Jamaica’s outlook revised to stable by Fitch after hurricane

Introduction & Market Context

AGNC Investment Corp (NASDAQ:AGNC), a leading agency residential mortgage REIT with a market capitalization of $10.5 billion, presented its third quarter 2025 results on October 21, revealing a mixed performance. The company reported significant portfolio growth and book value improvement, despite missing earnings per share expectations. Following the announcement, AGNC's stock declined 0.54% to close at $10.07, with an additional 0.3% drop in premarket trading.

The mortgage REIT operates in a challenging interest rate environment, with the presentation highlighting shifts in agency MBS yields and Treasury rates. During Q3 2025, 30-year current coupon yields decreased by 28 basis points, while 10-year Treasury yields fell by 8 basis points, creating a complex backdrop for the company's operations.

Quarterly Performance Highlights

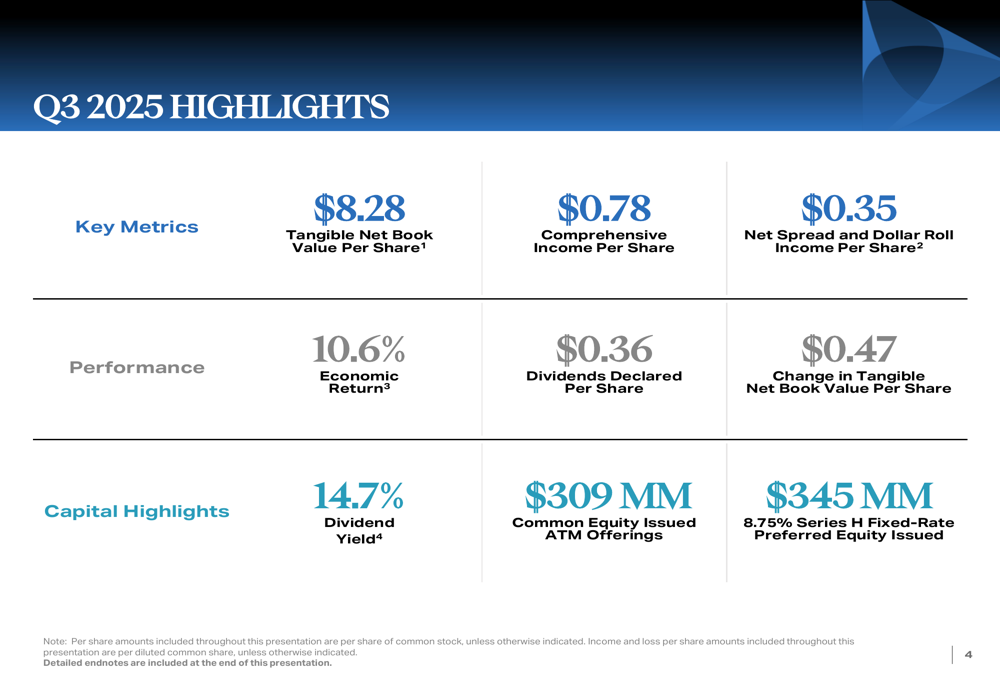

AGNC reported comprehensive income of $0.78 per share for Q3 2025, while net spread and dollar roll income came in at $0.35 per share, falling short of the $0.39 analyst expectations. However, the company's tangible net book value increased by $0.47 to $8.28 per share, generating an economic return of 10.6% for the quarter.

As shown in the following quarterly highlights:

The company maintained its dividend at $0.36 per share, representing an annualized yield of 14.7% based on current share prices. This continues to position AGNC as one of the highest-yielding mortgage REITs in the market.

AGNC's revenue performance was a bright spot, with actual figures of $903 million exceeding forecasts of $883.28 million by 2.23%, according to the earnings report. This revenue outperformance came despite the challenges in maintaining profit margins.

