Trump says envoy Witkoff had productive meeting with Putin

Introduction & Market Context

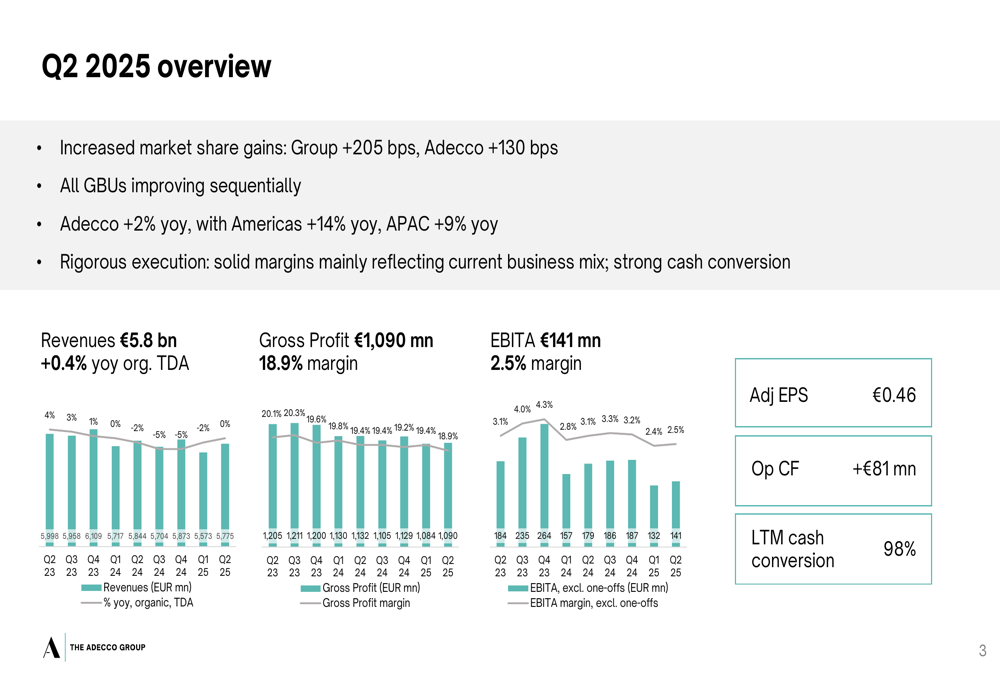

Adecco Group (SWX:SIX:ADEN) reported modest revenue growth in its Q2 2025 financial results presentation on August 5, highlighting significant market share gains across its business units. The staffing and HR solutions provider achieved revenues of €5.8 billion, representing a 0.4% year-over-year organic increase, while outperforming competitors by 205 basis points.

CEO Denis Machuel and CFO Coram Williams emphasized the company’s ability to capture market share amid varying regional conditions, with particularly strong performance in the Americas and Asia-Pacific regions offsetting challenges in Europe and the Akkodis business unit.

Quarterly Performance Highlights

Adecco Group delivered solid financial results in Q2 2025, maintaining stable profitability despite a challenging business mix. The company reported gross profit of €1,090 million with an 18.9% margin, while EBITA reached €141 million, representing a 2.5% margin. Adjusted earnings per share stood at €0.46, with operating cash flow of €81 million and last twelve months cash conversion at a robust 98%.

As shown in the following overview of key financial metrics:

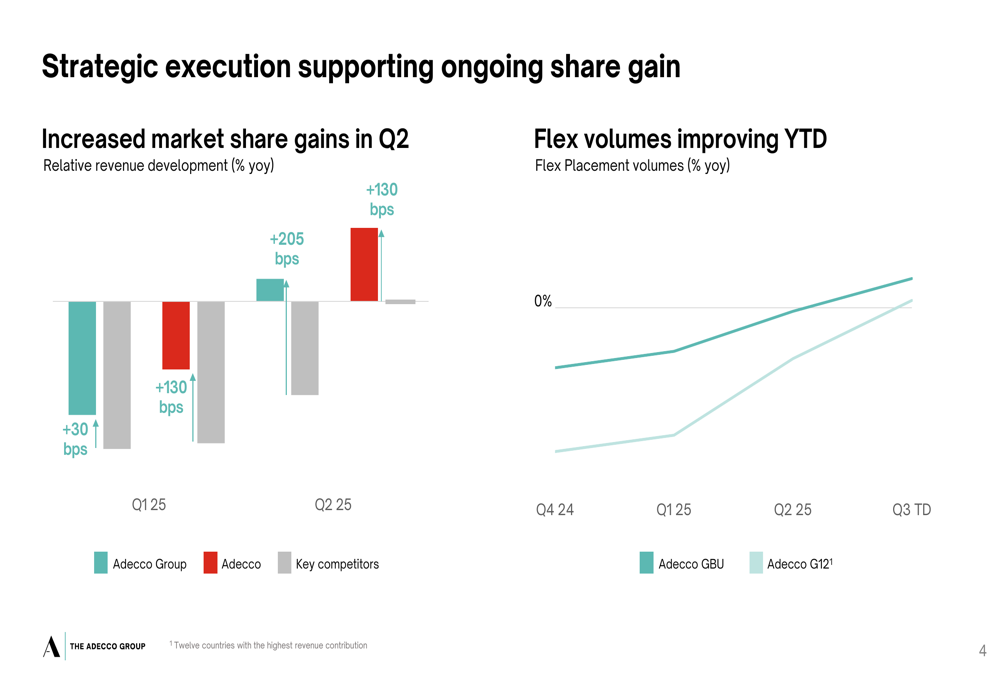

The company’s market share gains were particularly notable, with the Group outperforming competitors by 205 basis points and the Adecco business unit specifically gaining 130 basis points. This performance contrasts sharply with negative growth reported by key competitors, as illustrated in the strategic execution slide:

Regional Performance Analysis

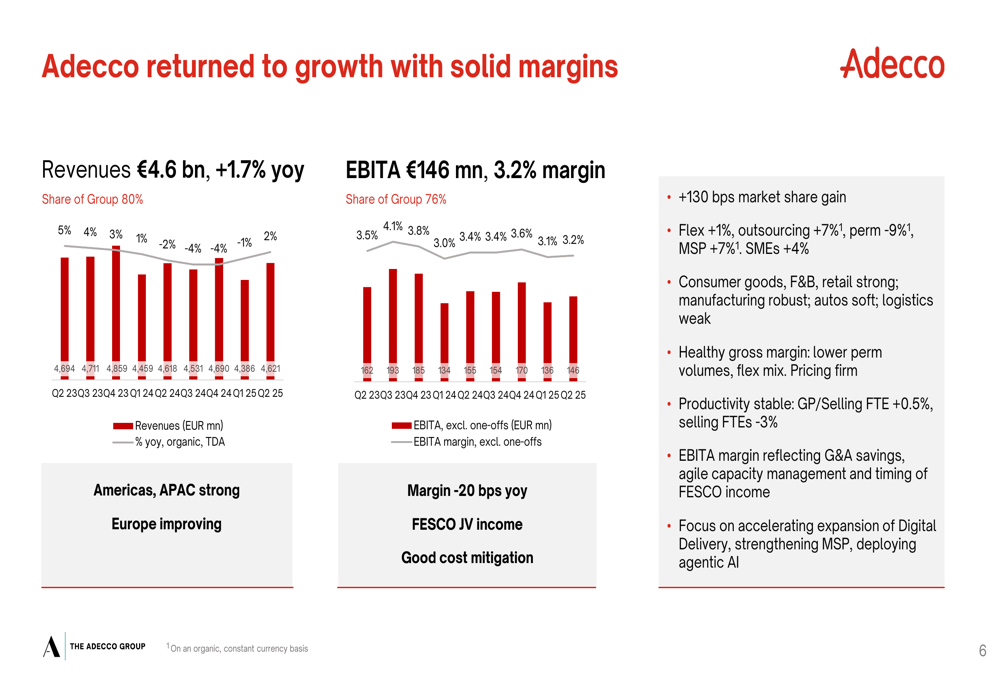

The Adecco business unit, which accounts for 80% of Group revenue, returned to growth with a 1.7% year-over-year increase to €4.6 billion. This unit delivered an EBITA of €146 million with a 3.2% margin, representing 76% of Group EBITA. Flexible staffing grew by 1%, while outsourcing increased by 7%, offsetting a 9% decline in permanent placement.

