Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Air France-KLM (EURONEXT:AF) reported strong second-quarter results for 2025, with revenue growth of 6.2% and significant margin expansion. The airline group’s stock responded positively, closing up 3.26% at €11.335 following the July 31 earnings presentation. The results demonstrate the company’s successful implementation of its premiumization strategy and operational improvements, particularly at Air France, while KLM continues to face cost challenges.

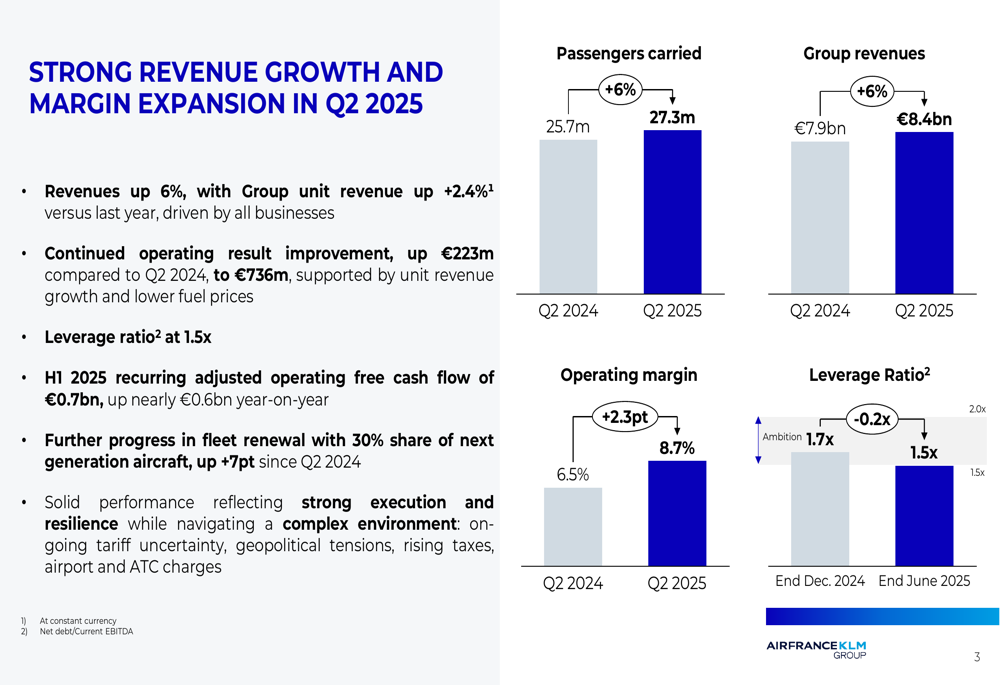

The airline group transported 27.3 million passengers in Q2 2025, representing a 6% increase compared to the same period last year, as travel demand remained robust across most regions despite ongoing economic uncertainties.