Portfolio and Investment Strategy

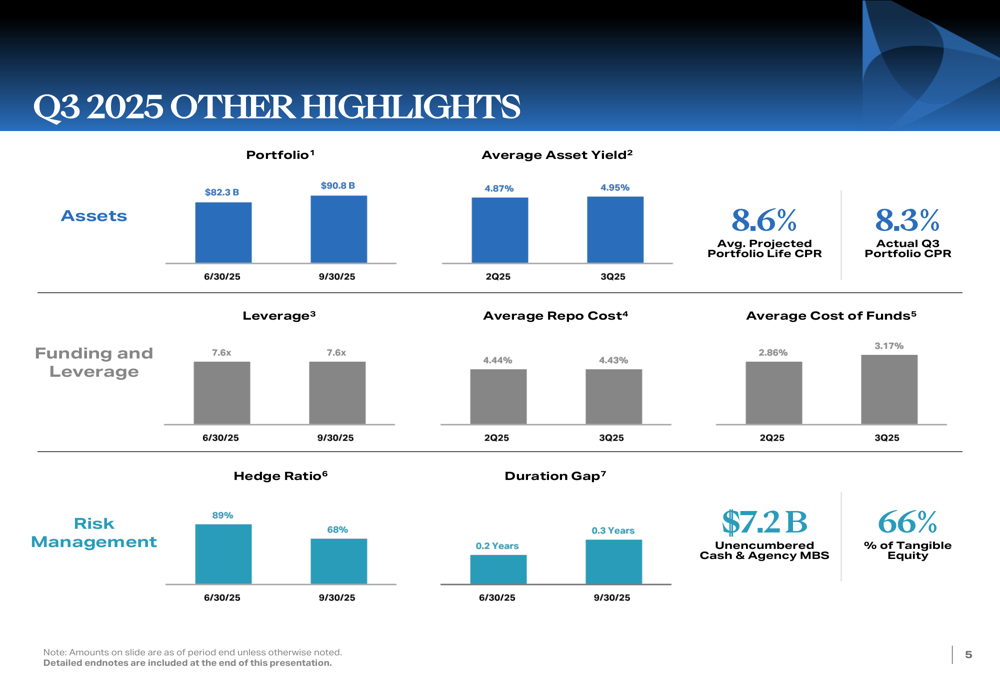

AGNC significantly expanded its investment portfolio during the quarter, increasing from $82.3 billion as of June 30, 2025, to $90.8 billion by September 30, 2025. This 10.3% growth was accompanied by an improvement in average asset yield from 4.87% to 4.95%.

The portfolio expansion details are illustrated in the following slide:

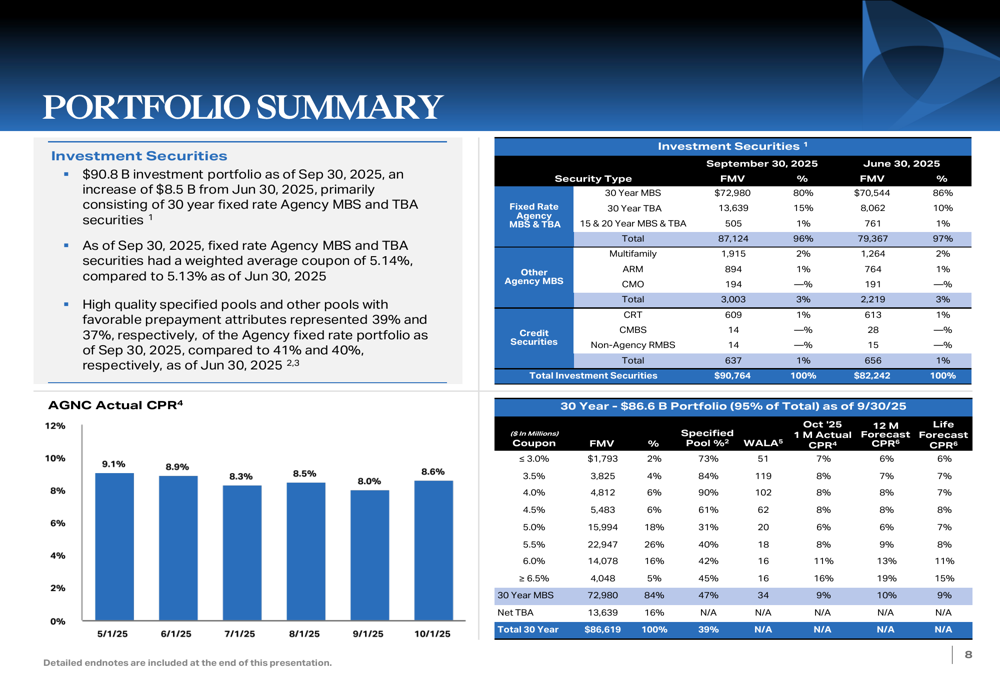

The company's investment portfolio remains heavily concentrated in 30-year mortgage-backed securities, which account for 95% of total holdings. Within this category, 30-year MBS represent 80% ($73.0 billion) while 30-year TBA (to-be-announced) positions make up 15% ($13.6 billion) of the portfolio.

