Morgan Stanley again adjusts its Fed forecast, now sees 4 cuts in 2026

Introduction & Market Context

Affirm Holdings Inc (NASDAQ:AFRM) presented its fiscal fourth quarter 2025 earnings results on August 28, 2025, showcasing robust growth across key metrics while achieving significant profitability milestones. The buy now, pay later (BNPL) provider closed the trading day at $77.59, with a modest 0.46% gain in after-hours trading, suggesting a cautiously positive market reaction to the results.

The company’s performance comes amid continued expansion in the BNPL sector, with Affirm successfully diversifying its business across multiple retail categories while growing its direct-to-consumer offerings, particularly the Affirm Card.

Quarterly Performance Highlights

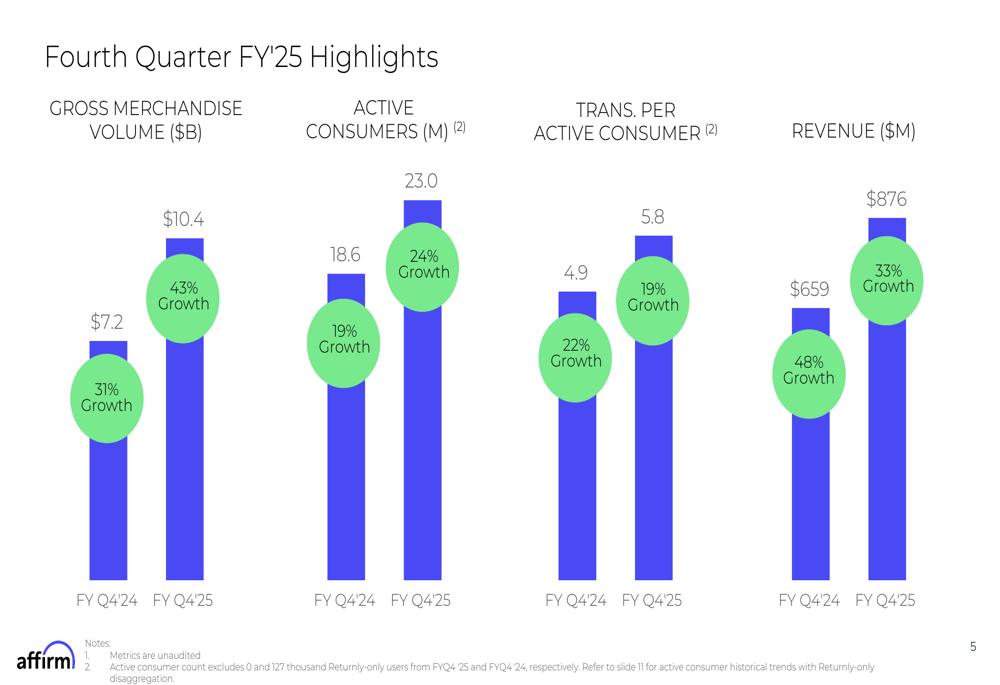

Affirm reported exceptional growth across all key performance indicators for the fourth quarter of fiscal year 2025, significantly outpacing the previous year’s results.

As shown in the following chart of quarterly performance metrics, Gross Merchandise Volume (GMV) reached $10.4 billion, representing a 43% year-over-year increase. Active consumers grew to 23.0 million, up 24% from the prior year, while transactions per active consumer increased by 19% to 5.8. Revenue climbed to $876 million, a 33% improvement compared to Q4 2024:

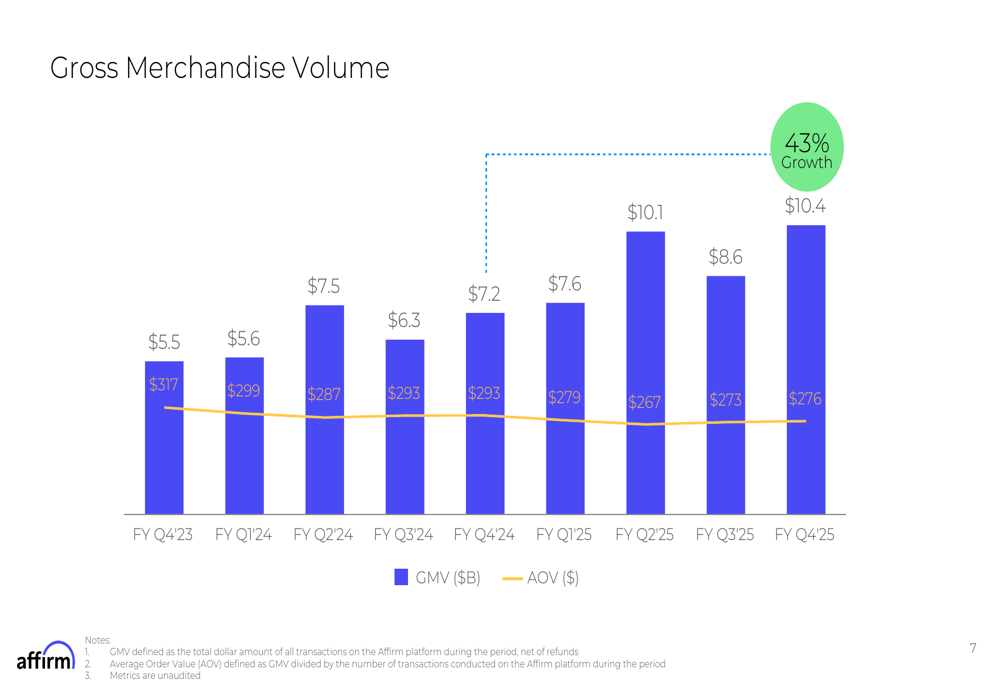

The company’s GMV has shown consistent growth over the past two years, with Q4 2025 marking the highest quarterly volume to date. Average Order Value (AOV) has remained relatively stable, hovering around $276 in the most recent quarter:

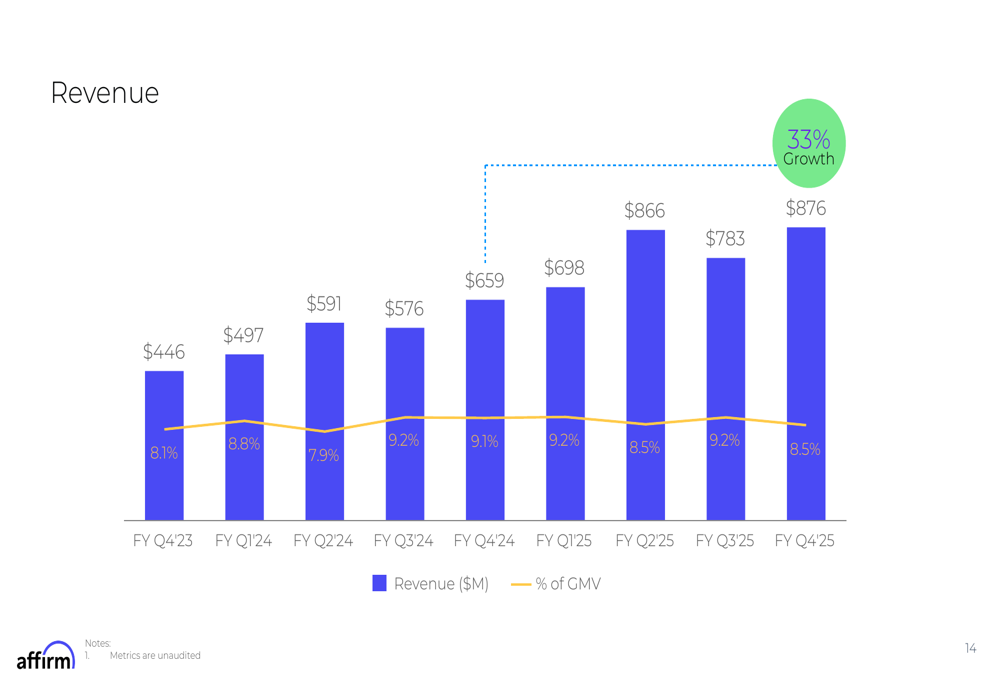

Revenue growth has closely tracked GMV expansion, with Q4 2025 revenue reaching $876 million, a 33% increase year-over-year. Revenue as a percentage of GMV has remained relatively stable at 8.8%, indicating consistent monetization of transaction volume:

Affirm Card and Direct-to-Consumer Growth

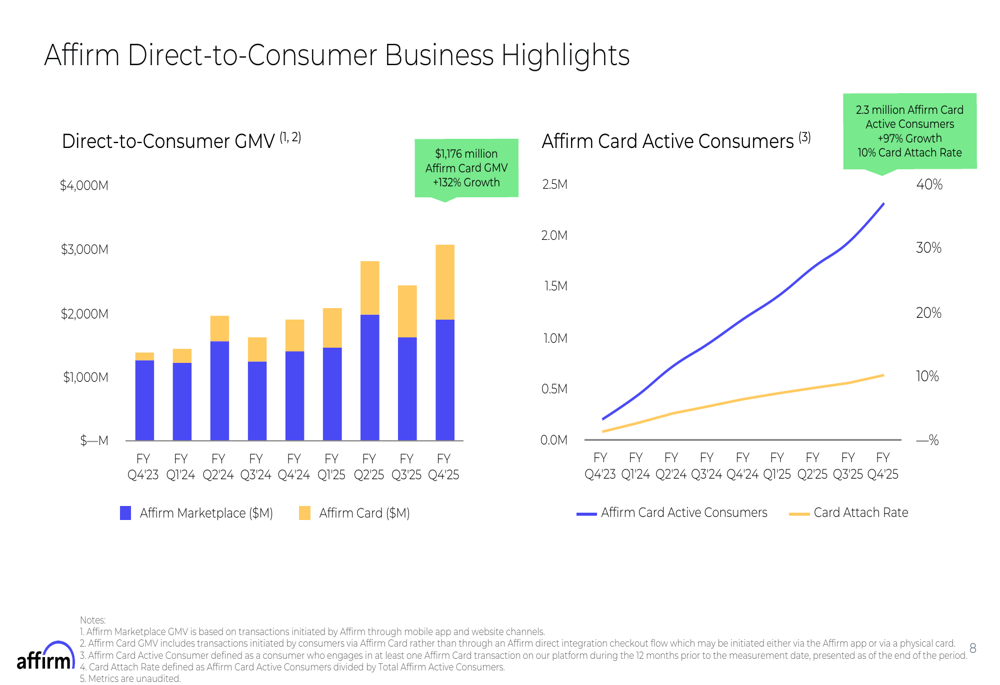

A standout element of Affirm’s Q4 results was the exceptional performance of its direct-to-consumer business, particularly the Affirm Card. The company’s strategic push into direct consumer relationships is yielding significant results, reducing dependence on merchant partnerships.

As illustrated in the following chart, Affirm Card GMV reached $1,176 million in Q4 2025, representing an impressive 132% growth. Simultaneously, Affirm Card active consumers grew to 2.3 million, a 97% increase, with the card achieving a 10% attach rate among Affirm’s customer base:

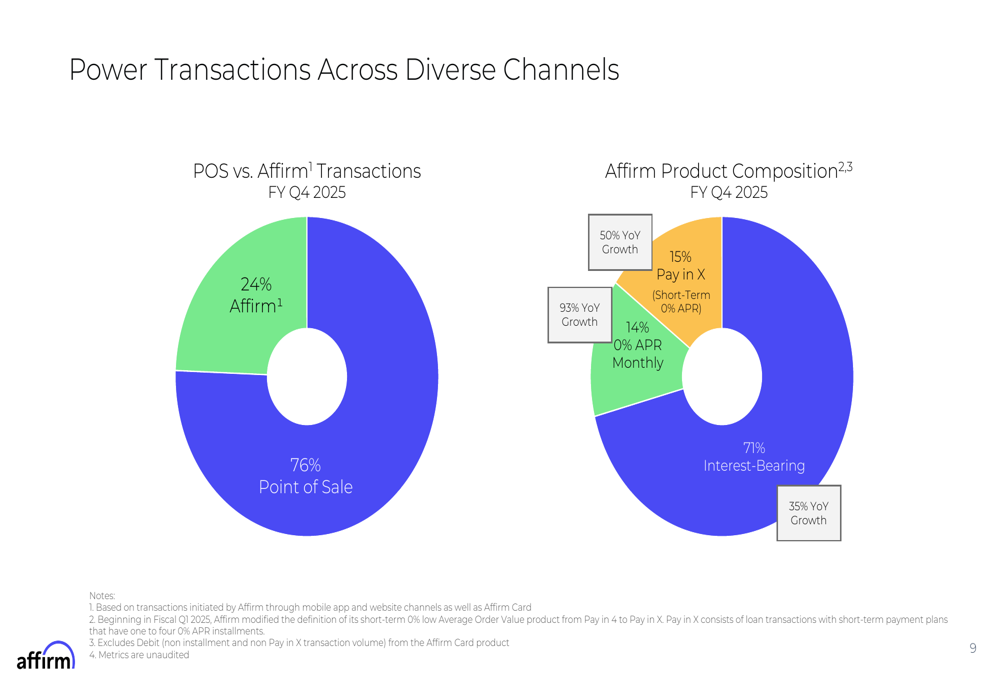

The company’s transaction mix shows that while 76% of transactions occur at the point of sale, 24% now take place directly through Affirm channels. The product composition reveals that interest-bearing loans comprise 71% of loan volume (growing 35% year-over-year), while 0% APR monthly plans and Pay in X options represent 14% and 15% respectively, with the latter growing 50% compared to the previous year:

Industry Diversification and Merchant Growth

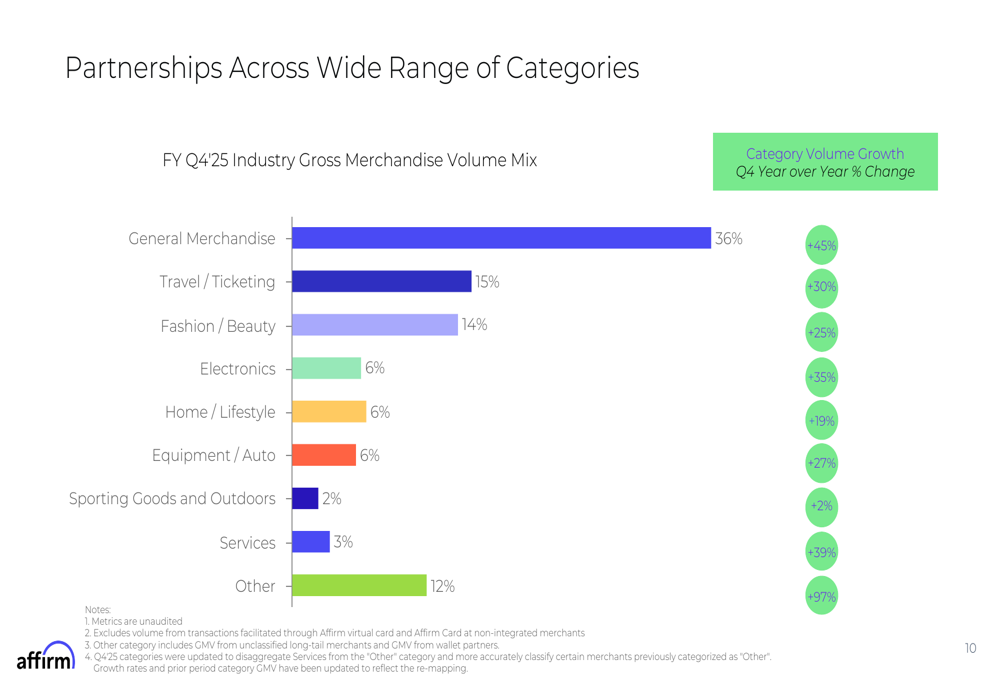

Affirm continues to diversify its business across multiple retail categories, reducing concentration risk and expanding its addressable market. The company’s GMV is now distributed across nine major industry categories, with general merchandise representing the largest share at 36%.

As shown in the following breakdown, all major categories demonstrated strong year-over-year growth, with "Other" categories showing the most dramatic increase at 97%:

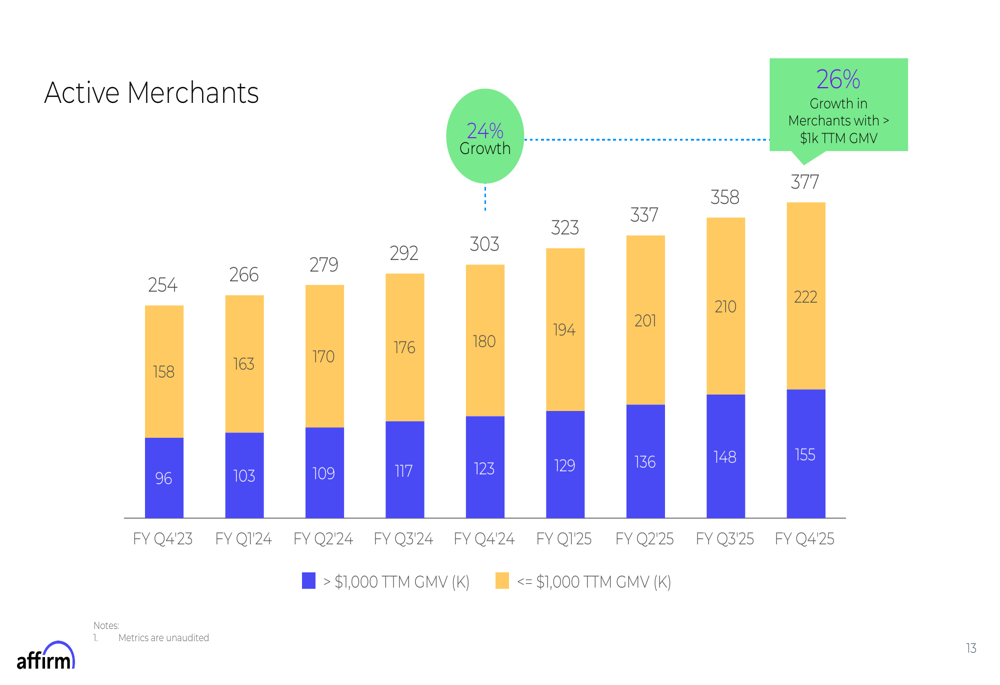

The company’s merchant base continues to expand, with 155 merchants generating more than $1,000 in trailing twelve-month GMV as of Q4 2025, representing 26% growth year-over-year:

Profitability and Financial Health

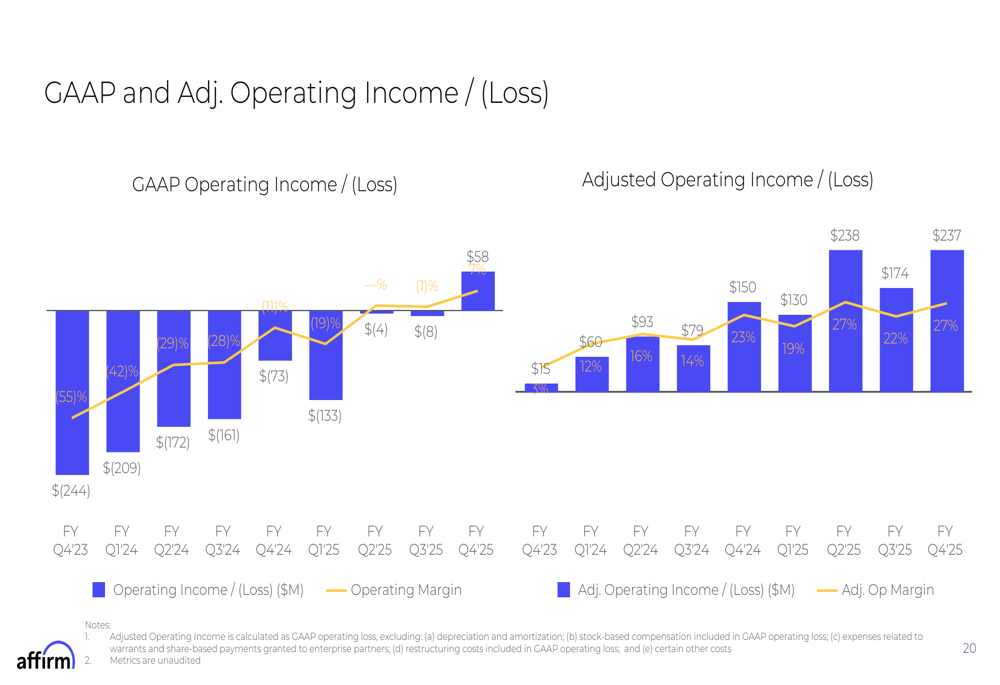

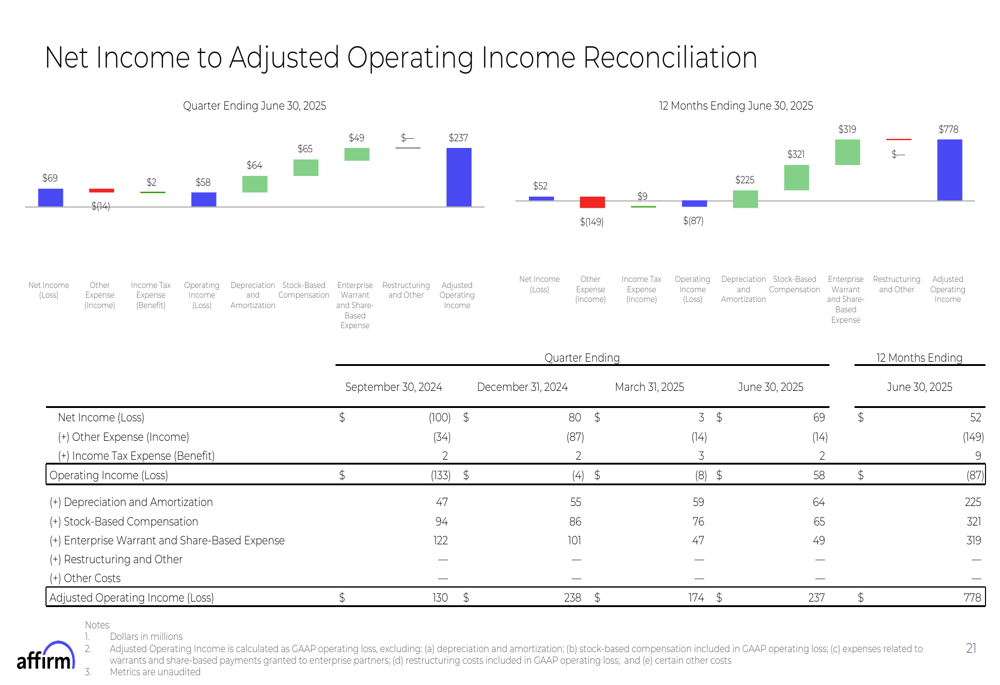

A significant milestone in Affirm’s Q4 2025 results is the achievement of positive operating income on both a GAAP and adjusted basis. This marks an important inflection point in the company’s journey toward sustainable profitability.

As illustrated in the following chart, Affirm reported GAAP operating income of $58 million and adjusted operating income of $237 million in Q4 2025, both representing substantial improvements from prior quarters:

The reconciliation between net income and adjusted operating income provides additional transparency into the company’s financial performance:

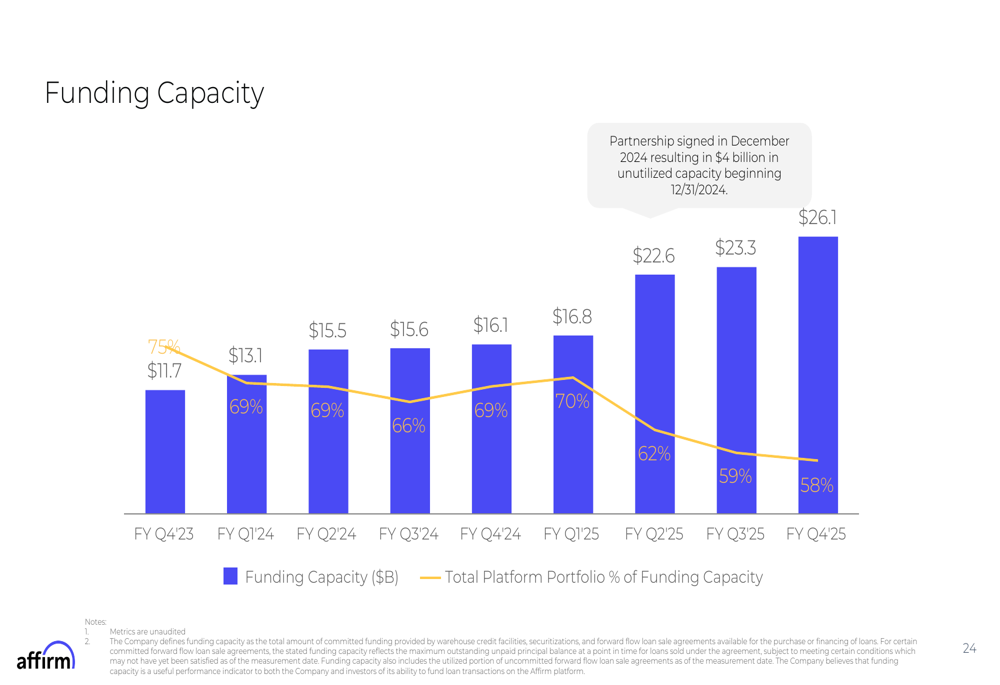

Affirm’s funding capacity remains strong at $26.1 billion, with the current portfolio utilizing only 58% of this capacity, positioning the company well for continued growth:

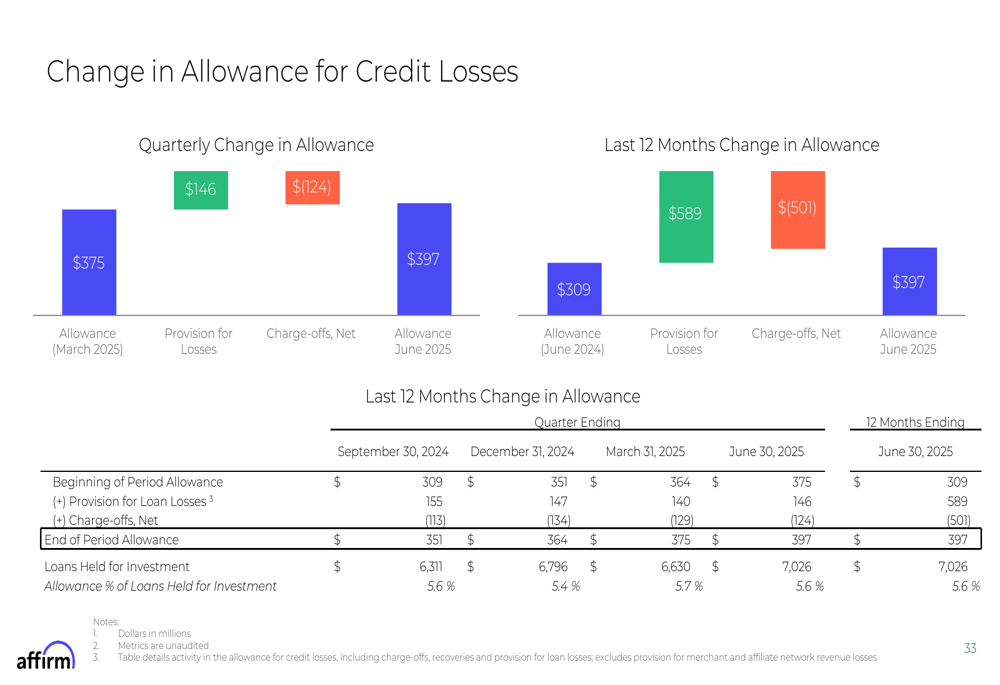

The company has maintained stable credit performance, with careful management of allowances for credit losses. As shown below, Affirm’s approach to credit risk management involves balancing provisions with charge-offs to maintain appropriate coverage:

Forward-Looking Statements

Looking ahead, Affirm provided an optimistic outlook for fiscal year 2026, projecting GMV to exceed $46 billion with revenue as a percentage of GMV at approximately 8.4%. The company expects to maintain its profitability trajectory, with adjusted operating margin forecast to exceed 26.1% and GAAP operating margin above 6.0%.

For the first quarter of fiscal year 2026, Affirm anticipates GMV between $10.10 billion and $10.40 billion, with revenue ranging from $855 million to $885 million, suggesting continued strong performance in the near term.

The company’s outlook incorporates assumptions regarding product mix, enterprise partnerships, interest rate environment, and ongoing product and go-to-market initiatives, reflecting management’s confidence in Affirm’s business model and growth strategy despite potential economic uncertainties.

Affirm’s Q4 2025 results demonstrate that the company has successfully scaled its business while achieving profitability milestones, positioning it well for continued growth in the competitive BNPL landscape. The exceptional performance of the Affirm Card suggests that the company’s direct-to-consumer strategy is gaining significant traction, potentially reducing reliance on merchant partnerships while deepening customer relationships.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.