The following chart illustrates Adecco’s return to growth and solid margins:

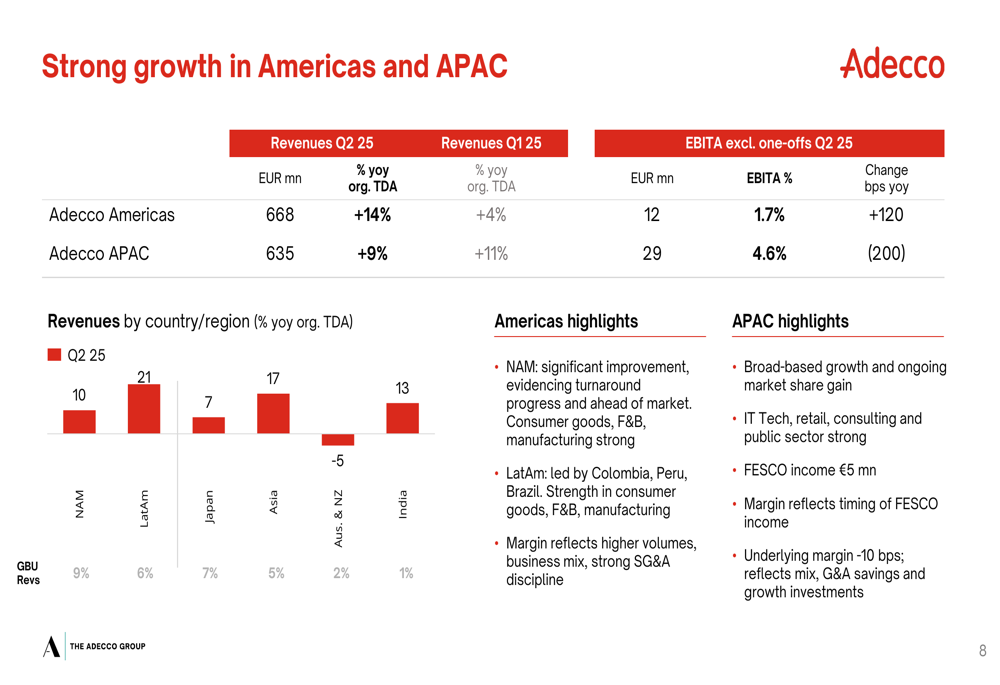

Regional performance varied significantly, with the Americas and Asia-Pacific regions driving growth while Europe showed sequential improvement. Adecco Americas delivered impressive 14% year-over-year organic growth to €668 million, while Adecco APAC grew 9% to €635 million. Within these regions, Latin America stood out with 21% growth, followed by Asia at 17%, India at 13%, and Japan at 7%.

The regional breakdown of strong growth in Americas and APAC is shown here:

European operations showed signs of improvement but remained mixed. Adecco France reported revenues of €1,127 million, down 4% year-over-year, while Adecco EMEA excluding France remained flat at €2,191 million. The company noted robust performance in food and beverage, retail, and construction sectors across Europe.

Strategic Initiatives & Business Unit Performance

Adecco highlighted several strategic client wins that leverage the Group’s digital expertise, scale, and breadth of solutions. These included a global OEM using AI-driven recruiting for EV battery manufacturing, a global consulting company selecting Adecco as a preferred supplier for permanent recruitment, and a French defense leader partnering with Akkodis for strategic transformation.

