Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

Advantage Energy Ltd. (TSX:AAV) recently shared its August 2025 investor presentation, highlighting the company’s strategic positioning as "A Progressive Montney Producer for the New Energy Market." The presentation comes after a Q2 earnings report that showed a significant earnings beat despite revenue challenges, reflecting the company’s ability to execute operationally in a difficult natural gas pricing environment.

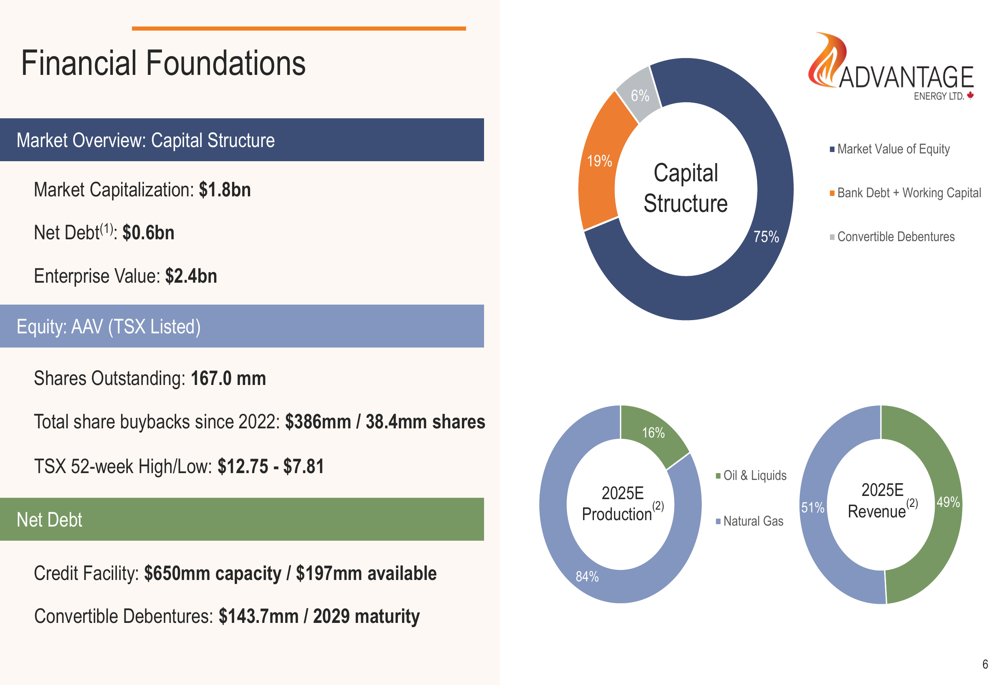

The company’s stock currently trades at $11.11, within its 52-week range of $7.81 to $12.75, and maintains a market capitalization of approximately $1.8 billion according to the presentation materials.

