Asahi shares mark weekly slide after cyberattack halts production

Aecon Group Inc . (TSX:ARE) delivered a significant improvement in its second quarter 2025 performance, according to the company’s latest presentation. Despite continuing to operate at a loss, the construction and infrastructure development firm reported substantial revenue growth and secured a record backlog that positions it well for future periods.

Quarterly Performance Highlights

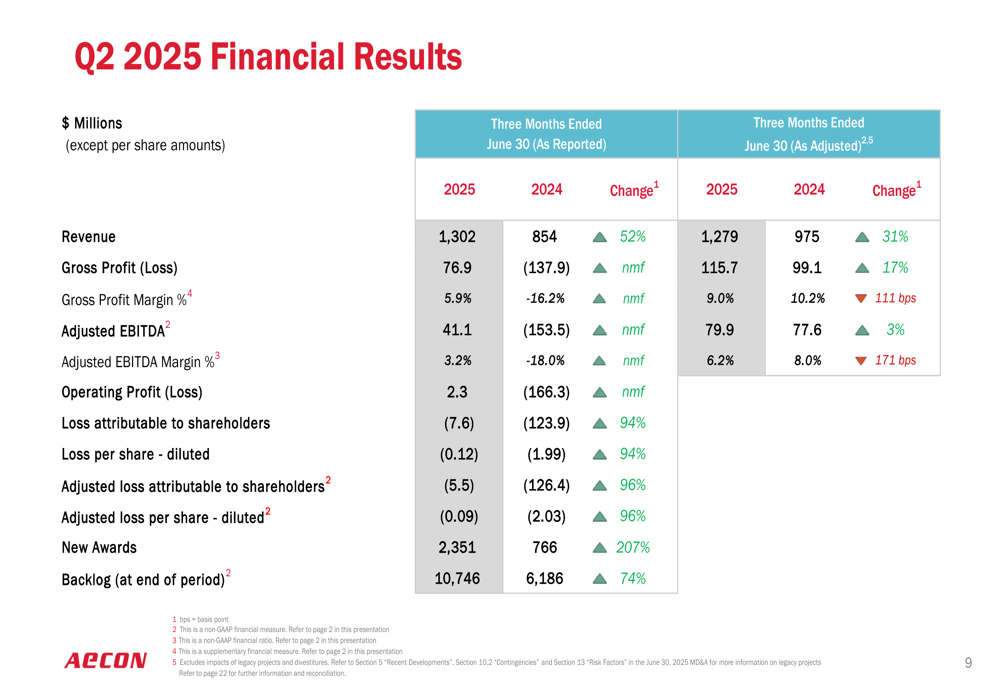

Aecon reported Q2 2025 revenue of $1.3 billion, representing a 52% increase compared to the same period in 2024. On an adjusted basis, which accounts for legacy projects and divestitures, revenue grew 31% year-over-year to $1.28 billion.

Despite the strong revenue growth, the company still recorded a loss attributable to shareholders of $7.6 million ($0.12 per share) in Q2 2025. However, this marks a substantial improvement from the $123.9 million loss ($1.99 per share) reported in Q2 2024.

Adjusted EBITDA reached $41.1 million as reported, or $79.9 million on an adjusted basis, compared to a negative $153.5 million in the same quarter last year. The adjusted EBITDA margin stood at 6.2%, down from 8.0% in Q2 2024.

As shown in the following financial results summary:

The company’s performance represents a significant turnaround from its Q1 2025 results, when Aecon reported an EPS of -$0.54, missing analyst expectations of -$0.1271, which had triggered a 10% stock drop. The sequential improvement suggests the company’s strategic initiatives may be gaining traction.

