U.S. stocks lower as investors rotate out of tech ahead of Jackson Hole

Introduction & Market Context

Alcon AG (NYSE:ALC), the global leader in eye care, reported its first quarter 2025 results on May 14, 2025, showing flat sales growth on a reported basis but a 3% increase in constant currency. The company raised its full-year revenue guidance while simultaneously lowering its margin and earnings per share expectations due to tariff impacts and recent business development activities.

In after-hours trading following the presentation, Alcon shares fell 2.41% to $91.00, reflecting investor concerns about the reduced profit outlook despite the improved revenue forecast.

Quarterly Performance Highlights

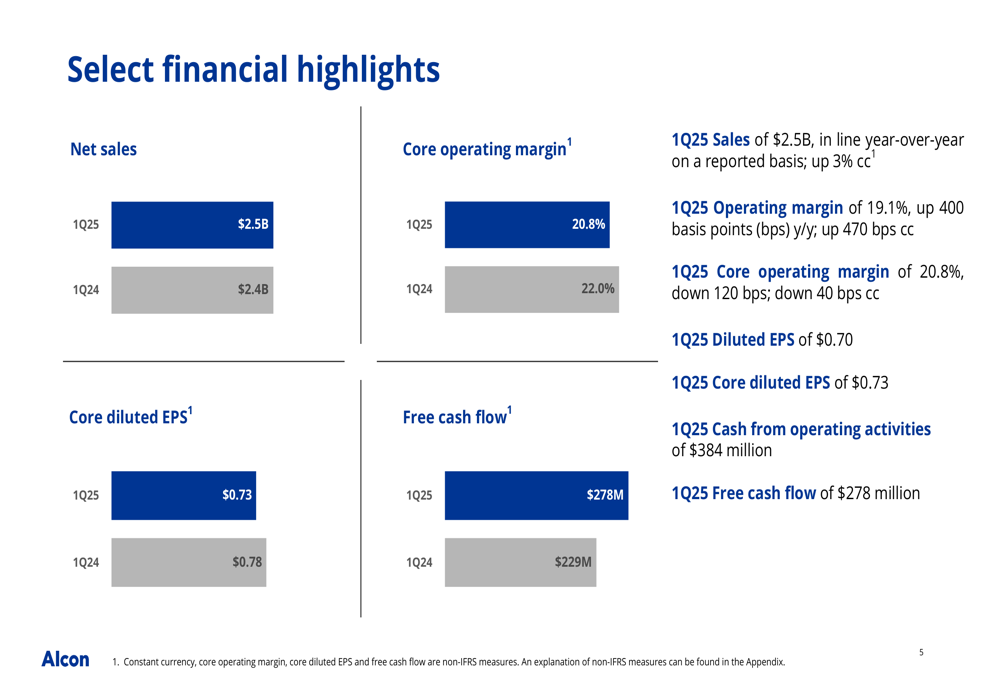

Alcon reported first quarter 2025 net sales of $2.5 billion, unchanged year-over-year on a reported basis but up 3% in constant currency. The company’s IFRS operating margin improved significantly to 19.1%, a 400 basis point increase from the prior year, while diluted earnings per share jumped 40% to $0.70.

As shown in the following financial highlights chart:

However, the substantial improvement in IFRS results was largely driven by $142 million in gains from fair value remeasurements of investments in associated companies. Core results, which exclude these one-time gains, showed a different picture with core operating margin declining 120 basis points to 20.8% and core diluted EPS remaining flat at $0.73.

