Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

AdvanSix Inc . (NYSE:ASIX) released its first quarter 2025 earnings presentation on May 2, revealing a substantial year-over-year improvement across all key financial metrics. The chemical manufacturer, which operates primarily in the United States, benefited from stronger operational performance and a significant insurance settlement, helping to offset mixed market conditions across its various business segments.

The company’s shares were trading at $21.30 at the previous close, down slightly in pre-market trading by 0.94% to $21.10. The stock has traded between $18.44 and $33.00 over the past 52 weeks, indicating some volatility in investor sentiment toward the specialty chemicals manufacturer.

Quarterly Performance Highlights

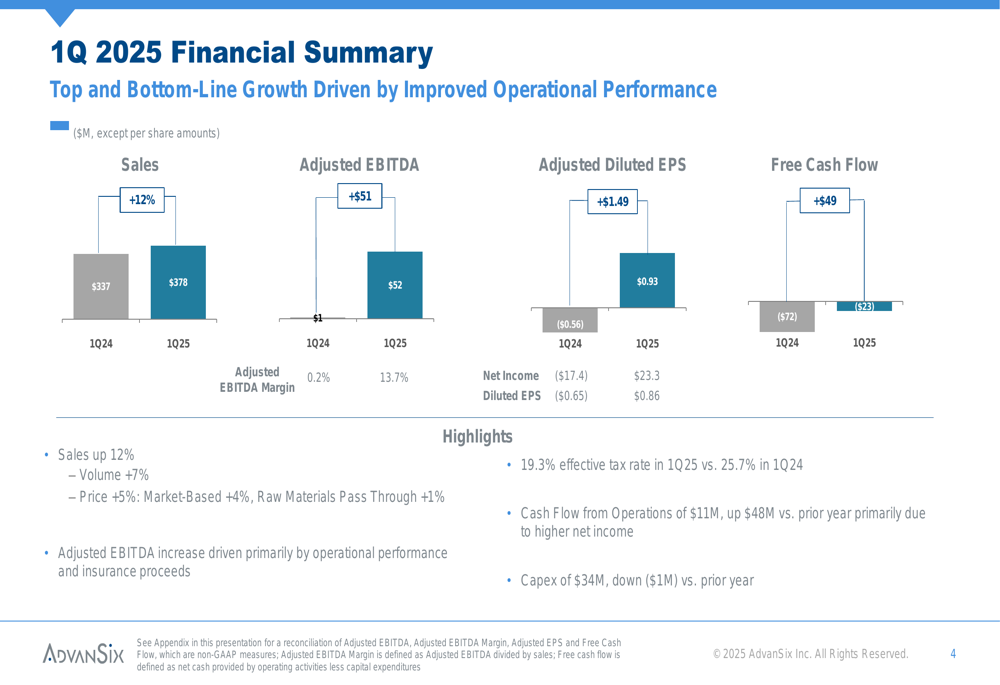

AdvanSix reported impressive financial results for Q1 2025, with sales reaching $378 million, a 12% increase from $337 million in the same period last year. This growth was driven by a 7% increase in volume and a 5% improvement in pricing, with market-based pricing contributing 4% and raw material pass-through adding 1%.

The company’s profitability metrics showed even more dramatic improvement. Adjusted EBITDA surged to $52 million from just $1 million in Q1 2024, resulting in an adjusted EBITDA margin of 13.7% compared to a mere 0.2% in the prior year period. Adjusted earnings per share reached $0.93, a substantial recovery from a loss of $0.56 per share in Q1 2024.

As shown in the following comprehensive financial summary:

The company’s net income for the quarter was $23 million, a significant turnaround from a $17 million loss in the same period last year. Cash flow from operations improved to $11 million, up $48 million from the prior year, primarily due to higher net income.

