Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Alaska Air Group (NYSE:ALK) presented its second quarter 2025 earnings results on July 23, revealing performance that exceeded initial guidance despite ongoing revenue challenges. The company’s stock is trading down 1.38% at market open following the presentation, with premarket activity showing a more pronounced decline of 2.93%.

The results mark a significant improvement from the company’s disappointing first quarter, when Alaska Air missed expectations with an EPS of -$0.77 against a forecast of -$0.71. The airline’s Q2 performance demonstrates progress in its integration with Hawaiian Airlines and advancement of strategic initiatives, though investors appear cautious about the revised capacity outlook and persistent revenue pressures.

Quarterly Performance Highlights

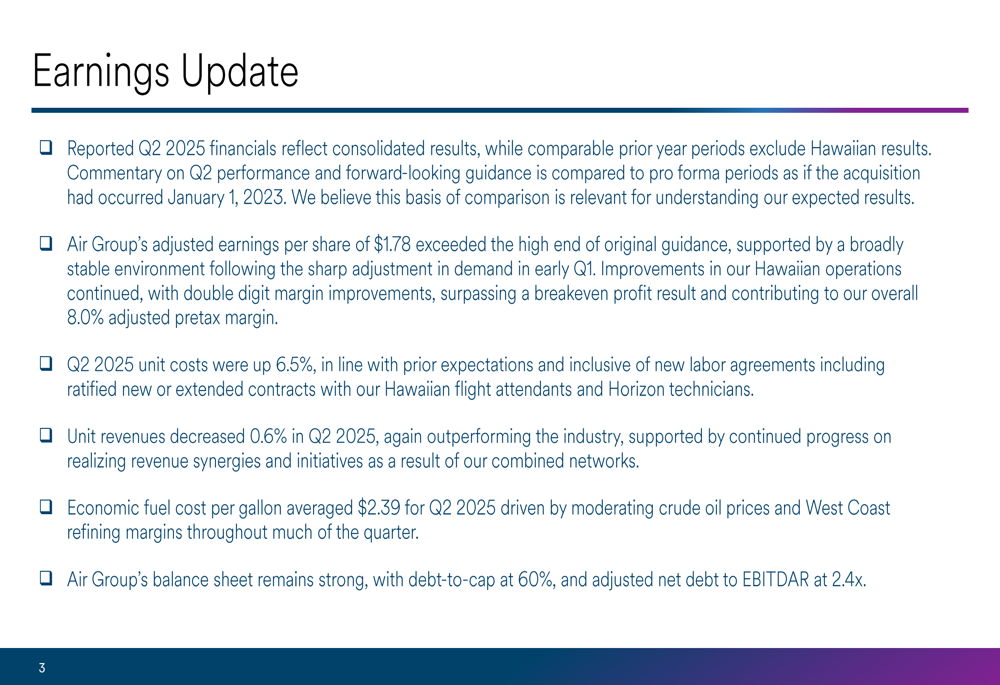

Alaska Air reported an adjusted earnings per share of $1.78 for Q2 2025, exceeding the high end of the company’s original guidance. The results reflect consolidated performance including Hawaiian Airlines operations, which achieved their first profitable quarter since acquisition with double-digit margin improvements. Overall, the company delivered an 8.0% adjusted pretax margin.

As shown in the quarterly earnings summary:

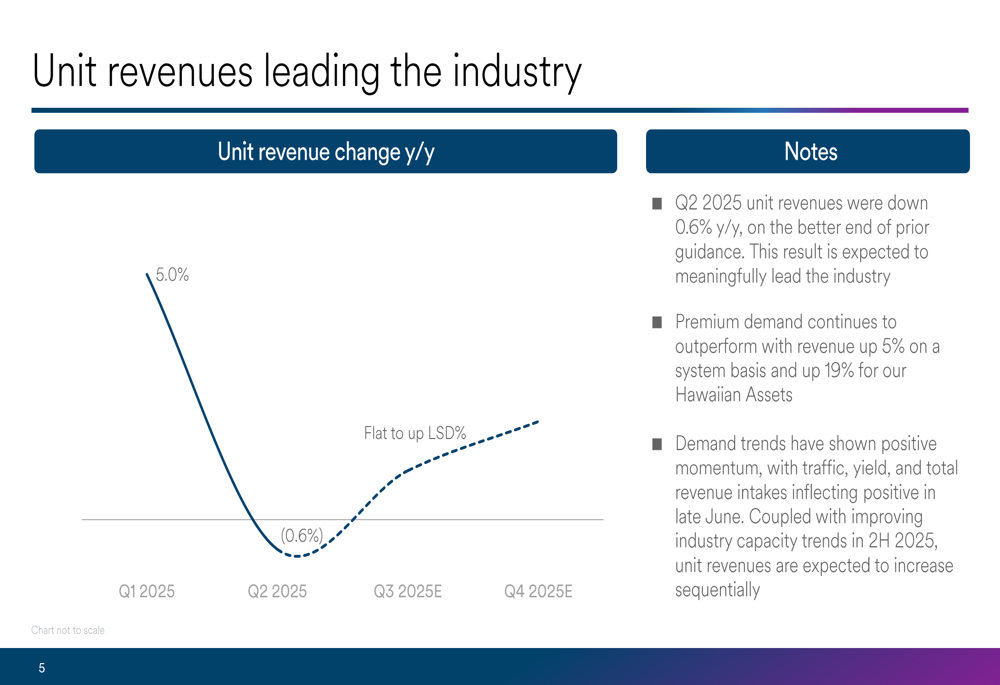

Unit revenues decreased slightly by 0.6% year-over-year in Q2 2025, following a 5.0% increase in Q1. However, the company noted that demand trends showed positive momentum toward the end of the quarter, with traffic, yield, and total revenue intakes turning positive in late June. Premium demand continues to outperform, with revenue up 5% system-wide and an impressive 19% increase for Hawaiian assets.

The revenue trend visualization shows the company’s performance and expectations for the remainder of 2025:

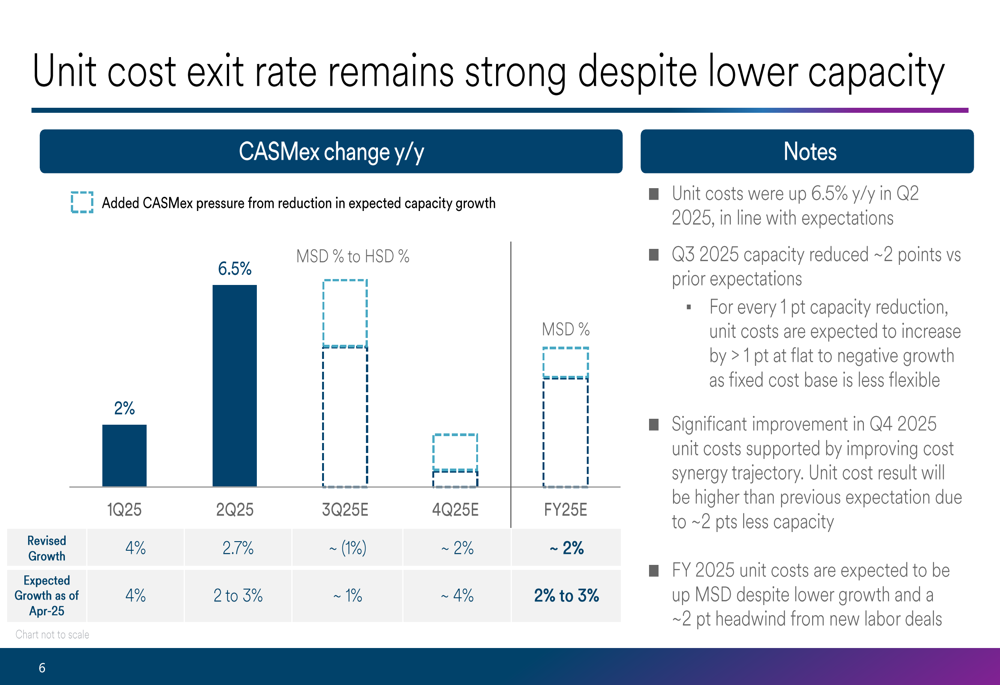

On the cost side, unit costs increased by 6.5% year-over-year in Q2, in line with management’s expectations. The company has revised its capacity growth downward, which puts additional pressure on unit costs as fixed expenses are spread across fewer available seat miles. Alaska now expects full-year capacity growth of approximately 2%, down from the previous guidance of 2-3%.

