S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

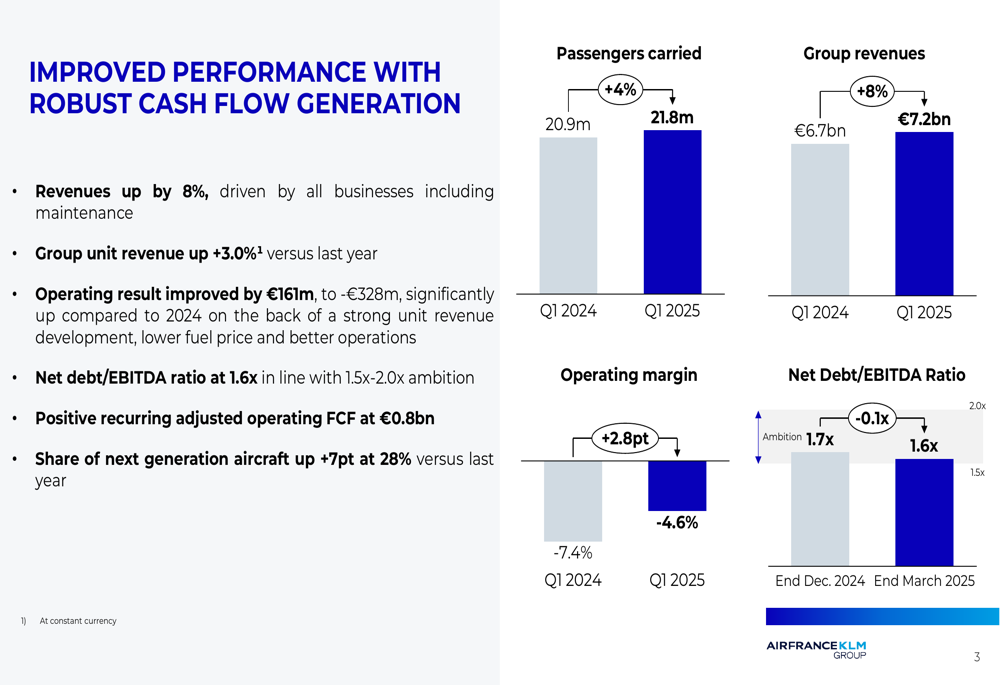

Air France-KLM (EURONEXT:AF) presented its first quarter 2025 results on April 30, showing significant improvement in operating performance despite the traditionally challenging winter season for European airlines. The Franco-Dutch carrier reported an 8% increase in revenues to €7.2 billion, while narrowing its operating loss by €161 million compared to the same period last year.

The airline group continues to benefit from robust travel demand, particularly in premium segments, even as it navigates ongoing geopolitical and economic uncertainties. Europe remains an attractive destination for international travelers, with France positioned as a particularly strong inbound market.

As shown in the following chart highlighting key performance metrics, the group carried 21.8 million passengers in Q1, representing a 4% increase year-over-year:

Quarterly Performance Highlights

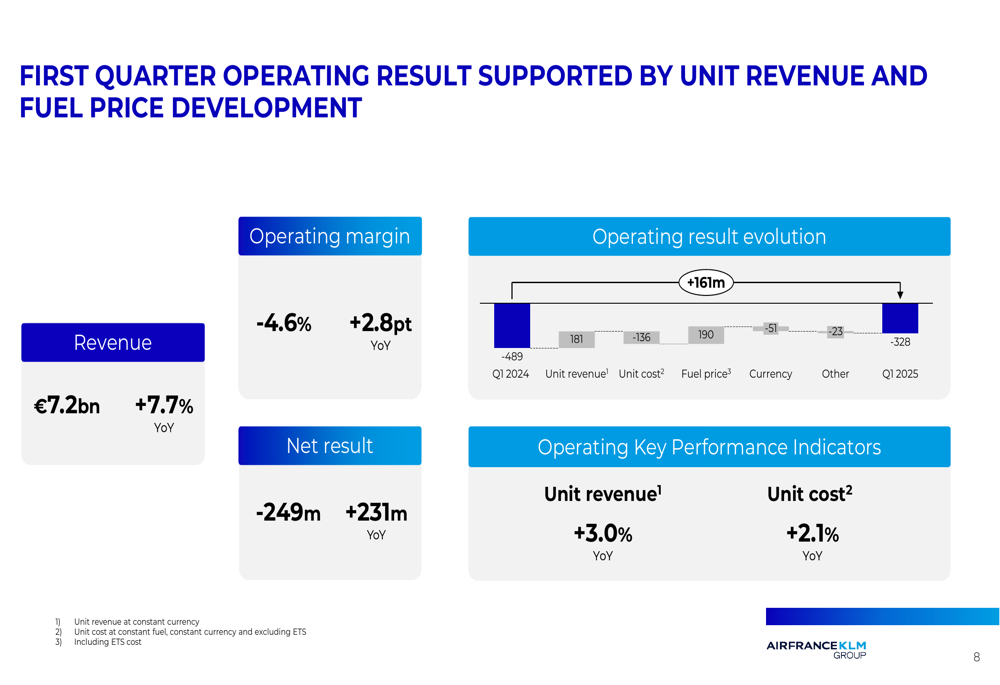

Air France-KLM reported an operating result of -€328 million for Q1 2025, a substantial improvement from the -€489 million recorded in Q1 2024. This performance was driven by a 3.0% increase in unit revenue, partially offset by a 2.1% rise in unit costs. The operating margin improved by 2.8 percentage points to -4.6%.

The company’s financial performance benefited from favorable fuel price developments and positive currency effects, as illustrated in the following breakdown:

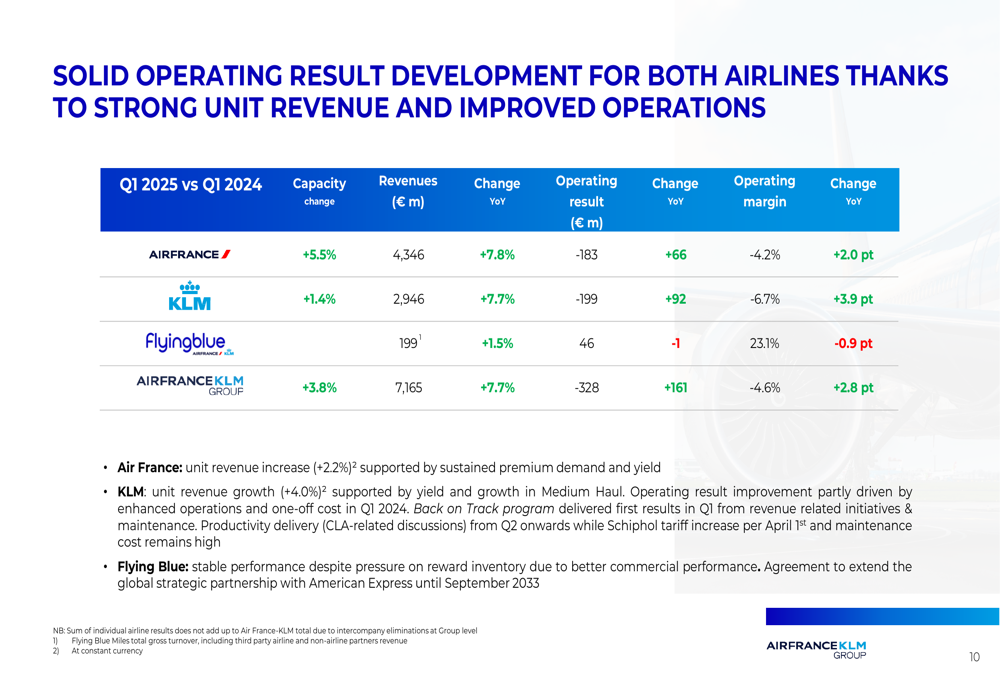

Both airlines within the group showed solid operating result development. Air France improved its operating margin by 2.0 percentage points to -4.2%, while KLM saw a more significant improvement of 3.9 percentage points, though its operating margin remained lower at -6.7%. The group’s loyalty program, Flying Blue, maintained a strong 23.1% operating margin despite a slight 0.9 percentage point decline.

The following chart details the performance of both airlines and Flying Blue:

Detailed Financial Analysis

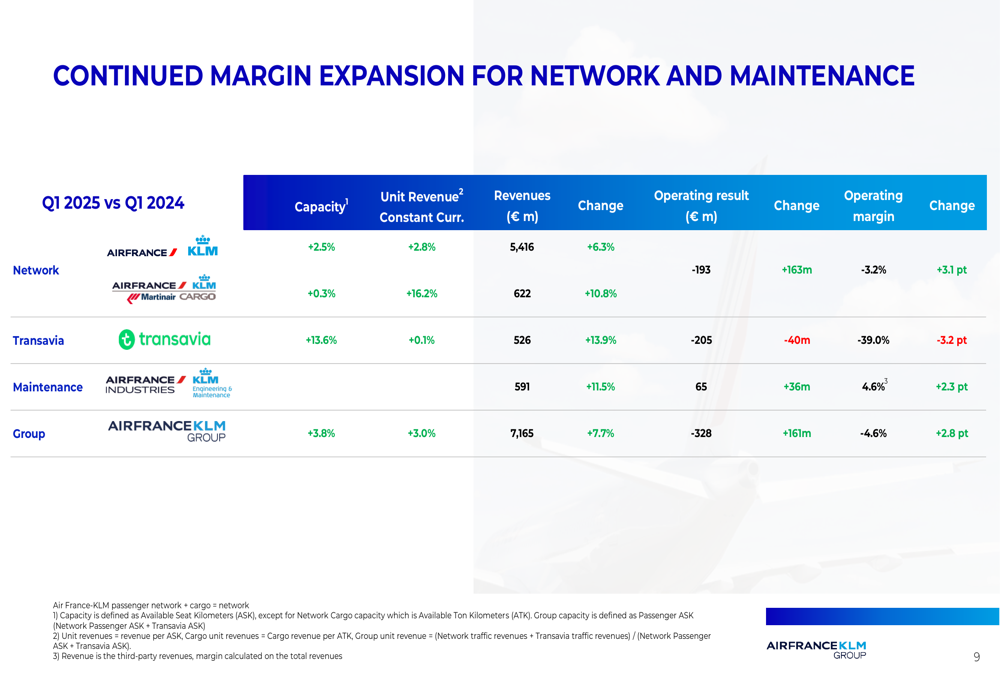

The Network business (passenger and cargo operations of Air France and KLM) showed strong improvement, with an operating margin increase of 3.1 percentage points to -3.2%. Cargo unit revenue was particularly strong, up 16.2% year-over-year.

Transavia, the group’s low-cost carrier, expanded capacity by 13.6% but saw its operating margin deteriorate by 3.2 percentage points to -39.0%. Meanwhile, the Maintenance business continued to perform well with an operating margin of 4.6%, up 2.3 percentage points from last year.

As shown in the following segment breakdown, the Network and Maintenance businesses drove the overall margin improvement:

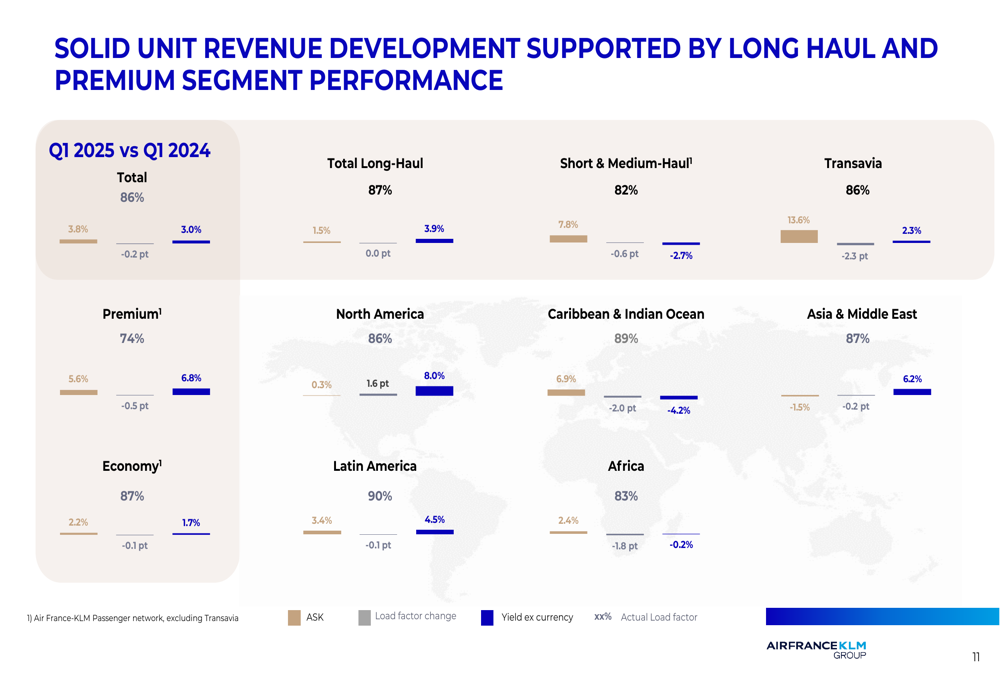

Unit revenue development was positive across most regions, with particularly strong performance in the Caribbean & Indian Ocean (+6.9%) and Short & Medium-Haul (+7.8%) segments. The Premium cabin segment also performed well with a 5.6% increase in unit revenue, underscoring the success of the group’s premiumization strategy.

