60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

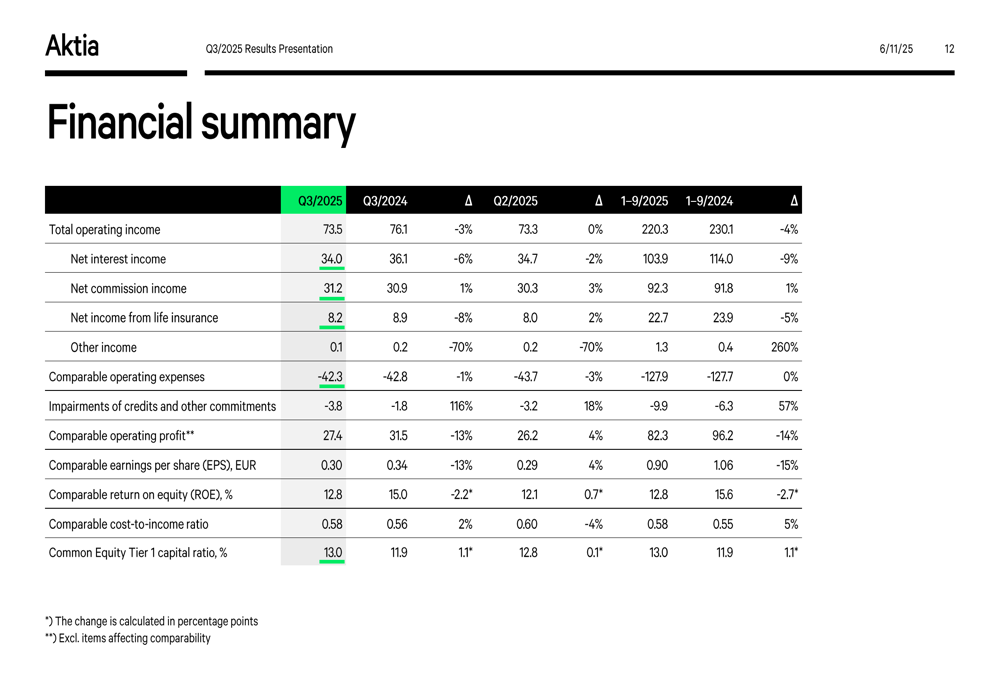

Aktia Bank (HEL:AKTIA) presented its third-quarter 2025 results on November 6, showing mixed performance with stable commission income offsetting some of the pressure from declining interest income. The Finnish bank reported comparable operating profit of EUR 27.4 million, falling short of analyst expectations despite revenue exceeding forecasts.

The stock remained steady at €10.56 following the presentation, suggesting investors had already priced in the bank's challenges amid the lower interest rate environment. Aktia continues to position itself as "the leading wealth manager empowered by a strong banking heritage," with its strategy showing some success in growing assets under management despite headwinds.

Quarterly Performance Highlights

Aktia reported total operating income of EUR 73.5 million for Q3 2025, down from EUR 76.1 million in the same quarter last year but slightly exceeding analyst expectations of EUR 72.23 million. The comparable operating profit of EUR 27.4 million represented a decrease from EUR 31.5 million in Q3 2024.

As shown in the following comprehensive financial summary, the bank's comparable earnings per share stood at EUR 0.30, down from EUR 0.34 in the same period last year:

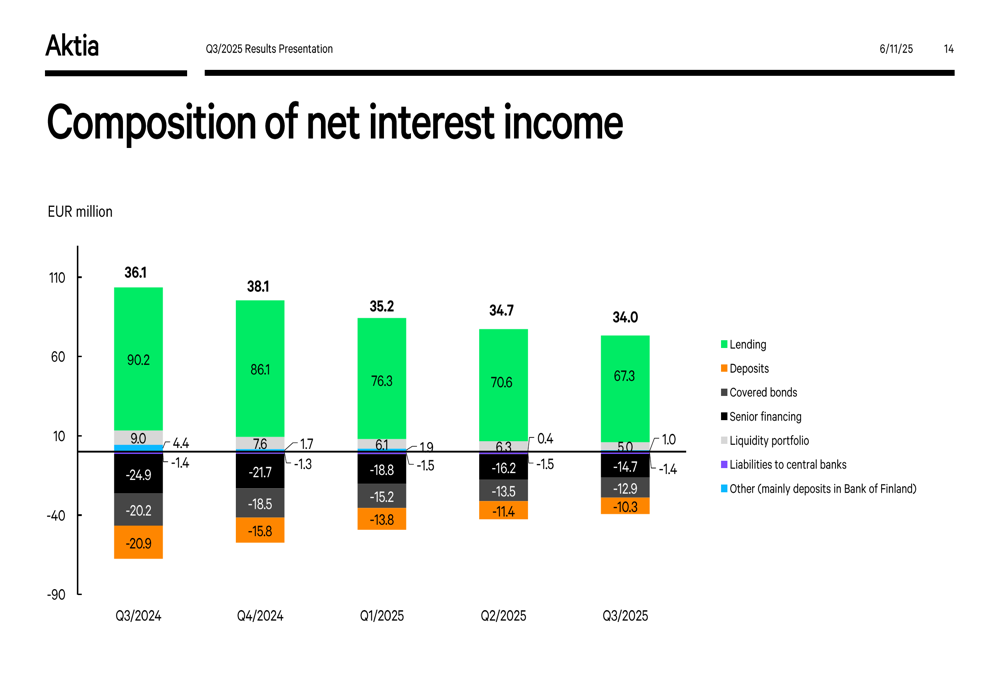

Net interest income declined to EUR 34.0 million from EUR 36.1 million year-over-year, reflecting the impact of lower market rates. However, this 6% decline represented an improvement from the 10% decline seen in the first half of the year, suggesting some stabilization.

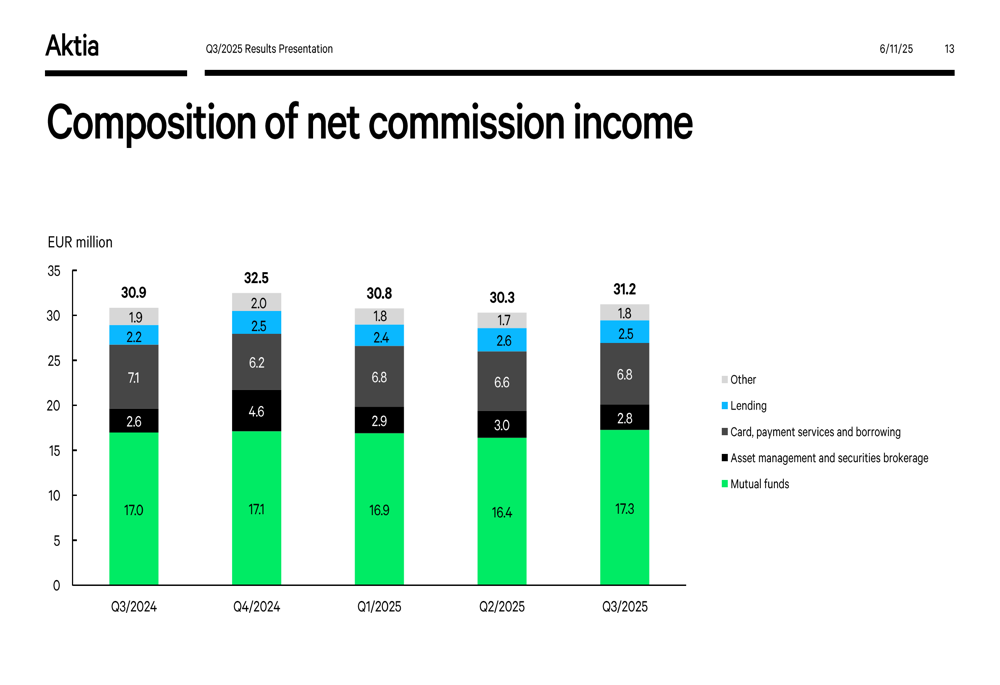

Meanwhile, net commission income showed resilience, increasing slightly to EUR 31.2 million from EUR 30.9 million in Q3 2024. The breakdown of commission income reveals the importance of mutual funds to Aktia's business model:

The composition of net interest income highlights the pressure points in Aktia's business, with lending contributing positively while other components like senior financing created drag:

Strategic Initiatives

Aktia's focus on wealth management continues to bear fruit, with assets under management increasing to EUR 16.3 billion during Q3 2025. The bank reported positive net subscriptions across all key customer segments and benefited from favorable market developments.

