BETA Technologies launches IPO of 25 million shares priced $27-$33

Introduction & Market Context

Advantage Energy Ltd. (TSX:AAV) unveiled its May 2025 investor presentation outlining the company’s strategic direction following a disappointing Q4 2024 earnings report. The Canadian energy producer, which missed EPS forecasts by 57% in March, is positioning itself as "A Progressive Montney Producer for the New Energy Market" with a dual focus on conventional production growth and carbon capture initiatives.

The company’s stock has recovered somewhat since the earnings miss, trading at $9.79 as of May 1, 2025, up 1.33% on the day and well above its 52-week low of $7.81, though still below its high of $11.73.

Advantage’s presentation emphasizes its first principles of converting energy to shareholder wealth through exceptional performance, highlighting its concentrated high-quality assets, operational excellence, prudent financial management, and leadership in carbon capture and storage.

Resource Base and Infrastructure

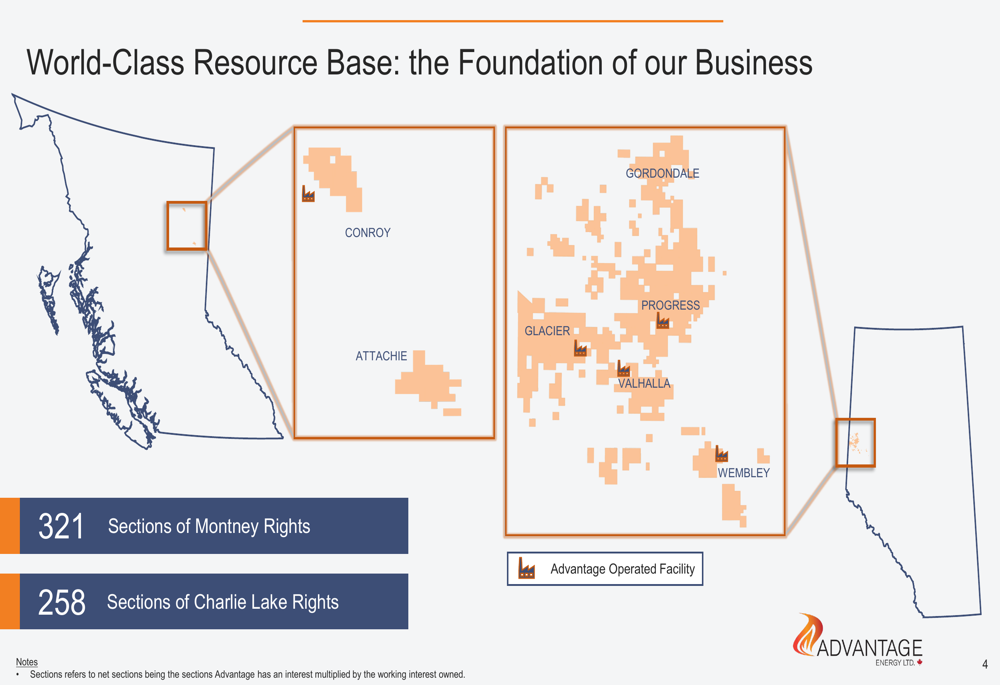

Advantage Energy boasts a substantial resource base across Western Canada, with 321 sections of Montney rights and 258 sections of Charlie Lake rights. The company’s presentation maps show its strategic positioning across key production areas including Gordondale, Progress, Glacier, Attachie, Valhalla, and Wembley.

As shown in the following detailed map of the company’s land holdings and resource base:

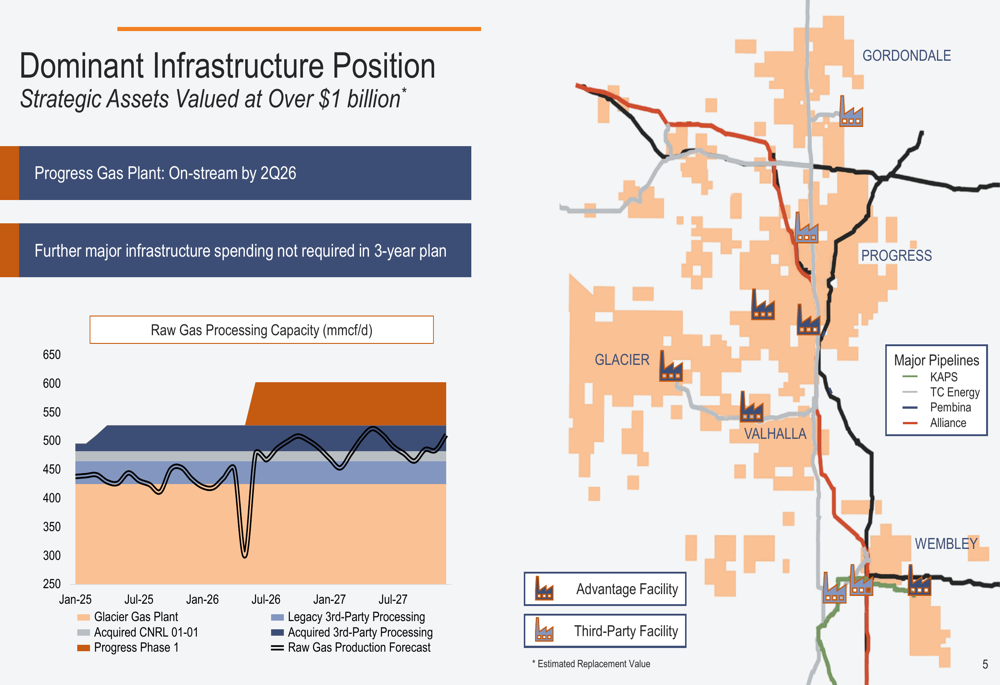

The company has built what it describes as a "dominant infrastructure position" valued at over $1 billion, with the Progress Gas Plant expected to come online by Q2 2026. According to the presentation, Advantage will not require further major infrastructure spending in its three-year plan beyond what’s already allocated.

The following chart illustrates the company’s raw gas processing capacity expansion plans through mid-2027:

Financial Position and Performance

Despite the recent earnings miss, Advantage Energy presents a relatively strong financial foundation with a market capitalization of $1.7 billion, net debt of $0.6 billion (aligning with the $626 million reported in Q4 results), and an enterprise value of $2.3 billion. The company has repurchased $384 million worth of shares (38.2 million shares) since 2022, representing approximately 20% of shares outstanding.

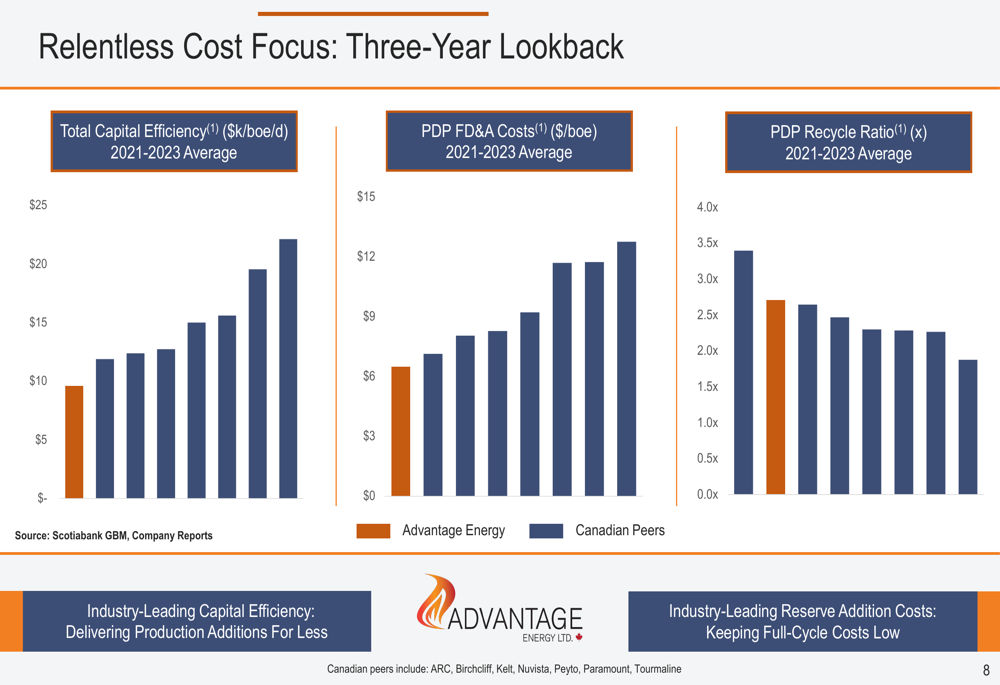

Advantage Energy emphasizes its cost efficiency compared to Canadian peers. The following chart shows the company’s three-year average (2021-2023) performance in total capital efficiency, PDP FD&A costs, and PDP recycle ratio:

Strategic Initiatives and Three-Year Plan

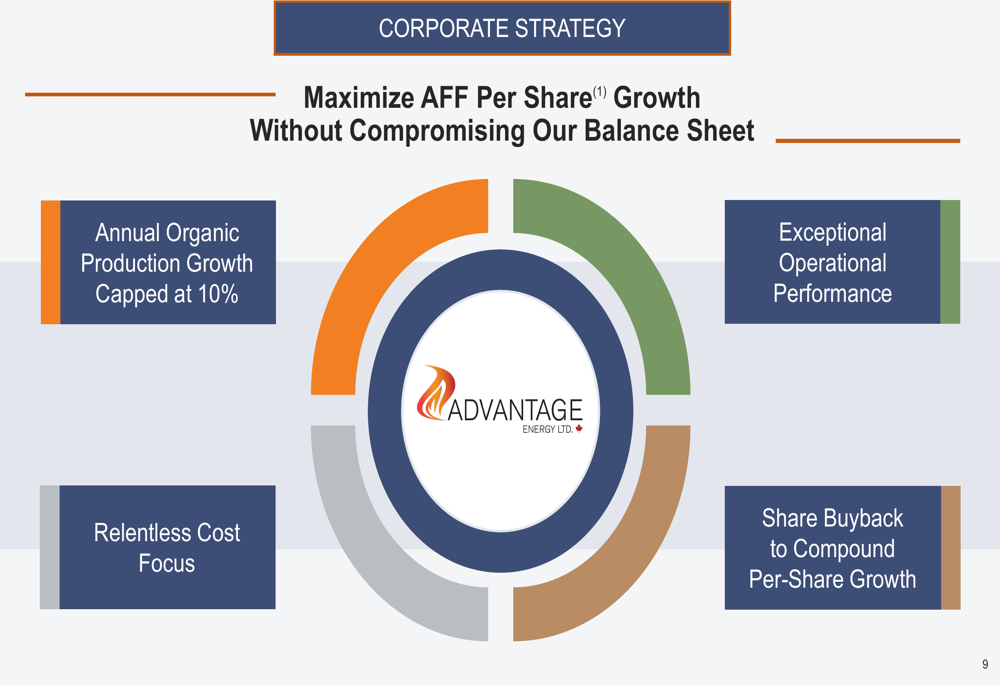

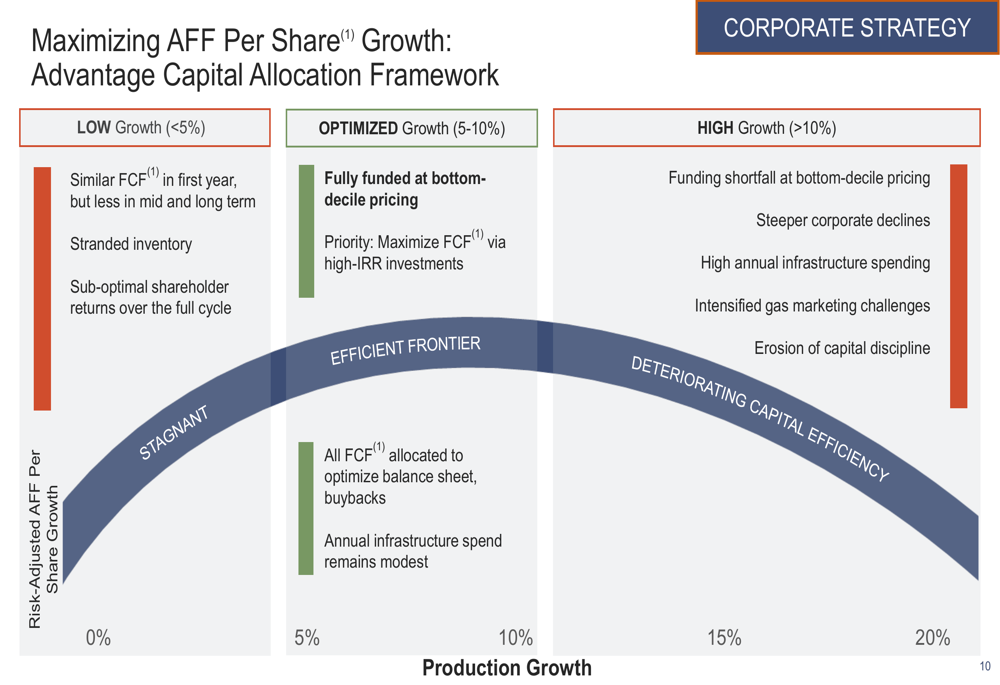

The company’s corporate strategy centers on maximizing adjusted funds flow (AFF) per share growth without compromising its balance sheet. This approach includes capping annual organic production growth at 10%, maintaining a relentless cost focus, driving exceptional operational performance, and using share buybacks to compound per-share growth.