The following chart illustrates the unit cost trajectory and revised capacity expectations:

Strategic Initiatives

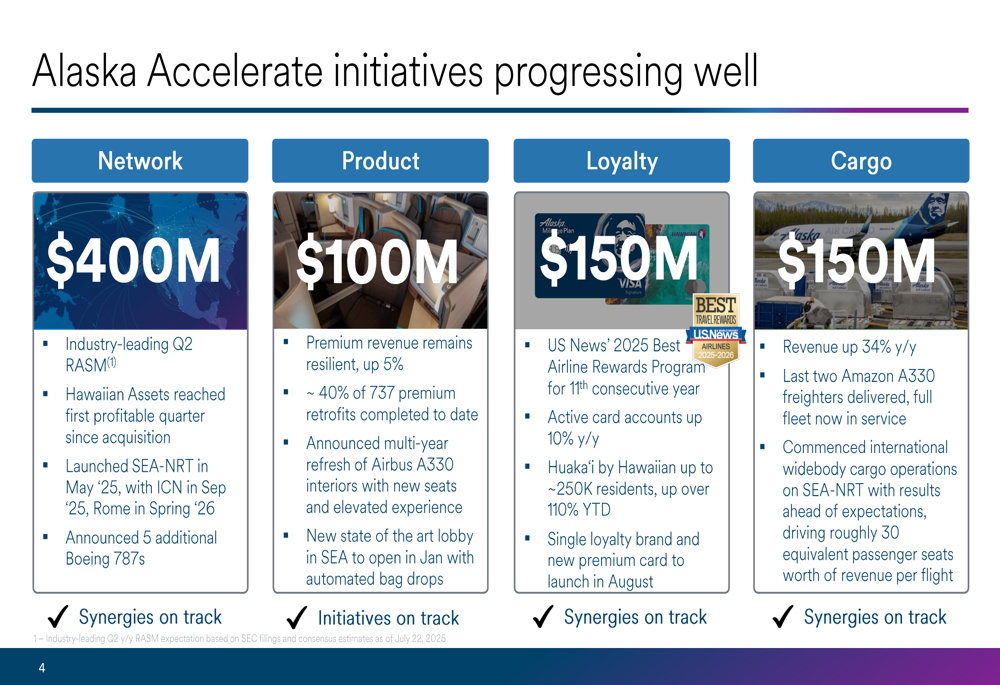

Alaska Air’s "Alaska Accelerate" program, designed to drive $800 million in incremental value, is progressing well across four key areas. The network optimization initiative ($400M) has delivered industry-leading unit revenue performance in Q2, while the Hawaiian assets achieved their first profitable quarter since acquisition. The company has expanded internationally with the launch of Seattle-Tokyo service in May 2025, with Seoul service planned for September 2025 and Rome in Spring 2026.

The product enhancement initiative ($100M) continues to show resilience in premium revenue, which grew 5% despite broader revenue challenges. Approximately 40% of the 737 premium retrofits have been completed, and the company announced a multi-year refresh of Airbus A330 interiors.

The comprehensive strategic initiatives are detailed in this slide:

Integration Progress with Hawaiian Airlines

A key focus for investors has been the integration of Hawaiian Airlines, which Alaska acquired earlier this year. The Q2 results show meaningful progress, with Hawaiian operations achieving their first profitable quarter since acquisition and contributing to the overall company performance with double-digit margin improvements.

