Can anything shut down the Gold rally?

Introduction & Market Context

AEDAS Homes (BME:AEDAS) presented its fiscal year 2024/25 results on May 28, 2025, highlighting strong performance against a backdrop of improving market conditions in Spain. The company reported that the Spanish residential market is underpinned by solid fundamentals, including a positive economic outlook with projected GDP growth of 2.5% in 2025 and 1.8% in 2026, alongside a more favorable monetary environment with interest rates cut by 210 basis points since June 2024.

Despite the positive results presentation, AEDAS shares fell 6.75% on the day to close at €26.25, suggesting investors may have had concerns not fully addressed in the company’s outlook or had already priced in the strong performance.

Financial Performance Highlights

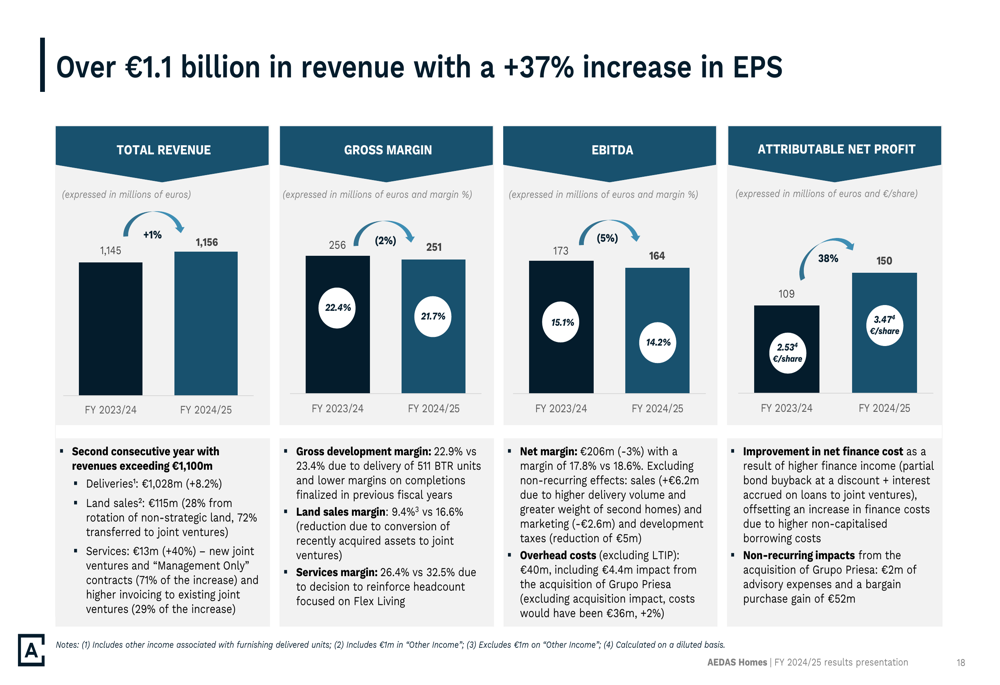

AEDAS Homes reported total revenue of €1.16 billion for FY 2024/25, representing a modest 1% increase year-over-year, but with residential development revenue growing by a more substantial 8% to €1.03 billion. The company achieved a 37% increase in earnings per share, driven by strong sales momentum and operational efficiency.

As shown in the following financial performance overview:

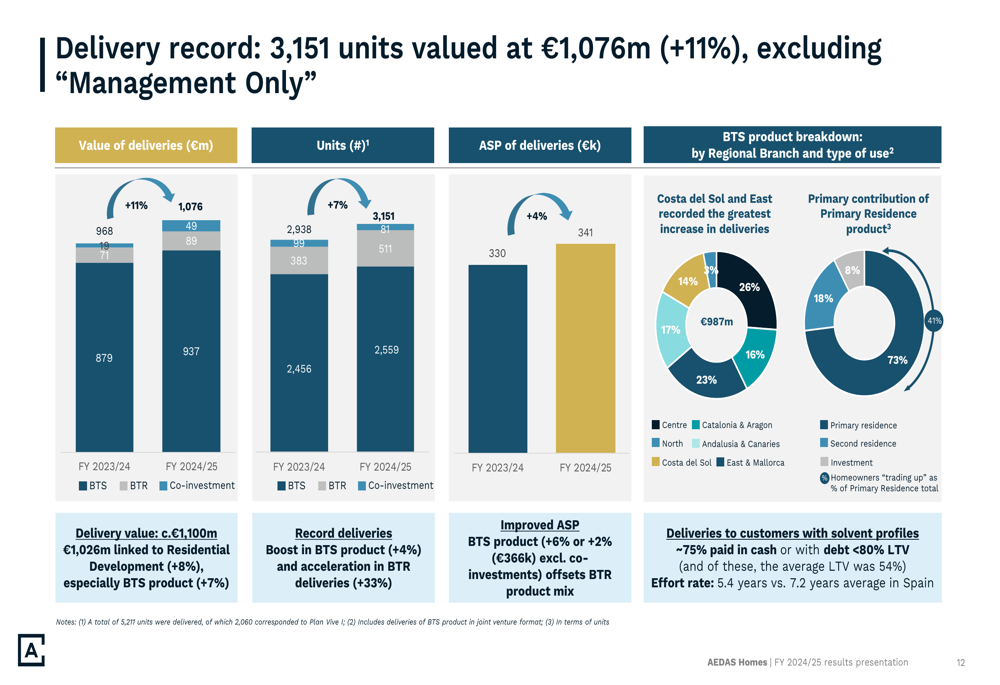

The company’s gross development margin remained relatively stable at 22.9%, compared to 23.4% in the previous year. AEDAS delivered 3,151 units valued at €1.08 billion (excluding "Management Only" units), representing an 11% increase in value. The Build-to-Sell (BTS) segment, which forms the core of AEDAS’s business, saw deliveries increase by 7% with revenues of €937 million.

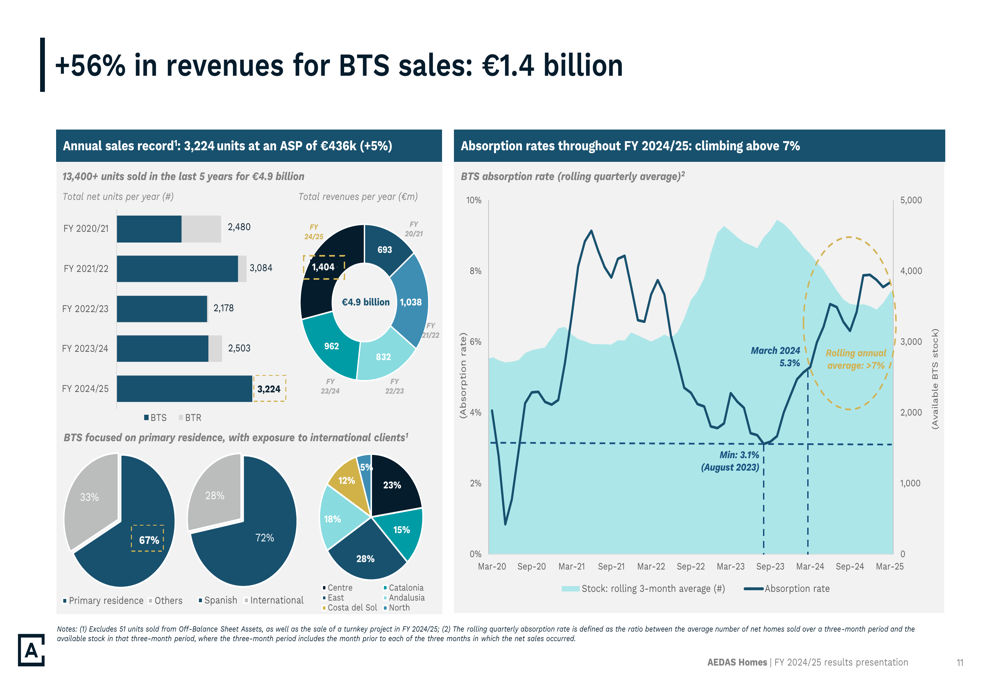

Sales momentum was particularly strong, with 3,224 net BTS sales, a 48% increase compared to the previous year, at an average selling price of €436,000 (+5%). This exceptional sales performance is illustrated in the following chart:

The company’s delivery record shows significant growth, with the East & Mallorca and Costa del Sol regions being the main contributors to revenue growth:

Strategic Initiatives and Business Diversification

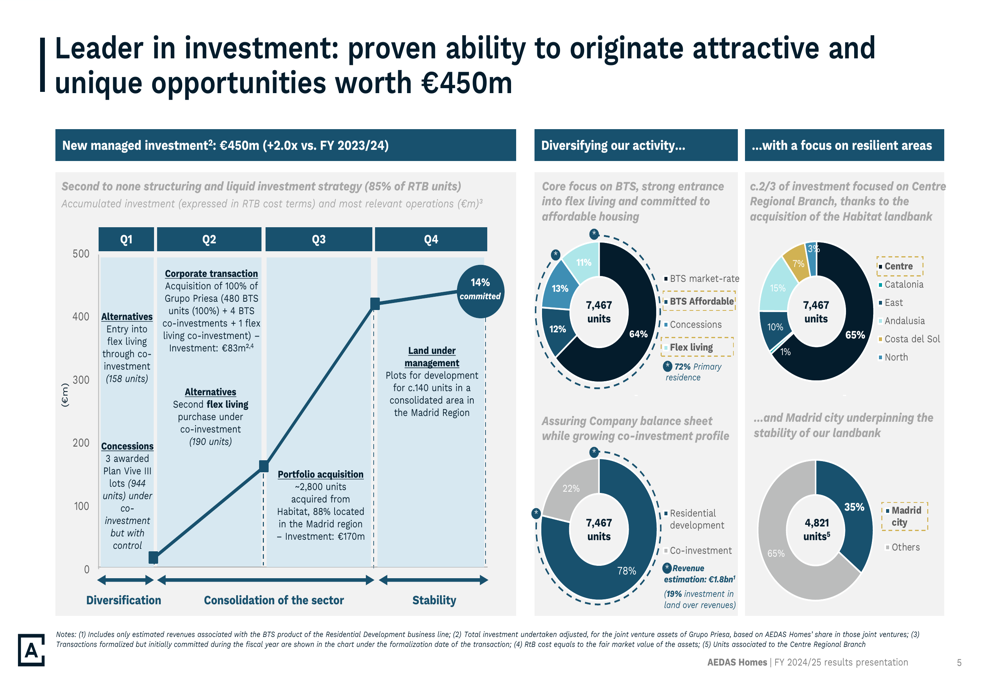

AEDAS Homes is actively diversifying its business model beyond traditional residential development. The company has made significant investments of €450 million in FY 2024/25, more than double the amount invested in the previous fiscal year, with 85% in ready-to-build (RTB) units.

The investment strategy focuses on diversification across different product types, as shown in the following breakdown:

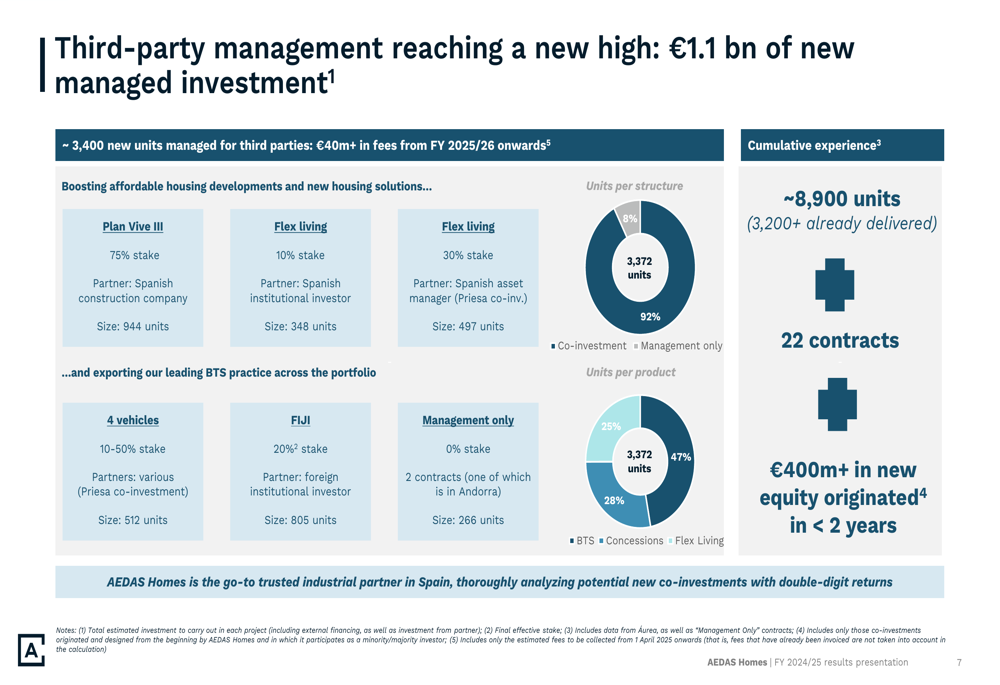

The company is also expanding its third-party management business, which saw a 40.2% increase in revenue. AEDAS reported €1.1 billion of new managed investment, representing approximately 3,400 new units managed for third parties, which is expected to generate over €40 million in fees from FY 2025/26 onwards.

Additionally, AEDAS Homes has introduced a new ESG Strategic Plan for 2024-2026, which outlines 31 specific actions across various sustainability areas:

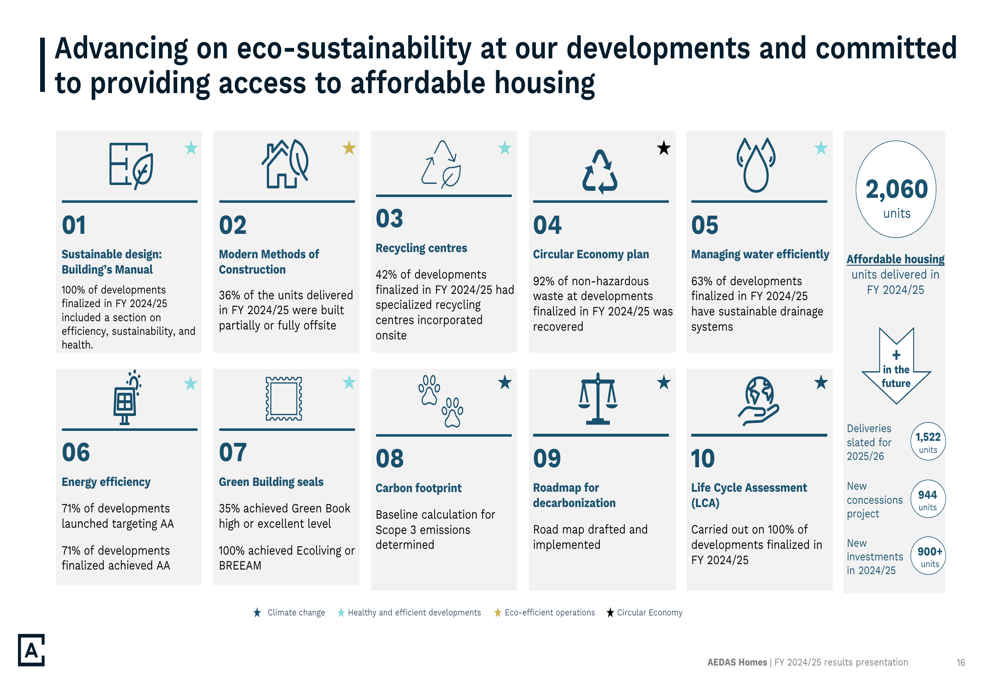

The company has made significant progress in eco-sustainability at its developments and has delivered 2,060 affordable housing units in FY 2024/25, demonstrating its commitment to addressing housing accessibility:

Landbank and Future Growth Outlook

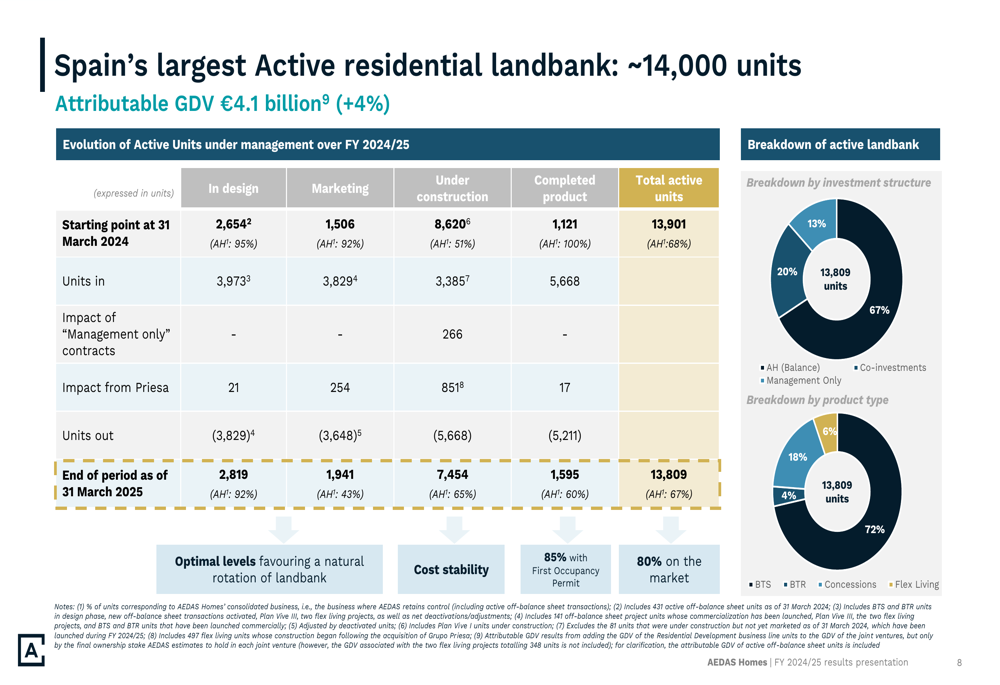

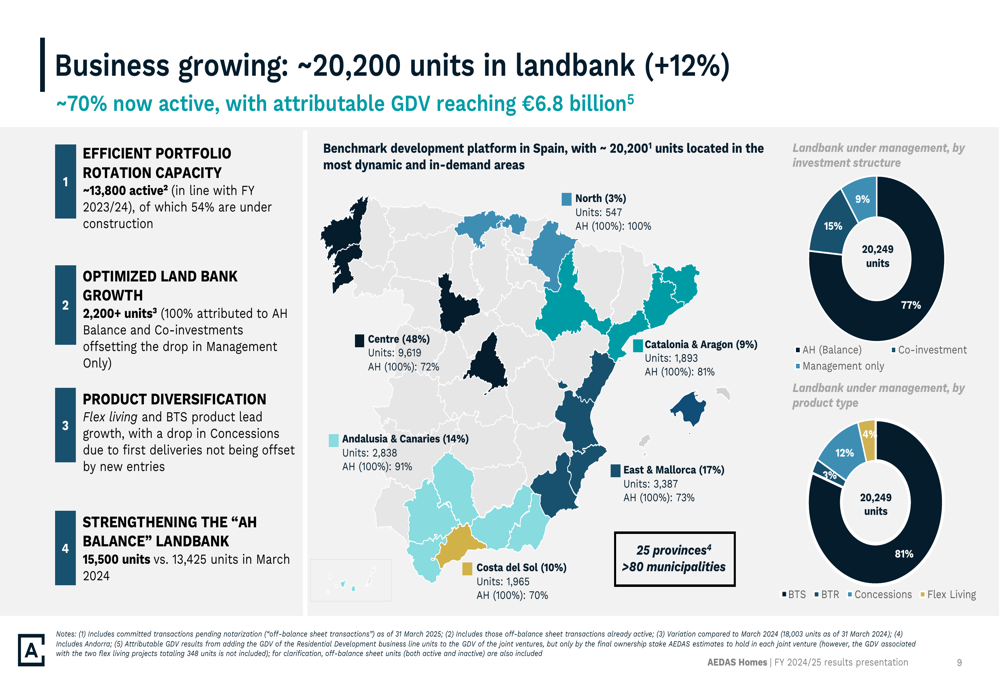

AEDAS Homes maintains Spain’s largest active residential landbank with approximately 14,000 units, providing strong visibility for future growth. The total landbank has grown to around 20,200 units (+12% year-over-year) with an attributable Gross Development Value (GDV) of €6.8 billion.

