Street Calls of the Week

Introduction & Market Context

Advanced Flower Capital Inc (NASDAQ:AFCG), the first Nasdaq-listed commercial mortgage REIT focused on providing institutional loans to state-compliant cannabis operators, presented its Q2 2025 investor update on August 14, 2025. The presentation comes amid challenging conditions for the cannabis finance sector, with AFCG’s stock trading at $4.56 as of August 13, down 4.6% for the day and significantly below its 52-week high of $10.88.

The company continues to position itself as a specialized lender in a capital-constrained industry, emphasizing its high-yield portfolio despite recent financial headwinds. This presentation follows a disappointing Q1 2025 earnings report where AFCG missed EPS forecasts by approximately 37.2%.

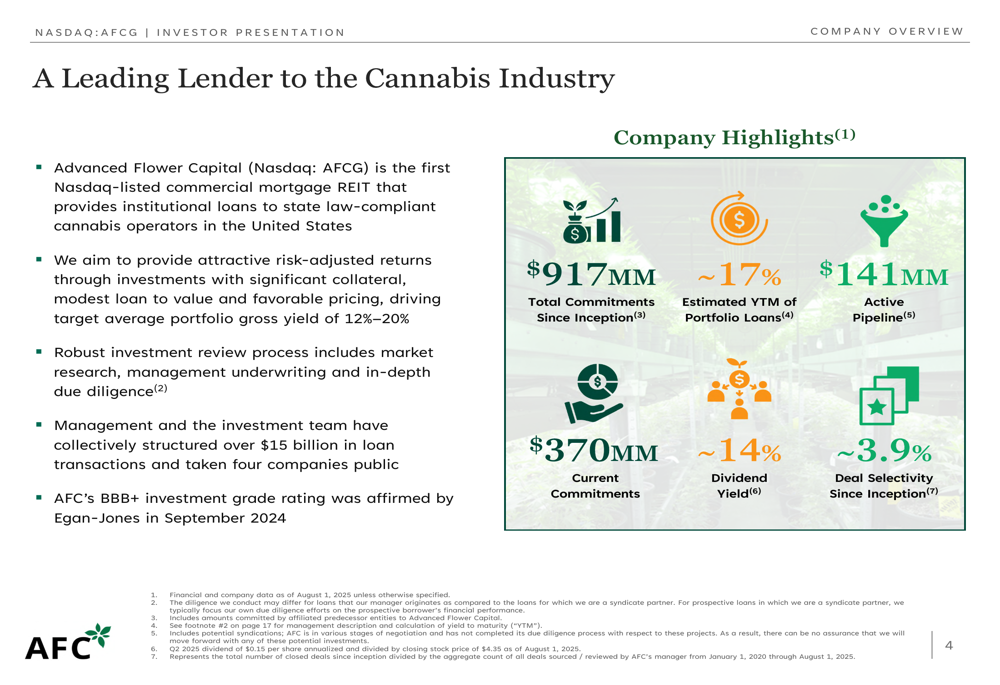

As shown in the following company overview slide, AFCG maintains substantial commitments and an attractive yield profile:

Quarterly Performance Highlights

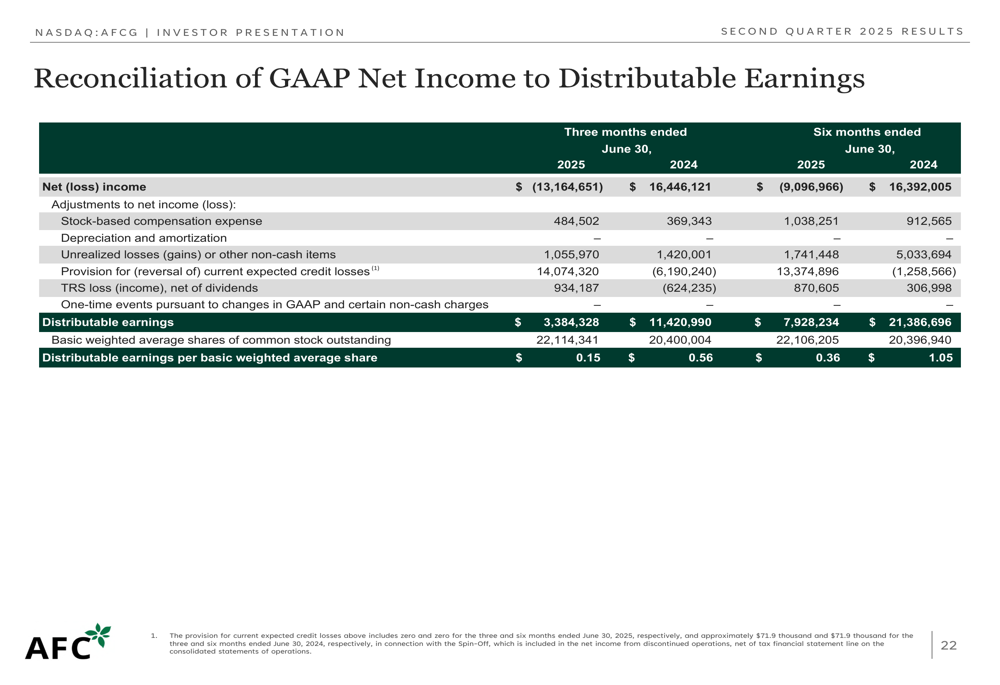

AFCG’s Q2 2025 financial results reveal mixed performance. The company reported a net loss of $(13,164,651) for the three months ended June 30, 2025, compared to net income of $5,638,520 for the same period in 2024. Despite the GAAP loss, distributable earnings totaled $3,384,328 ($0.15 per share) for the quarter.

Total assets declined to $290,589,955 as of June 30, 2025, down from $402,057,313 at the end of 2024, representing a significant 27.7% reduction. Similarly, shareholders’ equity decreased to $184,731,074 from $201,376,138 over the same period.

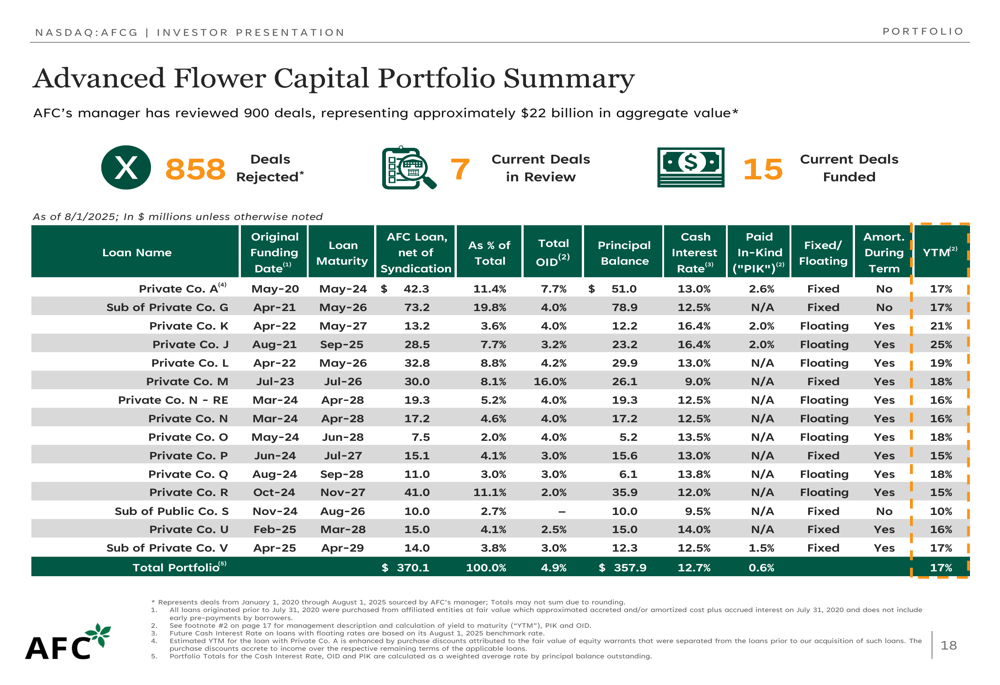

The company’s portfolio activity shows relatively stable funded commitments over recent quarters, with $360 million in funded commitments as of August 1, 2025, and an additional $10 million unfunded. The portfolio maintains a weighted average yield-to-maturity of approximately 17%.