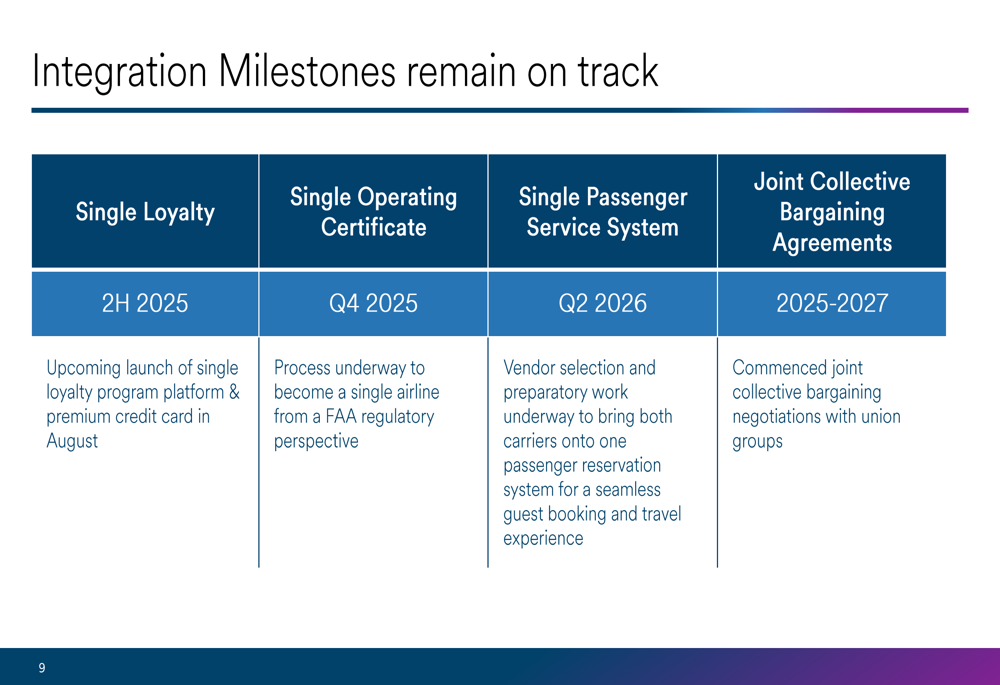

The integration timeline remains on track, with several key milestones approaching. The company plans to launch a unified loyalty program platform and premium credit card in August 2025, with a single operating certificate expected by Q4 2025. The migration to a single passenger service system is scheduled for Q2 2026, while joint collective bargaining agreements will be negotiated between 2025-2027.

The integration roadmap is outlined here:

Financial Outlook and Guidance

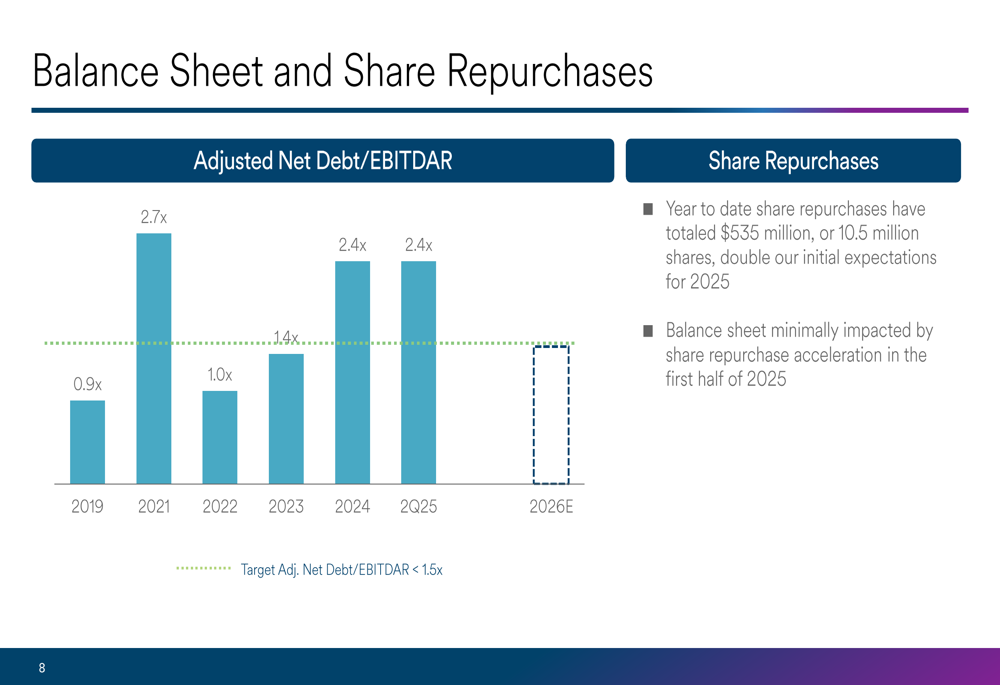

Alaska Air maintains a strong balance sheet despite accelerating its share repurchase program. Year-to-date share repurchases have totaled $535 million, or 10.5 million shares, double the initial expectations for 2025. The company’s debt-to-capitalization ratio stands at 60%, with adjusted net debt to EBITDAR at 2.4x, unchanged from 2024 despite the increased buyback activity.

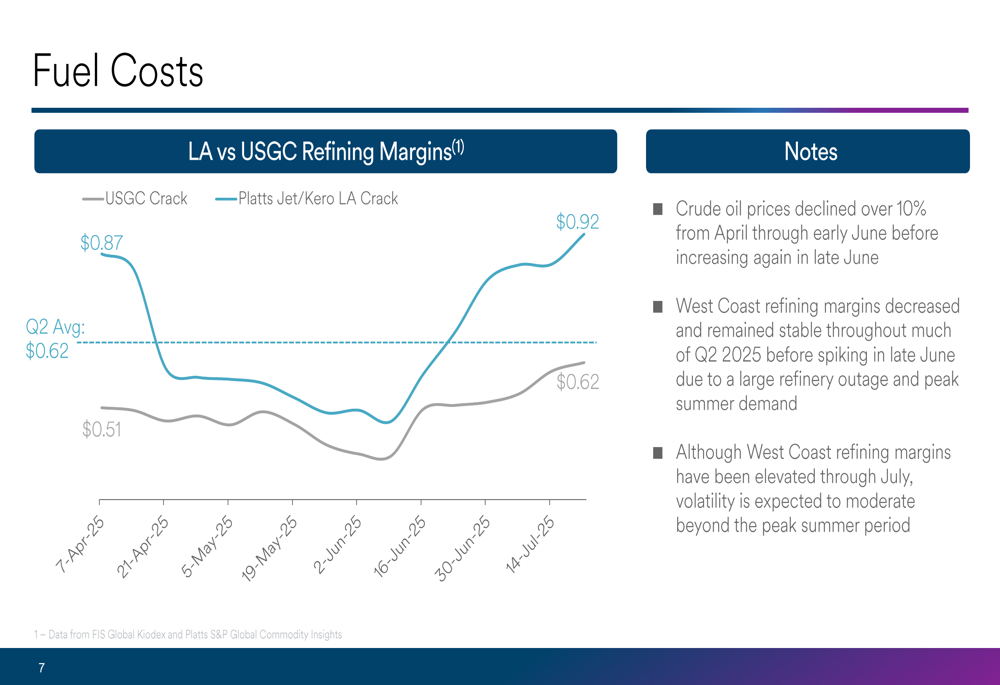

The company’s fuel costs averaged $2.39 per gallon in Q2 2025, with management noting that crude oil prices declined over 10% from April through early June before increasing again in late June. West Coast refining margins decreased and remained stable throughout much of Q2 before spiking in late June due to a large refinery outage and peak summer demand.

The following chart illustrates the company’s balance sheet metrics and target leverage ratio:

Looking ahead, Alaska Air expects unit revenues to be "flat to up low-single-digits" for both Q3 and Q4 2025. The company has reduced its capacity growth outlook for Q3 2025 to -1% (from the previous ~1%) and for Q4 2025 to ~2% (from the previous 4%). This capacity reduction is expected to put pressure on unit costs in the near term, though significant improvement is anticipated in Q4 2025 as cost synergies from the Hawaiian integration begin to materialize.

The fuel cost trends that impact the company’s financial performance are shown here:

Despite near-term challenges, Alaska Air’s management remains confident in its strategic positioning and long-term value creation potential through the Alaska Accelerate initiatives and successful integration of Hawaiian Airlines.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.