Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

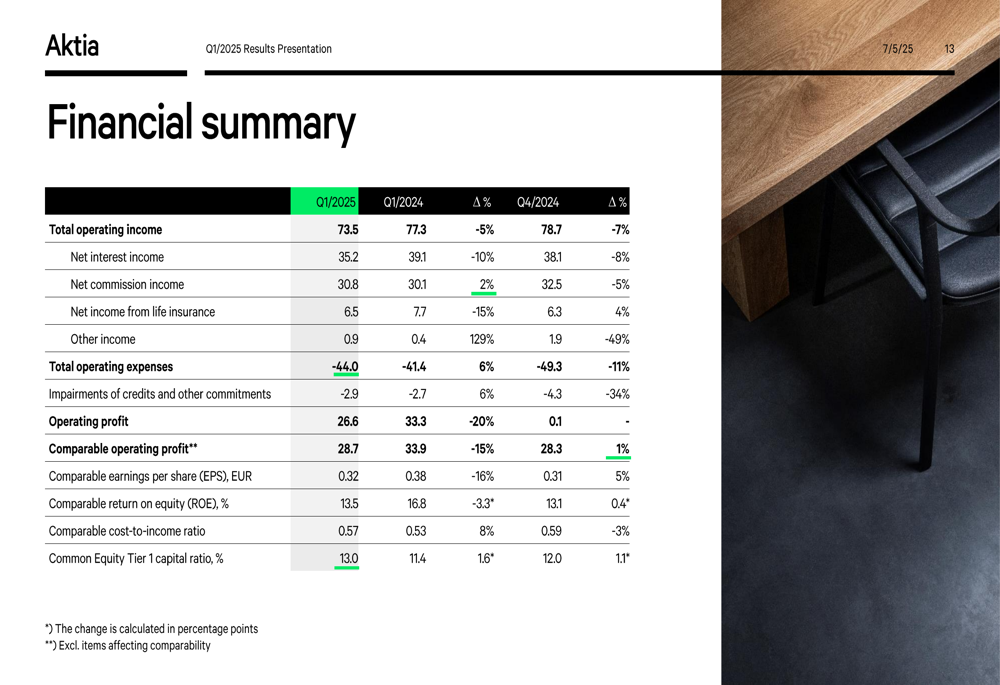

Aktia Bank Abp (HEL:AKTIA) reported a 15% year-over-year decline in comparable operating profit for the first quarter of 2025, as the Finnish financial services provider navigated a challenging interest rate environment. The bank’s shares closed at €9.87 on May 6, 2025, down 0.6% ahead of the earnings presentation.

The Q1 results, presented by CEO Aleksi Lehtonen and CFO Sakari Järvelä on May 7, 2025, revealed that while profits declined compared to the strong first quarter of 2024, they showed a slight improvement over Q4 2024, suggesting some stabilization despite market headwinds.

Quarterly Performance Highlights

Aktia reported a comparable operating profit of €28.7 million for Q1 2025, down 15% from €33.9 million in Q1 2024, but up 1% from €28.3 million in Q4 2024. The company attributed this performance primarily to lower interest rates impacting net interest income.

As shown in the following comprehensive financial summary, total operating income decreased by 5% year-over-year to €73.5 million:

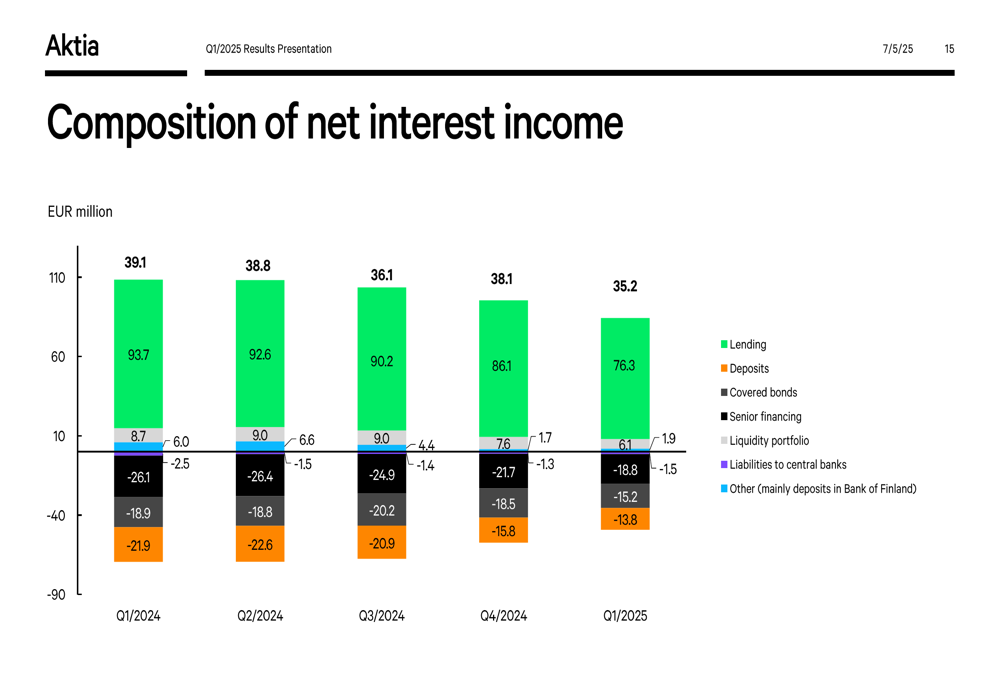

Net interest income, a key revenue driver for the bank, fell 10% year-over-year to €35.2 million, reflecting the impact of lower market rates. The composition of net interest income shows how various components have evolved over recent quarters:

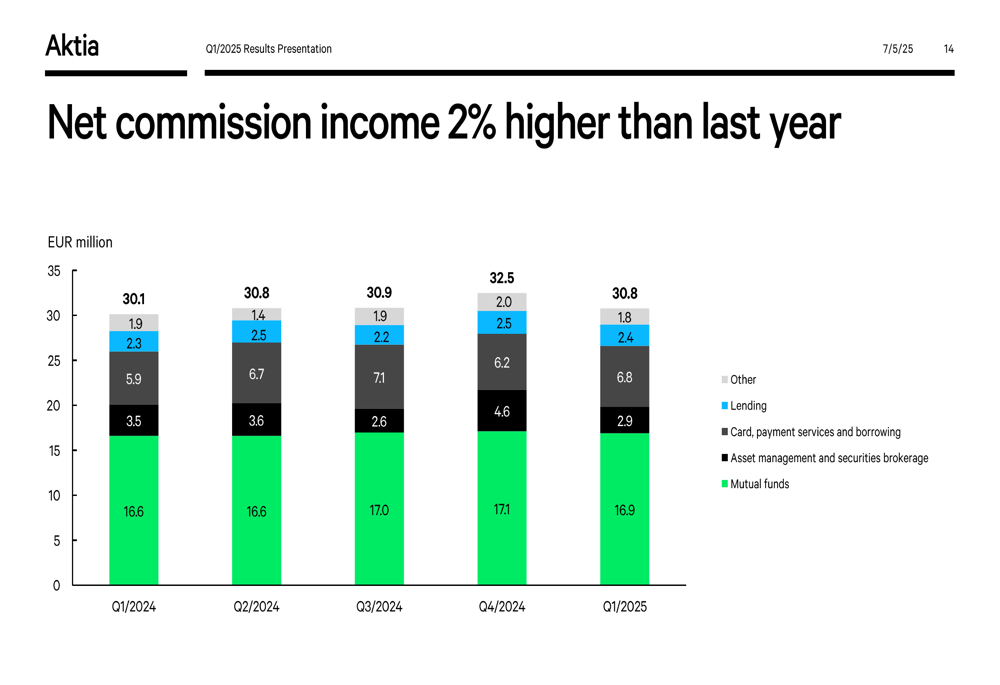

Despite challenges in the interest rate environment, Aktia’s net commission income showed resilience, growing 2% year-over-year to €30.8 million. This positive development was primarily driven by mutual funds, which contributed €16.9 million to the total:

Strategic Initiatives

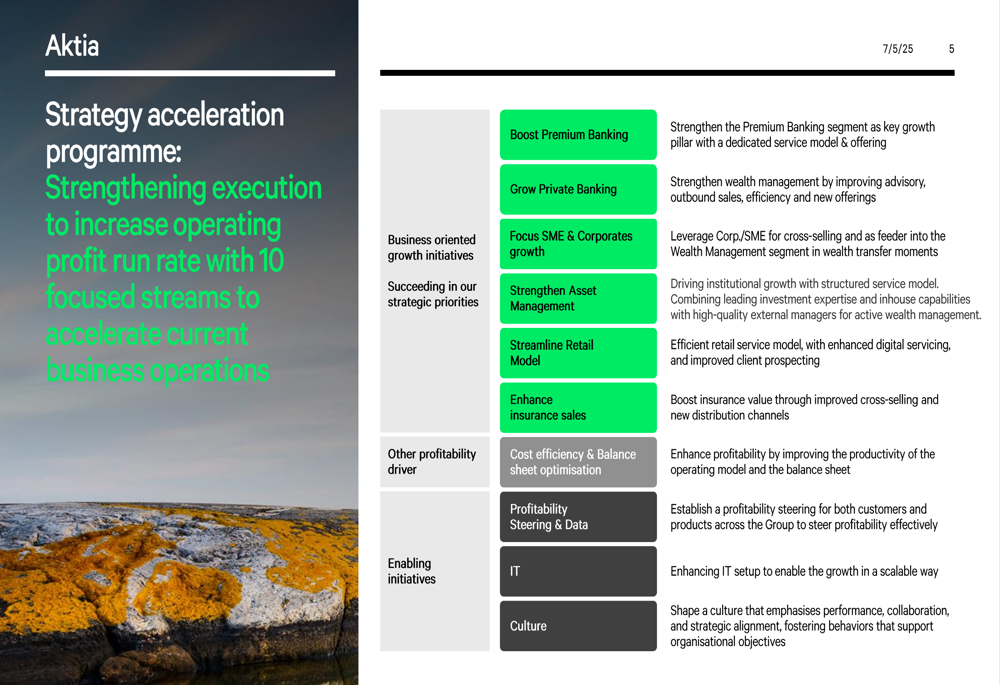

Aktia continues to position itself as "the leading wealth manager empowered by a strong banking heritage," with a mission to "democratise private banking services and build wealth for customers and society." The bank has launched a strategy acceleration program with 10 focused streams to drive growth and enhance profitability.

The strategy acceleration program includes several business-oriented growth initiatives focused on boosting Premium Banking, growing Private Banking, focusing on SME & Corporate growth, strengthening Asset Management, and streamlining the Retail Model:

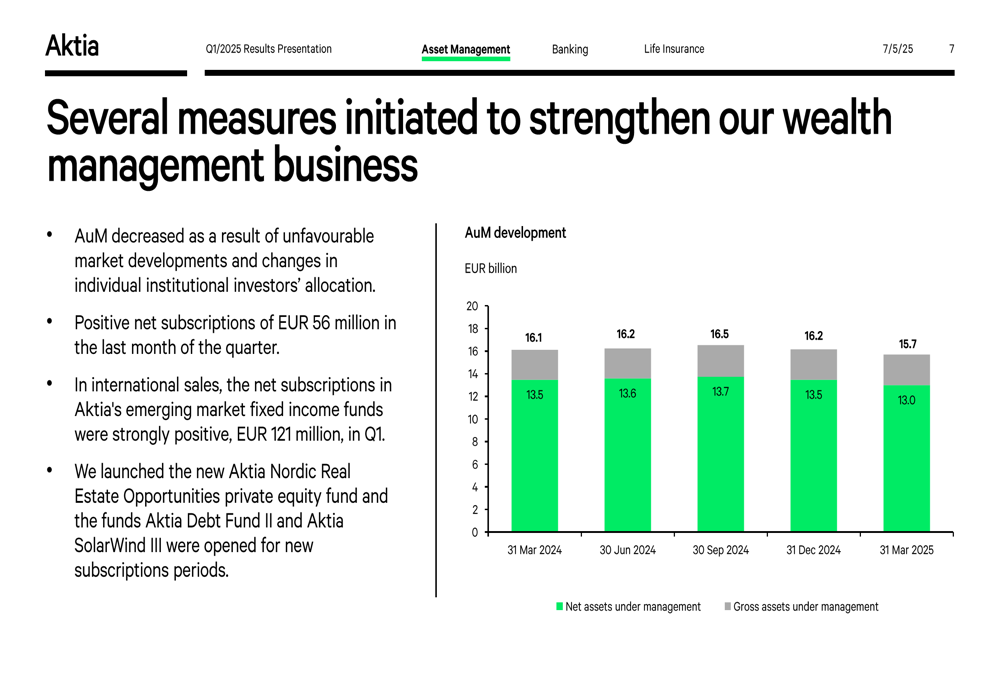

In wealth management, Aktia reported that Assets under Management (AuM) decreased to €13.0 billion from €13.5 billion in Q1 2024, primarily due to unfavorable market developments and changes in individual institutional investors’ allocation. However, the company highlighted positive net subscriptions of €56 million in the last month of the quarter and strong performance in emerging market fixed income funds with €121 million in net subscriptions during Q1:

Detailed Financial Analysis

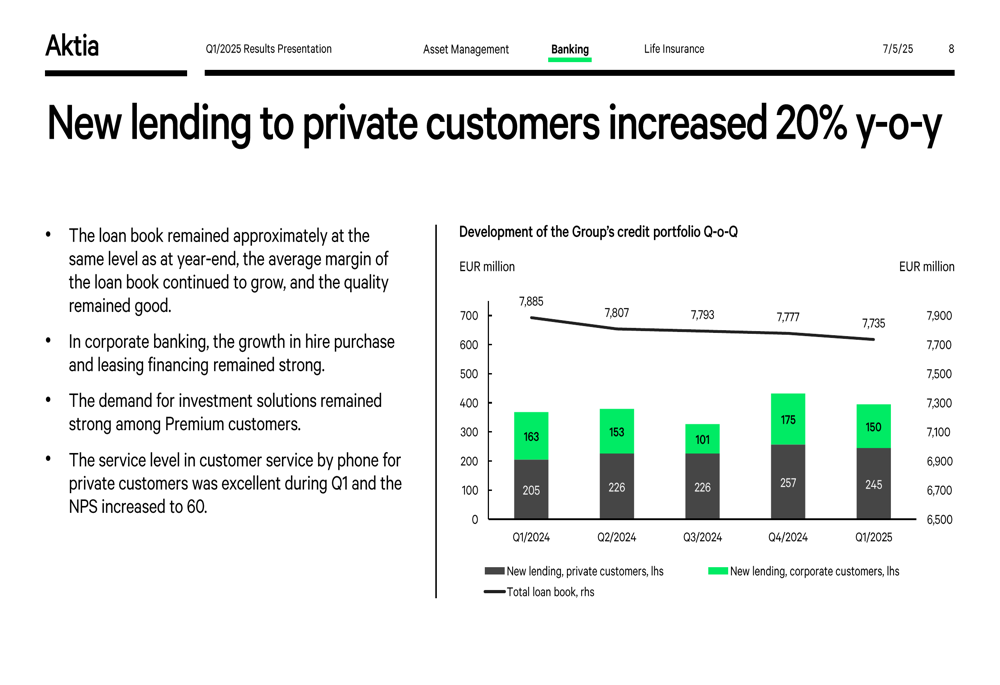

A bright spot in Aktia’s Q1 performance was the 20% year-over-year increase in new lending to private customers, although the overall loan book remained at approximately the same level as at year-end. The company noted that the average margin of the loan book continued to grow, and its quality remained good:

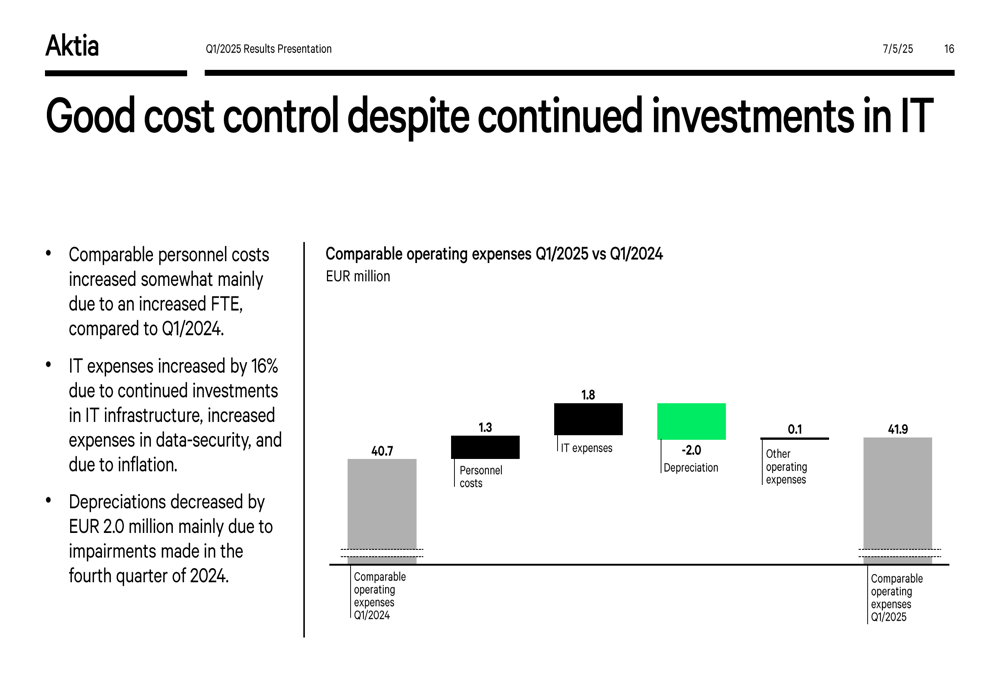

Operating expenses increased by 6% year-over-year to €44.0 million, primarily driven by higher IT expenses, which grew by 16% due to continued investments in IT infrastructure, increased expenses in data security, and inflation. Personnel costs also increased somewhat mainly due to higher FTE count compared to Q1 2024:

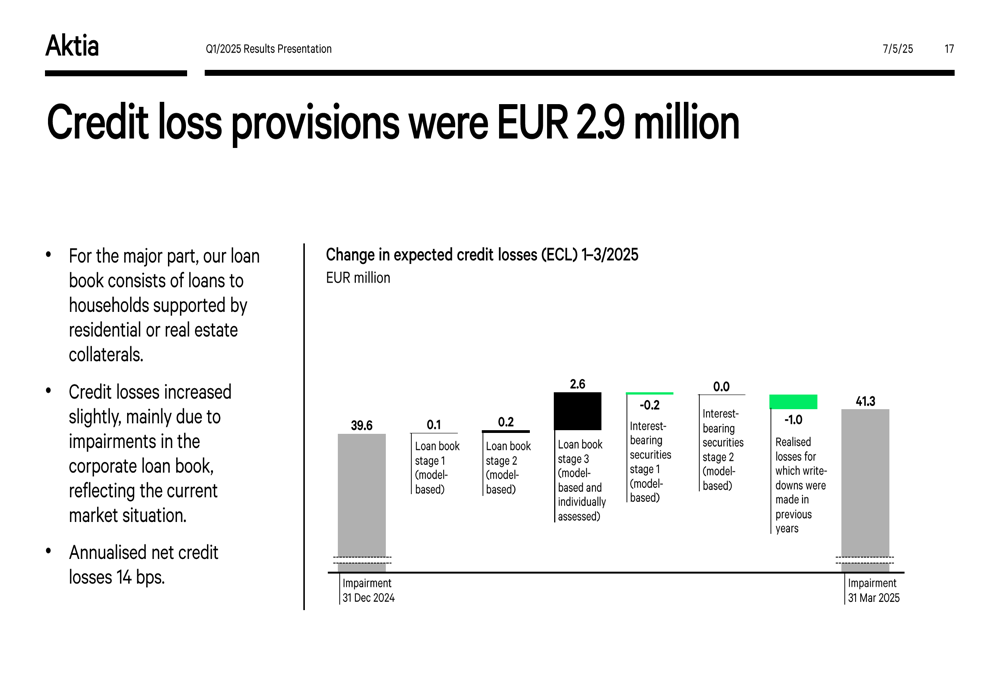

Credit losses increased slightly to €2.9 million, mainly due to impairments in the corporate loan book, reflecting the current market situation. Annualized net credit losses stood at 14 basis points:

Forward-Looking Statements

Aktia maintained its outlook for 2025, expecting comparable operating profit to be lower than the €124.5 million achieved in 2024. The bank anticipates lower net interest income due to the lower interest rate environment, while net commission income is expected to be slightly higher than in 2024, though market uncertainty may have a negative impact.