The following chart illustrates the composition and distribution of the company’s landbank:

The company’s expanded landbank is strategically distributed across Spain, with a focus on high-demand areas:

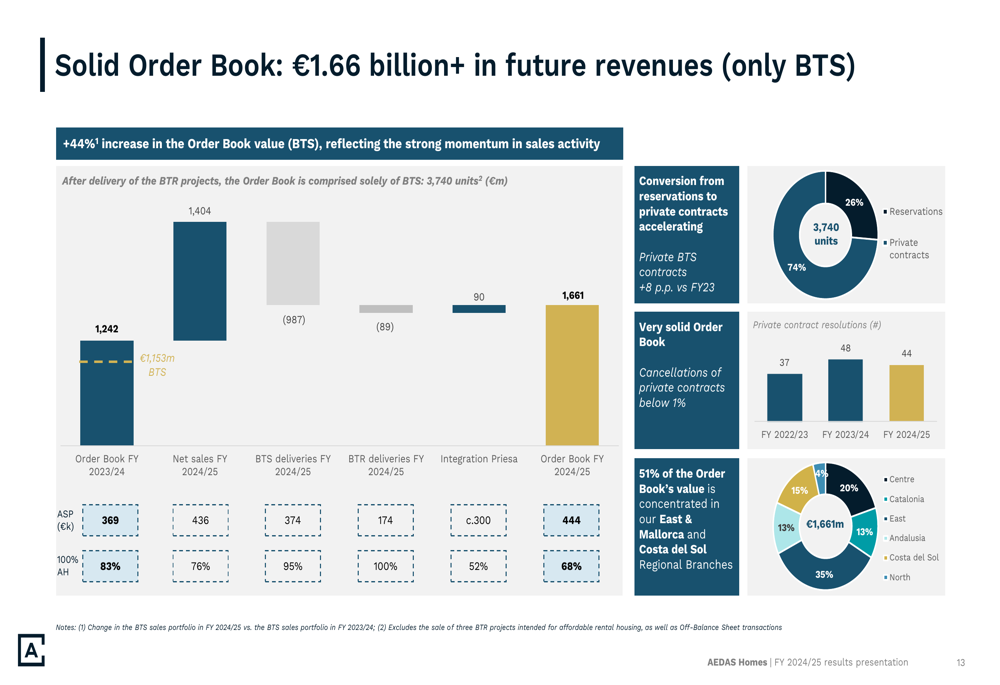

This extensive landbank provides AEDAS with significant revenue visibility for the coming years. The company expects to generate approximately €1 billion in annual revenue over the next two years, with a solid order book of €1.66 billion in future revenues from BTS projects alone, representing a 44% increase in order book value.