Detailed Financial Analysis

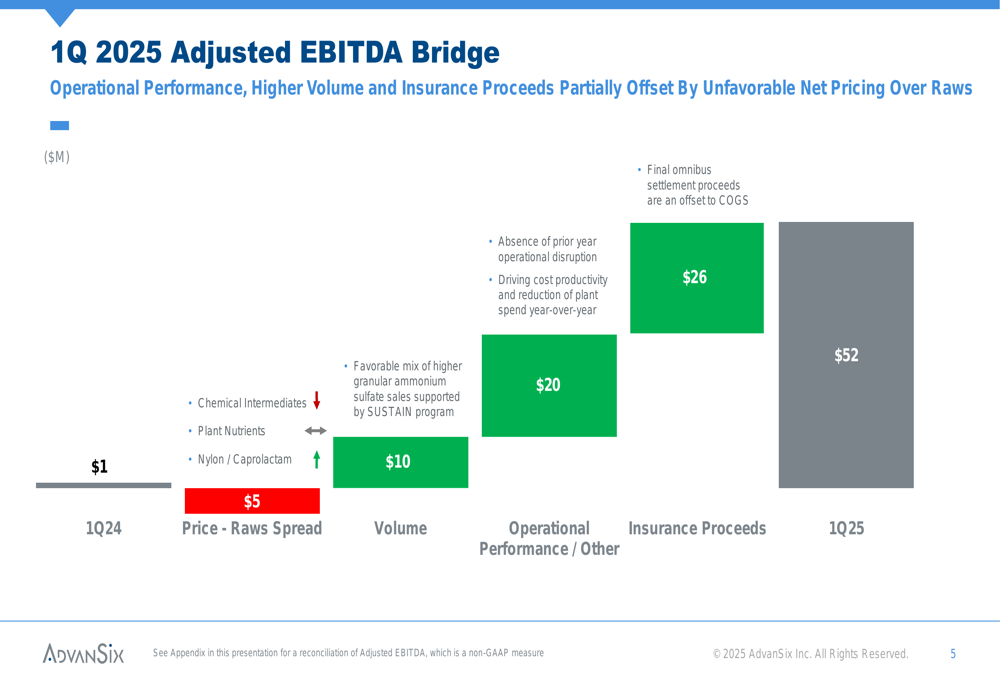

The dramatic improvement in AdvanSix’s adjusted EBITDA can be attributed to several key factors. As illustrated in the EBITDA bridge below, the $51 million year-over-year increase was driven by $10 million from higher volumes, $20 million from improved operational performance, and $26 million from insurance proceeds. These positive factors were partially offset by a $5 million headwind from price-to-raw material spread.

The insurance proceeds of approximately $26 million came from a final omnibus settlement related to the 2019 PES supplier shutdown. The operational performance improvements reflect the absence of the prior year’s disruption at the Frankford, PA site, cost productivity initiatives, reduced plant spending, and a favorable mix of higher granular ammonium sulfate sales supported by the company’s SUSTAIN program.

Free cash flow, while still negative at -$23 million, improved by $49 million compared to -$72 million in Q1 2024. Capital expenditures were $34 million, slightly down from $35 million in the prior year period.

Segment Performance & Market Outlook

AdvanSix operates across three main segments: Plant Nutrients, Nylon Solutions, and Chemical Intermediates, each facing different market dynamics.