Advantage’s capital allocation framework targets what it calls "optimized growth" of 5-10%, which it believes balances free cash flow generation with sustainable development. The company argues that lower growth would strand inventory and reduce shareholder returns, while higher growth would create funding shortfalls at bottom-decile pricing and erode capital discipline.

The three-year strategic plan projects production growth from 80,000-83,000 boe/d in 2025 to approximately 95,000 boe/d by 2027, with capital expenditures expected to reach around $350 million in 2027. The company notes that the Glacier Plant will undergo a turnaround in 2026, taking 425 mmcf/d offline for 17 days.

Well Economics and Asset Performance

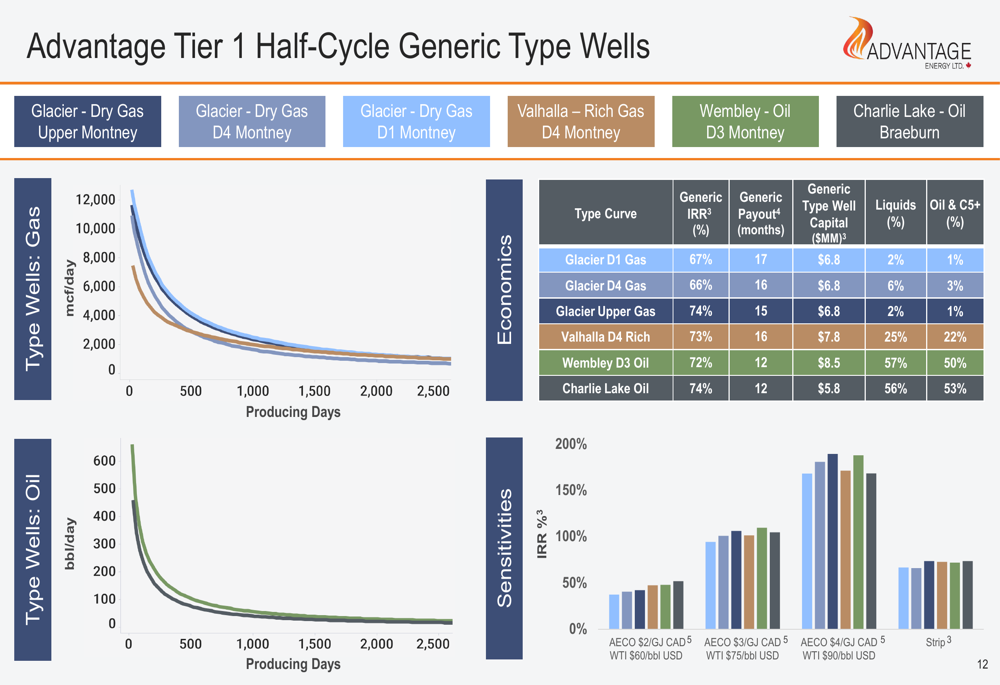

Advantage Energy’s presentation highlights the economics of its Tier 1 half-cycle generic type wells across various formations. The company provides detailed breakdowns of IRR percentages, payout periods, capital requirements, and liquids percentages for each well type, along with sensitivity analyses based on AECO and WTI prices.