Strategic Positioning and Business Mix

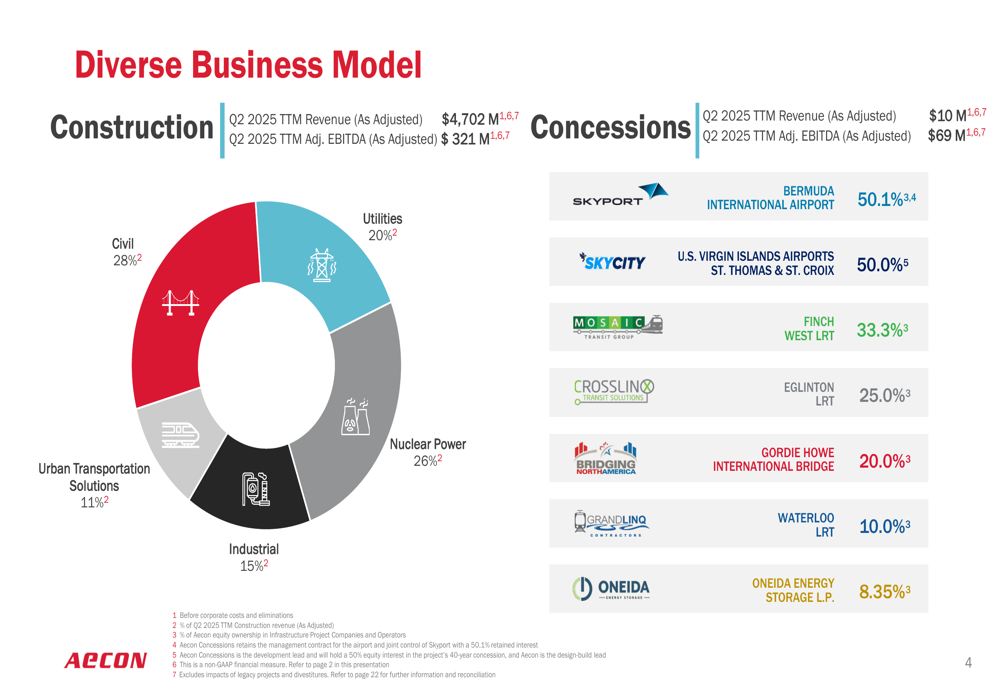

Aecon maintains a diversified business model across construction and concessions segments. The construction segment, which generated $4.7 billion in trailing twelve-month revenue as of Q2 2025, is well-balanced across civil infrastructure (28%), nuclear power (26%), utilities (20%), industrial (15%), and urban transportation solutions (11%).

The following chart illustrates Aecon’s diverse business model:

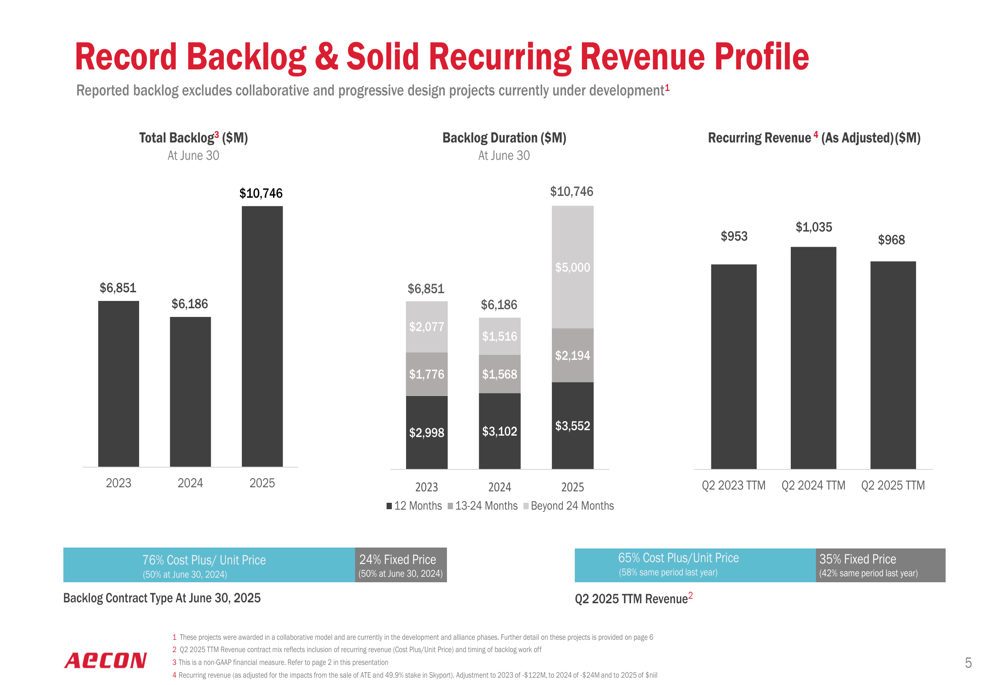

The company has strategically shifted toward lower-risk contract types, with 76% of its backlog now comprised of cost plus/unit price contracts versus 24% fixed price. This represents a significant risk-mitigation strategy, as fixed-price contracts have historically been associated with cost overruns and margin pressure in the construction industry.

