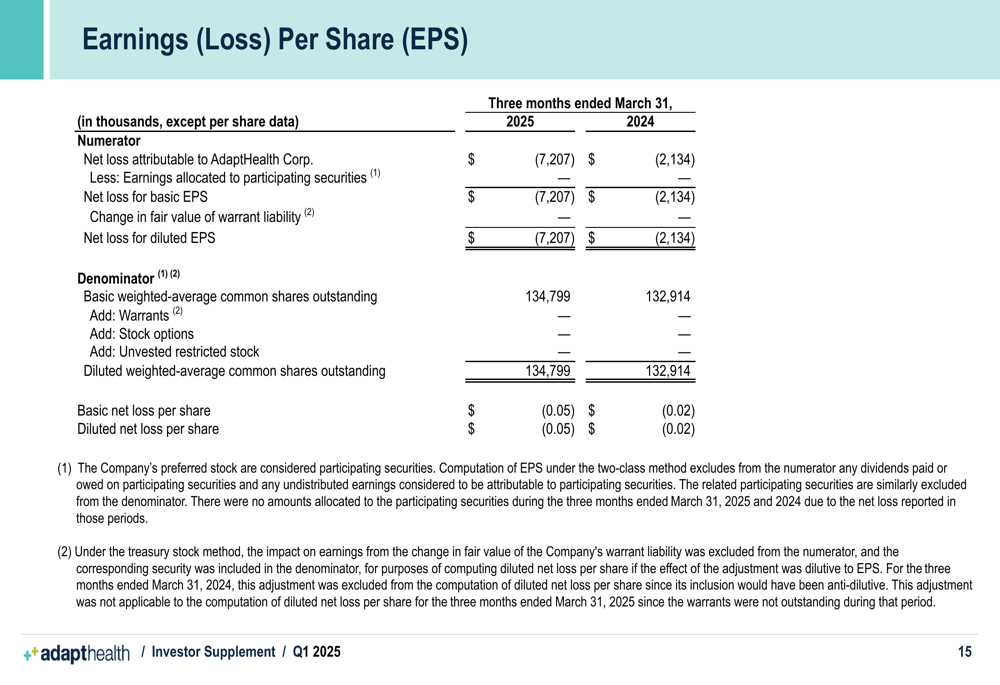

Earnings Per Share

AdaptHealth’s loss per share widened in Q1 2025 compared to the same period last year. The company reported a basic net loss per share of $(0.05), compared to $(0.02) in Q1 2024. Diluted net loss per share followed the same pattern.

The following table details the company’s earnings per share calculations:

Forward-Looking Statements

While the Q1 2025 presentation did not include specific forward guidance, the company’s performance suggests continued challenges ahead, particularly in the diabetes segment. In its Q3 2024 earnings call, AdaptHealth had raised its full-year 2024 guidance, projecting revenue between $3.22 billion and $3.26 billion and adjusted EBITDA between $655 million and $675 million.

However, the significant decline in revenue and profitability metrics in Q1 2025 raises questions about the company’s ability to maintain growth momentum. The negative free cash flow is particularly concerning given management’s stated focus on debt reduction.

AdaptHealth’s management had previously outlined a strategy focused on operational improvements and debt reduction, with limited acquisition activity in the near term. The effectiveness of these initiatives will be closely watched by investors in the coming quarters as the company works to address the challenges evident in its Q1 2025 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.