Quarterly Performance Highlights

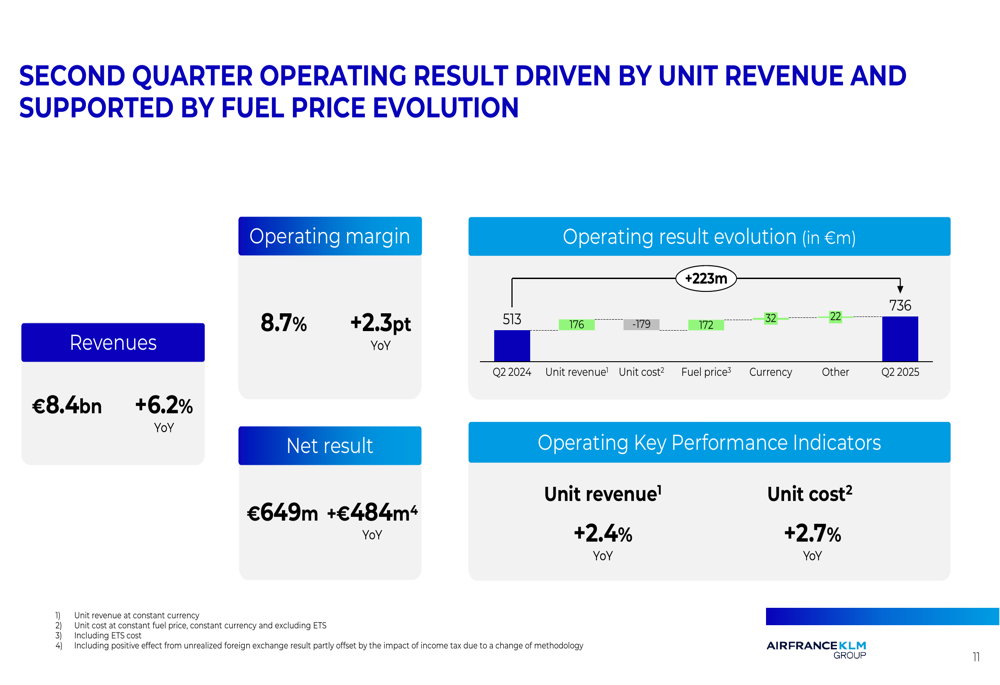

Air France-KLM reported revenues of €8.4 billion in Q2 2025, up 6.2% year-over-year, while the operating result improved by €223 million to reach €736 million. This translated to an operating margin of 8.7%, representing a significant 2.3 percentage point improvement from Q2 2024.

As shown in the following chart, both passenger numbers and group revenues showed strong 6% growth compared to the previous year:

The improved operating result was primarily driven by stronger unit revenue and favorable fuel price evolution, which helped offset increasing unit costs. The net result for the quarter reached €649 million, representing a substantial €484 million improvement year-over-year.

The following breakdown illustrates the key factors contributing to the operating result evolution:

Segment Performance Analysis

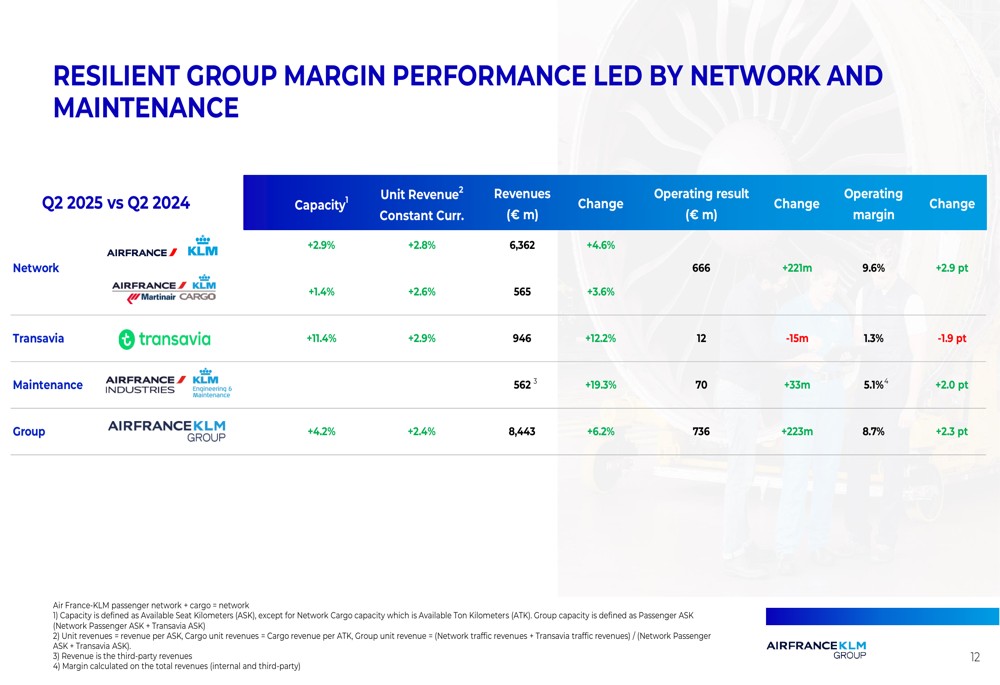

Performance across the group’s business segments was mixed, with Network and Maintenance operations showing strong improvements while Transavia experienced margin pressure. The Network business, which includes Air France and KLM’s passenger operations, delivered a 9.6% operating margin, up 2.9 percentage points year-over-year.