Segment Performance

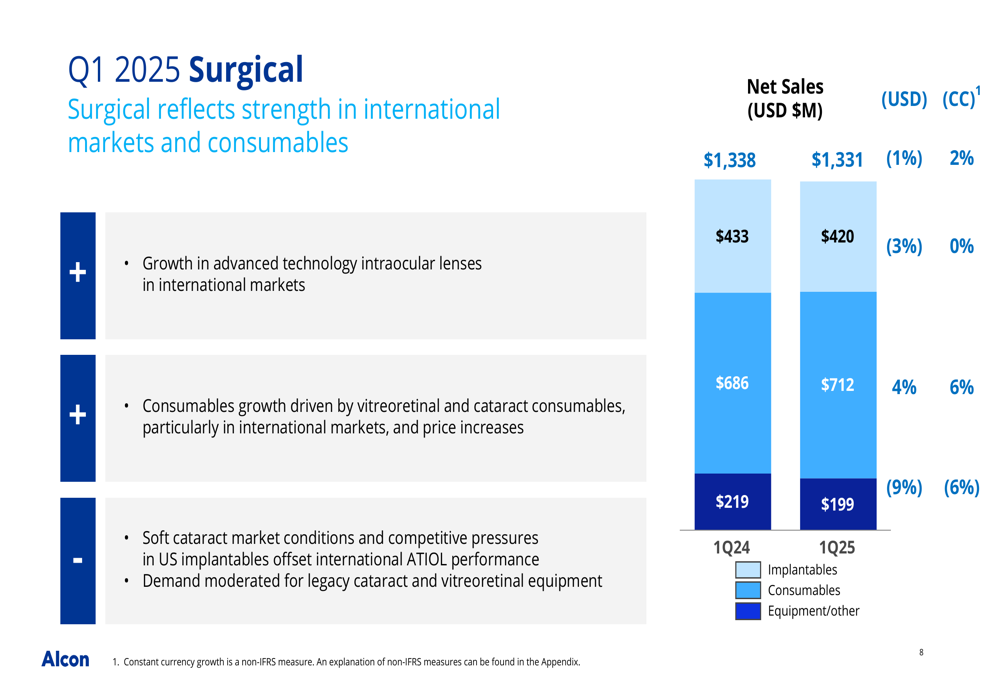

Alcon’s business is divided into two main segments: Surgical and Vision Care. The Surgical segment, accounting for 54% of total sales, experienced a 1% decline in reported sales to $1.33 billion, though it grew 2% in constant currency.

The following chart breaks down the surgical segment performance:

Within Surgical, consumables showed the strongest performance with 4% growth (6% in constant currency) to $712 million, driven by vitreoretinal and cataract consumables, particularly in international markets. However, implantables declined 3% to $420 million, and equipment/other fell 9% to $199 million, reflecting soft cataract market conditions and competitive pressures in the U.S.

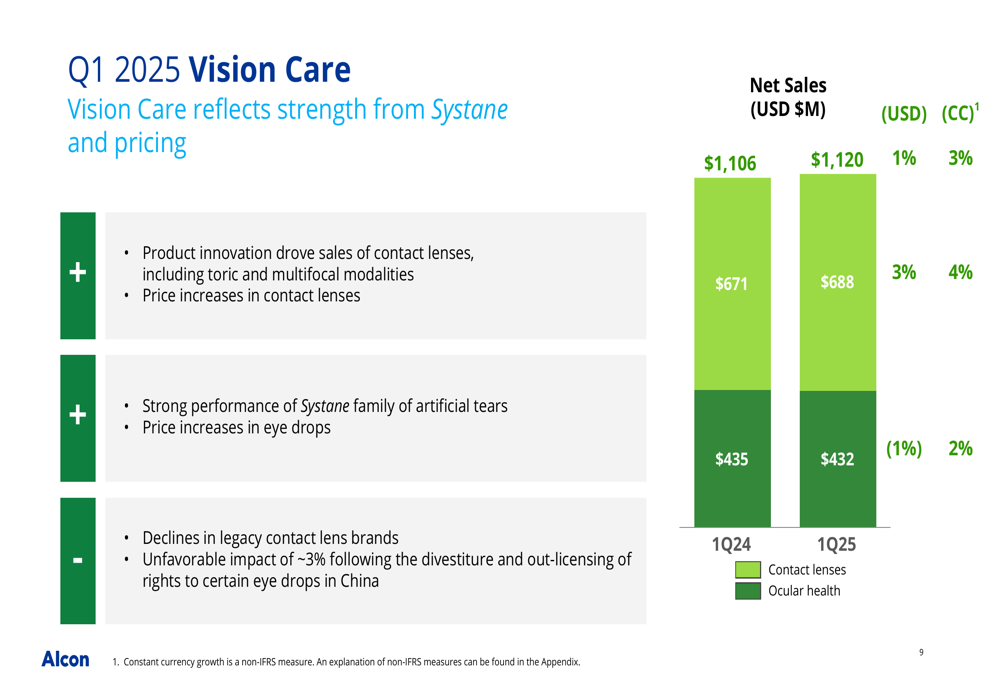

The Vision Care segment, representing 46% of total sales, grew 1% to $1.12 billion (3% in constant currency). This segment’s performance is illustrated in the following chart:

Contact lenses, which comprise 61% of Vision Care sales, increased 3% to $688 million, driven by product innovation in toric and multifocal modalities. Ocular health products declined 1% to $432 million but grew 2% in constant currency, with strong performance from the Systane family of artificial tears offset by the divestiture of certain eye drops in China.

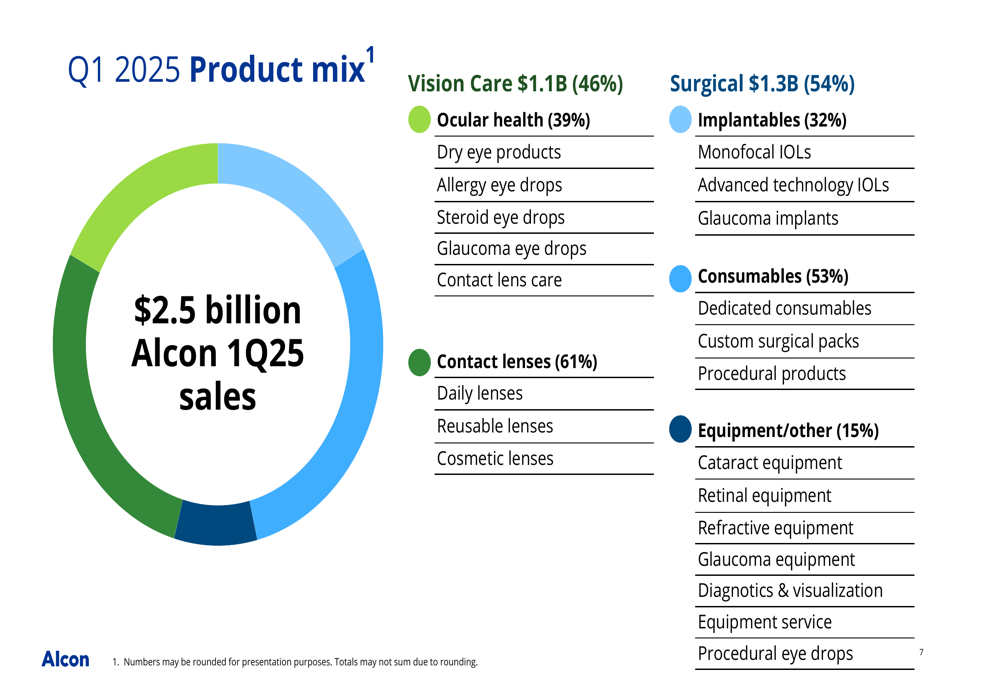

The overall product mix for Q1 2025 is illustrated in the following chart:

Detailed Financial Analysis

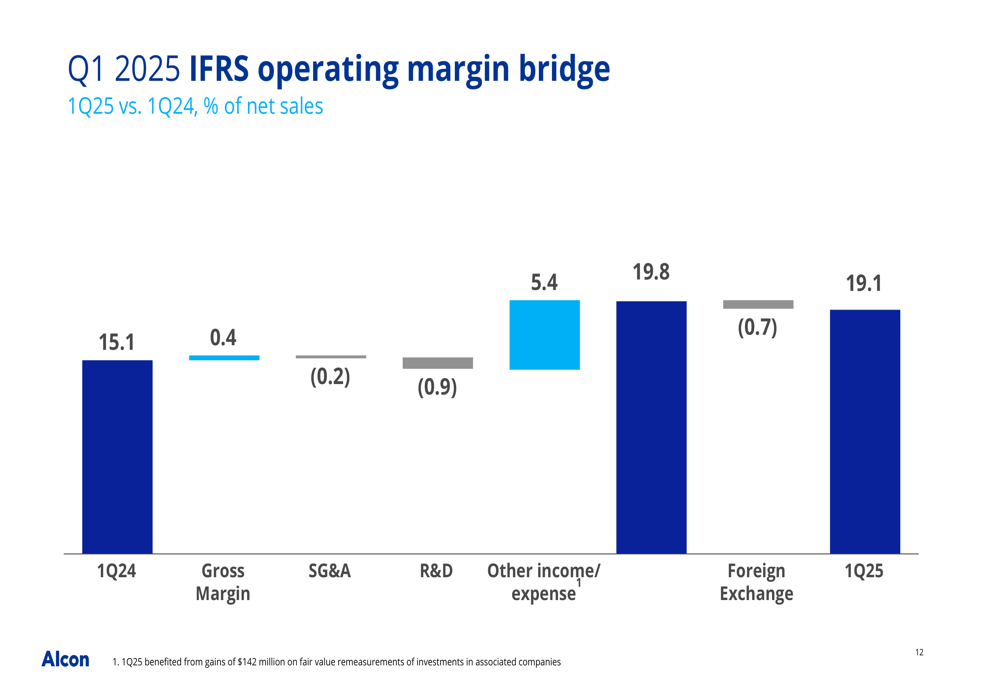

Alcon’s IFRS operating margin improved dramatically from 15.1% in Q1 2024 to 19.1% in Q1 2025. The following bridge chart explains the components of this improvement:

The 400 basis point improvement was primarily driven by a 5.4 percentage point benefit from other income/expense, which included the $142 million gain from fair value remeasurements of investments. This was partially offset by a 0.9 percentage point increase in R&D expenses and a 0.7 percentage point negative impact from foreign exchange.

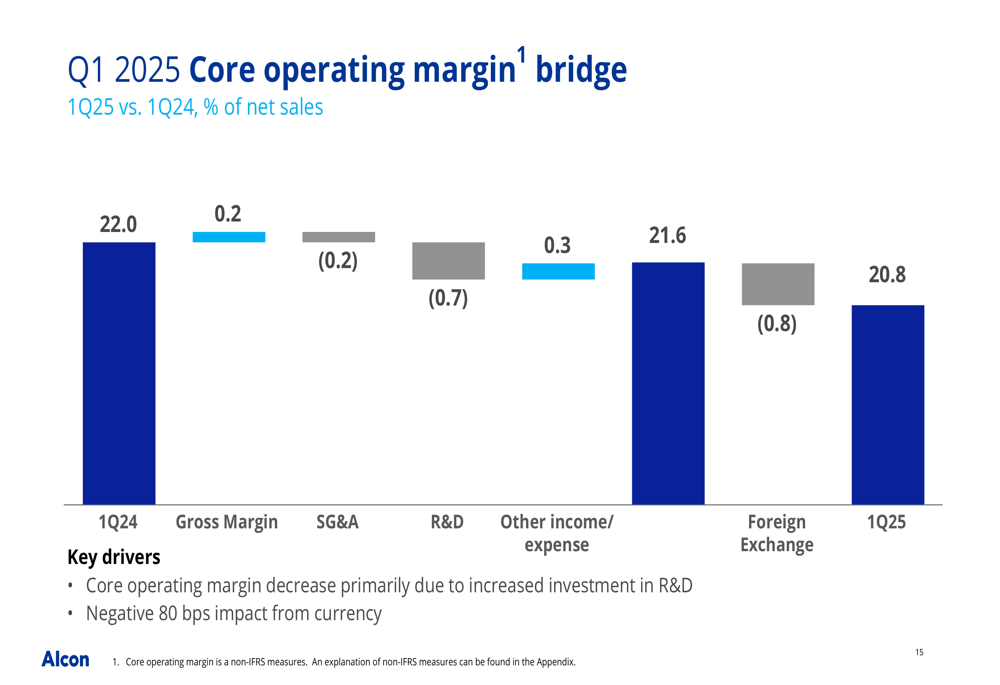

Core operating margin, which excludes certain one-time items, declined from 22.0% to 20.8%. The following chart breaks down this change:

The core margin decrease was primarily due to increased investment in R&D and an 80 basis point negative impact from currency fluctuations.