Strategic Initiatives

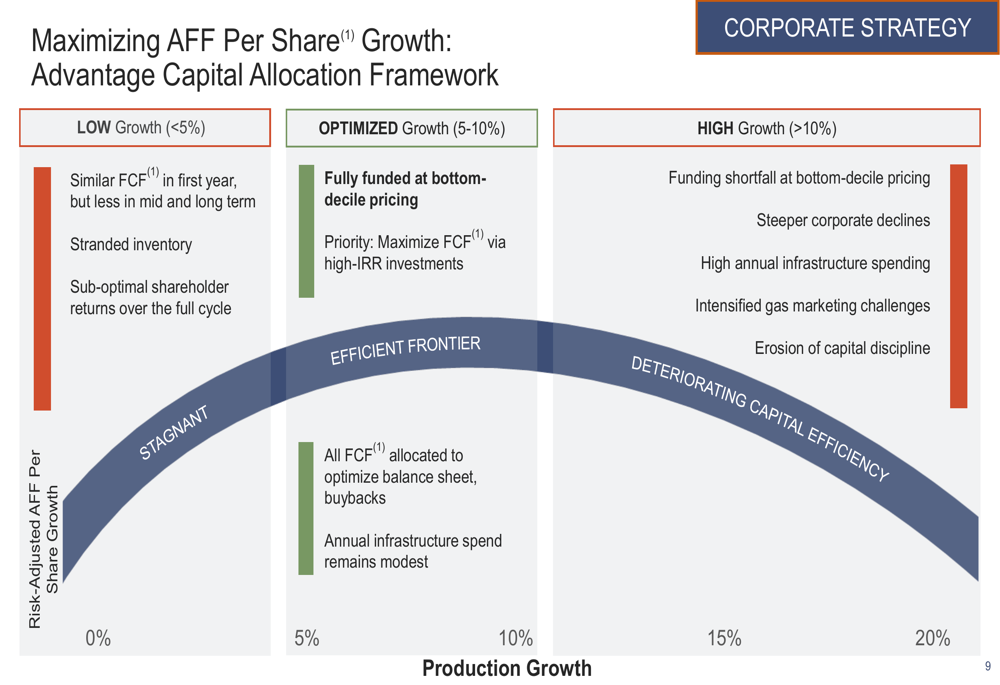

Advantage Energy’s corporate strategy centers on maximizing adjusted funds flow (AFF) per share growth without compromising its balance sheet. The company has established a disciplined approach to growth, capping annual organic production increases at 10%.

As shown in the following chart illustrating the company’s capital allocation framework:

The company identifies three growth scenarios, with an optimal zone between 5-10% production growth that balances risk and return. This strategic framework guides Advantage’s investment decisions, focusing on high-return projects while maintaining financial discipline.

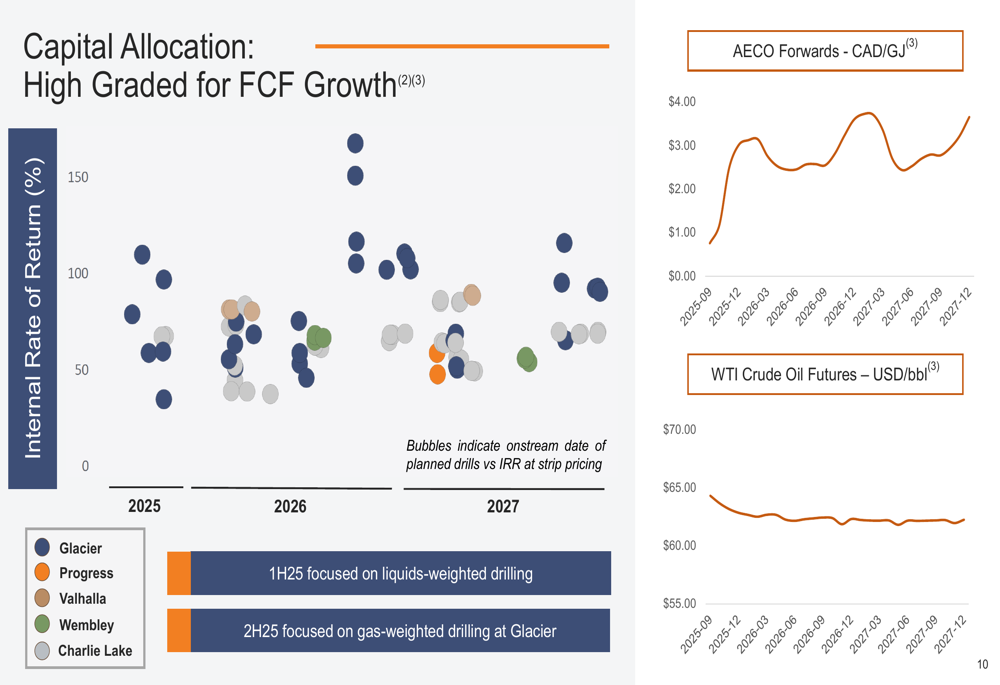

For the remainder of 2025, Advantage plans to focus its capital allocation on liquids-weighted drilling in the first half of the year, shifting to gas-weighted drilling at its Glacier asset in the second half. This approach aligns with the company’s efforts to optimize returns based on commodity price forecasts.