The detailed segment performance is illustrated in this table:

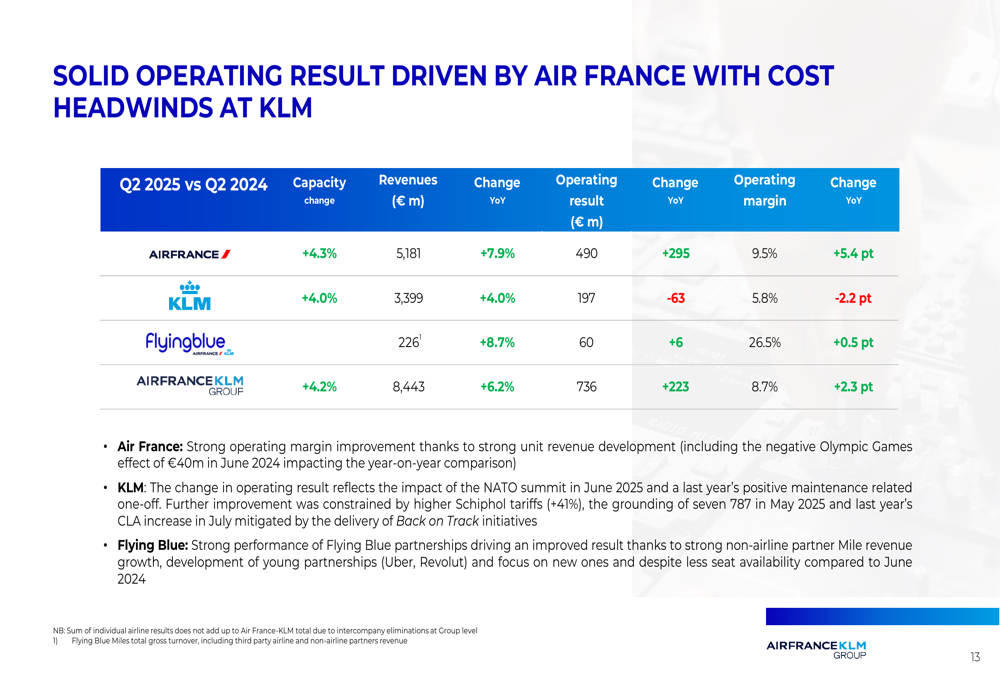

Notably, Air France significantly outperformed KLM in the quarter. Air France achieved a 9.5% operating margin (up 5.4 percentage points), while KLM’s margin declined to 5.8% (down 2.2 percentage points) due to cost headwinds. The Flying Blue loyalty program continued to deliver strong profitability with a 26.5% operating margin.

This performance divergence between the two main airlines is clearly shown in the following breakdown:

To address KLM’s challenges, management highlighted the "Back on Track" program, which has already delivered €185 million in benefits during the first half of 2025 and remains on track to achieve its €450 million target for the full year despite headwinds.