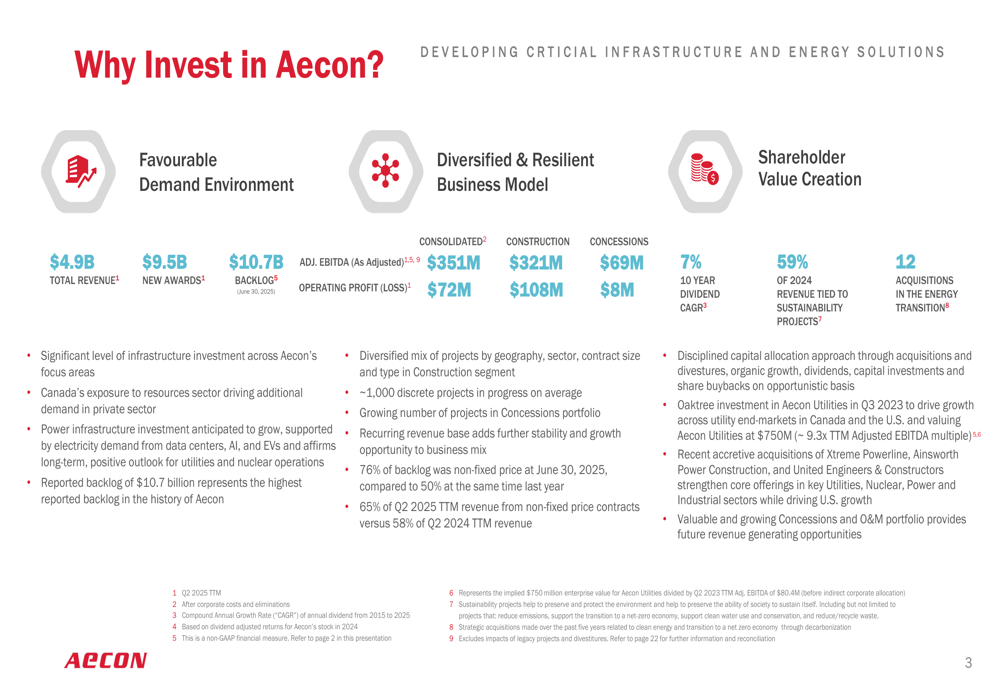

Aecon’s presentation highlighted three key investment pillars: a favorable demand environment, a diversified and resilient business model, and shareholder value creation. The company emphasized its exposure to significant infrastructure investment and Canada’s resource sector, as well as its growing power infrastructure business.

As illustrated in this comprehensive investment overview:

Backlog and Future Outlook

Perhaps the most impressive metric from Aecon’s presentation was its record backlog of $10.75 billion as of June 30, 2025, representing a 74% increase from $6.19 billion a year earlier. New awards in Q2 2025 totaled $2.35 billion, up 207% from Q2 2024.

The following chart shows the dramatic growth in Aecon’s backlog:

The company’s outlook for the remainder of 2025 appears positive, with management expecting stronger revenue compared to 2024. Aecon noted that demand for its services across Canada and in select U.S. and international markets continues to be strong.

A key factor in the company’s future profitability will be the completion of its remaining legacy projects, which are expected to reach substantial completion by the end of 2025. Management anticipates this will lead to improved profitability and margin predictability going forward.