Operational Highlights

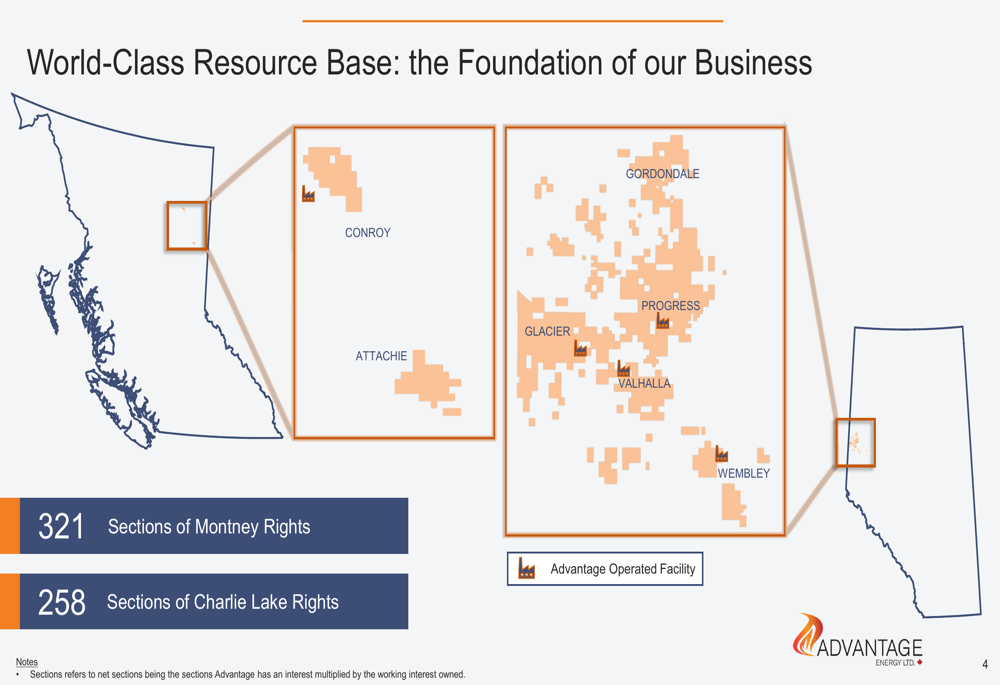

Advantage Energy has established a significant resource base across British Columbia and Alberta, with 321 sections of Montney Rights and 258 sections of Charlie Lake Rights. The company’s asset map illustrates its concentrated position in these prolific areas:

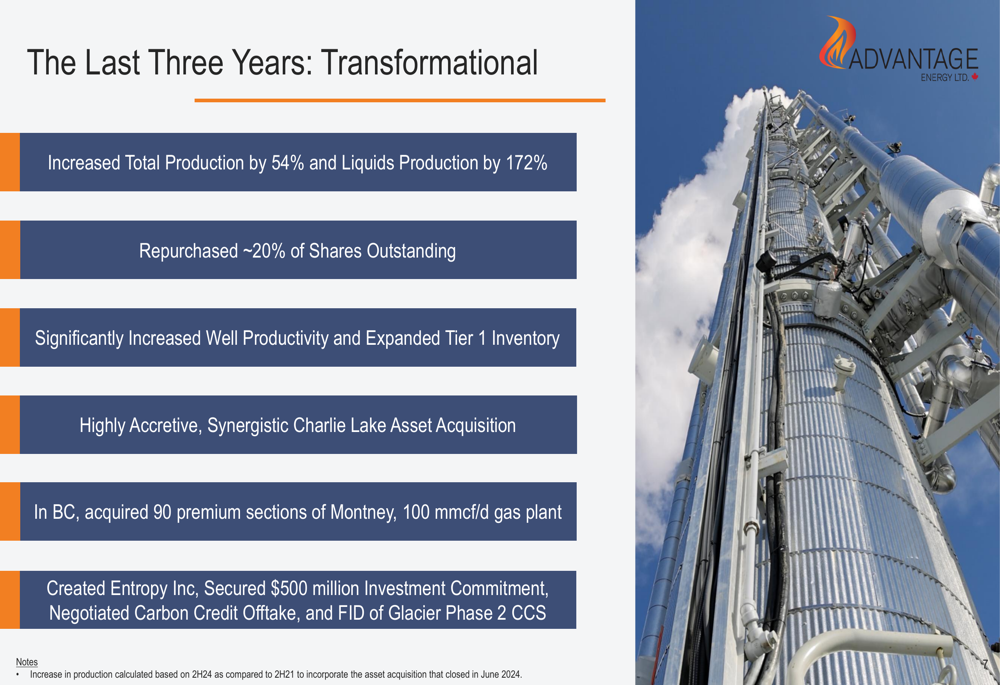

This extensive resource base has supported impressive operational growth. According to the presentation, Advantage has increased total production by 54% and liquids production by 172% over the past three years. This aligns with the Q2 2025 earnings report, which noted production reaching 78,108 barrels of oil equivalent per day, representing an 18% year-over-year increase, with liquids production up 66%.

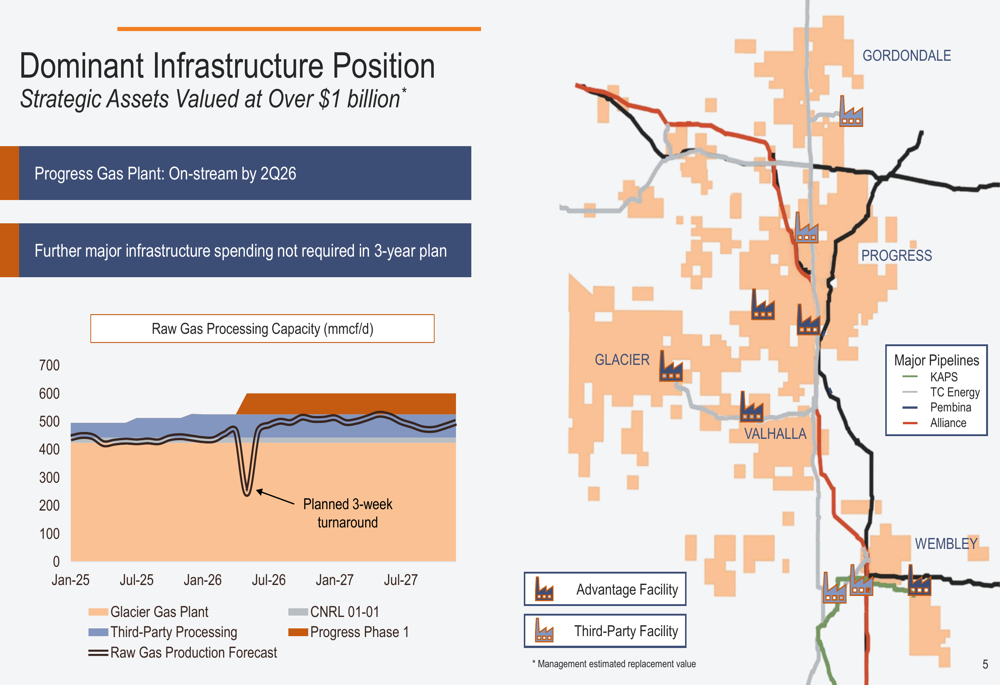

The company has also developed a dominant infrastructure position, with strategic assets valued at over $1 billion. A key development is the Progress Gas Plant, scheduled to come online by Q2 2026, which will support future production growth without requiring additional major infrastructure spending in the company’s three-year plan.

CEO Mike Belenke emphasized these operational improvements during the Q2 earnings call, stating, "We’ve significantly improved well productivity versus historical and cost structure." This focus on operational efficiency has helped the company reduce operating costs to $4.9 per BOE in Q2, below previous guidance.

Financial Performance

Advantage Energy’s financial foundations remain solid, with a capital structure that balances equity and debt. The company reports an enterprise value of $2.4 billion, comprising $1.8 billion in market capitalization and $0.6 billion in net debt.

While the company’s production mix is heavily weighted toward natural gas (84%), its revenue mix is more balanced, with oil and liquids contributing 49% of revenue. This diversification has helped mitigate some of the impact from challenging natural gas prices, which contributed to the revenue shortfall in Q2 2025 ($164.59 million versus a forecast of $194.17 million).