The detailed portfolio composition shows:

Risk Management and Hedging Approach

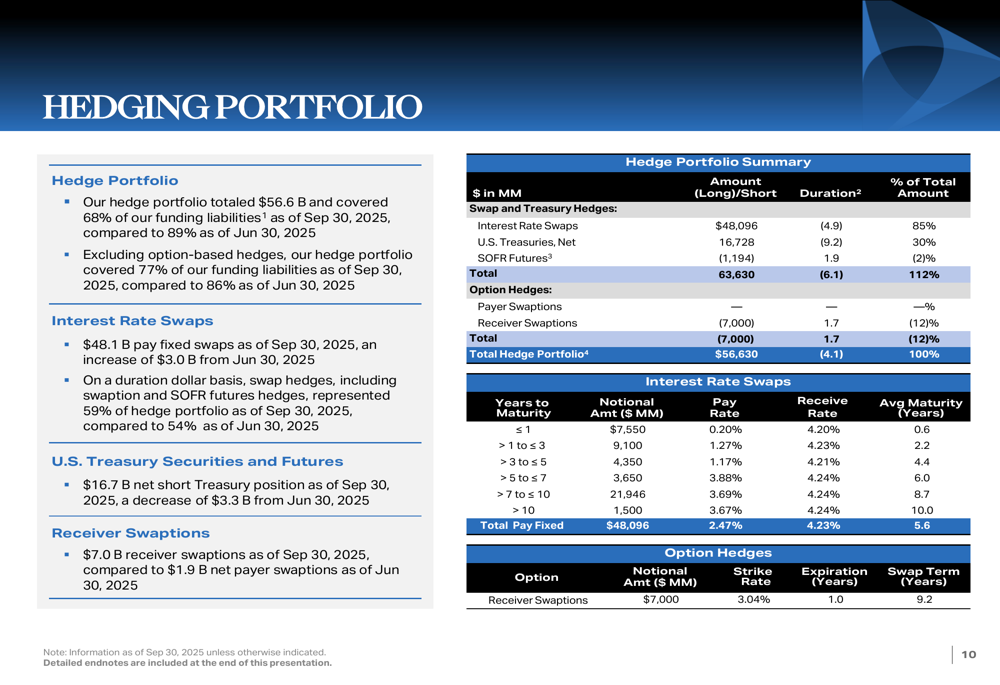

A notable strategic shift in Q3 was AGNC's decision to reduce its hedge ratio from 89% to 68% of funding liabilities. This reduction suggests management anticipates a more favorable interest rate environment ahead, potentially positioning for expected Federal Reserve rate cuts.

Despite this reduction, the company maintained a stable leverage ratio of 7.6x, indicating disciplined risk management amid portfolio growth. The duration gap increased slightly from 0.2 years to 0.3 years, still representing a relatively balanced interest rate risk profile.

The hedging portfolio details reveal:

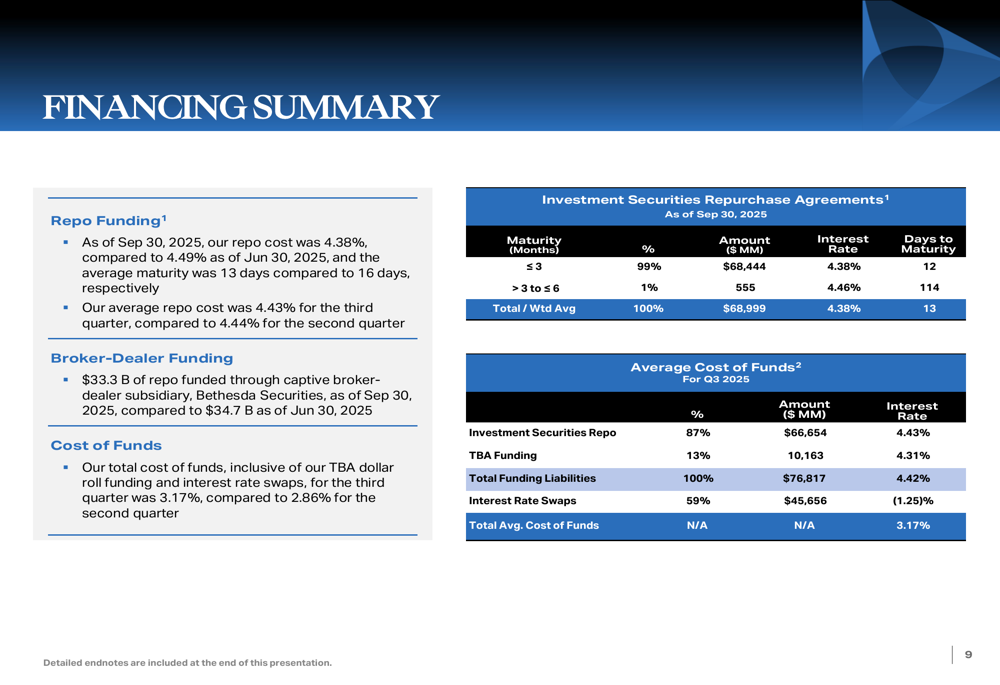

AGNC's financing structure shows a slight improvement in repo costs, decreasing from 4.49% to 4.38% quarter-over-quarter. However, the average cost of funds increased from 2.86% to 3.17%, partially offsetting the benefits of improved asset yields.

The financing summary provides additional context:

Forward-Looking Statements

AGNC maintains a strong liquidity position with $7.2 billion in unencumbered cash and agency MBS, representing 66% of tangible equity. This provides significant flexibility to navigate market volatility and capitalize on investment opportunities.

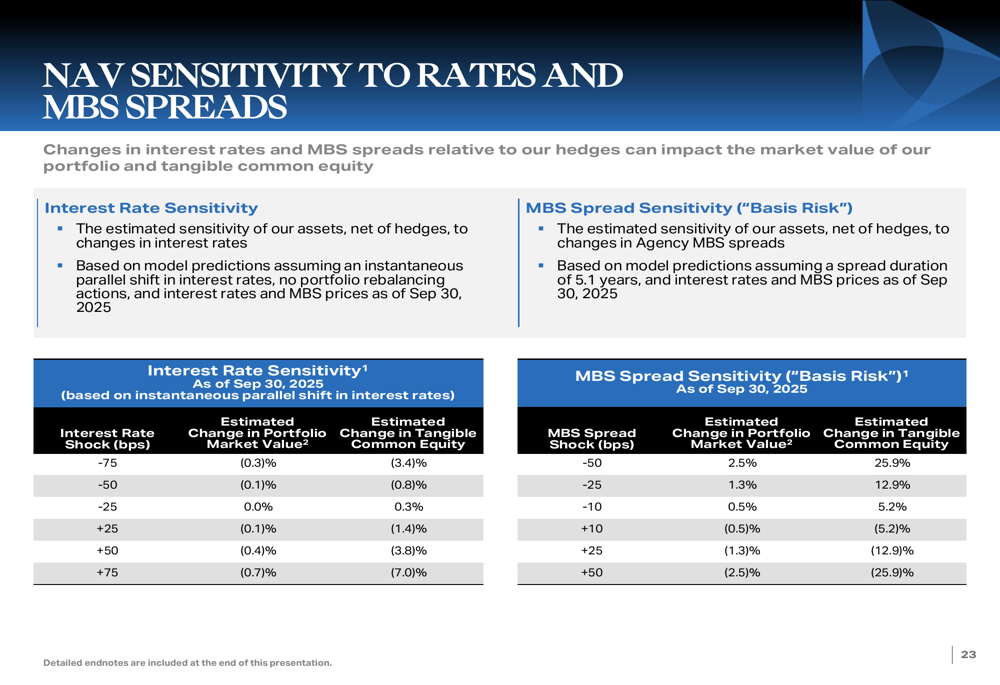

The company's sensitivity analysis to interest rates and MBS spreads indicates moderate exposure to market fluctuations:

According to the earnings call, CEO Peter Federico highlighted the company's strategic initiatives, including the launch of new indices aimed at enhancing market transparency. Management expressed optimism about moderate tailwinds to net spread income and projected an EPS of $0.40 for the next two quarters, representing an improvement over the current quarter's $0.35.

Despite the EPS miss, AGNC's strong capital position, portfolio growth, and strategic positioning suggest the company remains well-equipped to navigate the evolving mortgage market landscape while continuing to deliver substantial dividend income to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.