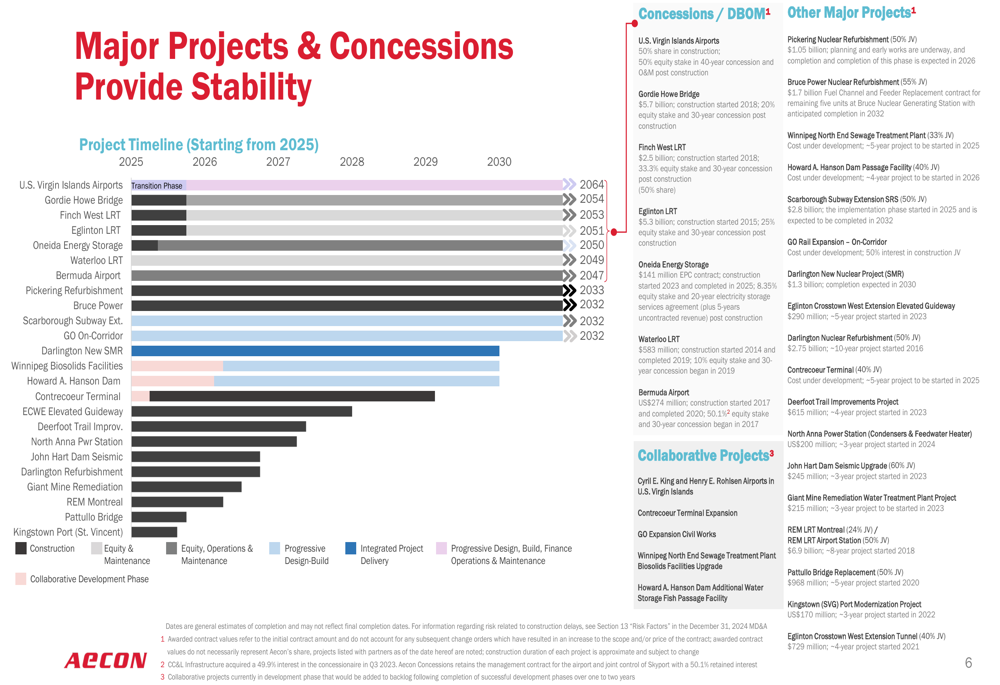

The company’s major projects timeline demonstrates the long-term nature of many of its contracts, providing visibility into future revenue:

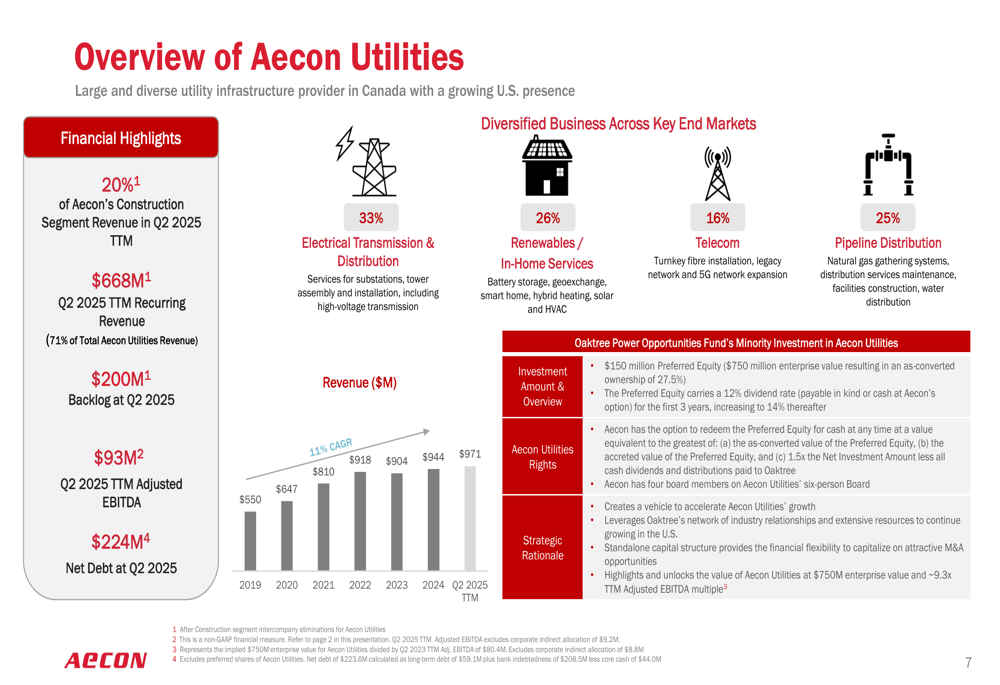

Aecon Utilities and Concessions Portfolio

Aecon highlighted its utilities business, which represents 20% of its construction segment revenue. This division generated $668 million in recurring revenue for the trailing twelve months ended Q2 2025, with an adjusted EBITDA of $93 million. The business has attracted investment from Oaktree, suggesting confidence in its growth potential.

