Intel surges more than 8% after chipmaker’s profits top expectations

Introduction & Market Context

Alcoa Corporation (NYSE:AA) presented its third-quarter 2025 earnings on October 22, revealing mixed results across its business segments amid divergent market conditions. The aluminum producer reported an adjusted loss despite higher aluminum prices, as restructuring charges and weaker alumina segment performance weighed on results. Alcoa’s stock fell 4.24% in after-hours trading following the announcement, reflecting investor disappointment with the earnings miss.

The company’s presentation highlighted a challenging quarter marked by significant one-time items, including a $786 million gain on the sale of its interest in the Ma’aden joint venture, offset by $895 million in restructuring charges related to the permanent closure of the Kwinana refinery in Australia.

Quarterly Performance Highlights

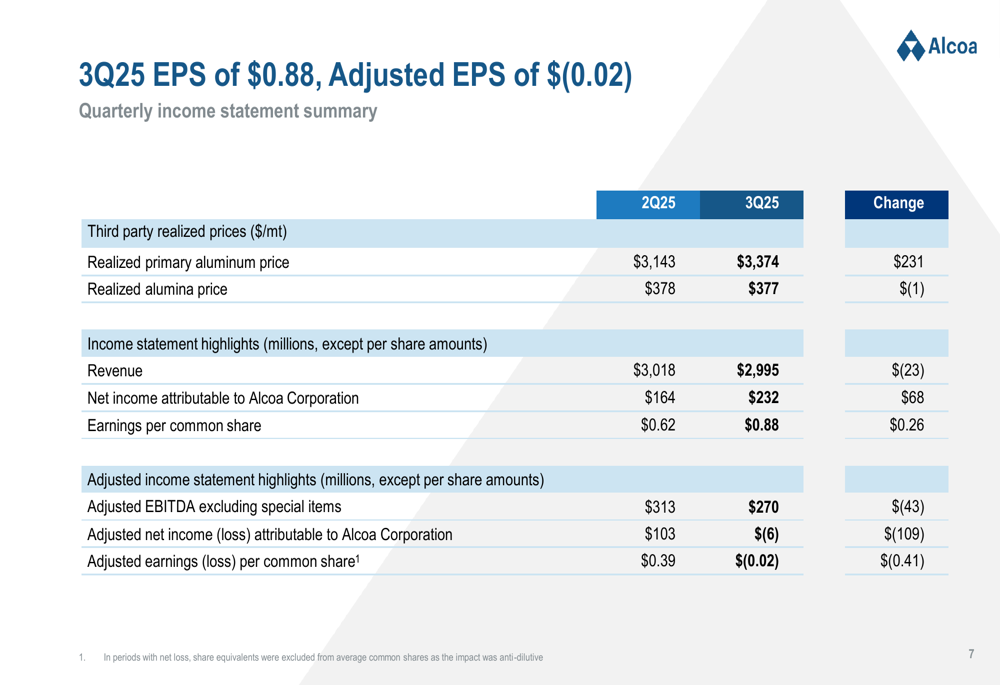

Alcoa reported third-quarter revenue of $2.995 billion, down slightly from $3.018 billion in the previous quarter and below analysts’ expectations of $3.13 billion. While GAAP earnings per share came in at $0.88, adjusted EPS showed a loss of $0.02, missing the forecasted positive $0.02 and representing a 200% negative surprise.

As shown in the following comprehensive income statement, the company’s realized primary aluminum price increased significantly to $3,374 per metric ton from $3,143 in the previous quarter, while alumina prices remained relatively flat:

Adjusted EBITDA declined to $270 million in the third quarter from $313 million in the second quarter. This decrease was primarily driven by the divergent performance of Alcoa’s two main segments: Aluminum showed strong improvement with $307 million in Adjusted EBITDA (up from $97 million), while the Alumina segment declined sharply to $67 million (down from $139 million).

