Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Alcon AG (NYSE:ALC) released its second quarter 2025 earnings presentation on August 20, highlighting moderate growth and a major strategic acquisition. The global eye care leader reported net sales of $2.6 billion, up 4% year-over-year (3% in constant currency), while announcing a $1.5 billion acquisition of STAAR Surgical (NASDAQ:STAA) to strengthen its position in the myopia market.

The company’s stock responded positively to the announcement, with shares rising 2.26% to close at $88.13 before the earnings release, and gaining an additional 0.99% in after-hours trading.

Quarterly Performance Highlights

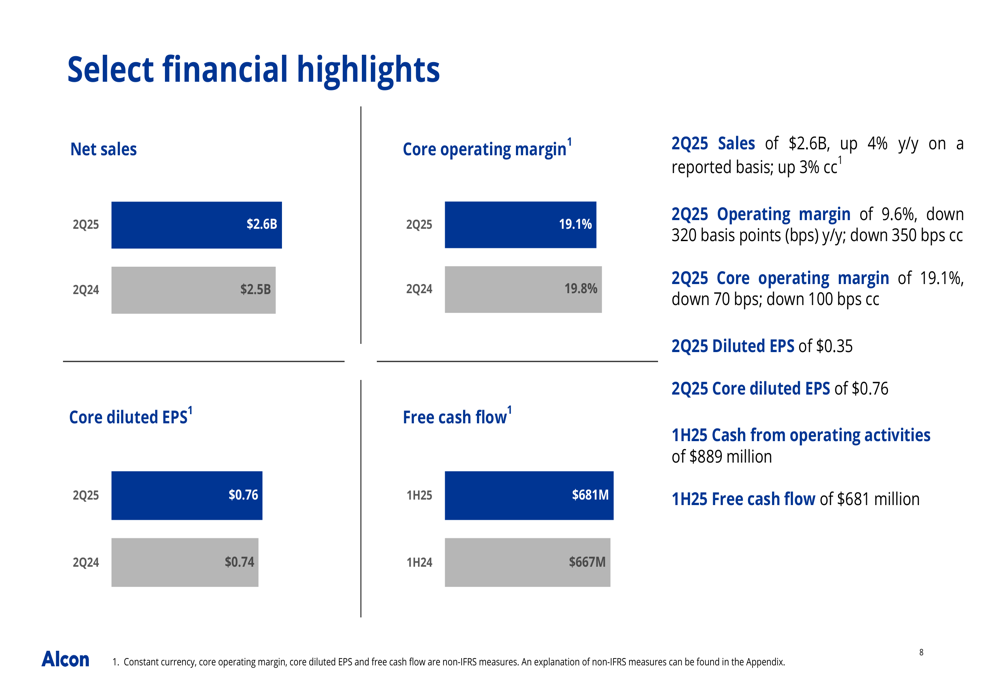

Alcon’s Q2 2025 performance showed mixed results across its business segments. Overall net sales reached $2.6 billion, with core operating margin at 19.1%, down 70 basis points year-over-year. Core diluted EPS was $0.76, while free cash flow remained strong at $681 million.

As shown in the following financial highlights chart:

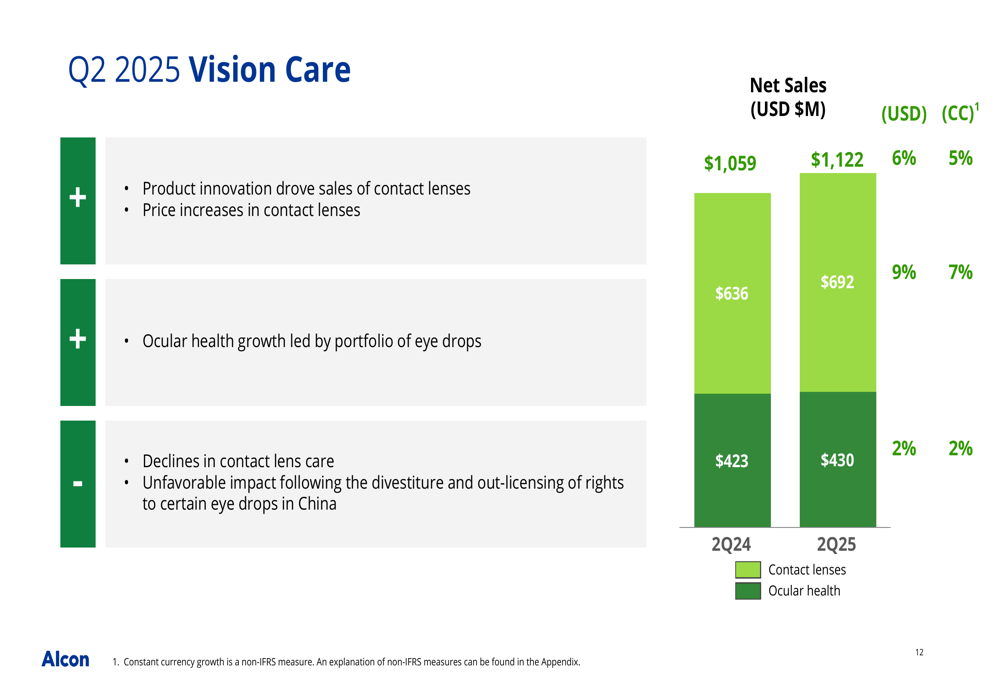

The company’s Vision Care segment outperformed Surgical, with Vision Care sales reaching $1,122 million, up 6% (5% in constant currency). This growth was primarily driven by product innovation in contact lenses and strong performance in the eye drop portfolio.

The detailed breakdown of Vision Care sales performance reveals:

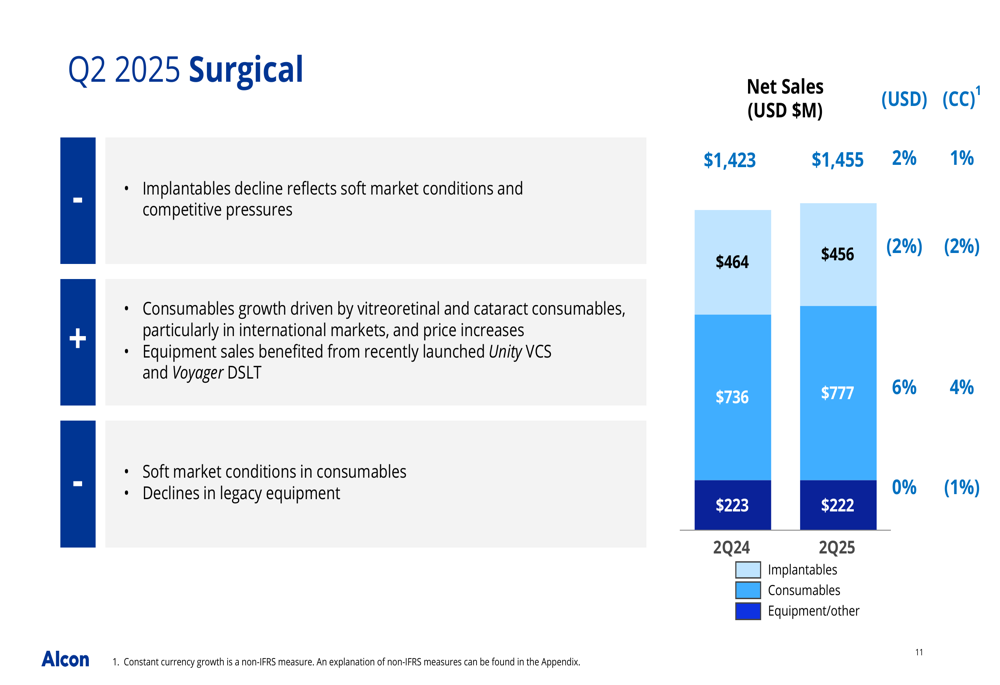

Meanwhile, Surgical sales grew more modestly at $1,455 million, up 2% (1% in constant currency), with implantables facing headwinds from soft market conditions and competitive pressures. However, consumables showed growth driven by vitreoretinal and cataract products.