As shown in the following overview of Aecon Utilities:

The company’s concessions portfolio includes international airports, Canadian light rail transit systems, and energy storage facilities. While this segment is smaller, generating just $10 million in TTM revenue, it contributed $69 million in adjusted EBITDA, highlighting its profitability.

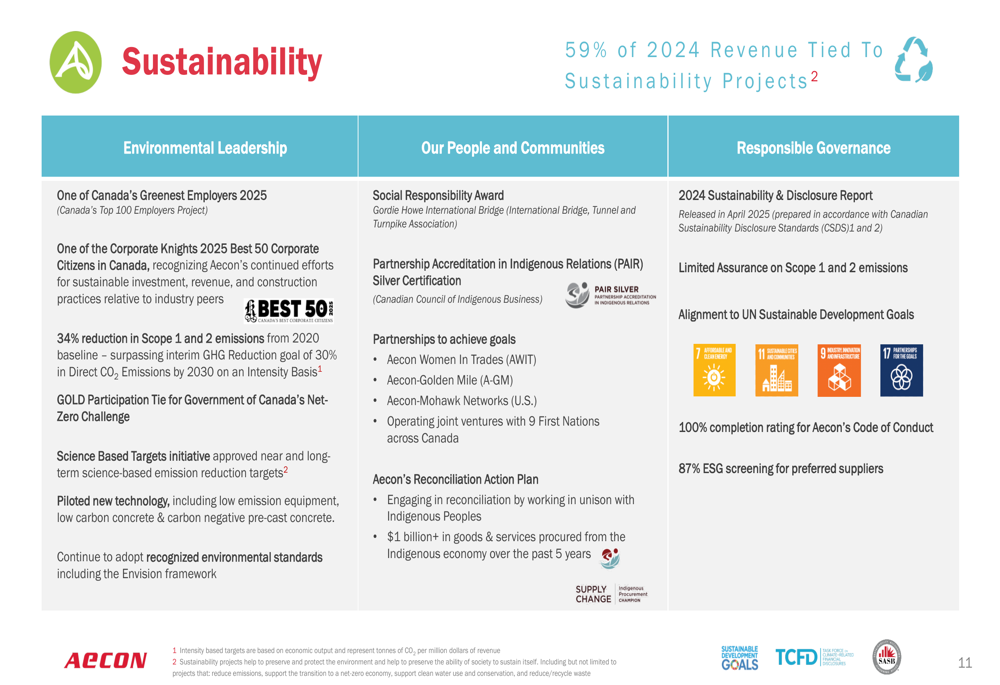

Sustainability Initiatives

Aecon has made sustainability a core part of its business strategy, with 59% of its 2024 revenue tied to sustainability projects. The company has achieved a 34% reduction in Scope 1 and 2 emissions from its 2020 baseline and has received recognition as one of Canada’s Greenest Employers in 2025.

The following overview details Aecon’s sustainability efforts:

The company has established science-based emission reduction targets and is working toward net-zero construction by 2050, with interim targets of 30% emission reduction by 2024 (already achieved) and 50% by 2032.

Market Position and Investor Perspective

Aecon’s stock closed at $19.00 on July 31, 2025, down 1.32% for the day. The company’s shares have traded between $15.21 and $29.70 over the past 52 weeks, indicating significant volatility. With a current dividend yield of 4.0% and a market capitalization of approximately $1.2 billion, Aecon represents a mid-cap player in the infrastructure and construction sector.

Despite the improved quarterly performance, investors should note that Aecon still faces challenges, including negative free cash flow of $10.1 million for the trailing twelve months ended Q2 2025, compared to positive $202.0 million in the prior-year period. The company’s net debt position and ongoing losses, albeit reduced, suggest that the turnaround remains a work in progress.

As Aecon continues to execute on its strategic initiatives and completes its legacy projects, investors will be watching closely to see if the company can translate its growing backlog and revenue into sustainable profitability in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.