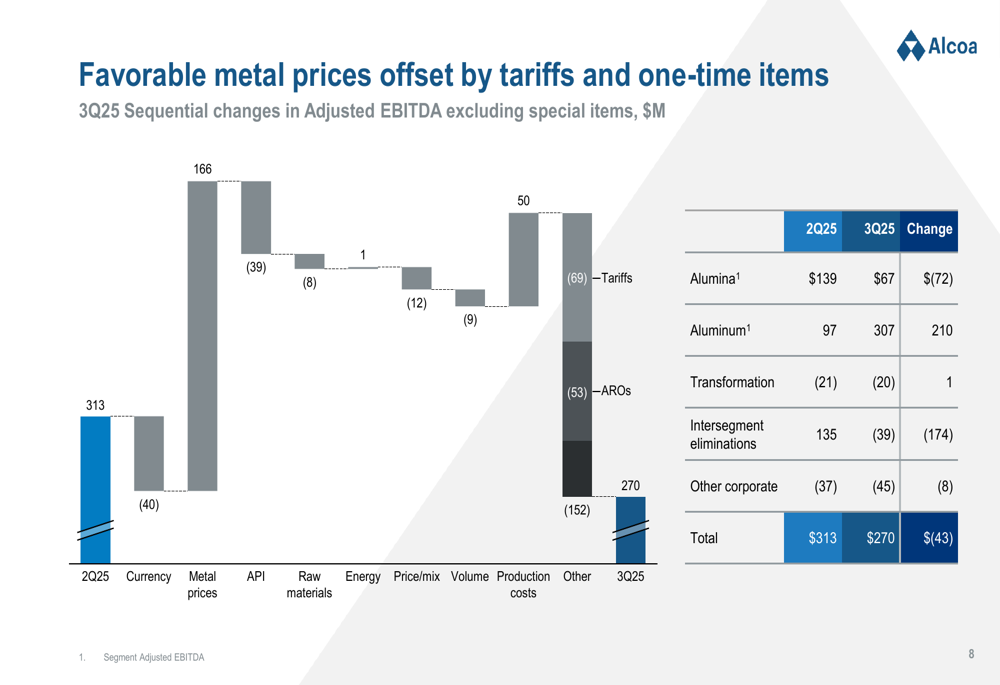

The following chart illustrates how favorable metal prices were offset by tariffs and other factors:

Detailed Financial Analysis

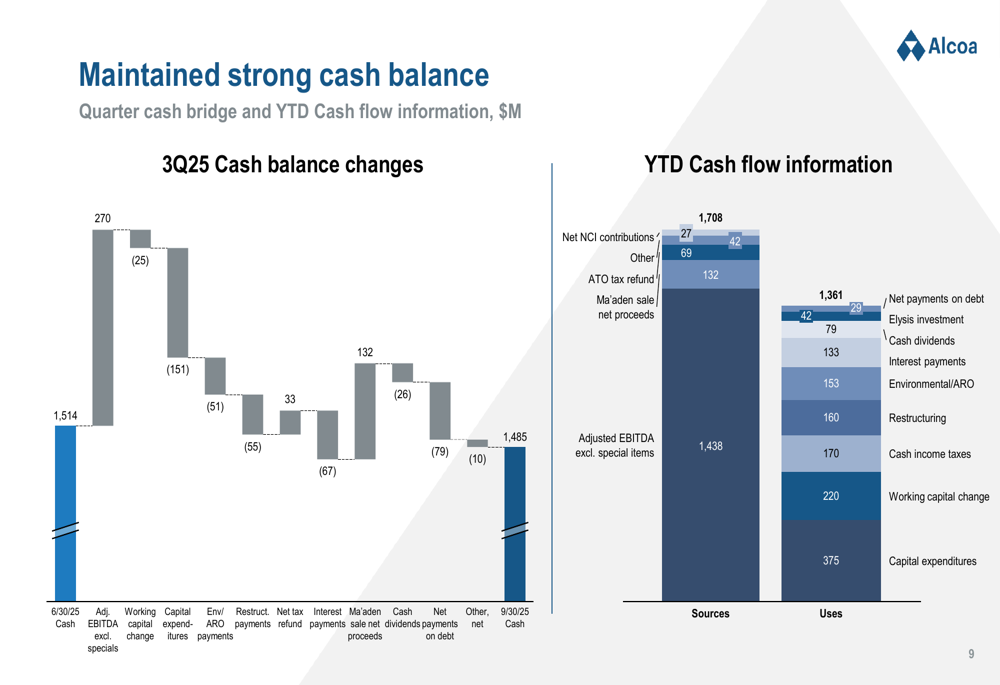

Alcoa maintained a strong cash position of $1.485 billion at the end of the quarter, slightly down from $1.514 billion on June 30. The company’s financial position continues to benefit from operational cash flow, though this was partially offset by capital expenditures and other items.