Cash Flow & Balance Sheet

Alcon generated $384 million in cash from operations during the first quarter of 2025, up from $341 million in the same period last year. Free cash flow improved to $278 million from $229 million in Q1 2024.

The company reported $1.4 billion in cash and cash equivalents on its balance sheet, with total debt of $4.7 billion. Capital expenditures totaled $106 million in the quarter, primarily for investments in new contact lens manufacturing capacity.

Updated Outlook & Guidance

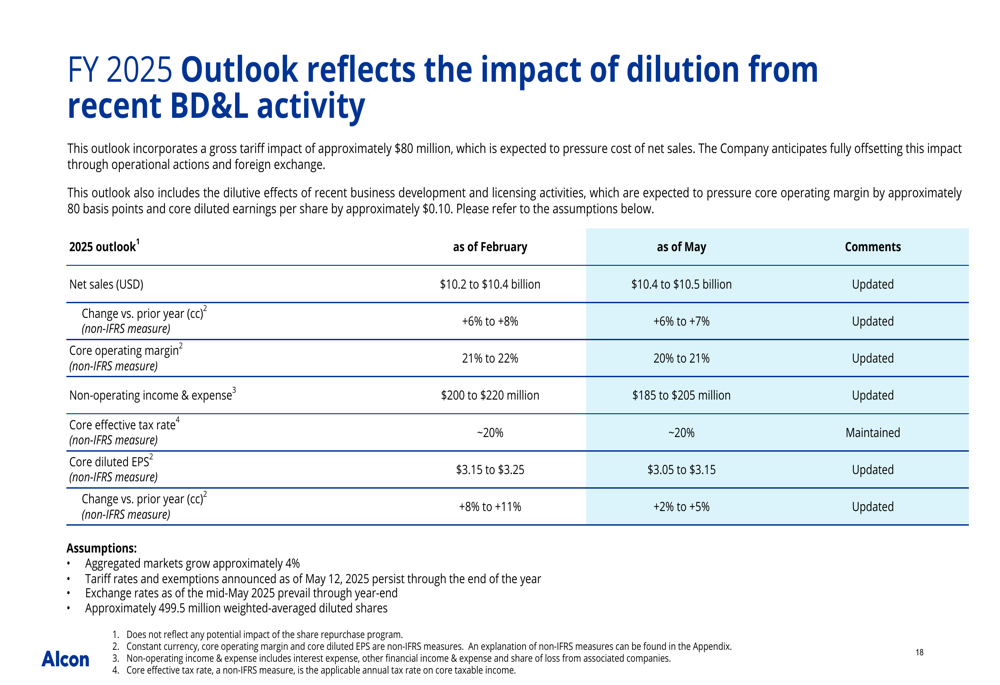

Alcon updated its full-year 2025 guidance, as shown in the following outlook table:

The company raised its net sales forecast to $10.4-10.5 billion (previously $10.2-10.4 billion), representing 6-7% growth in constant currency. However, Alcon lowered its core operating margin guidance to 20-21% from the previous 21-22% and reduced its core diluted EPS outlook to $3.05-3.15 from $3.15-3.25.

These adjustments reflect approximately $80 million in gross tariff impacts expected to pressure cost of net sales, though the company anticipates fully offsetting this through operational actions and foreign exchange benefits. Additionally, recent business development and licensing activities are expected to dilute core operating margin by approximately 80 basis points and core diluted EPS by approximately $0.10.

The updated guidance assumes aggregate market growth of approximately 4%, persistence of current tariff rates and exemptions through year-end, and approximately 499.5 million weighted-averaged diluted shares outstanding.

This first quarter performance and updated outlook suggest Alcon continues to navigate a complex global market environment, with strength in international markets and consumables helping to offset challenges in the U.S. surgical business and the impact of recent strategic investments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.