The Surgical segment performance is illustrated in this chart:

Strategic Initiatives

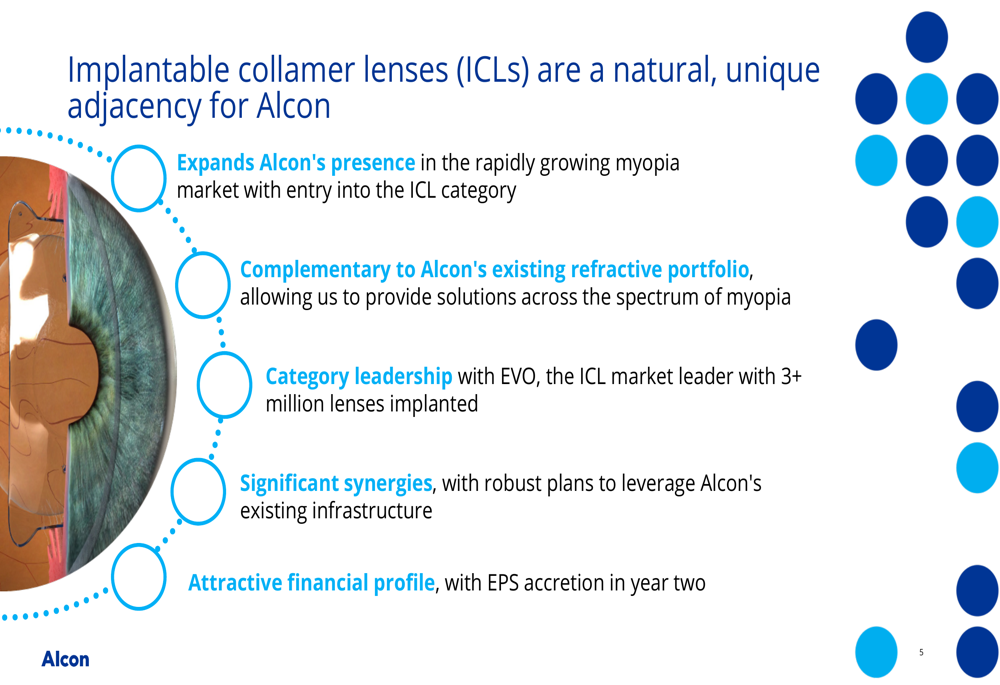

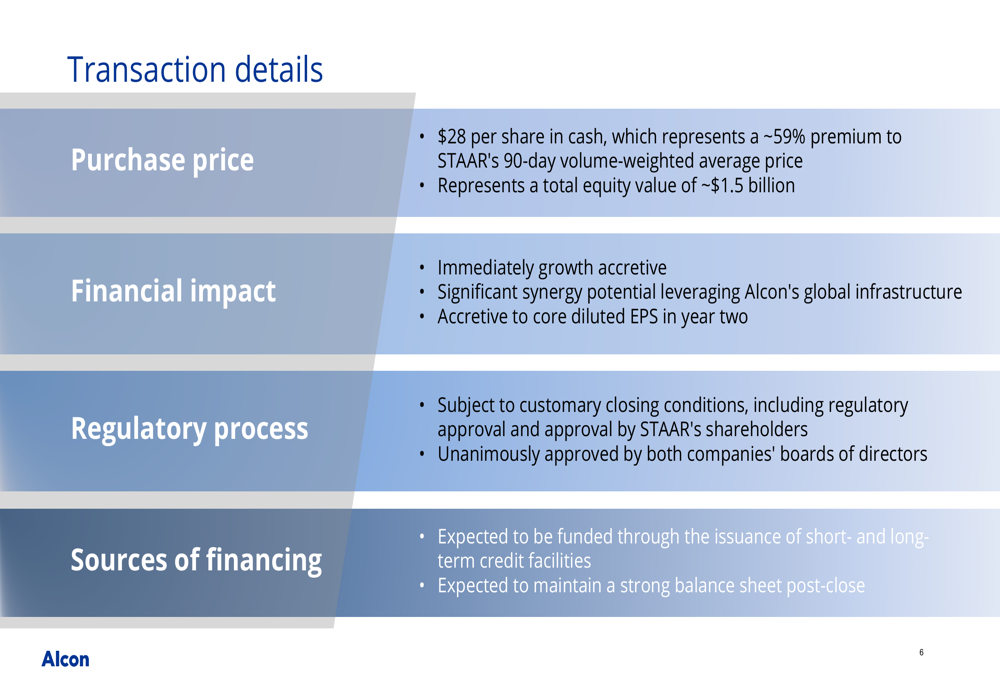

The headline announcement was Alcon’s acquisition of STAAR Surgical, a leader in implantable collamer lenses (ICLs) for myopia correction. The $28 per share all-cash transaction represents a 59% premium to STAAR’s 90-day volume-weighted average price, with a total equity value of approximately $1.5 billion.