Despite these revenue challenges, Advantage delivered exceptional earnings performance in Q2, with EPS of $0.41 significantly exceeding the forecast of $0.155. This 164.52% earnings beat demonstrates the company’s ability to control costs and improve production efficiency even as revenue targets were missed.

The company has also been active in returning capital to shareholders, repurchasing approximately 20% of outstanding shares over the past three years, with total share buybacks since 2022 amounting to $386 million for 38.4 million shares.

Forward-Looking Statements

Advantage Energy’s presentation outlines several transformational achievements over the past three years that position the company for future growth:

Looking ahead, the company maintains its annual production guidance of 80,000 to 83,000 BOEs per day for 2025. It aims to reduce net debt to $450 million by year-end and plans to resume aggressive share buybacks.

The Progress Gas Plant coming online by Q2 2026 represents a significant infrastructure expansion that will support the company’s growth plans without requiring additional major capital expenditures in the near term.

However, challenges remain, particularly in the natural gas market. During the Q2 earnings call, management acknowledged ongoing AECO cash pricing challenges and noted the company’s proactive approach: "We’re not just sitting around and hoping that the AECO market improves."

The company’s strategic shift toward more liquids-weighted drilling in the first half of 2025 appears designed to mitigate some of these natural gas pricing risks while capitalizing on stronger returns from liquids production.

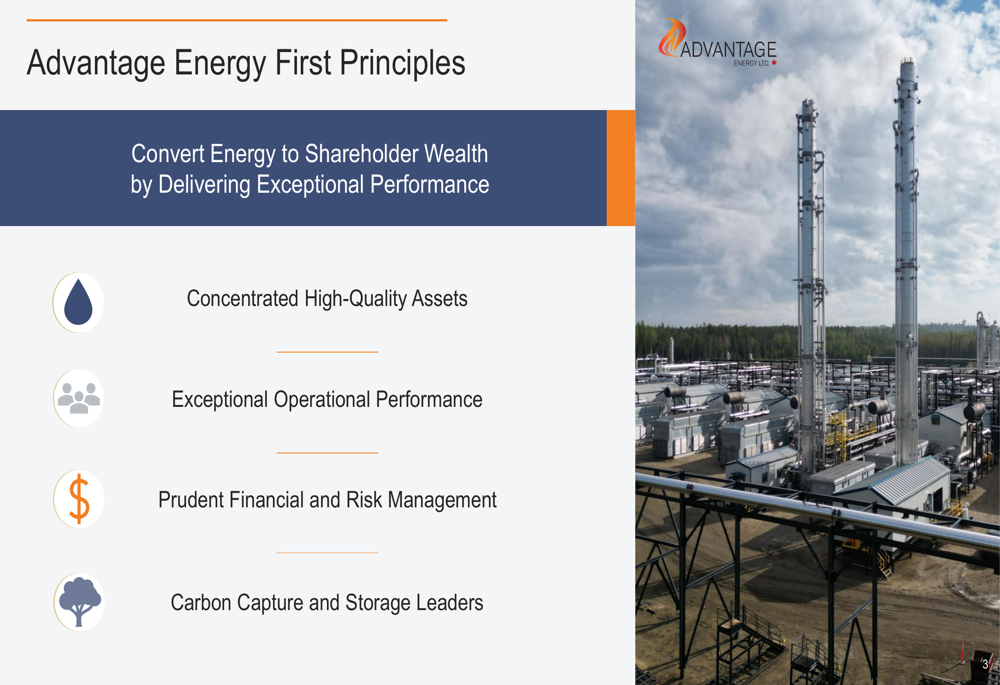

Advantage’s first principles, which guide its overall strategy, emphasize converting energy to shareholder wealth through exceptional performance, with a focus on high-quality assets, operational excellence, prudent financial management, and leadership in carbon capture and storage.

As Advantage Energy navigates the evolving energy landscape, its balanced approach to growth, operational efficiency, and financial discipline positions the company to continue delivering value despite market challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.