The following geographical breakdown illustrates the unit revenue development across regions:

Strategic Initiatives

Air France-KLM continues to advance its premiumization strategy, most notably with the launch of its new La Première luxury cabin on April 8, 2025. This ultra-premium product features a day bed and armchair that transforms into a full flat bed, five windows providing 3.5m² of space (25% larger than previous versions), and the option for complete privatization with a double suite.

The new La Première cabin represents the pinnacle of the group’s premium offerings and is designed to create a halo effect across the brand, as illustrated below:

The group is also making progress on its sustainability commitments, increasing the share of next-generation aircraft in its fleet by 7 percentage points to 28% compared to last year. This fleet modernization is a key component of the company’s decarbonization strategy, alongside its increased use of sustainable aviation fuel (SAF).

Forward-Looking Statements

Despite current market uncertainties, Air France-KLM maintained its outlook for 2025, projecting capacity growth of 4-5% compared to 2024. The company expects unit costs to increase in the low single digits and plans net capital expenditure of €3.2-3.4 billion, with approximately 80% allocated to fleet renewal and related investments.

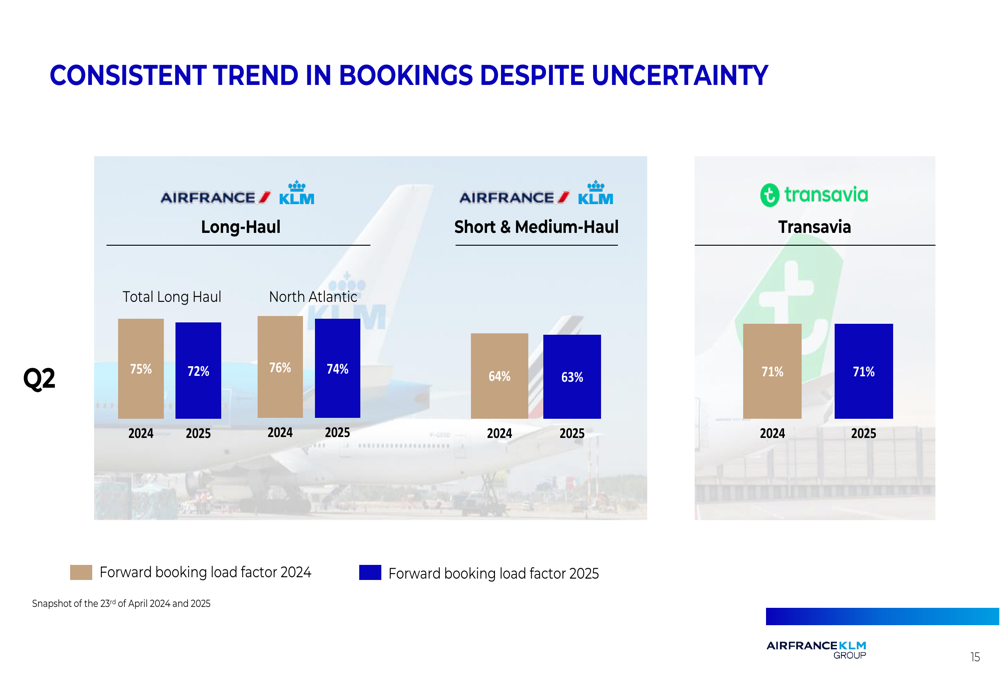

The group’s forward booking trends remain consistent with previous years, as shown in the following chart comparing load factors:

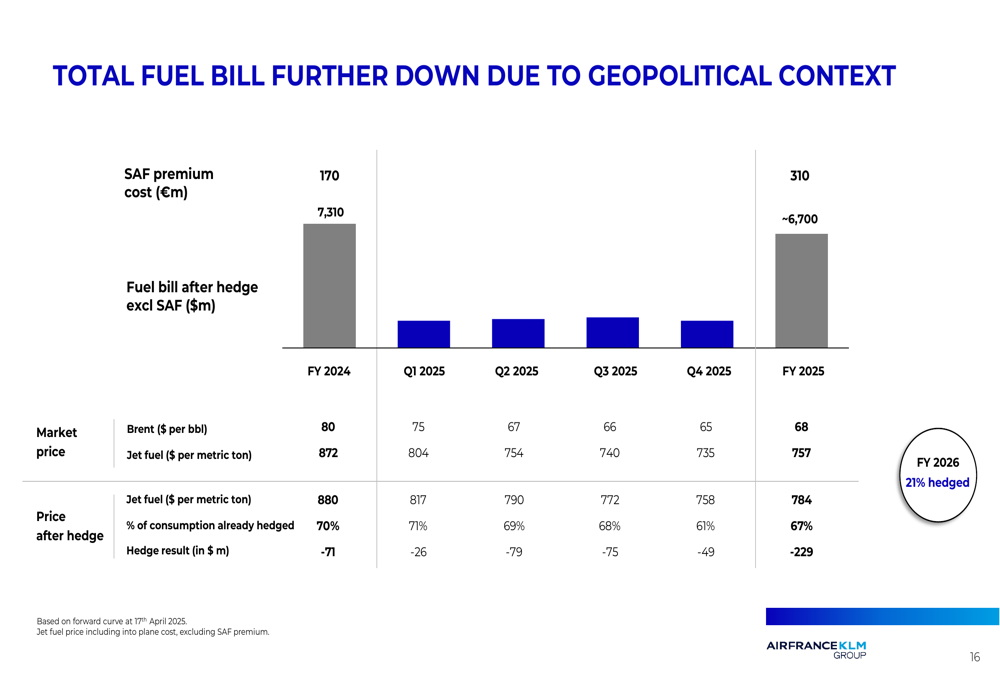

Air France-KLM expects to benefit from lower fuel costs in 2025, with its fuel bill after hedging (excluding SAF) projected to decrease from $7.31 billion in 2024 to approximately $6.7 billion in 2025. The company has hedged 67% of its fuel consumption for the full year 2025 and 21% for 2026.

The following chart details the projected fuel costs and hedging positions:

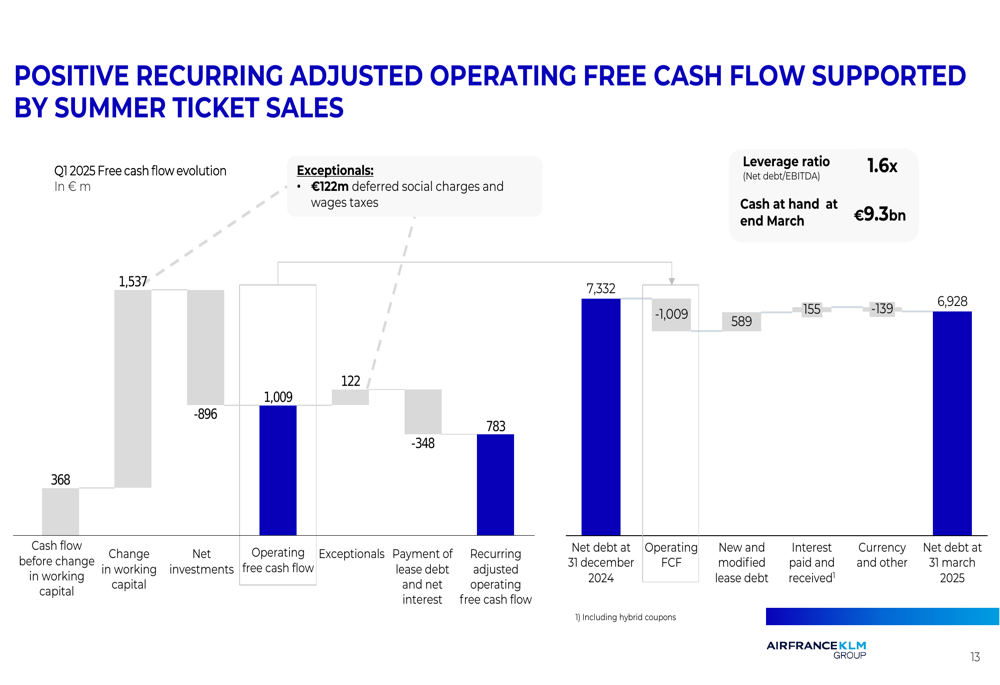

The company generated a positive recurring adjusted operating free cash flow of €783 million in Q1 2025, supported by strong summer ticket sales. This contributed to a reduction in net debt from €7.33 billion at the end of December 2024 to €6.93 billion at the end of March 2025, maintaining a net debt to EBITDA ratio of 1.6x, within the target range of 1.5x to 2.0x.

The following cash flow breakdown illustrates the key components contributing to this positive performance:

In conclusion, Air France-KLM’s Q1 2025 results demonstrate the company’s ability to improve performance even during the traditionally challenging winter season. With a robust summer booking outlook, ongoing fleet modernization, and premium product enhancements, the group appears well-positioned to continue its recovery trajectory despite macroeconomic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.