The strategic rationale for this significant acquisition is detailed in the following slide:

Alcon expects the transaction to be immediately growth accretive and to contribute positively to core diluted EPS by the second year. The acquisition will expand Alcon’s presence in the growing myopia market and complement its existing refractive portfolio.

The transaction details and financing structure are outlined here:

Detailed Financial Analysis

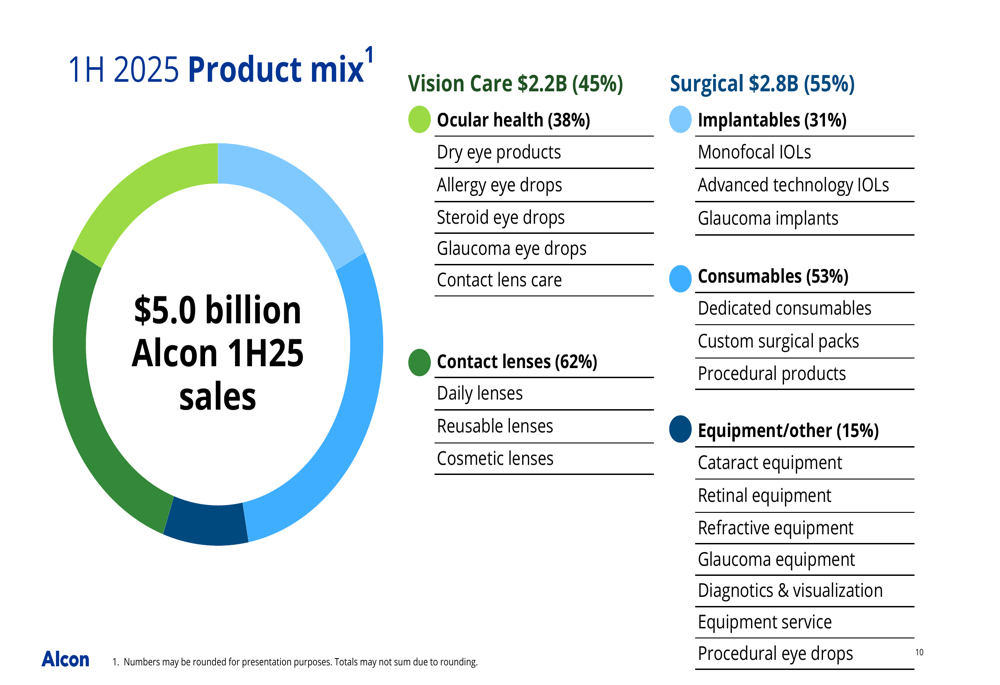

For the first half of 2025, Alcon reported total sales of $5.0 billion, with Vision Care accounting for 45% ($2.2 billion) and Surgical contributing 55% ($2.8 billion). Within these segments, Contact lenses represented 62% of Vision Care sales, while Consumables made up 53% of Surgical sales.

The company’s product mix is visualized in this chart:

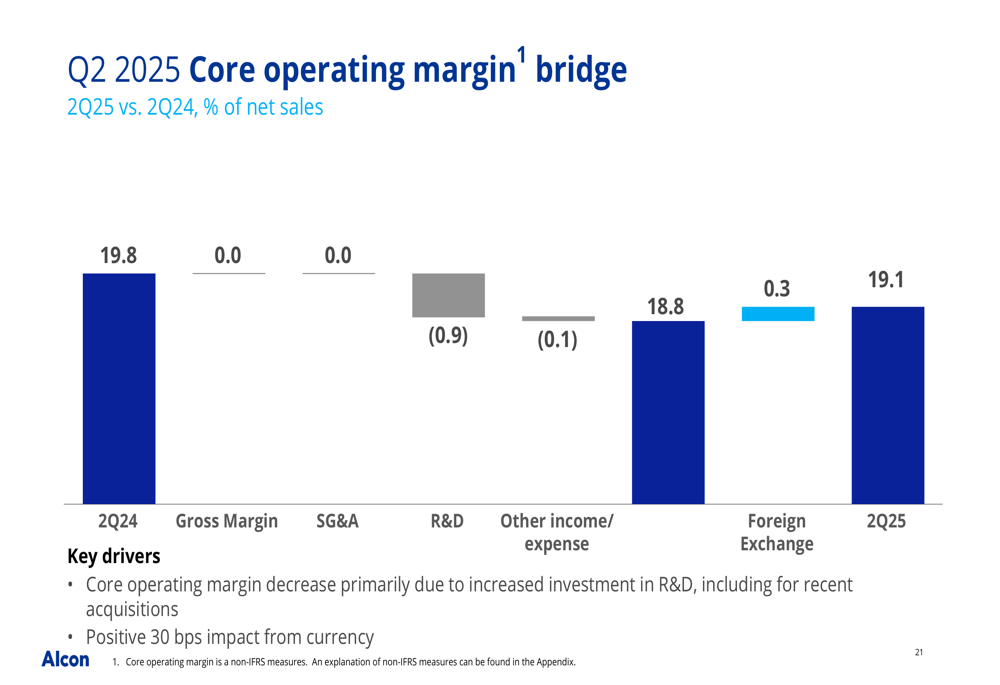

On the profitability front, Alcon’s core operating margin declined by 100 basis points in Q2 2025, primarily due to increased R&D investment. The margin bridge shows no change in gross margin and SG&A, with R&D accounting for a 0.9 percentage point decrease:

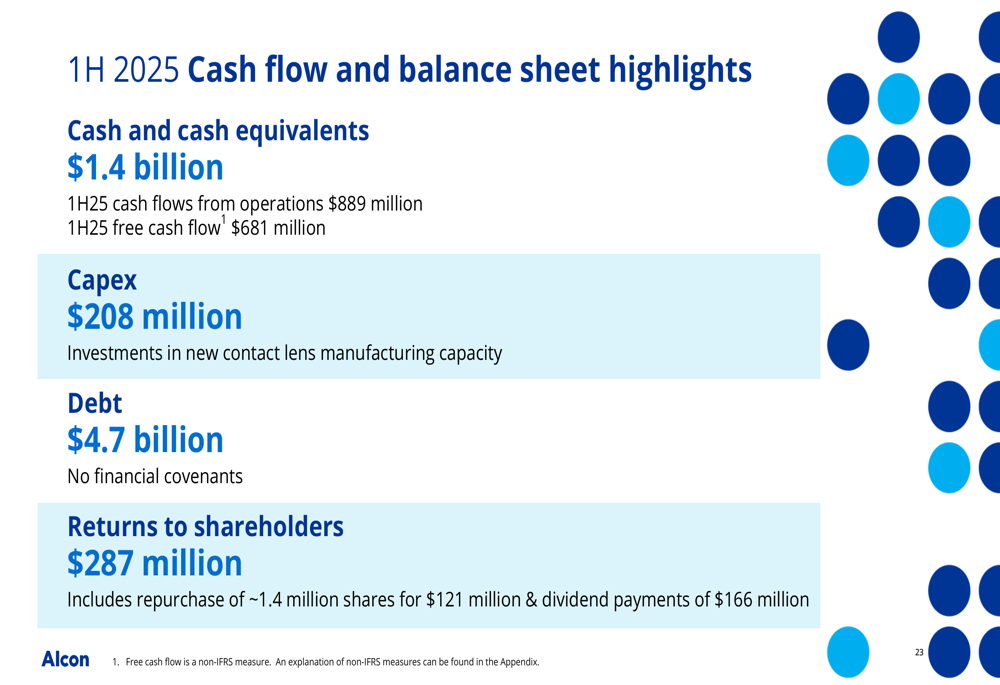

Cash flow and balance sheet metrics remained solid, with cash and cash equivalents of $1.4 billion and debt of $4.7 billion. The company returned $287 million to shareholders in the first half of 2025, while investing $208 million in capital expenditures, primarily for new contact lens manufacturing capacity.