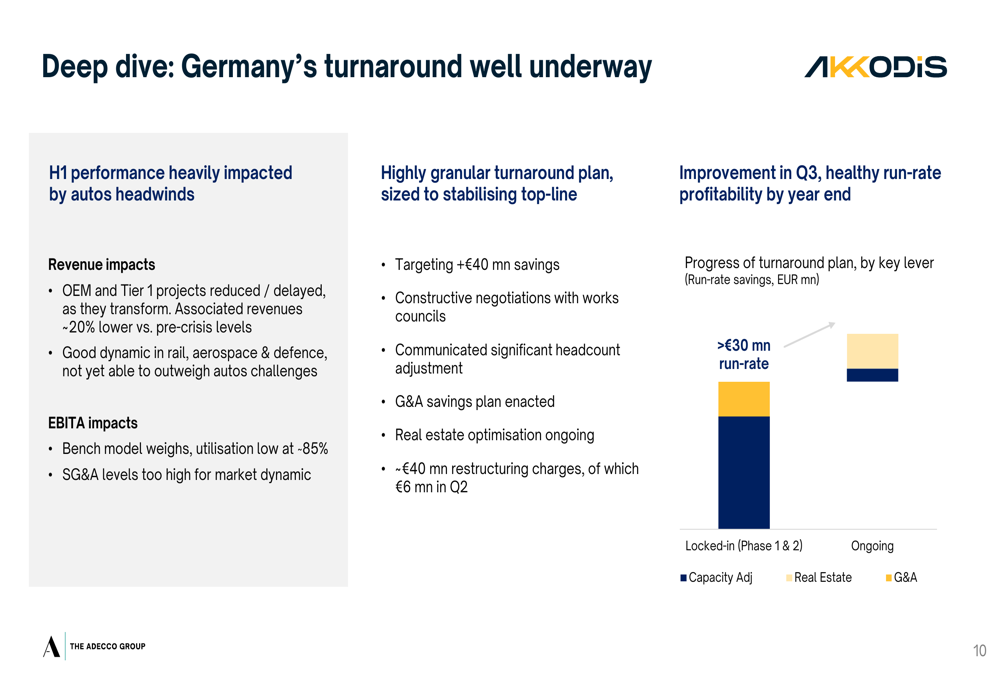

The Akkodis business unit, focused on technology consulting, faced challenges with revenues declining 6% year-over-year to €835 million and EBITA falling to €13 million (1.6% margin). Germany’s performance was particularly weak, down 14% due to automotive sector headwinds affecting OEM and Tier 1 projects.

Management detailed a comprehensive turnaround plan for Akkodis Germany:

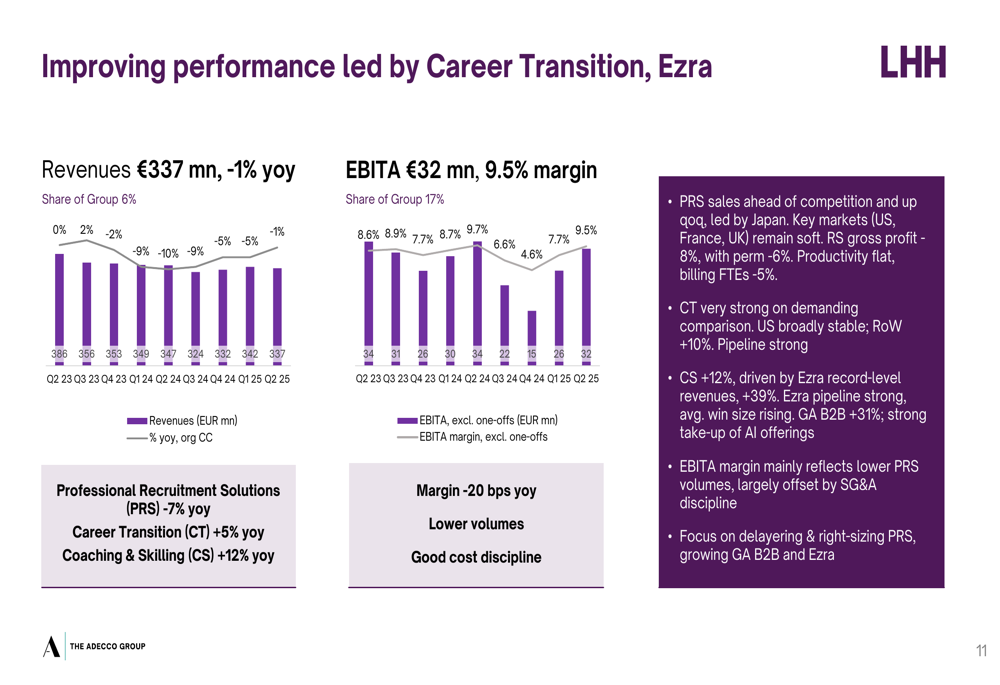

Meanwhile, the LHH business unit showed improving performance led by Career Transition and Ezra coaching services. LHH revenues were €337 million, down 1% year-over-year, but EBITA remained strong at €32 million with a 9.5% margin. Career Services grew by 12%, driven by Ezra’s record-level revenues increasing 39%.

Financial Structure & Outlook

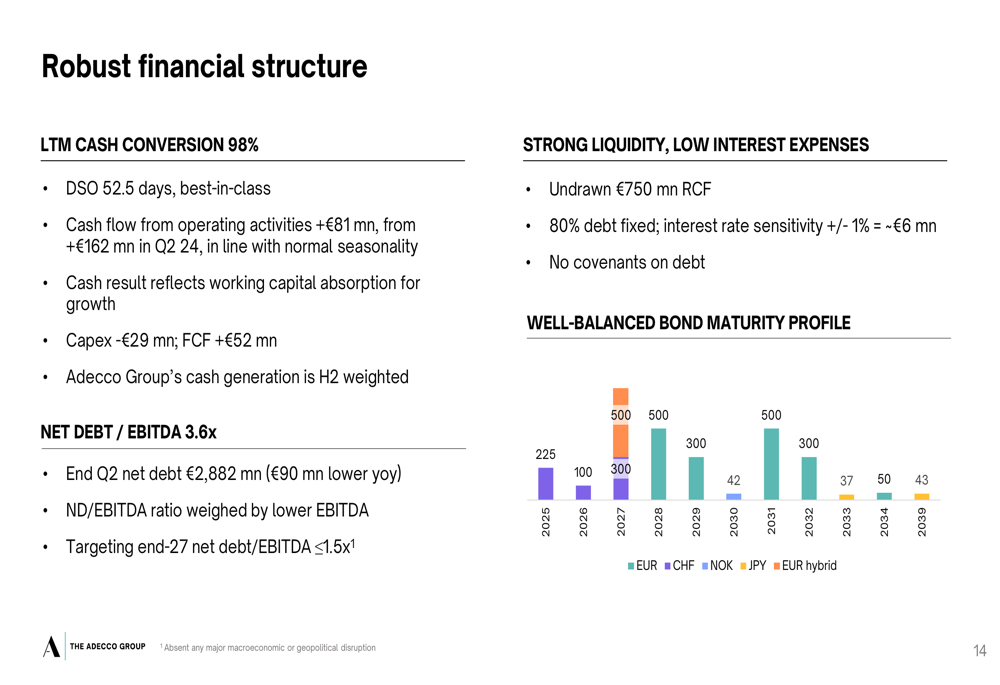

Adecco maintained a robust financial structure with strong liquidity, including an undrawn €750 million revolving credit facility. The company’s net debt to EBITDA ratio stood at 3.6x, supported by a well-balanced bond maturity profile.

The financial structure details are illustrated here:

Looking ahead, management indicated that volumes improved through Q2 and expects gross margin to rise sequentially in Q3, in line with seasonality. The company remains focused on managing capacity with agility to balance market share gains and productivity, with profitability expected to improve from H1 levels as it progresses through H2 2025.

Adecco also announced its upcoming Capital Markets Day, scheduled for November 26, 2025, in London, where it will likely provide more details on its strategic direction and financial targets.

Key takeaways from the presentation include increased market share gains with solid margins across all business units, strong growth in Adecco US, progress in the Akkodis Germany turnaround, and continued focus on agile capacity management and cost discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.