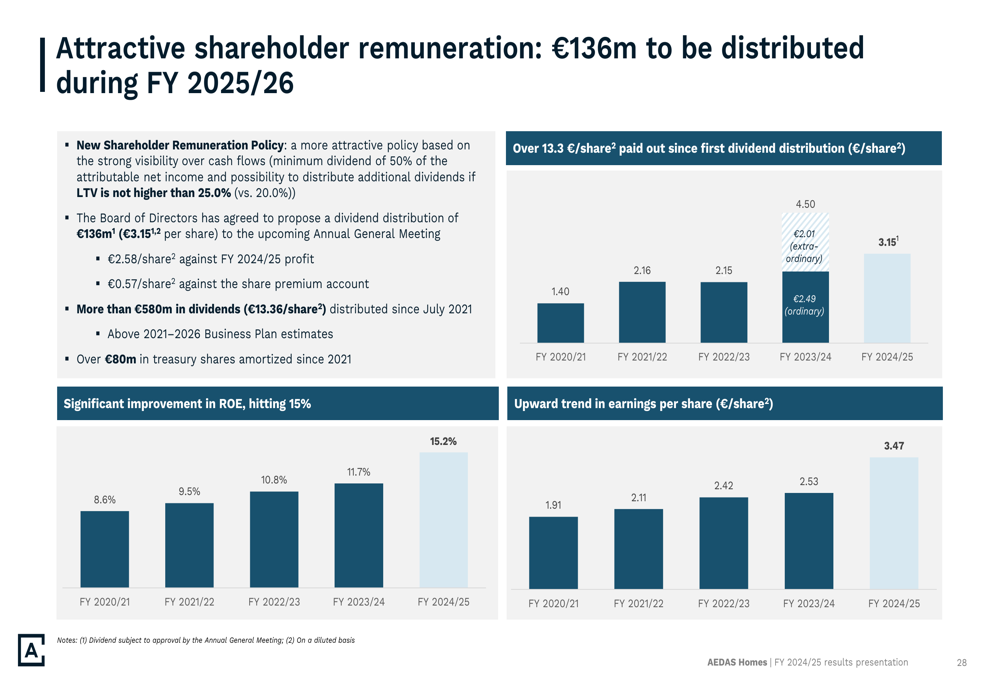

Shareholder Remuneration

AEDAS Homes announced plans to distribute €136 million to shareholders during FY 2025/26 as part of its commitment to providing attractive returns. The company has distributed more than €580 million in dividends since its IPO and reported a significant improvement in Return on Equity (ROE).

The dividend policy and historical payouts are illustrated in the following chart:

Market Reaction and Conclusion

Despite the strong operational and financial performance reported in the presentation, AEDAS Homes’ stock price fell 6.75% on the day of the announcement to €26.25. This disconnect between positive results and negative market reaction could be attributed to several factors, including broader market concerns about the sustainability of the Spanish housing market recovery, potential margin pressures, or simply a "sell the news" reaction after the stock had already appreciated in anticipation of strong results.

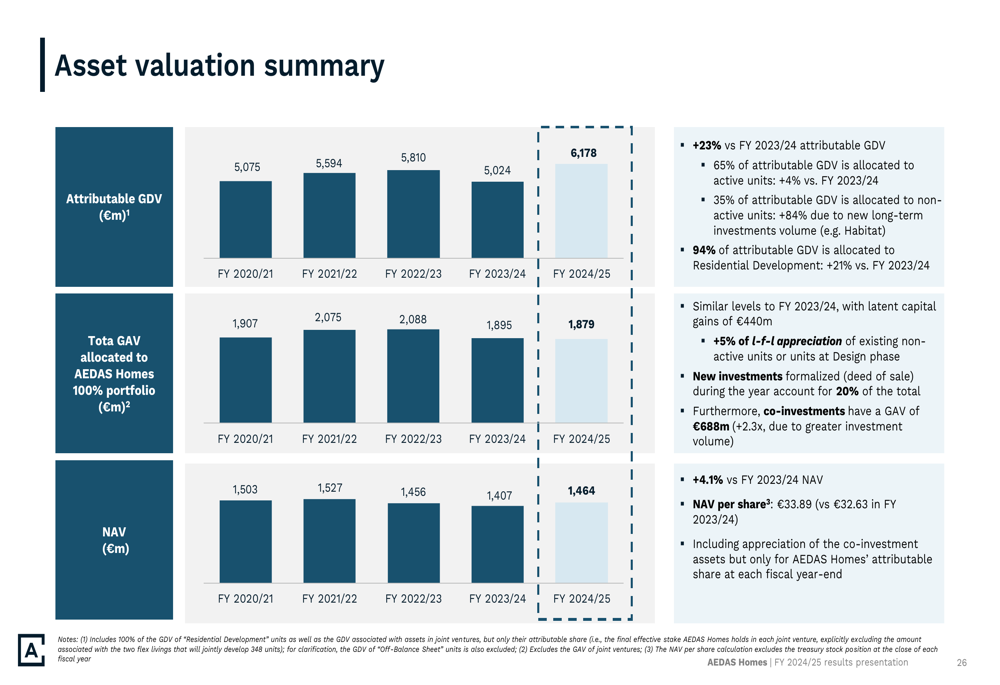

AEDAS Homes remains well-positioned in the Spanish residential market with its diversified business model, strong landbank, and solid financial position. The company’s asset valuation summary shows significant value creation potential:

Looking ahead, AEDAS Homes expects to maintain its growth trajectory, supported by favorable market conditions, its diversified product portfolio, and the largest active landbank under management in Spain. However, investors will likely be watching closely for signs that the company can maintain its margins and sales momentum in the face of potential economic headwinds and increasing competition in the Spanish residential market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.