Forward-Looking Statements

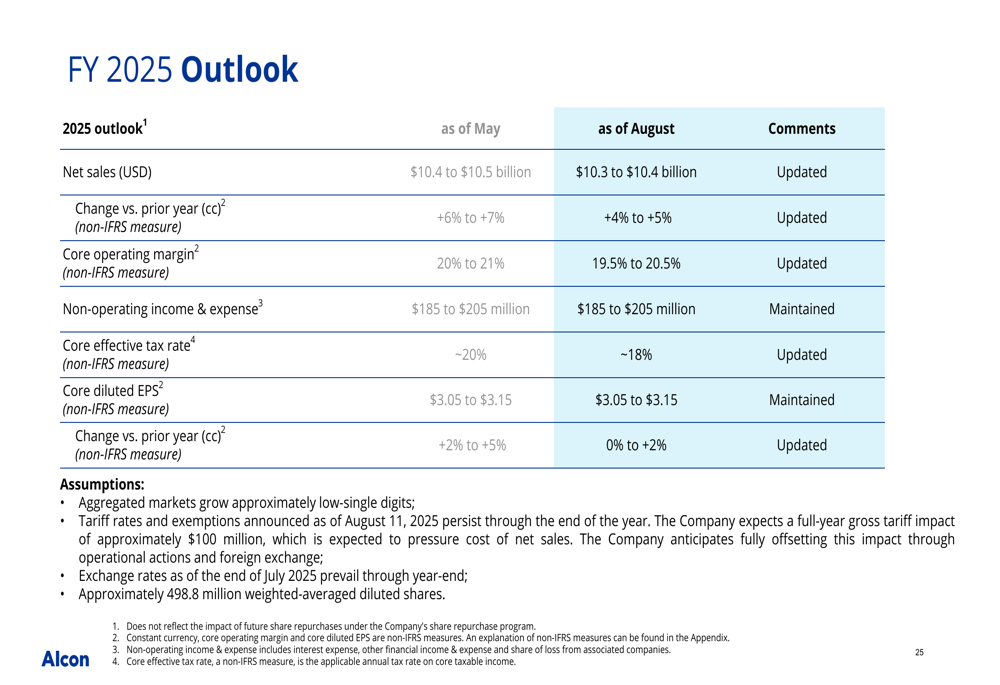

In light of current market conditions, Alcon revised its full-year 2025 guidance downward. The company now expects net sales of $10.3-10.4 billion (previously $10.4-10.5 billion), representing 4-5% growth in constant currency (down from 6-7% previously). Core operating margin guidance was also lowered to 19.5-20.5% from 20-21%.

Despite these reductions, Alcon maintained its core diluted EPS guidance of $3.05-3.15, helped by a lower expected core effective tax rate of approximately 18% (down from 20%).

The updated outlook is detailed in this comparative table:

Competitive Industry Position

Alcon’s Q2 2025 results reflect both opportunities and challenges in the eye care market. While the company continues to benefit from innovation in contact lenses and eye drops, it faces increasing competitive pressures in the surgical implantables segment.

The acquisition of STAAR Surgical represents a strategic move to strengthen Alcon’s position in the refractive surgery market, particularly for myopia correction. With over 3 million EVO implantable collamer lenses already implanted globally, this acquisition gives Alcon leadership in an important and growing category.

This strategic positioning comes at a time when the company appears to be experiencing some slowdown compared to previous quarters. In Q3 2024, Alcon reported 6% sales growth and a core operating margin of 20.6%, compared to the 4% growth and 19.1% margin in the current quarter.

The company’s increased R&D investment, while pressuring margins in the short term, signals a commitment to future innovation and growth. However, the downward revision in full-year guidance suggests that Alcon is navigating some headwinds in its core markets, particularly in the surgical segment.

As Alcon integrates STAAR Surgical and continues to invest in innovation, investors will be watching closely to see if these strategic initiatives can offset the current market challenges and deliver the projected financial benefits in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.