Strategic Initiatives

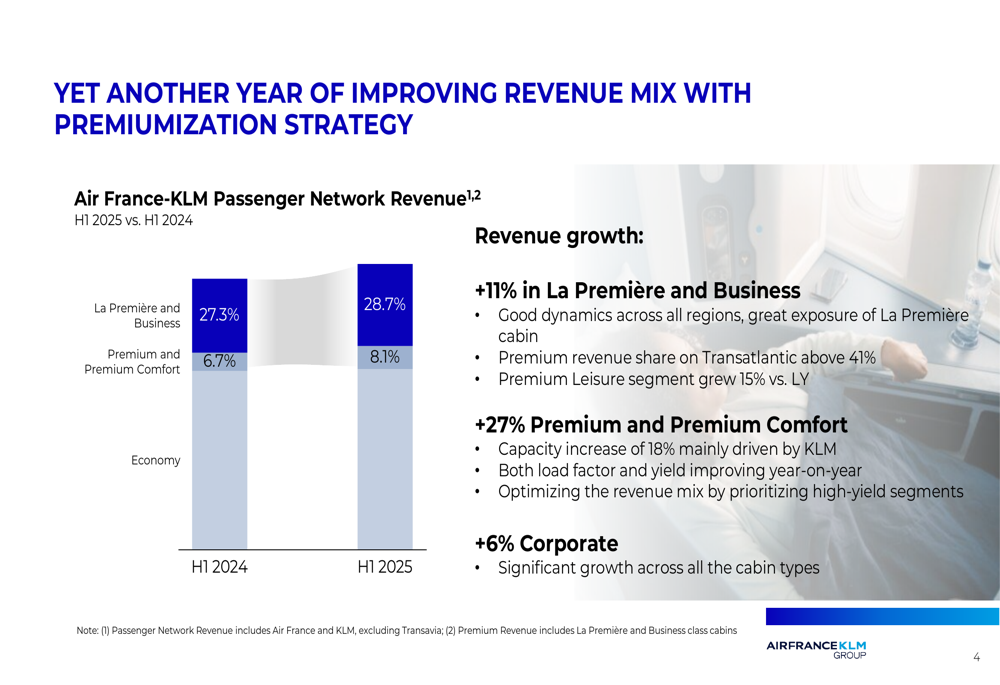

Air France-KLM’s premiumization strategy continues to gain traction, with La Premiere and Business class revenue increasing to 28.7% of passenger network revenue (up from 27.3% in H1 2024), while Premium and Premium Comfort classes grew to 8.1% (from 6.7%). This shift toward higher-yielding segments is helping drive revenue growth and margin expansion.

The following chart illustrates this improving revenue mix:

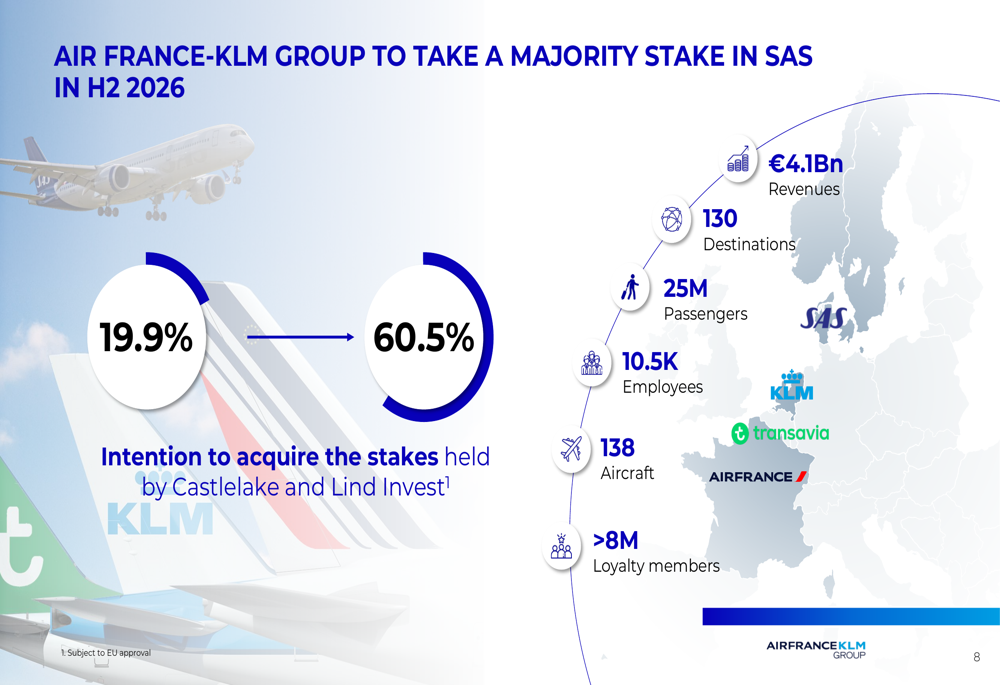

The group is also expanding its global footprint through strategic partnerships and acquisitions. Most notably, Air France-KLM plans to take a majority stake in SAS in the second half of 2026, which will add €4.1 billion in revenues, 130 destinations, and 25 million passengers to the group.