The following comprehensive chart details the economic performance of the company’s various well types:

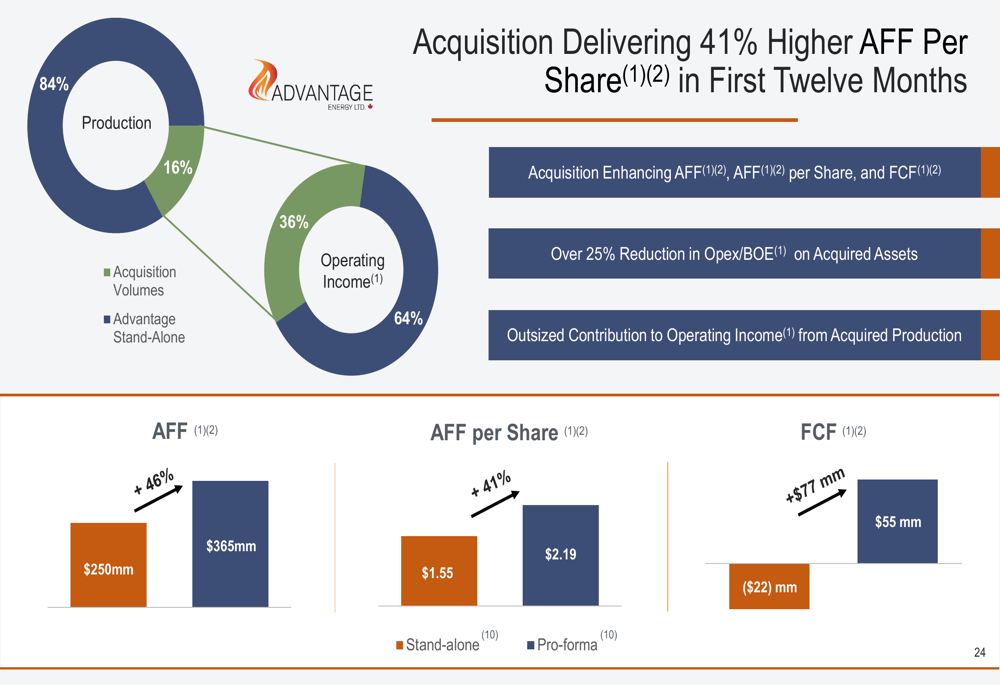

The company’s recent acquisition is projected to deliver significant financial benefits, with a claimed 41% higher AFF per share in the first twelve months. According to the presentation, the acquisition is enhancing AFF, AFF per share, and FCF, with over 25% reduction in operating expenses per BOE on acquired assets.

Financial Outlook

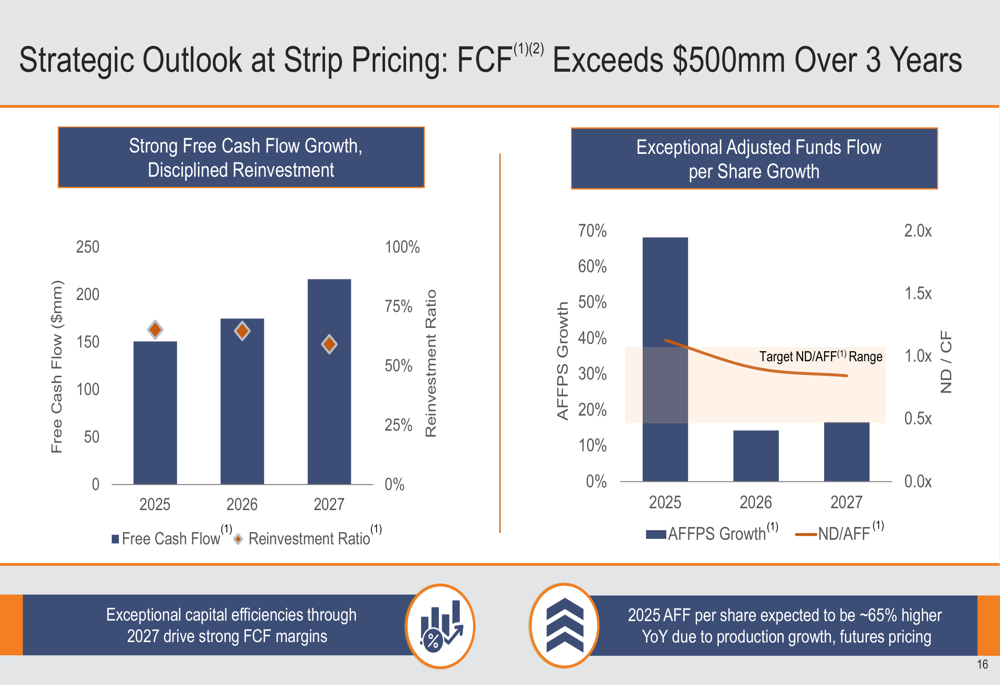

Advantage Energy projects strong free cash flow growth over its three-year plan, with FCF expected to increase from approximately $150 million in 2025 to $200 million in 2027. Simultaneously, the company aims to reduce its reinvestment ratio from 75% to 50%.