The reconciliation between GAAP net income and distributable earnings highlights the impact of non-cash items and one-time charges affecting reported results:

Strategic Positioning

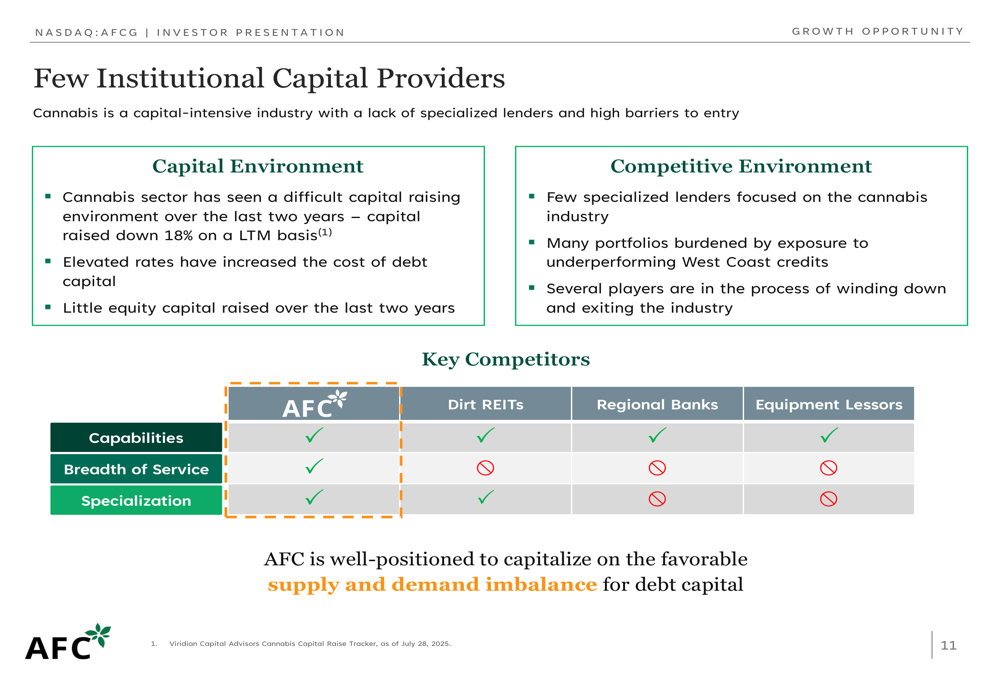

AFCG emphasizes its competitive advantage in a market with few institutional capital providers. The cannabis industry remains capital-intensive with high barriers to entry for lenders, creating what the company describes as a favorable supply-demand imbalance for debt capital.

The presentation highlights AFCG’s disciplined investment approach, noting that the company has reviewed approximately $22 billion in potential deals since inception but has only selected 3.9% of opportunities. This selectivity aligns with comments from the Q1 earnings call, where President and CIO Robin Tanenbaum stated, "We are going to be extremely selective," highlighting the cautious approach in a volatile market.