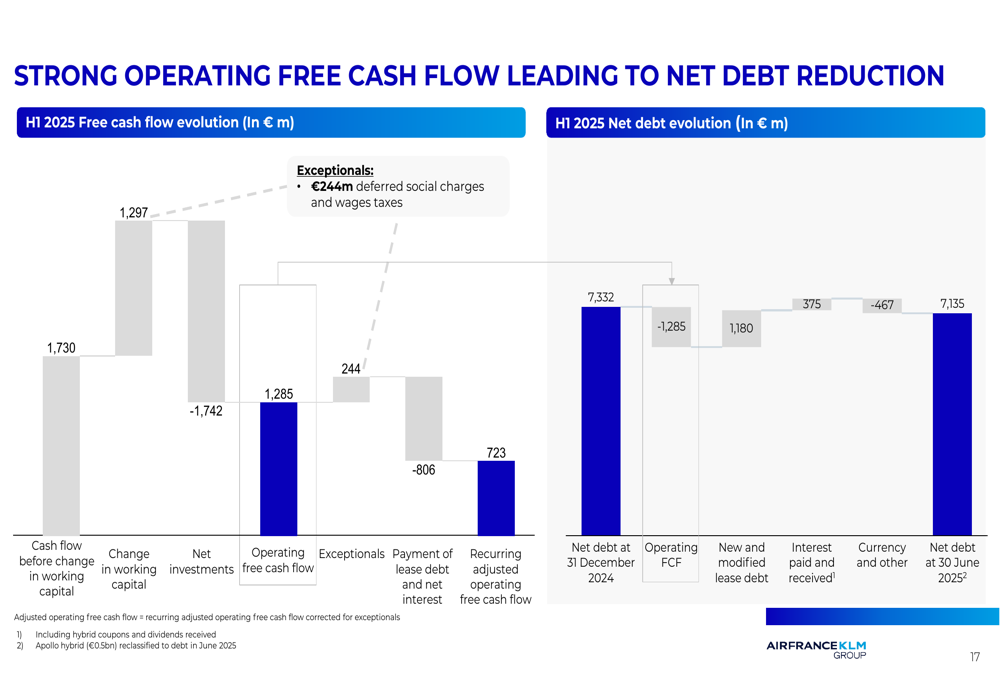

Financial discipline remains a priority, with the group reporting strong operating free cash flow that has contributed to net debt reduction. The leverage ratio improved to 1.5x (from 1.7x), moving closer to the company’s target of achieving an investment-grade rating.

Outlook and Guidance

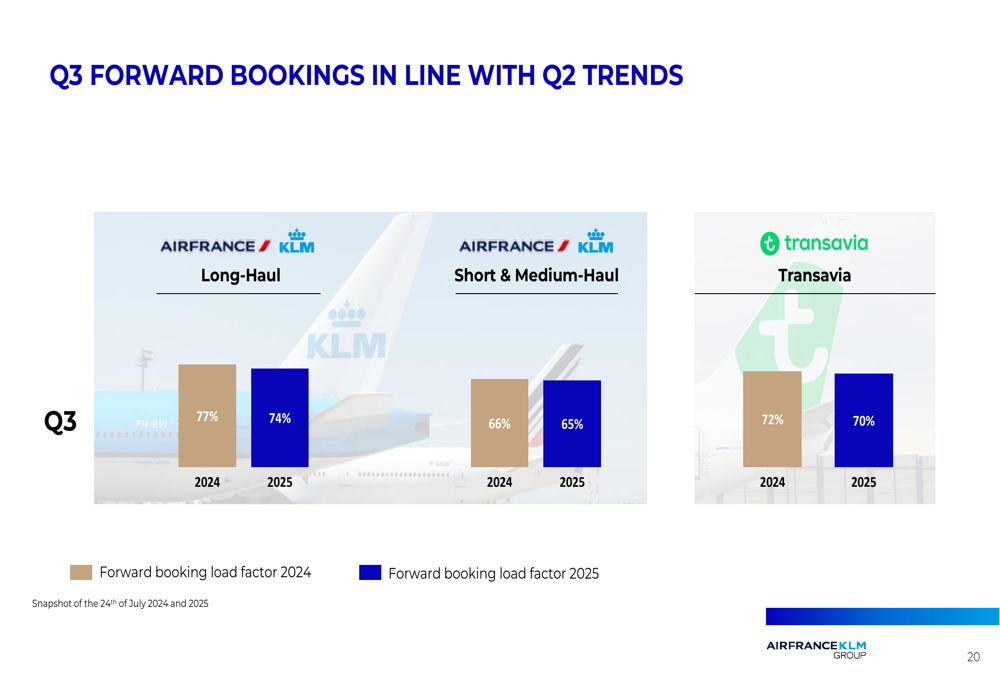

For the third quarter, forward bookings are slightly below last year’s levels but remain in line with Q2 trends. Long-haul bookings stand at 74% (versus 77% last year), while Short & Medium-Haul and Transavia bookings are at 65% and 70% respectively (compared to 66% and 72% in 2024).