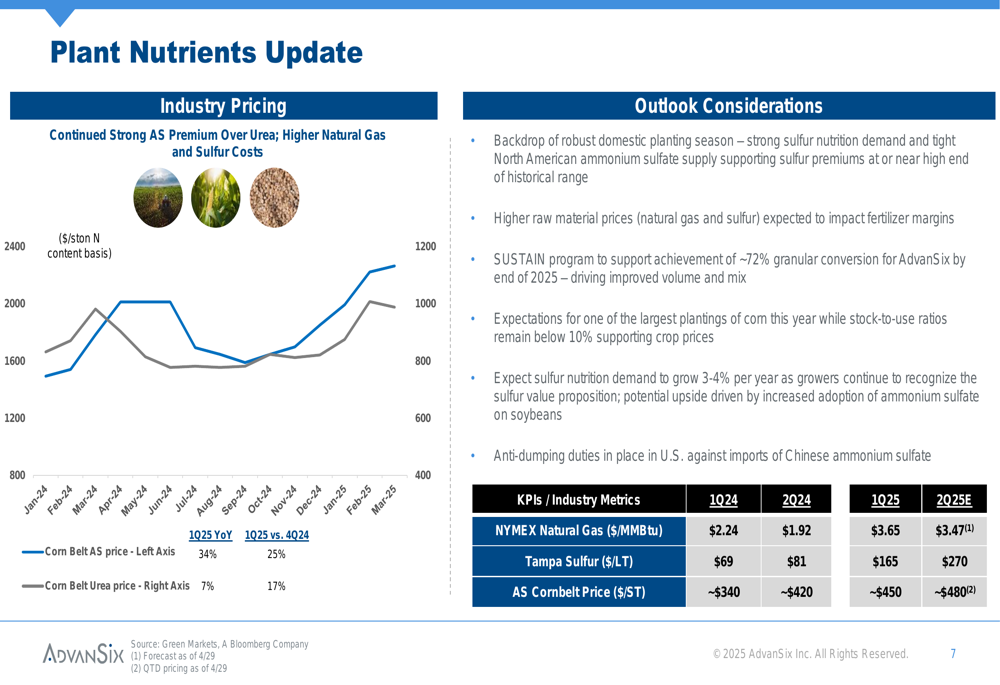

The Plant Nutrients segment is experiencing strong market conditions, with robust domestic planting season driving sulfur nutrition demand and tight North American ammonium sulfate supply. This has supported sulfur premiums at or near the high end of the historical range.

As shown in the Plant Nutrients market update:

The ammonium sulfate Corn Belt price reached approximately $450 per short ton in Q1 2025, up 34% year-over-year and 25% from Q4 2024. However, higher raw material prices, particularly natural gas (up 63% to $3.65/MMBtu) and sulfur (up 139% to $165/LT), are expected to impact fertilizer margins.

In contrast, the Nylon Solutions segment faces more challenging conditions. Global oversupply is pressuring pricing, leading to what the company describes as "a more protracted downturn in the cycle." While North American nylon demand remains stable, the company is monitoring tariff uncertainty for engineering plastics in the automotive sector.

The Chemical Intermediates segment had a soft start to the year, particularly in the large buyer segment. The acetone spread over refinery grade propylene costs is lower year-over-year but expected to remain at or above cycle averages. Acetone demand is anticipated to moderately improve in Q2 2025.

Capital Allocation Strategy

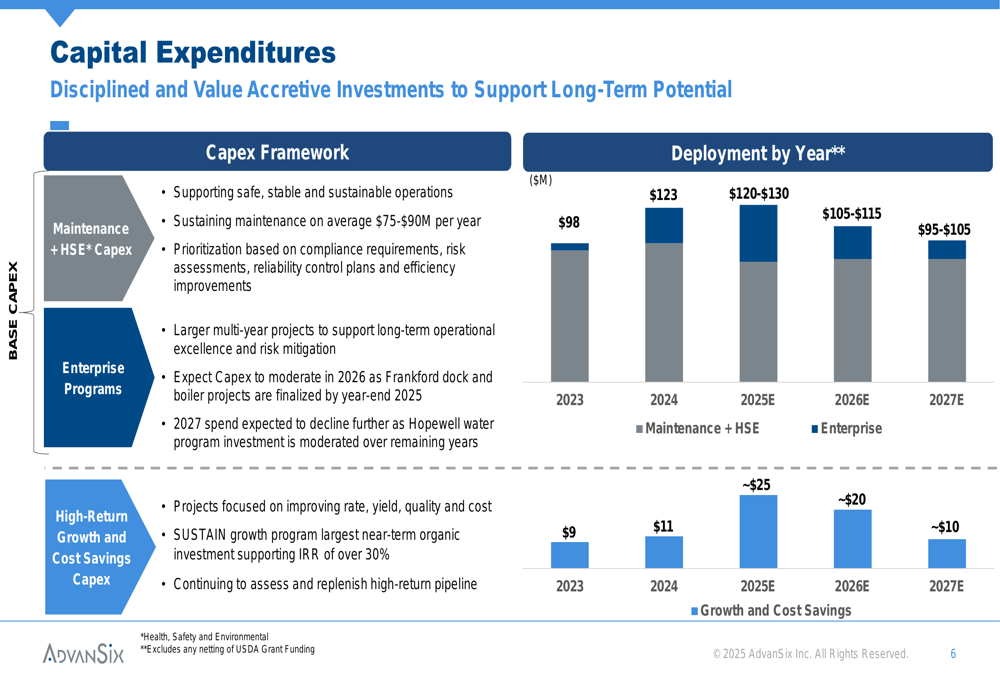

AdvanSix outlined a structured capital expenditure framework that suggests a gradual reduction in spending over the coming years. The company categorizes its capital investments into maintenance and HSE (Health, Safety, and Environment), enterprise programs, and high-return growth and cost savings initiatives.