The company's international expansion efforts progressed with Oceanside Capital Partners representing Aktia's fund products in the Netherlands. Additionally, the portfolio managers of the Aktia Emerging Market Local Currency Bond+ fund received Citywire's AAA rating, enhancing the bank's credibility in the asset management space.

Sustainability remains a key strategic priority for Aktia. The bank maintains a high share of sustainable funds, with 98.2% of its funds classified under SFDR Article 8 and 9. The company has also achieved a 47.9% reduction in relative carbon footprint against its target of 30% by 2025 (versus 2019 baseline).

Detailed Financial Analysis

Aktia demonstrated strong cost control, with comparable operating expenses decreasing by 1% year-over-year to EUR 42.3 million. However, IT expenses increased by 11% due to continued investments in technology infrastructure, reflecting the bank's commitment to digital transformation.

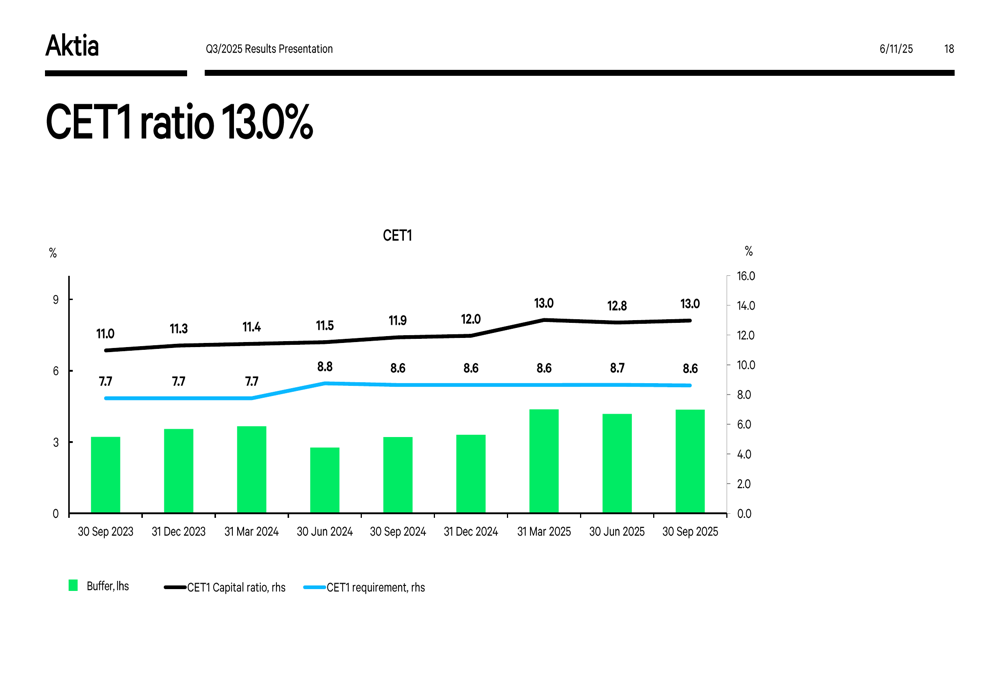

The bank's capital position strengthened significantly, with the Common Equity Tier 1 (CET1) capital ratio improving to 13.0% from 11.9% in Q3 2024, comfortably above regulatory requirements:

Credit losses increased during the period, primarily due to individual impairments. The majority of Aktia's loan book consists of household loans secured by residential or real estate collateral, providing some protection against potential defaults.

