Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Aimia Inc. (TSX:AIM) presented its second quarter 2025 results on August 14, 2025, highlighting improved operational performance despite posting a net loss. The company’s stock closed at $3.22 on August 13, showing a 3.87% increase, reflecting positive investor sentiment ahead of the earnings presentation.

The presentation, delivered by Executive Chairman Rhys Summerton and President & CFO Steve Leonard, emphasized Aimia’s progress in its strategic transition to a permanent capital vehicle structure while showcasing improved financial metrics across its core holdings.

Quarterly Performance Highlights

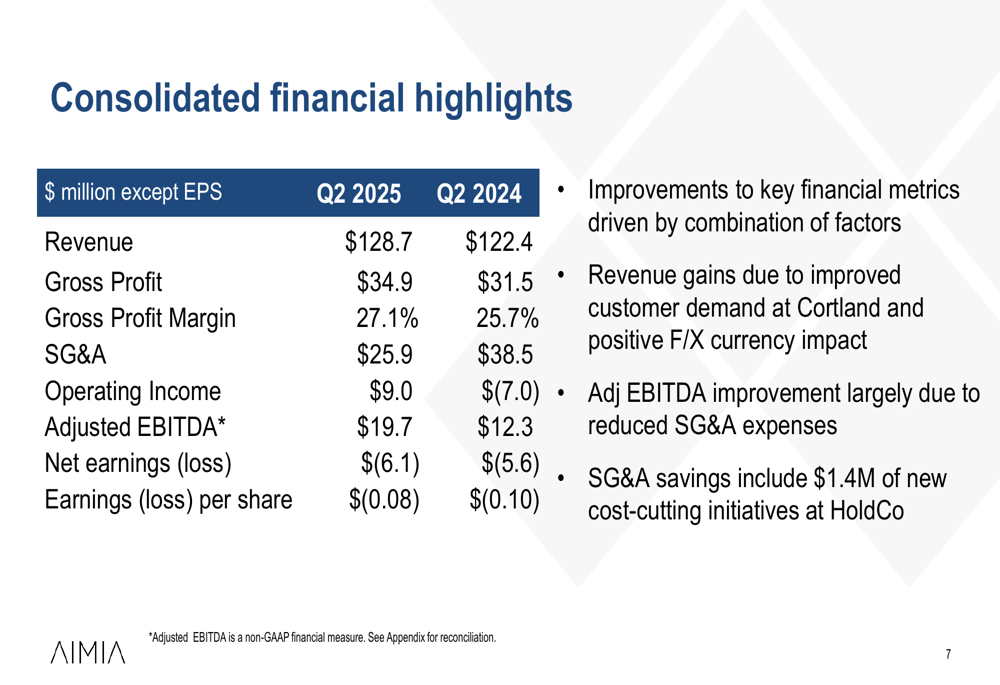

Aimia reported Q2 2025 revenue of $128.7 million, a 5.1% increase from $122.4 million in the same period last year. Gross profit rose to $34.9 million (27.1% margin) compared to $31.5 million (25.7% margin) in Q2 2024. The company achieved a significant improvement in operating income, posting $9.0 million versus a $7.0 million loss in the prior year.

As shown in the following consolidated financial highlights:

Despite the operational improvements, Aimia reported a net loss of $6.1 million or $0.08 per share, compared to a $5.6 million loss or $0.10 per share in Q2 2024. Adjusted EBITDA, a key metric for the company, increased substantially to $19.7 million from $12.3 million in the prior year period, driven primarily by reduced SG&A expenses, which fell to $25.9 million from $38.5 million.