The following chart illustrates the projected financial performance through 2027:

For 2025, the company’s budget guidance includes:

- Cash used in investing activities: $270-300 million

- Total (EPA:TTEF) production: 80,000-83,000 boe/d

- Natural gas percentage: 84-85%

- Crude oil and condensate percentage: 11-12%

- Operating expense: $5.20-5.90/boe

- Transportation expense: $3.95-4.25/boe

This guidance comes despite the Q4 2024 earnings miss, suggesting management remains confident in its operational capabilities despite recent financial underperformance.

Carbon Capture and Storage Strategy

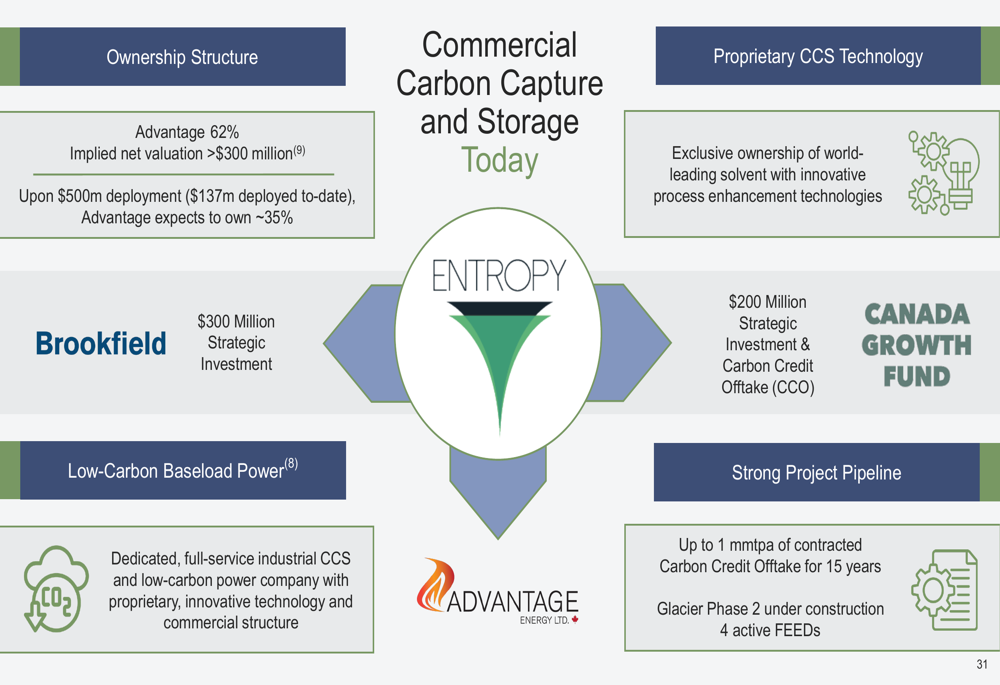

A significant portion of Advantage’s presentation focuses on its carbon capture and storage (CCS) initiatives through Entropy Inc., in which Advantage maintains a 62% ownership stake. The company has secured a $200 million strategic investment from the Canada Growth Fund, along with a carbon credit offtake agreement.

The following chart outlines Advantage’s commercial carbon capture and storage strategy through Entropy:

Entropy’s flagship project, Glacier Phase 2, is described as the "world’s first commercial post-combustion CCS" with a capture capacity of 160,000 tonnes per annum. The project, scheduled to come online in Q2 2026, represents an 86% reduction in emissions from the Glacier gas facility.

Forward-Looking Statements and Risks

While Advantage Energy’s presentation paints an optimistic picture of future growth and financial performance, investors should consider the company’s recent earnings miss and the inherent risks in the energy sector. The Q4 2024 results, which fell significantly short of analyst expectations, raise questions about the company’s ability to execute on its ambitious plans.

Key risks identified in the earnings call include volatile natural gas prices, high net debt levels, potential tariffs and AECO price impacts, integration challenges with newly acquired assets, and regulatory changes that could affect strategic initiatives.

Nevertheless, Advantage Energy appears well-positioned within the Canadian energy landscape, with a substantial resource base, strategic infrastructure, and a forward-looking approach that balances conventional production with carbon capture initiatives. The company’s three-year plan, if successfully executed, could deliver significant value to shareholders despite the recent financial underperformance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.