The following chart illustrates the company’s capital expenditure plan through 2027:

Total (EPA:TTEF) capital expenditures are expected to be $145-155 million in 2025, declining to $125-135 million in 2026 and $105-115 million in 2027. This reduction is primarily due to the completion of major enterprise programs, including the Frankford dock and boiler projects by 2026 and the moderation of the Hopewell water program investment by 2027.

The company is increasing its allocation to high-return growth and cost savings projects, with approximately $25 million planned for 2025. The SUSTAIN growth program represents the largest near-term organic investment, supporting an internal rate of return of over 30%.

Forward-Looking Statements

AdvanSix provided a constructive commercial outlook, highlighting the strong sulfur nutrition demand and tight North American ammonium sulfate supply. The company expects to achieve approximately 72% granular conversion for ammonium sulfate by the end of 2025 through its SUSTAIN program.

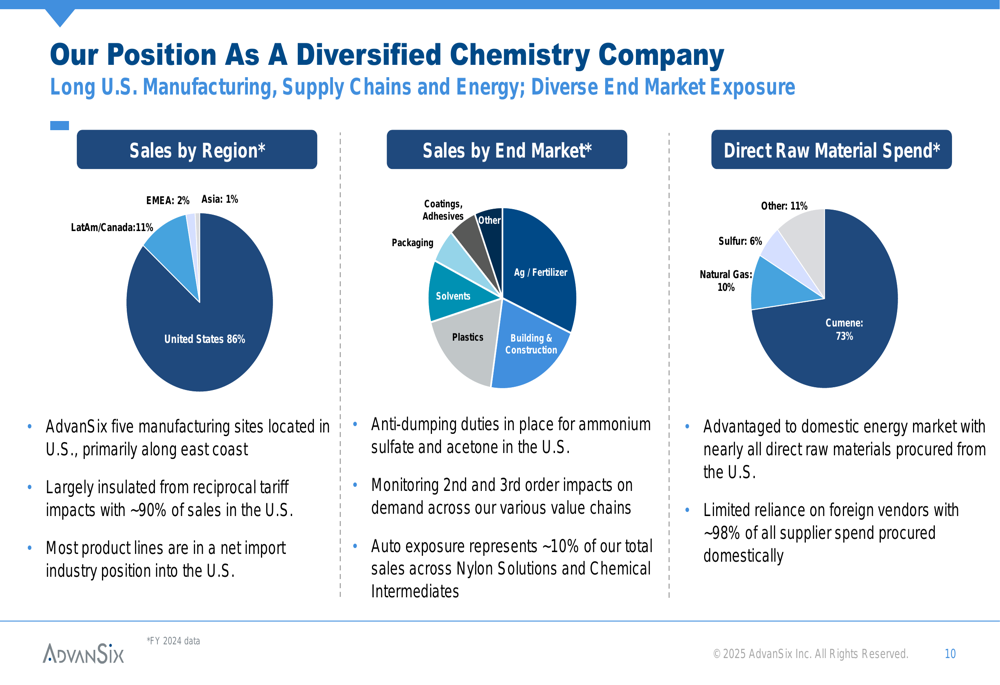

The company’s diversified business model provides some insulation from market volatility, with 86% of sales in the United States and diverse end-market exposure across industries including agriculture, automotive, building and construction, packaging, and consumer goods.

As illustrated in the following breakdown of the company’s diversification:

AdvanSix’s positioning as a domestic manufacturer with U.S.-based supply chains provides advantages in the current trade environment. The company is largely insulated from reciprocal tariff impacts, with approximately 90% of sales in the U.S. Additionally, anti-dumping duties are in place for ammonium sulfate and acetone in the U.S., providing further protection for the company’s domestic operations.

With a continued focus on operational excellence, strategic growth initiatives, and disciplined capital allocation, AdvanSix appears well-positioned to navigate the mixed market conditions while delivering improved financial performance compared to the challenging prior year period.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.