The cash flow bridge below shows the various factors affecting Alcoa’s cash balance during the quarter:

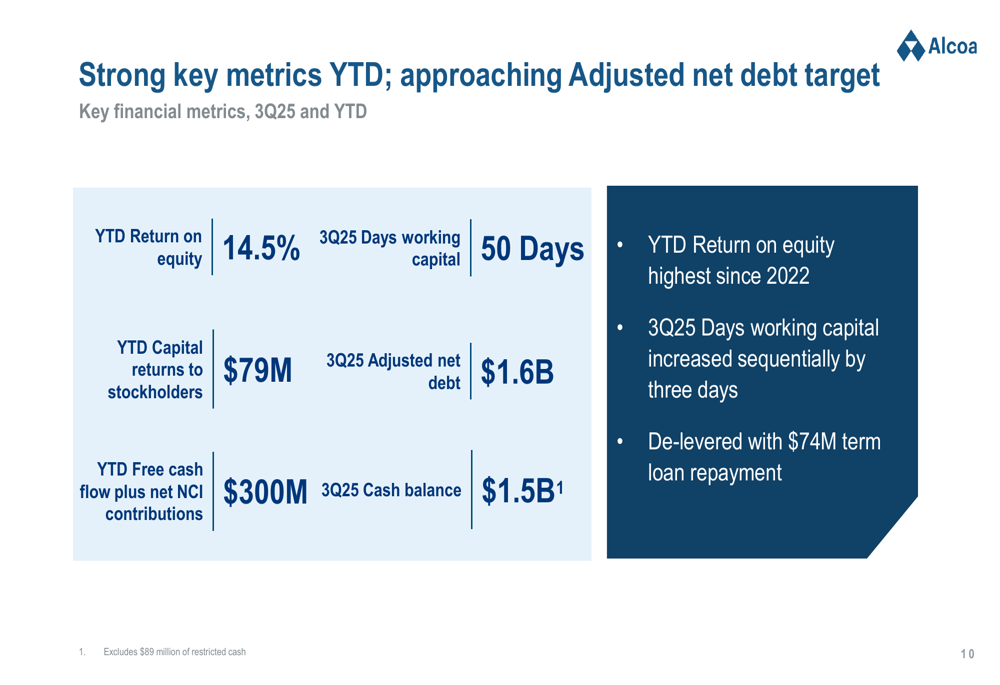

Despite the quarterly challenges, Alcoa highlighted several positive year-to-date metrics, including a 14.5% return on equity, which the company noted was the highest since 2022. The company also maintained its focus on shareholder returns, with $79 million in capital returned to stockholders year-to-date.

The following slide presents these key financial metrics:

Strategic Initiatives

Alcoa’s presentation emphasized several strategic initiatives aimed at transforming its portfolio and strengthening its competitive position. The permanent closure of the Kwinana refinery, while resulting in significant restructuring charges, aligns with the company’s efforts to optimize its refinery capacity.

The company is also strengthening its U.S. primary aluminum production capabilities at Massena through a new long-term energy contract and approximately $60 million in capital investment for the facility’s anode baking furnace. Additionally, Alcoa highlighted government support from both the U.S. and Australia for its gallium project, positioning the company to develop supply chains outside of China.

CEO William Oplinger emphasized the strategic importance of these initiatives, stating, "The real strategic advantage of this deal is that it provides a supply chain outside of China," according to the earnings call transcript.