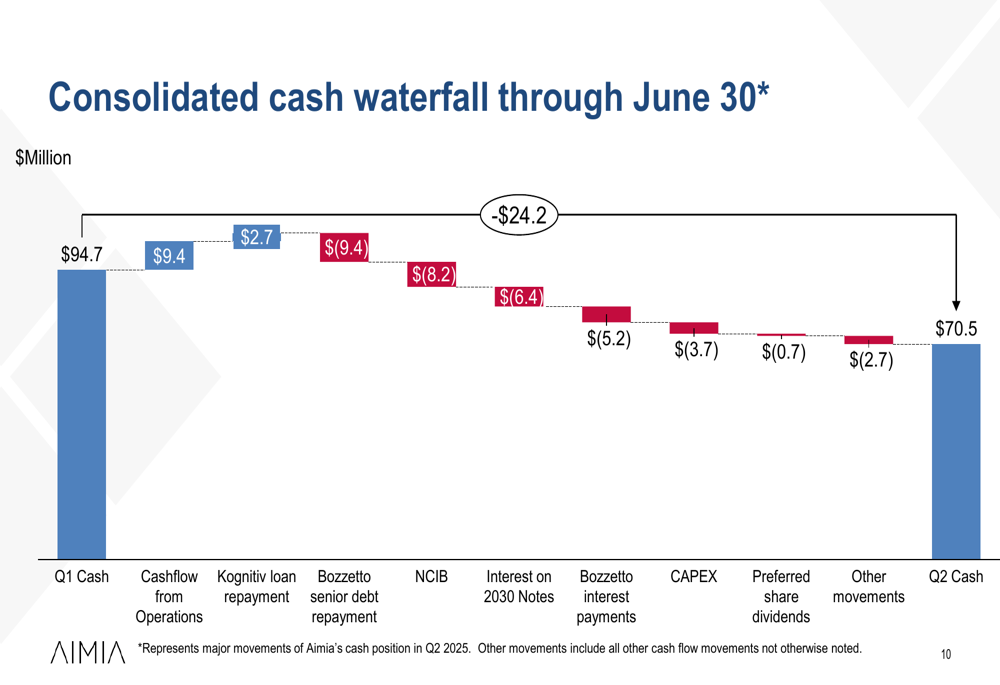

The company’s cash position stood at $70.5 million at the end of Q2, with liquidity distributed across Cortland ($10.2 million), Bozzetto ($36.9 million), and HoldCo ($23.4 million). This represents a decrease from the $94.7 million reported at the end of Q1 2025, primarily due to debt repayments, share repurchases, and interest payments.

The following chart illustrates the company’s cash movements during the quarter:

Segment Performance Analysis

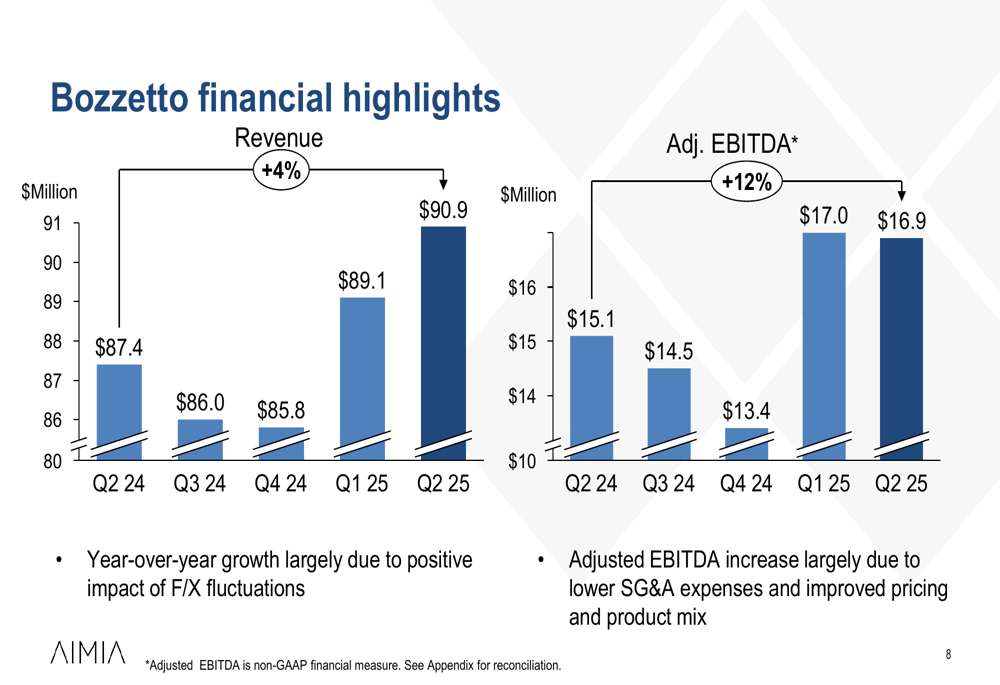

Bozzetto, one of Aimia’s core holdings, delivered revenue of $90.9 million in Q2 2025, a 4% increase from $87.4 million in Q2 2024. Adjusted EBITDA grew 12% to $16.9 million, with an improved margin of 18.6% compared to 17.3% in the prior year. Management attributed the growth to positive foreign exchange impacts and improved pricing and product mix.