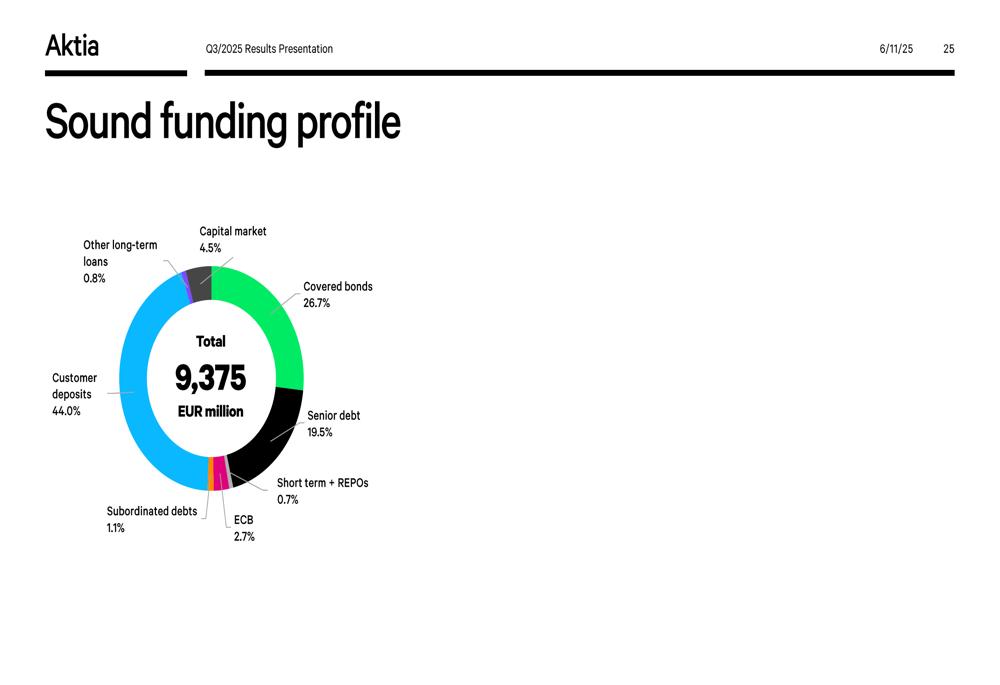

Aktia maintains a diversified funding profile, with customer deposits accounting for 44% of total funding:

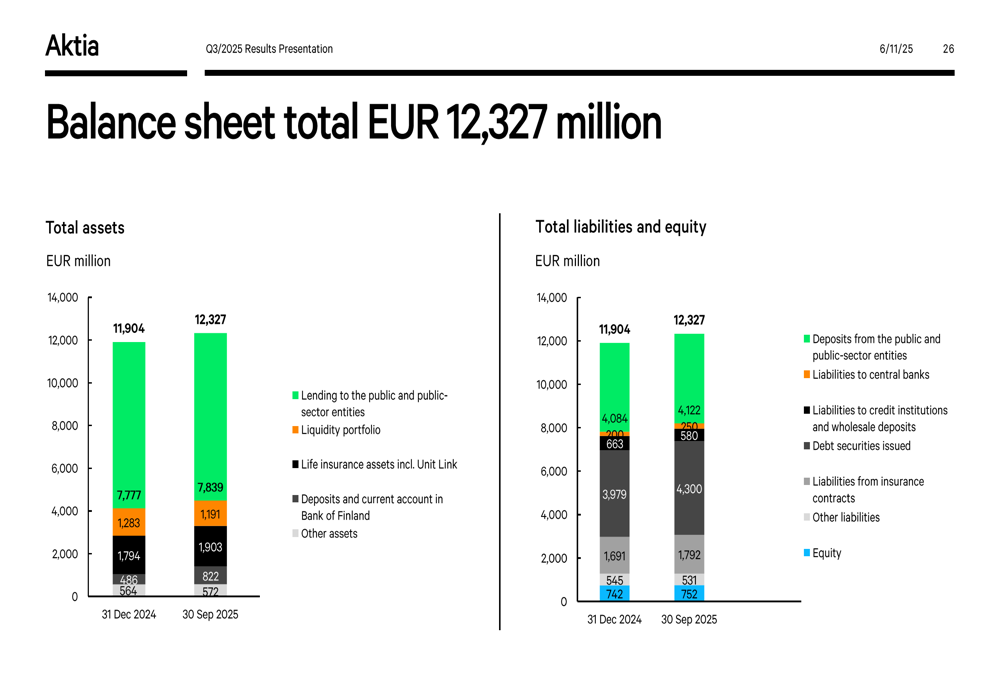

The bank's balance sheet totaled EUR 12,327 million, with a breakdown showing the importance of lending to the public and liquidity portfolio on the asset side:

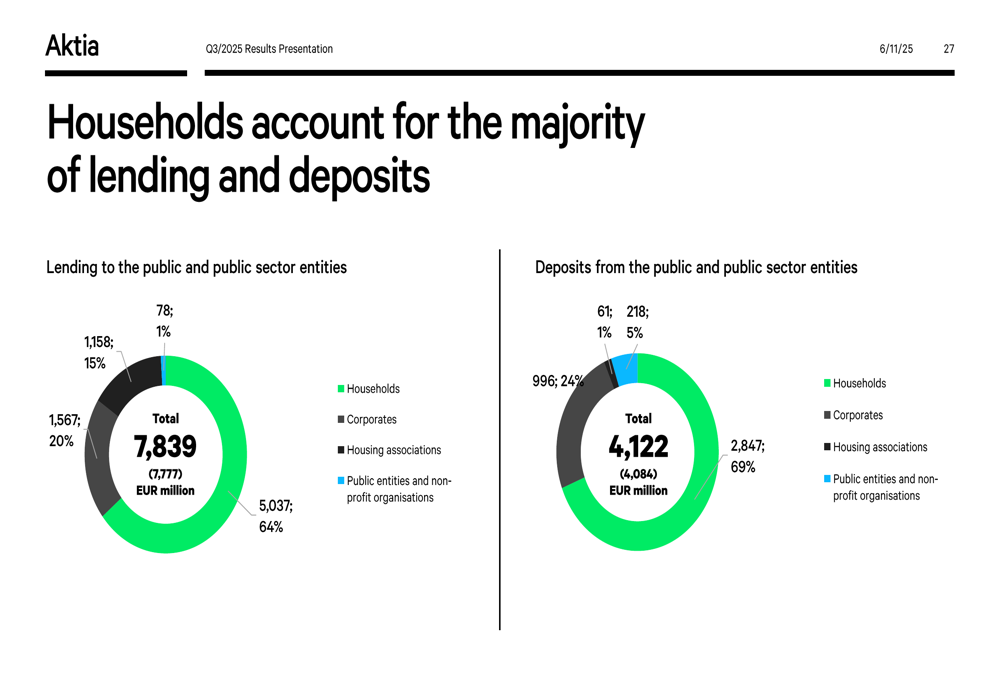

Households remain the dominant customer segment for both lending and deposits, accounting for 64% of lending and 69% of deposits:

Forward-Looking Statements

Aktia's management expects the bank's comparable operating profit for 2025 to be lower than the EUR 124.5 million reported in 2024. This cautious outlook reflects continued pressure on net interest income and potential challenges in the life insurance investment portfolio.

CEO Anssi Huhta emphasized the bank's commitment to its strategy, stating, "We stay true to our strategy, growing with our customers and creating value through the Aktia experience." Meanwhile, CFO Sakari Järvelä highlighted the focus on operational plans and delivering on key performance indicators.

The bank's liquidity position remains strong, with a Liquidity Coverage Ratio (LCR) of 235% at the end of Q3. Aktia successfully issued another benchmark-sized Covered Bond in September, further strengthening its funding base.

While facing headwinds from the interest rate environment, Aktia continues to focus on stability, long-term value creation, and implementing its strategic initiatives in wealth management and sustainability. The bank's improved capital position provides a solid foundation for navigating the challenges ahead, even as it prepares for potentially lower profitability in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.