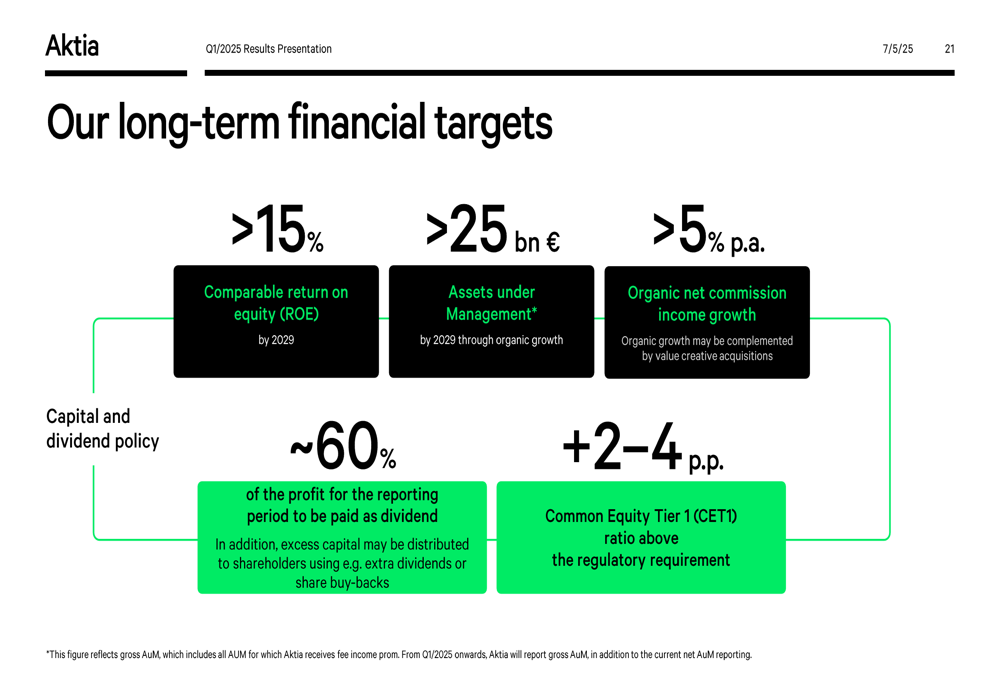

Looking further ahead, Aktia has set ambitious long-term financial targets to be achieved by 2029:

The bank aims to achieve over 15% comparable return on equity (ROE) by 2029, grow assets under management to over €25 billion through organic growth, and deliver over 5% annual organic net commission income growth. Additionally, Aktia plans to maintain a Common Equity Tier 1 (CET1) ratio above the regulatory requirement plus 2-4 percentage points, and continue its dividend policy of distributing roughly 60% of the profit for the reporting period.

Competitive Industry Position

Aktia continues to strengthen its position in sustainability, with 98.2% of its funds classified as SFDR Article 8 and 9, up slightly from 98.1% in Q4 2024. The company’s employee Net Promoter Score (eNPS) rose significantly from 19 to 32, indicating improved employee satisfaction.

The bank’s service level in customer service by phone for private customers was described as "excellent" during Q1, with the Net Promoter Score (NPS) increasing to 60. This strong customer satisfaction, combined with Aktia’s focus on personalized advisory services and product quality, positions the company well in the competitive Finnish banking landscape.

On February 26, 2025, Moody’s Investors Service upgraded the long-term outlook on Aktia’s credit ratings from negative to stable, while confirming the bank’s short-term funding rating at A2/P-1 and long-term funding rating at A2. This positive rating action reflects confidence in Aktia’s financial stability despite the challenging operating environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.