Market Dynamics and Forward Outlook

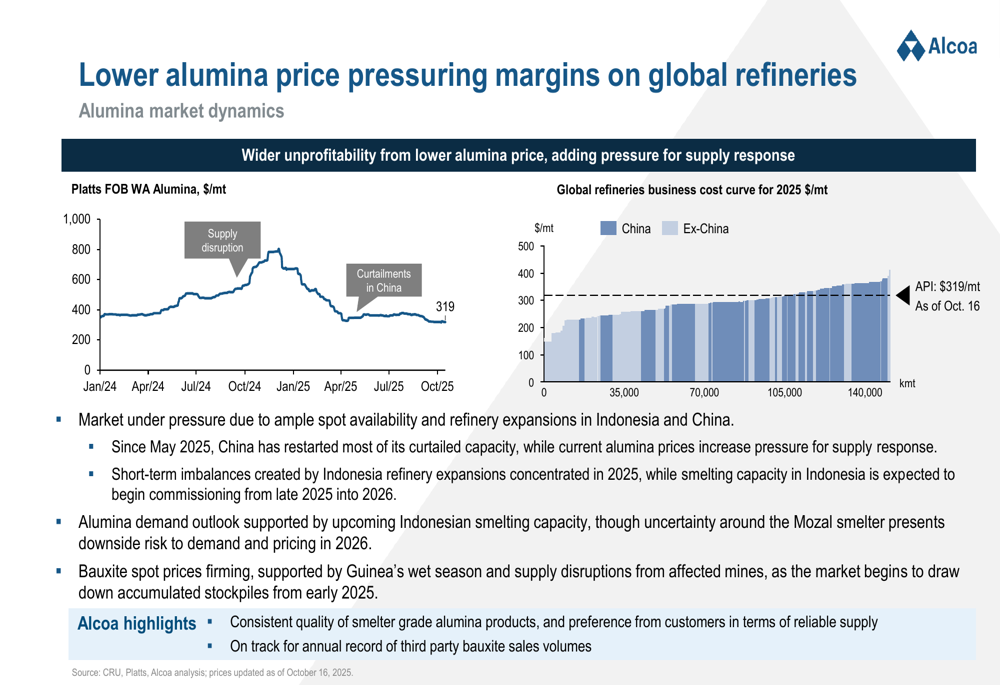

The presentation provided insights into the contrasting market dynamics affecting Alcoa’s business segments. Alumina prices are under pressure due to ample spot availability and refinery expansions in Indonesia and China, as illustrated in the following market analysis:

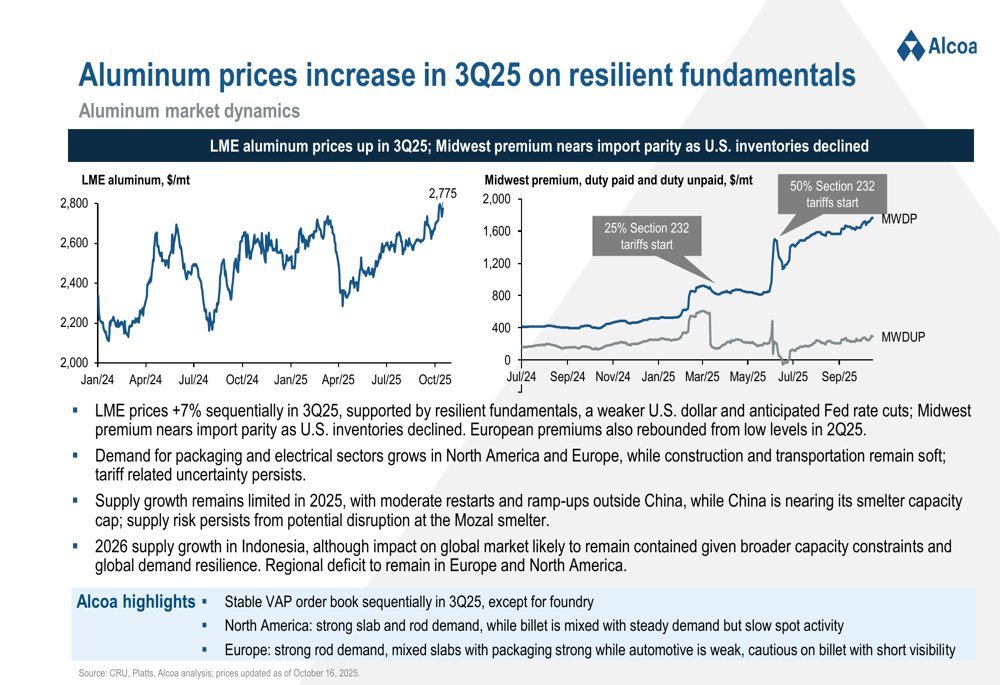

In contrast, aluminum prices increased by 7% sequentially in the third quarter, supported by resilient fundamentals and growing demand in packaging and electrical sectors in North America and Europe:

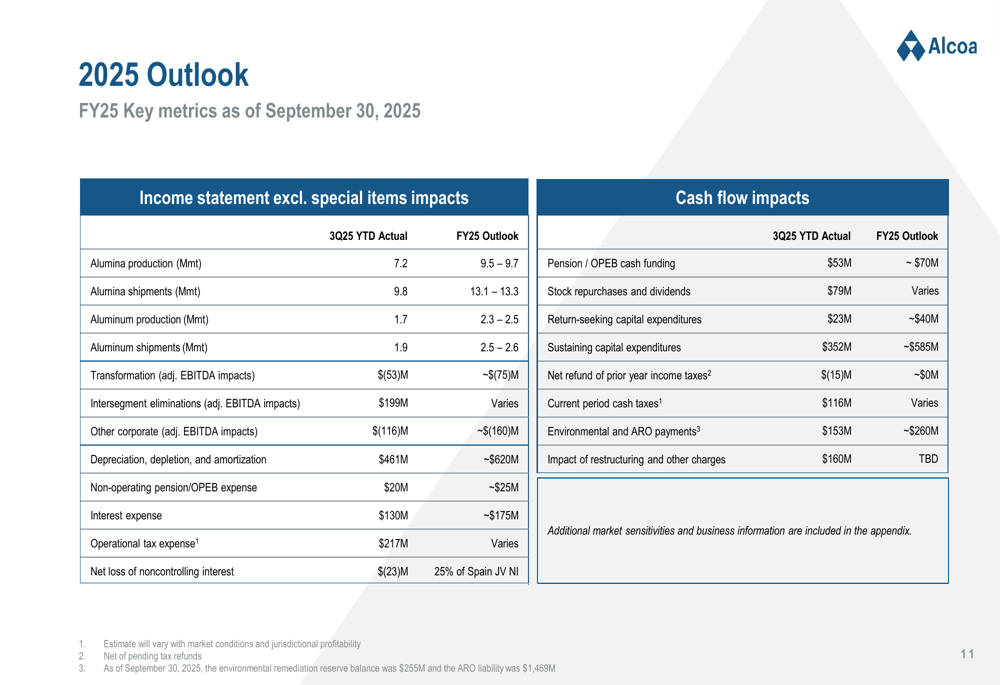

Looking ahead to the fourth quarter of 2025, Alcoa expects several improvements, including higher shipments and working capital release. The company also provided its 2025 outlook, projecting alumina production of 9.5-9.7 million metric tons and aluminum production of 2.3-2.5 million metric tons for the full year:

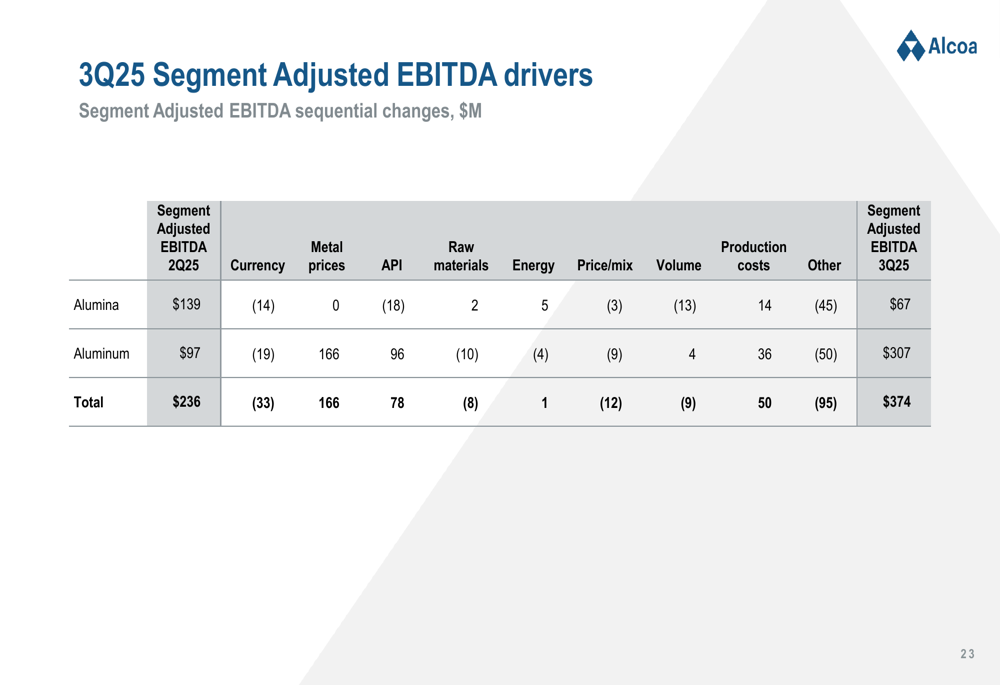

Segment Performance Analysis

A deeper dive into segment performance reveals the key drivers behind the changes in Adjusted EBITDA. The Aluminum segment benefited significantly from higher metal prices and improved production costs, while the Alumina segment faced challenges from lower pricing and higher costs.

The following detailed breakdown shows the specific factors driving each segment’s performance:

Conclusion

Alcoa’s third-quarter 2025 presentation reflects a company navigating mixed market conditions while implementing significant strategic changes. Despite the earnings miss and stock price decline, the company maintains a strong financial position with opportunities for improvement in the coming quarters.

The contrast between the strengthening aluminum market and challenging alumina environment continues to create segment-level volatility. Meanwhile, Alcoa’s portfolio transformation initiatives, including facility closures, strategic investments, and government partnerships, aim to position the company for long-term success in an evolving global market.

Investors will be watching closely to see if Alcoa’s strategic moves and anticipated fourth-quarter improvements materialize as expected, particularly as the company prepares for its upcoming Investor Day on October 30, 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.