As illustrated in the following slide, AFCG positions itself as having unique capabilities compared to other potential capital sources:

Growth Opportunities

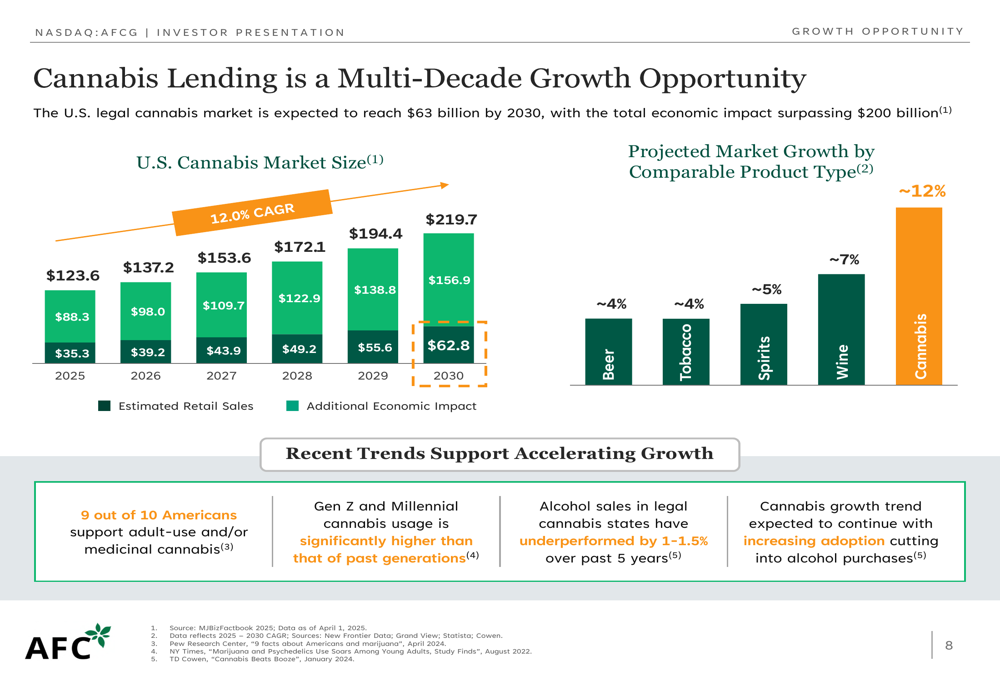

Despite near-term financial challenges, AFCG’s presentation emphasizes substantial long-term growth opportunities in cannabis lending. The U.S. legal cannabis market is projected to reach $63 billion by 2030, with a total economic impact exceeding $200 billion. The market is expected to grow at a 12% CAGR, significantly outpacing other consumer categories like beer, tobacco, and wine.