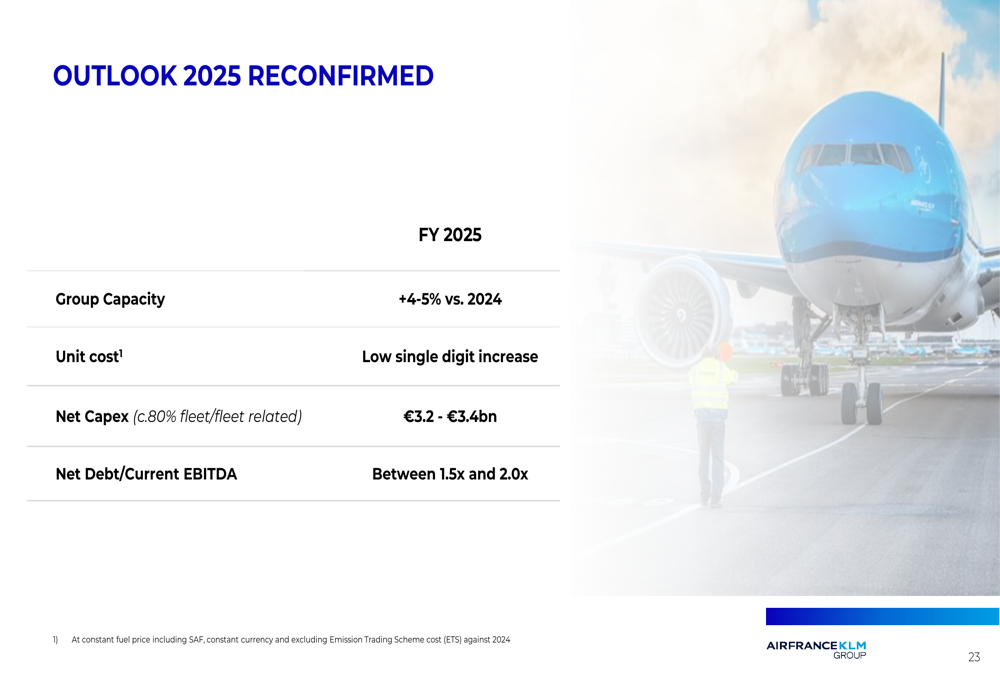

Air France-KLM reconfirmed its outlook for 2025, maintaining guidance for capacity growth of 4-5% compared to 2024, with unit costs expected to increase in the low single digits. Capital expenditures are projected at €3.2-3.4 billion, with approximately 80% allocated to fleet and fleet-related investments.