The following chart shows Bozzetto’s financial performance over the past five quarters:

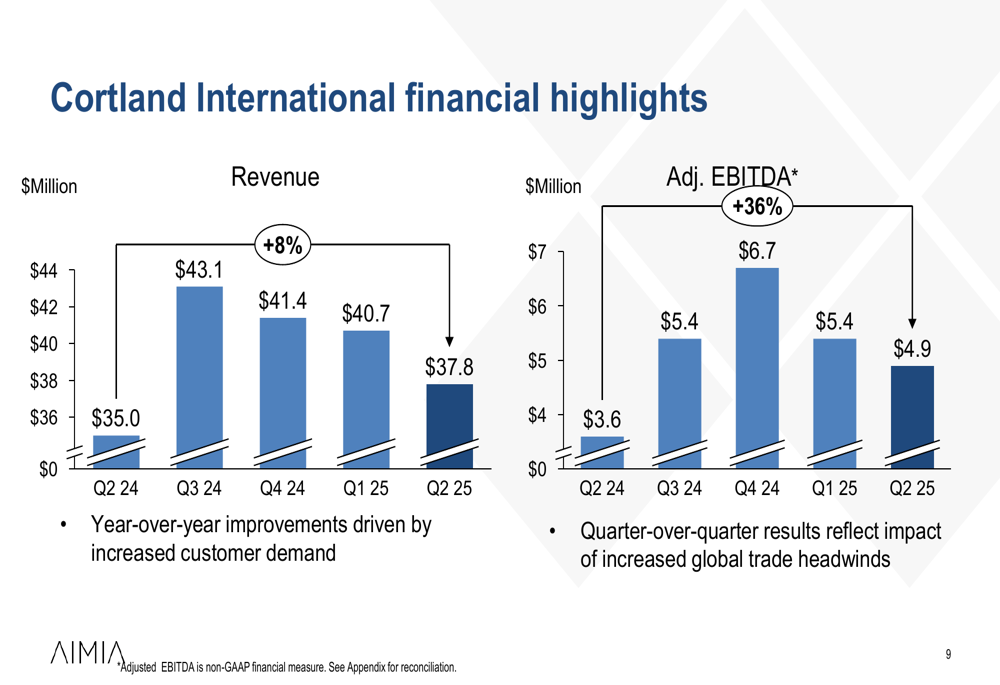

Cortland International also showed strong year-over-year improvements, with revenue increasing 8% to $37.8 million and Adjusted EBITDA rising 36% to $4.9 million in Q2 2025. The Adjusted EBITDA margin expanded to 13.0% from 10.3% in Q2 2024. However, management noted that quarter-over-quarter results reflect the impact of increased global trade headwinds.

As illustrated in Cortland’s financial highlights:

Strategic Initiatives & Capital Allocation

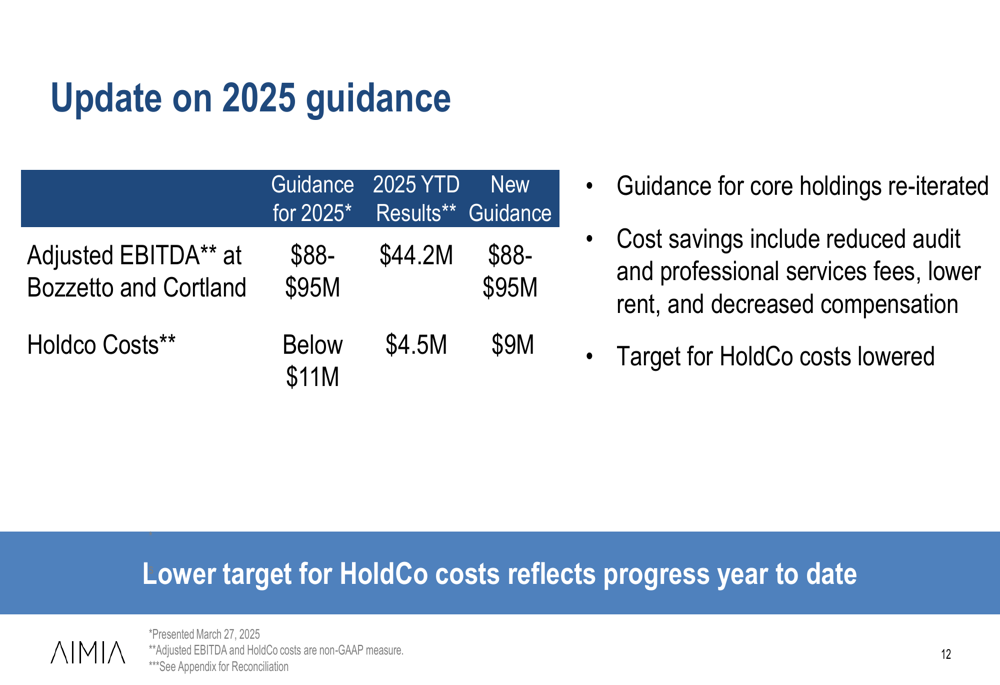

Aimia reaffirmed its 2025 Adjusted EBITDA guidance for Bozzetto and Cortland at $88-$95 million, with year-to-date results at $44.2 million. Notably, the company lowered its HoldCo cost guidance from "below $11 million" to "$9 million" for 2025, with year-to-date costs at $4.5 million. The reduced guidance reflects cost-cutting initiatives including lower audit and professional services fees, reduced rent, and decreased compensation.

The updated guidance is presented in the following table:

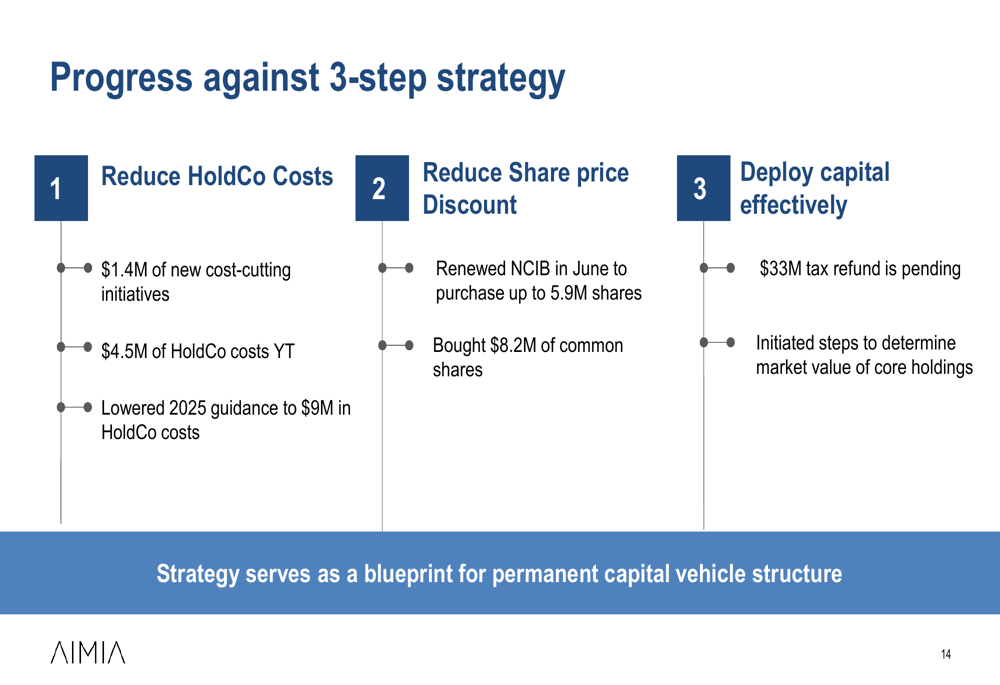

The company continues to execute its three-step strategy focused on reducing HoldCo costs, reducing share price discount, and deploying capital effectively. As part of this strategy, Aimia renewed its Normal Course Issuer Bid (NCIB) through June 2026 to purchase up to 5.9 million shares and has already bought back $8.2 million worth of common shares.

The progress against the company’s three-step strategy is outlined below:

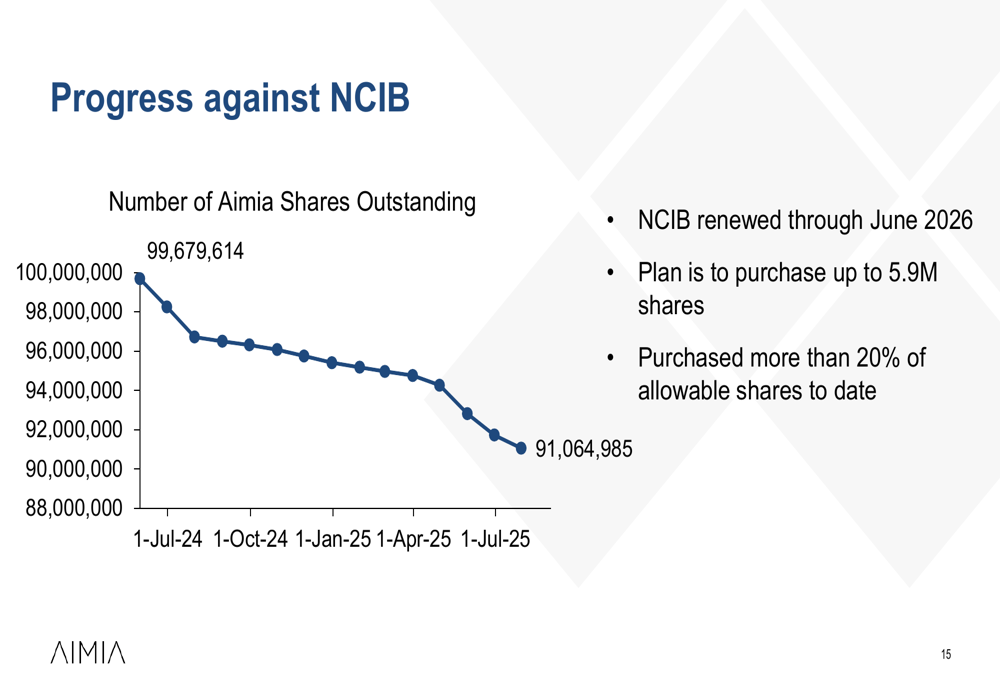

The NCIB program has resulted in a significant reduction in outstanding shares, from 99,679,614 in July 2024 to 91,064,985 in July 2025, as shown in the following chart:

Forward-Looking Statements

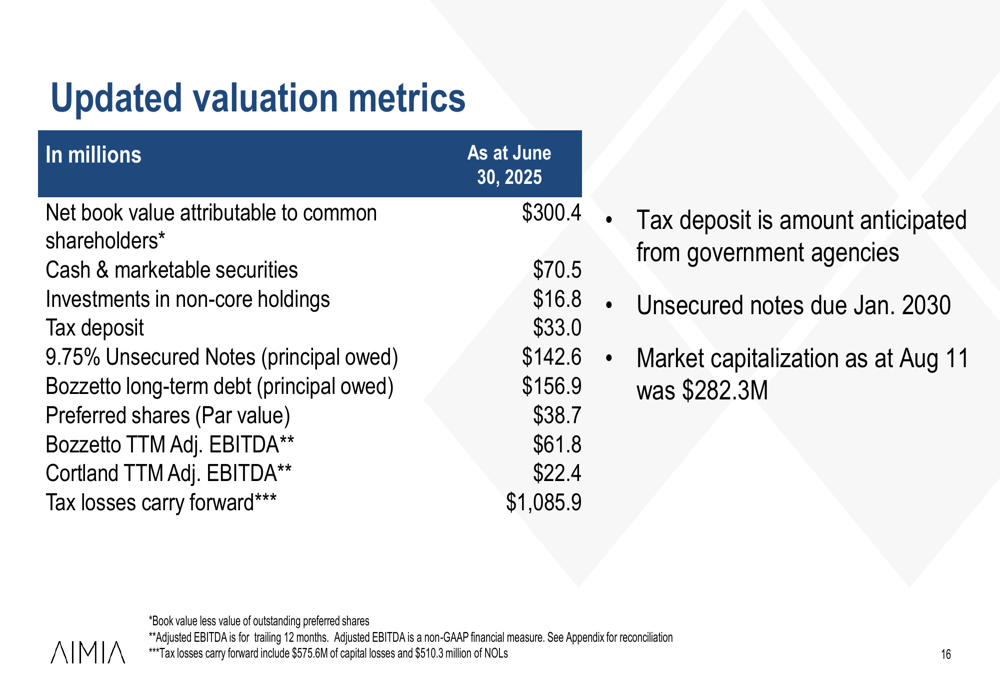

Aimia highlighted several key developments that will impact its future performance, including an expected $33 million tax refund following a settlement with the Canada Revenue Agency (CRA). The company also provided updated valuation metrics, including a net book value attributable to common shareholders of $300.4 million and significant tax losses carried forward of $1,085.9 million.

The company’s valuation metrics as of June 30, 2025, are presented below:

Looking ahead, Aimia’s priorities include achieving its financial guidance, further reducing HoldCo costs, and completing the NCIB program. Management also noted that efforts are underway to determine the market value of core holdings as part of its transition into a permanent capital vehicle.

The presentation emphasized that Q2 2025 was a period of transition for Aimia, marked by progress against its strategic initiatives and continued momentum in its core holdings. While the company has shown operational improvements and cost reductions, investors will be watching closely to see if these efforts translate into consistent profitability in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.