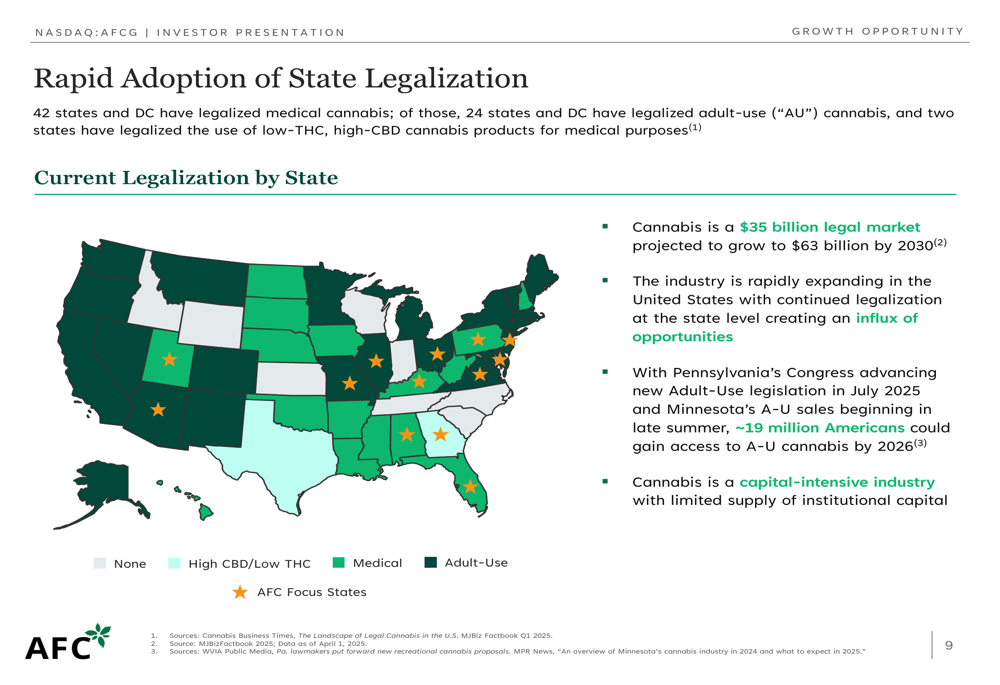

The company highlights the ongoing state-level legalization trend, with 42 states now permitting medical cannabis and 24 states allowing adult-use. This regulatory evolution is creating new capital demand, particularly as states transition from medical to adult-use markets.

The following chart illustrates the projected growth trajectory of the U.S. cannabis market:

State-level legalization continues to expand the addressable market, with AFCG identifying specific capital needs in states transitioning to adult-use (Pennsylvania, Minnesota, Ohio) and launching medical programs (Georgia, Alabama, Kentucky):

Valuation & Outlook

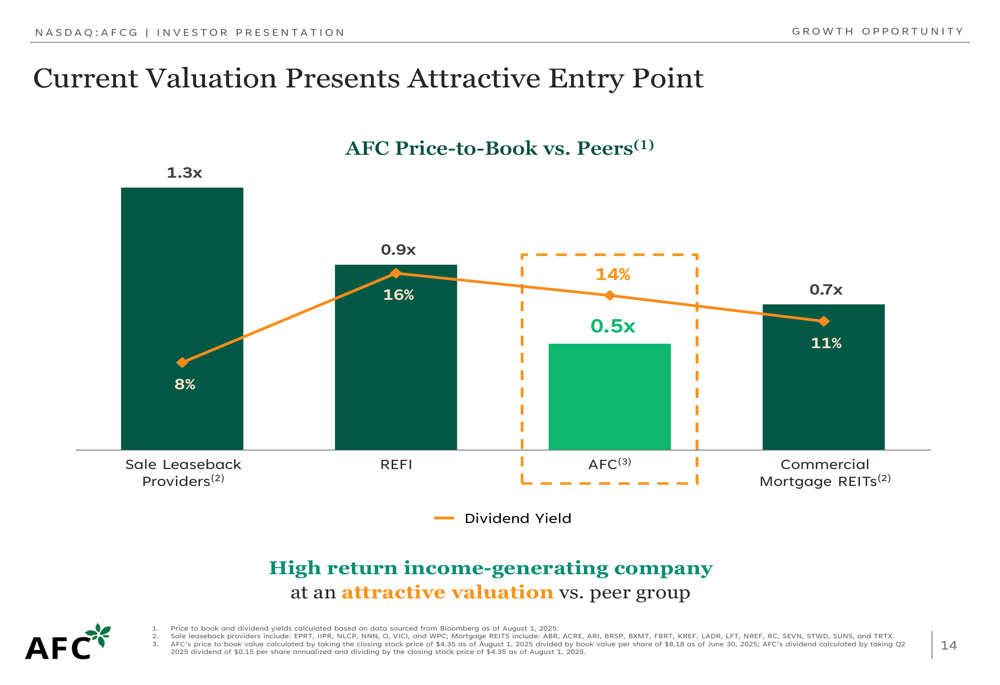

One of the most striking aspects of AFCG’s presentation is the apparent valuation disconnect. Despite maintaining a high-yield portfolio and dividend yield of approximately 14%, the stock trades at just 0.5x price-to-book value, significantly below peers in related sectors.