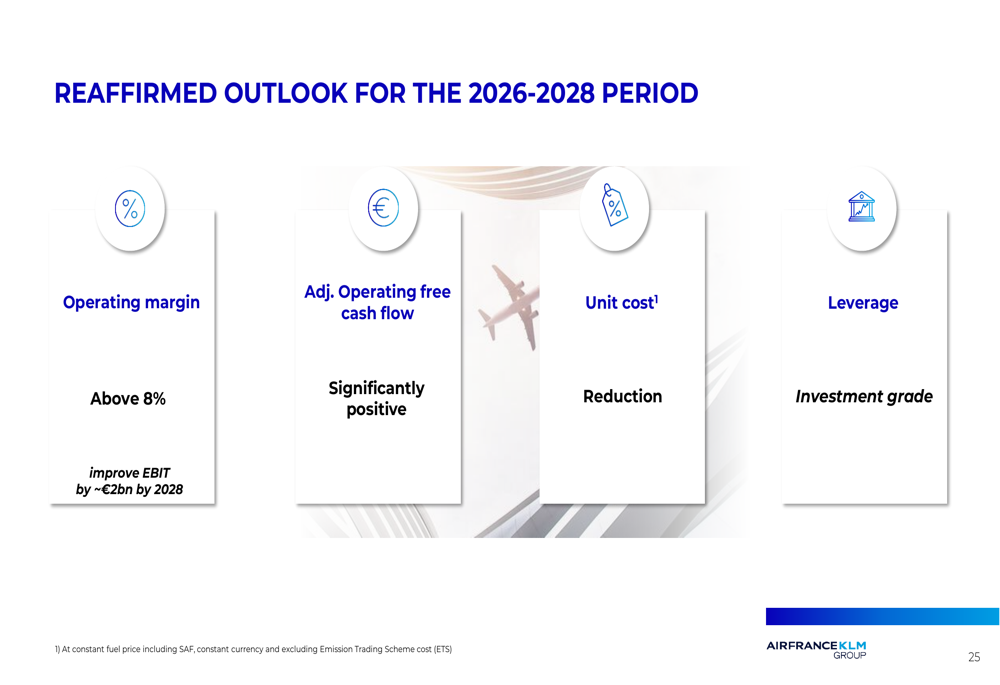

Looking further ahead, the group reaffirmed its medium-term targets for 2026-2028, which include achieving an operating margin above 8% and improving EBIT by approximately €2 billion by 2028. Management remains focused on unit cost reduction, generating significantly positive adjusted operating free cash flow, and reaching an investment-grade leverage ratio.

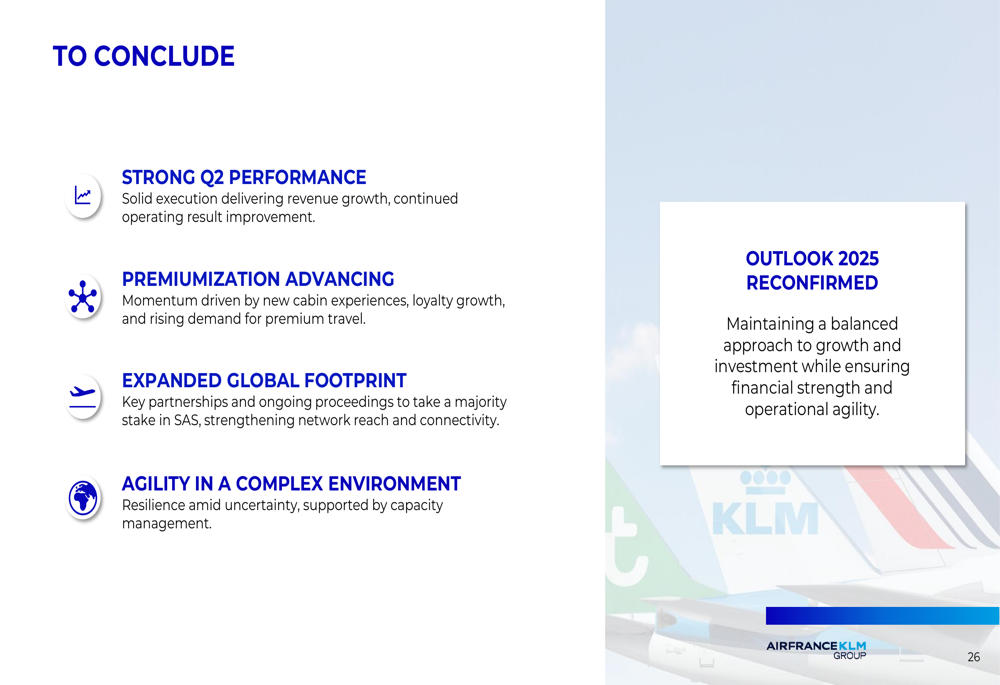

In conclusion, Air France-KLM’s Q2 2025 results demonstrate the company’s progress in implementing its strategic priorities while navigating a complex operating environment. The successful premiumization strategy, expanding global footprint, and focus on financial discipline have contributed to strong performance, particularly at Air France, though challenges remain at KLM. As the group continues to balance growth with investment, it appears well-positioned to achieve its medium-term financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.