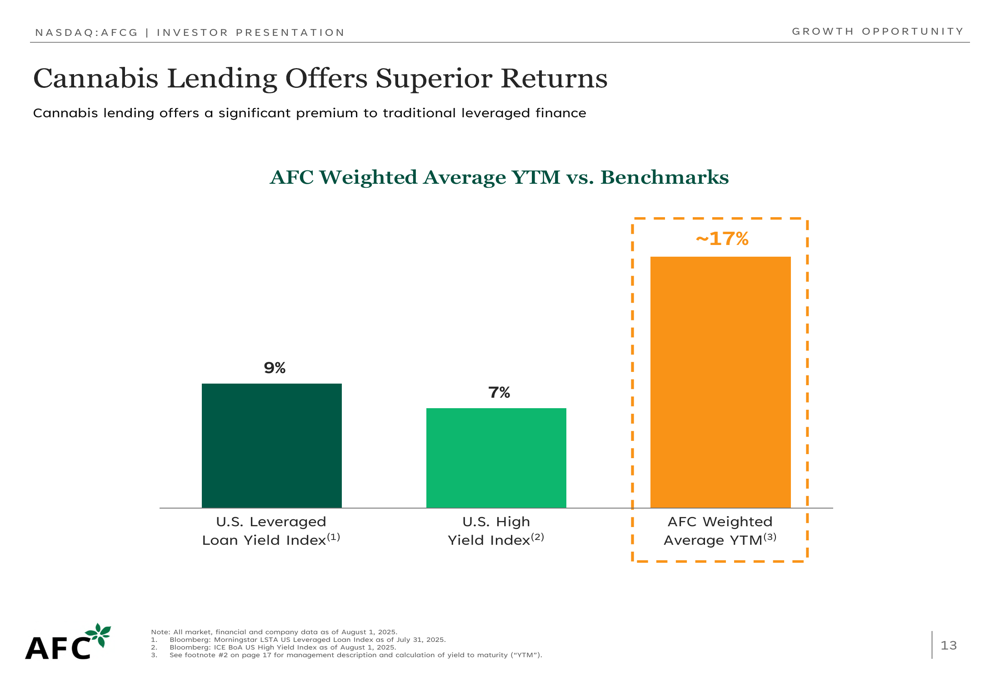

The company’s superior yield compared to traditional leveraged finance is highlighted as a key investment advantage:

However, this yield premium must be viewed in the context of increased risk and recent financial underperformance. The stock’s 32.58% decline over the past six months (noted in the Q1 earnings coverage) suggests investors remain cautious about the company’s prospects despite the attractive yield.

AFCG’s current valuation metrics compared to peers suggest potential undervaluation if the company can stabilize its financial performance:

Forward-Looking Statements

Looking ahead, AFCG anticipates 2025 will see increased M&A activity in the cannabis sector due to persistent industry fragmentation and excessive leverage across subscale businesses. The company expects to benefit from interstate expansion opportunities and the emergence of "MSO 3.0 Players" with clean capital stacks and under-leveraged asset bases.

The presentation suggests that additional medical and adult-use transitions at the state level, along with potential elimination of 280E tax provisions, could drive client ambitions and capital demand. However, these forward-looking statements should be considered alongside CEO Daniel Neville’s Q1 earnings call comment that the company is "laser focused on unlocking value from underperforming loans," indicating ongoing portfolio challenges.

AFCG’s detailed portfolio summary reveals 15 active loans with varying terms and yields, providing insight into the company’s current investment focus:

Conclusion

Advanced Flower Capital’s Q2 2025 presentation paints an optimistic picture of long-term cannabis lending opportunities while acknowledging near-term industry challenges. The company’s ability to maintain high portfolio yields of approximately 17% represents a key strength, though recent financial results suggest ongoing difficulties in translating these yields into consistent profitability.

With the stock trading near 52-week lows and at a significant discount to book value, investors appear to be weighing the attractive dividend yield against concerns about asset quality and growth prospects in a challenging cannabis finance environment. The company’s selective lending approach and focus on quality operators may provide downside protection, but could also limit growth potential in the near term as the cannabis industry continues its uneven maturation process.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.